Good morning … well, today marks the beginning of front-end supply (2s, 5s and 7s) …

2yy DAILY: uptrend (noted) in tact BUT … momentum (stochastics, bottom panel) remain overSOLD … awaiting a catalyst

2yy WEEKLY: 2024 trend remains in place and nearly back to the magical “5.00%” which (too?)many deem a buying opportunity and here, too, momentum is now stretched into overSOLD territory

… Ultimately, the Fed is in charge here and while yesterdays markets made stock jockeys feel somewhat less bad, one day in a row does not a pattern make. And with the Fed in charge (and in their #Blackout period), we’ll be waiting for some sort of catalyst to arrive … perhaps some good news from the Middle East …

… Adding to the positive sentiment were growing hopes that a further escalation in the Middle East would be avoided, and Brent crude oil prices (-0.33%) fell back to their lowest level so far this month, at $87.00/bbl…Indeed, yesterday saw Iran’s foreign ministry spokesman say that Israel had received the “necessary response at this stage”. The apparent easing in tensions helped oil prices fall back, and there was also a sharp move lower in gold (-2.59%), which had its biggest daily decline since June 2021. It's down another -0.90% this morning… -DBs Early Morning Reid (4/23/24)

Unsure of the what next allows me then to quit while I’m behind … here is a snapshot OF USTs as of 706a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower this morning as global PMI numbers showed that April was a pretty decent month for global economic activity. DXY is UNCHD while front WTI futures are little changed too. Asian stocks were mixed, EU and UK share markets are all higher (SX5E +0.95%) while ES futures are showing +0.25% here at 6:30am. Our overnight US rates flows saw real$ buying in the long-end during Asian hours. During London's AM hours, flows were skewed toward better real$ buying in the belly (3's to 7's) as prices came off amid the PMI data. Overnight Treasury volume was ~75% of average overall with 2's (114%) seeing some relatively high average turnover overnight.

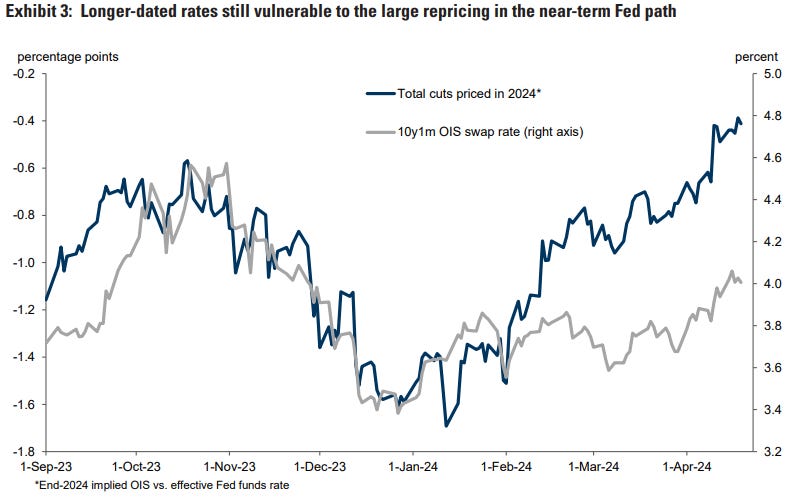

… You've seen this weekly chart of the 1y1y swap rate many times recently and we post it again to illustrate why front-end rates are holding supports well (see 2's at their 4.98% to 5.00% support area) despite the data and recent Fed rhetoric. A Friday close >4.57% in 1y1y would certainly grab our attention as it would confirm that the 'barrier of demand' at the level has likely been fully sated. Until then, 4.57% is your super major support in 1y1y.

… #Got2s? … and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures tentative ahead of a busy earnings slate, Bonds flat but pressured post EZ PMIs, XAU dips; US PMIs due … USTs initially remained in overnight ranges but succumbed to modest selling pressure following EZ PMIs … USTs initially remained in overnight ranges, though succumbed to selling pressure, sparked by EZ-PMIs, which dragged EGBs lower. USTs matched yesterday's 107.31 high earlier in the session before pulling back to circa 107.25, and further downside could bring Monday's 107.17 low into view.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

ABNAmro: Oil prices settle on signs of de-escalation

Crude prices have remained on an upward trend and witnessed a price surge beyond the 90$/b level driven by a supply deficit and more importantly the escalation of geopolitical risks. Meanwhile, the IEA revisited its oil demand growth forecasts downwards for 2024 and 2025 citing a higher speed of EVs adoption in advanced economies as a main driver. The market’s bullish sentiment was fuelled by fears that conflict between Israel and Iran would escalate in to a full-blown war, which could damage Iran’s oil supply capacity . Subsequent signs of de-escalation have seen the risk premium in oil prices diminish and confirmation of this could see Brent oil prices trending around 85 $/b.

It may not be saying a lot, but markets had their best performance in some time yesterday, as investors became a bit more optimistic about the near-term outlook. Equities recovered, and the S&P 500 (+0.87%) finally managed to advance after a run of 6 consecutive declines. Adding to the positive sentiment were growing hopes that a further escalation in the Middle East would be avoided, and Brent crude oil prices (-0.33%) fell back to their lowest level so far this month, at $87.00/bbl…

… Henry did a piece yesterday (link here) looking at what happens next after the S&P 500 has seen 6 consecutive declines as we saw before last night's positive close. The subsequent 1-month and 6-month performances have mostly been positive in recent history. Moreover, if the S&P had posted a 7th consecutive decline yesterday, that would have taken us into unusual territory, as it’s something we haven’t seen since February 2020 as Covid-19 spread globally. Indeed, the examples of 7 consecutive losses for the S&P 500 (in the 21st century at least) have either been during a crisis (GFC, US debt ceiling crisis, Euro Crisis, Covid-19) or in anticipation of a pivotal event with significant uncertainty (2016 US election).

As discussed at the top, sentiment was bolstered by the lack of any further escalation in the Middle East. Indeed, yesterday saw Iran’s foreign ministry spokesman say that Israel had received the “necessary response at this stage”. The apparent easing in tensions helped oil prices fall back, and there was also a sharp move lower in gold (-2.59%), which had its biggest daily decline since June 2021. It's down another -0.90% this morning.

The more positive tone was evident across sovereign bonds too. They were supported by the drop in oil prices, which added to hopes that any spike in inflation would prove temporary, and the 1yr US inflation swap (-1.2bps) fell back for a 4th session to 2.71%. In turn, that meant investors grew a bit more hopeful about the prospect of rate cuts, and the amount of Fed rate cuts priced by the December meeting (+1.2bps) inched up to 40bps. Similarly at the ECB, the number of rate cuts priced by December’s meeting (+4.2bps) rose to 78bps…

Goldilocks: Global Market Views: Paradise Postponed

A trickier form of US exceptionalism. Of the two potential shifts in the risk picture we highlighted some weeks ago—a broadening in global growth and some calming of inflation fear—the first has occurred, and the second has not. Continued inflation strength in the US has added to the upward pressure on US rates from firm growth and forced markets to reconsider the distribution of potential Fed outcomes to include the chances of no, or minimal, easing. The broadening of the global growth impulse over the last couple of months initially allowed a further broadening out of equity market and cyclical asset performance—and while it reinforced upward pressure on yields, it also limited USD strength. As the focus has turned to stickier US inflation—and tighter “real” policy—this has provided the first real challenge to equity markets in nearly 6 months, while also accentuating US “exceptionalism” and finally igniting “divergence” themes between the US and other major economies. With geopolitical risks also now firmly in focus, the setup for the risk picture has become more complicated. Our view is that inflation relief has likely been delayed not destroyed, so we expect the more constructive equity backdrop to reemerge over time. But even after a sizable rates market adjustment, we think the market is still vulnerable to the risk that further sticky inflation news alongside a strong US economy leads markets to lose confidence in an extended easing cycle. And we think near-term catalysts to calm those fears are not yet clear. This leaves us looking for an opportunity ahead to press the long equity view harder again in the coming weeks, but still reluctant to engage in rates from the long side given strong nominal growth. We continue to expect wider US rate spreads against other DM economies and to like the protection offered by USD upside.

Shifting from "growth upgrade" to "policy shock"

Inflation roadbumps—third time unlucky? Some new cracks in the easing façade

The market has continued to reduce the Fed easing it expects in 2024. Although we are now clearly pricing below the two cuts in our central case, we still do not see a compelling story for long positions here yet. More recently, the market has started to challenge the easing priced beyond 2024 and longer-dated rate pricing. We pointed out in March that deeper forward pricing in rates was getting more vulnerable to doubts over a prolonged easing cycle. Although those rates have moved meaningfully higher, forward rate pricing is still well below the peaks of last October, even though the path for rates through 2024 and 2025 is higher. And we are still pricing nearly 90bp of Fed cuts beyond this year, which could be vulnerable if the market more seriously weights the risk of a more classic “mid-cycle adjustment” or “higher for even longer” period. We worry that the belly and longer-dated US rate pricing could still prove vulnerable even after the moves we have seen if the growth environment remains strong. Our confidence in non-US easing is higher and it now seems likely that several central banks (ECB, BoE, BoC) could cut ahead of the Fed. The market has—at long last—begun to pull apart the pricing of the different central banks, with US-EUR spreads widening sharply after a period of puzzling stability. Our bias is to believe that those divergence dynamics can extend, but the opportunities may now be clearer in places that have priced less easing (Canada, UK, Australia, NZ).

Broadening in cyclical story provides some offset Not fatal for equity bulls, but more near-term risks Living in a strong Dollar world Commodities—a more nuanced picture Out of the “ultra-cheap” volatility zone EM resilience questioned by rates, oil and political risks. Narrower path to a friendly baseline

Goldilocks US Economics Analyst: Shelter Inflation: A Longer Lag for OER (in other words, higher for longer…?)

… But our original model of the “catch-up effect” simplified the calculation by estimating a single gap for rent and owners’ equivalent rent (OER). However, methodological changes to OER since we introduced our approach have made it a more imprecise simplification, because the OER weight on the hotter single-family detached segment is now twice as large as it is for rent.

We therefore update our model to calculate the gap between rents for new and continuing tenants separately for rent and OER. While the gap appears to have mostly closed for rent, we estimate that there is still a 2pp gap for OER, as new tenant rents weighted for OER have outpaced new tenant rents weighted for rent by 3pp over the last four years…

…Our revised shelter inflation forecast, alongside an upward revision to our airfares forecast to reflect the continued rise in oil prices, implies that core PCE inflation will stand at 2.6% year-over-year in December 2024 (vs. 2.5% previously) and 2.1% in December 2025 (vs. 2.0% previously).

Goldilocks: Why Core PCE Inflation Rose in Q1 and Will Fall in the Rest of the Year: A Category-Level Perspective (so, not all is lost, lower on the way…?)

… Looking ahead, we expect the sequential pace of monthly core PCE to slow from +0.33% on average in Q1 to 0.18% on average over the rest of the year, mostly reflecting softer consumer electronics, financial services, and healthcare services inflation. Recent dollar strength should weigh on foreign travel prices going forward, and we expect housing to be an ongoing source of disinflationary pressure this year and next. Our forecast implies that the average monthly annualized pace of core PCE inflation will return to 2.2% over the next three quarters, leaving the year-on-year rate at 2.6% in December 2024.

UBS (Donovan): Is sentiment saying anything

… US sentiment adds to the unreliability of gut instinct with the bile of political partisanship—which raises even more problems in so polarizing a political climate. The Philly Fed survey is due today. There are also revisions to past retail sales numbers—which are interesting to economists, but sadly less exciting for trades in financial markets …

Wells Fargo: Treasury Refunding Preview: Taking a Breather

Summary

On May 1, the U.S. Treasury will complete its regular quarterly refunding process. The quarterly refunding is the standard process through which Treasury communicates any changes in its debt management policy.

The torrid pace at which Treasury has been ramping up its debt issuance over the past year looks set for a breather. The federal budget deficit has narrowed in fiscal year (FY) 2024 compared to FY 2023, led by strong revenue growth and roughly flat spending. Furthermore, the Federal Reserve appears poised to slow its pace of balance sheet runoff in the months ahead.

In our view, current Treasury security coupon auction sizes appear well-suited to meet Treasury's financing need, and as a result we do not expect any changes to auction sizes at Treasury's upcoming refunding announcement. One small exception is in Treasury-Inflation Protected Securities (TIPS), where Treasury likely will continue to initiate small auction size increases in order to keep TIPS' share of the Treasury market unchanged.

That said, net issuance of coupon securities will remain sizable due to past auction size increases. With Treasury notes and bonds doing the heavy lifting for government financing in the quarters ahead, we expect Treasury to lean much less heavily on issuance of Treasury bills. The stock of outstanding T-bills has increased from $4 trillion to $6 trillion over the past year, an enormous 50% increase. We project net T-bill issuance to be -$225 billion (i.e. $225 billion of paydowns) from March 31 through year-end.

Given our expectations, we would be surprised if the May 1 Treasury refunding announcement created fireworks in financial markets similar to what occurred in the second half of last year. Treasury seems well-positioned to meet its financing need for at least the remainder of the year.

That said, the 2024 U.S. presidential election is less than seven months away, and with it may come material changes in U.S. fiscal policy. Sooner or later, Treasury likely will need to ramp up its auction sizes once again to meet the deficit needs of the future, and markets may need to adjust. Stay tuned.

… Coupon Auction Sizes To Be Unchanged from May-July Against this backdrop, we do not expect the U.S. Treasury to increase coupon auction sizes at the upcoming Treasury refunding on May 1.2 In August 2023 in the face of a growing financing need, Treasury began increasing monthly auction sizes for its coupon-bearing securities. The increases were considerable and played a role in the selloff in longer-term Treasury securities that occurred last year (Figure 7). A more moderate round of increases at the November refunding coincided with the peak in longer-term yields, and Treasury repeated this round of increases at the January refunding. The steady drumbeat higher in auction sizes for Treasury securities has led to monthly issuance that has risen considerably over the past year. For example, the Treasury will auction $69 billion of two-year notes on April 23, a material increase from the $42 billion of two-year notes auctioned in April 2023.

…Conclusion: Probably No Major Market Moves from the May 1 Refunding Given our expectations, we would be surprised if the May 1 refunding announcement created fireworks in financial markets similar to what occurred in the second half of last year. Treasury seems well-positioned to meet its financing need for at least the remainder of the year. That said, the 2024 U.S. presidential election is less than seven months away, and with it may come material changes in U.S. fiscal policy. Sooner or later, Treasury likely will need to ramp up its auction sizes once again to meet the deficit needs of the future, and markets may need to adjust. Stay tuned.

… And from Global Wall Street inbox TO the WWW,

Kimble: Is A 500% Rally In Interest Rates Enough, Or Will Rates Continue Higher? (NOT a fan of the TNX reference but hey, when in Rome … where there are NO Bloombergs … will just go with it … then the math about the move in the price? hey, it’s math, right? rates of change?)

… Finally, on this day in 1973 …

April 23, 1979 Dear Saul

Here is a souvenir from our annual report. My sincere thanks for making it a success.