CNBC: Oil falls as Qatar, Pakistan announce 60-day roadmap for U.S.-Iran deal

CNBC: Trump threatens Iran with fresh strikes as Vance leads peace talks in Switzerland

Bloomberg: Treasuries Decline as Trump’s Iran Threats Stoke Inflation Fears

Investing.COM: BofA now sees no Fed rate cuts until 2028

Investing.com -- Bank of America has shifted its Federal Reserve outlook, now forecasting three interest rate hikes totaling 75 basis points this year before an extended pause, pushing any prospect of rate cuts well into the future.

… AND a few thoughts …

Deal on again / off again and markets reading back on again as negotiations progress.

Markets closed vs markets OPEN seems to be very much like THIS.

Yield curve flattening has been ‘dramatic’ in wake of recent FOMC meeting (BMOs words) and this (noted over weekend, HERE) remains topical into the week ahead.

There’s a limited data calendar and likely fair amount of Fedspeak. There will be plenty of supply ($69bb 2s TWOSday, $70bb 5s Wednesday and $44bb 7s Thursday) and you’ll find some longer-term WEEKLY visuals where momentum seems to suggests #DipOrTunities and 7s ALSO holding TLINE support.

#Got7s?

Once again having that feeling that I’m not adding anything to the day so I’ll lean on final bullet above — NOW as we digest the new FOMC boss (NOT the same as the old), Global Wall and markets pricing in HIKES, EARL lower and the yield curve throwing penalty flag…pop always said, timing is everything and seems to ME that timing here, as well as flow of news (and EARL) may be worth watching.

Especially IF we’re witnessing the removal of the ‘FLATION part of the StagFLATION narrative.

Clearly NOT a done deal and worth watching … on THAT note, so, too, is the long-end of the curve for any / all those looking to curve trade into / around all the supply this week …

30yy DAILY (bars): 5.125, 5.00 and 4.9375 (middle of 5.125 to 4.75 range, noted)

… momentum here seems ‘suspect’ (ie overBOT, crossing/ leaning / pointing towards higher yields)_ so I’d look towards #DipOrTunities ahead — 5.00, and previous cheaps - 5.125 ‘ish

#Got30s? … AND to the BondBot …

THE MONDAY SHRUG: HIGHER YIELDS, CALMER OIL, SAME OLD MACRO HANGOVER

Equity futures are tiptoeing into the week like nothing happened, oil is behaving itself as U.S.-Iran talks continue, and Treasury yields are quietly grinding higher—the market's way of reminding everyone that geopolitics may grab headlines, but rates still write the ending. The consensus trade remains the same tired script: no war, lower oil, easier inflation, Fed cuts eventually. Maybe. Meanwhile, the bond market is staring at deficits, supply, sticky services inflation, and a Fed that still looks more "wait and see" than "cut and pray." SpaceX is already drifting lower after the usual IPO-adjacent excitement, proving once again that gravity remains undefeated. The curve is steepening not because growth is booming, but because long-end investors are demanding a larger bribe to finance Washington's spending habits. Stocks see calm seas; bonds see storm clouds on the horizon. One market is sipping a piña colada, the other is quietly buying flood insurance. As always, somebody is wrong—and history suggests it's usually the crowd.

Punchline:The Middle East is behaving, oil isn’t spiking, stocks are relaxed, and yields are rising anyway. Welcome to 2026, where even the good news comes with a higher term premium.

… FINE BUT … the part about rate CUTS maybe needs a tweak. Thankfully this will go into his file when comes time to see if we’re going to put / keep him on retainer.

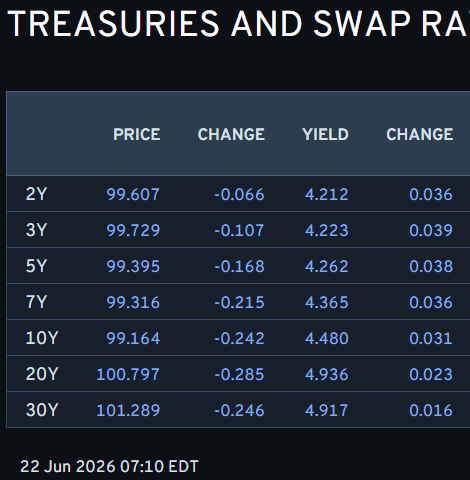

Onwards and upwards TO the reason many / most of you are likely here … whatever it may be on Global Wall’s mind but first … here is a snapshot OF USTs as of 710a:

… for somewhat MORE of the news you might be able to use … a few curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US indices quiet as energy trickles lower; GBP unreactive as UK PM steps down … Global fixed benchmarks are mixed; Gilts digest UK PM Starmer’s decision to resign … USTs lower as a function of catch-up from the holiday session on Friday, and as the complex acknowledged the gap higher in energy at the resumption of trade after Iran seemingly shut Hormuz transit amid ongoing conflict in Lebanon. However, the updates from negotiators thereafter and as technical talks take place this week in Switzerland, points that allowed energy to retreat and gave relief to EGBs. USTs look ahead to remarks from Fed’s Waller.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS of Global Wall you might be able to use …

New chair, NOW what … a few thoughts

June 22, 2026 MS Get Ready For the Noisiest US Front End In A Generation | US Rates Strategy

The toolkit the Fed uses determines the rates regime, and 36 years of data say the front end and the shape of the curve, not the level of yields, define it. A return to a short statement, little forward guidance, and a small balance sheet should bring back the noisiest front end in a generation.

Key takeaways

The level of yields does not separate the four Chairs in any clean way. Front-end volatility does, and it has fallen with every Chair since Greenspan took over.

Under Greenspan the front end was the curve’s engine, a 2-year move pulling the whole curve along. Under Yellen the front end sat still and the long end led.

We measure it directly. Correlation between 2-year moves and slope moves runs negative under Greenspan and positive under Yellen, near-perfect mirror images.

Curve-shape volatility tells the same story. Greenspan ran the highest curvature volatility of the four Chairs, and Yellen ran the lowest by a wide margin.

A Greenspan toolkit – short statement, little guidance, small balance sheet – means a noisier front end and a more volatile curve shape, even at a flat level.

…Front-end volatility works far better. We take the 3m yield, measure how much it moves over rolling 63-day windows, and annualize it (Exhibit 1). The data suggest that the front end was noisier under Greenspan, quieted through the crisis, went nearly silent under Yellen, and woke back up under Powell…

Exhibit 1: Front-end volatility: 3m par yield, daily changes, 63-day standard deviation, annualized

June 21, 2026 MS IDEA: Sunday Start | What’s Next in Global Macro: New Chair, New Chapter

…The market’s expectations for a rate hike this year were reinforced by the statement and Warsh’s press conference. The blunt statement that “[t]he Committee will deliver price stability” seems clear, but (again…by design) the path was not laid out. Before determining when the Fed will hike rates and by how much, consider the following. Chair Warsh did not write down his own projection for the policy rate. The median FOMC participant expects only one hike this year, but with the addition of that one dot, the median could have been no hikes.

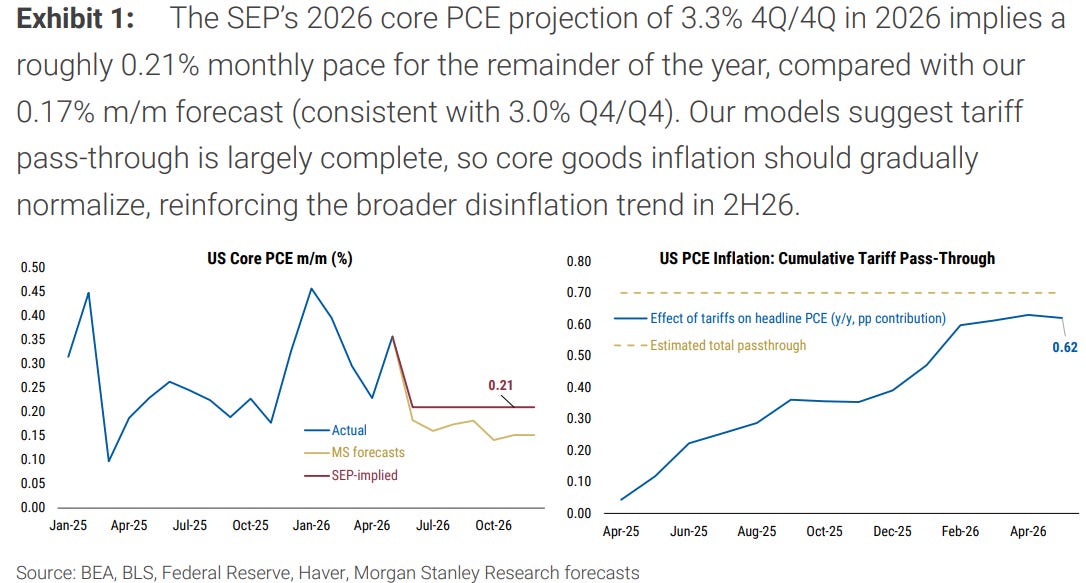

Moreover, that policy path was plotted alongside a forecast of 3.3% core inflation for 2026. But the boost to prices from tariffs is largely complete, so we expect notable disinflation for the remainder of the year. Oil prices are sharply lower, so the risk of “second-round” inflation from energy seems to have receded markedly. The FOMC’s inflation forecast is plausible, but not the most likely. If inflation materially undershoots, the fact that the median participant expected to cut rates next year presents a puzzle. Why hike rates only once if inflation undershoots and you expect to cut rates anyway? …

… How different will the Fed be a year from now? Very different, I suspect, in many aspects of the Chair’s communications. I also suspect the size of balance sheet could be very different. But when it comes to monetary policy through rates, I am less convinced the change will be as stark.

The US-Iran agreement and lower oil should ease inflation and support growth globally. Markets perceived the FOMC meeting as a hawkish shift, but if inflation undershoots the Fed’s forecasts, markets may have priced in too much tightening.

…We have to take the events together, though. Lower oil prices, if sustained, remove a lot of inflationary pressures in many economies. Greater chances of Fed hikes, however, means that other central banks may have to be more defensive. Previously, we have emphasized that a Fed hiking cycle driven by strong growth would have important global implications, particularly through financial conditions and the dollar. That narrative remains relevant, but the current environment adds an important layer. How much with the shift from the Fed sustain if inflation really does come down as we expect?

Our baseline view remains that the Fed will stay on hold this year, and we see the recent market repricing after Chairman Warsh’s first FOMC meeting as somewhat overdone. In particular, the median Fed forecast was for 3.3% core PCE inflation this year, well above our call for 3%. Tariff-related inflation is fading, and much lower oil prices mean “second-round effects” are unlikely. So the median FOMC participant who is looking to hike once this year but cut next year, would need to reconsider if inflation proves notably more tame than expected…

June 22, 2026 04:01 AM GMT MS Weekly Warm-up: Mixed Messages as Warsh Pushes for Fed Credibility

In February, we noted our view that Kevin Warsh was the right choice to fortify market credibility for the Fed, a critical element for the eventual success of the administration’s plan to grow out of the debt problem. The rally in S&P/Gold is supportive of that view as is last Wednesday’s FOMC meeting.

Short-Term Pain for Long-Term Gain...We continue to view the Warsh nomination and subsequent appointment as a market-stabilizing event even if it leads to some short-term turbulence. Following on from anotewe wrote in February, the roughly 40% rise in the S&P 500/Gold ratio since his nomination reinforces our view that markets are giving him the benefit of the doubt. Specifically, we think markets are signaling that Warsh can shake up the Fed, reduce reliance on the balance sheet as a policy tool, and help re-establish confidence in policy makers. Last Wednesday’s price action suggests that transition is off to a good start, but could be a bit messy for stocks in the short term alongside the initial reaction of a sharp bear flattening of the yield curve, a stronger dollar and weak precious metal prices.

Kevin Warsh’s First Fed Meeting Marked an Important Step Toward Restoring Credibility…

We See Liquidity, Rather than Rate Hikes, As the More Important Near-Term Risk for Equities...Balance-sheet support has already begun to fade with the RMP down 75% from peak. Treasury buybacks have been reduced, while lending growth is accelerating to fund a strong economy and capital spending. Net-net, we think liquidity conditions are tightening and may remain a headwind for stocks into July, especially if markets test the Fed’s newfound resolve. Peace negotiations with Iran are also likely to play a role in near-term price action, but longer term, we remain bearish on oil prices as this conflict likely drives new sources of supply out of a necessity for energy independence.

Ultimately, Earnings Remain the Primary Driver of this Bull Market…Our out of consensus view on the earnings recovery at the beginning of the year is no longer unique, but it’s still underappreciated in terms of the breadth and resilience of the data, and earnings are likely to exceed expectations for the full year. This growth has offset the multiple contraction YTD and will likely soften any further blows from tighter monetary policy or uncertainty due to less Fed guidance and/or market challenges of the new Chair.

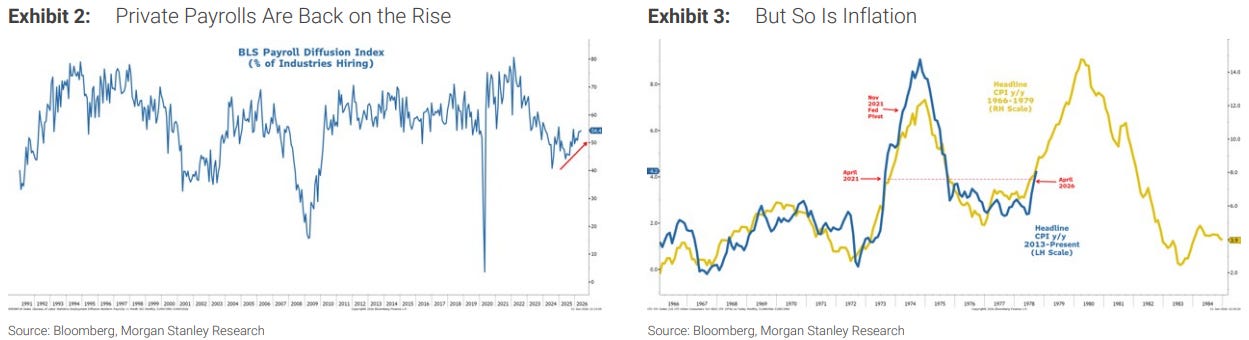

…In short, the Warsh nomination was the right choice if the goal is to fortify some questioned credibility for policy makers as evidenced by the moves in precious metals earlier this year and over the past decade. The improvement in the SPX/Gold ratio is a vote of confidence by markets, in our view. But now, the hard part begins—i.e., the new Chair must execute on that mission and deal with what is likely to be pressure from markets to test that resolve. Last week was a positive step in that direction, in our view. More specifically, Chair Warsh was crystal clear about the Fed's primary mandate—i.e., inflation, not labor markets/growth. Recent data on both employment and inflation support this position with private payrolls growing at their fastest pace in years due to the "rolling recovery" and policy changes (OBBBA, tax cuts, DOGE and immigration restrictions), and inflation still running well above target. He even called out the Fed for having missed its inflation target for the past 5 years, suggesting there is a new sheriff in town that will enforce that mandate.

…Bottom line, we believe last week’s Fed meeting set the stage for a new regime under which the Fed may be willing to take some short term pain in markets to establish a higher chance of success in its longer term goals to support the administration’s “Run it Hot” / rebalancing strategy. We commend this approach but wonder how it will react if markets test its resolve. It’s possible such a test may be forthcoming over the next few weeks as the rate of change on liquidity interacts with the rate of change peak in earnings revisions as discussed in last week’s note.

Finally, we’re not sure what to make of Thursday’s very positive rebound in stocks on the back of the US/Iran deal being signed only to be challenged again based on new headlines over the weekend.As of this writing, the talks are back on which could lead to either a continuation of Thursday’s rally or perhaps a sell the news on the premise this situation remains quite fluid.Longer term, we remain bearish on oil prices as this conflict simply highlighted how much excess oil and gas there is in the world and the resiliency of global energy markets. We also believe this conflict highlighted how unacceptable this choke point is going forward. We expect significant action to be taken by countries all over the world to ensure redundancies on oil supplies going forward which may include drilling activities in places thought to be off limits. We think this will keep the forward curve in check and could even act as a positive supply shock going forward that will help the Fed’s increased focus on inflation. See the latest views and oil forecasts from our commodities team here…

Is it right, wrong or ‘incoherent mkt bias’ to be positive on US / IRAN TALKS??

Thanks for reading The BondBeat! Subscribe for free to receive new posts and support my work.

22 Jun 2026 UBS: Sticking with the optimistic bias

There has been a heated exchange over the situation in the Gulf this weekend. However, US Vice President Vance is in Switzerland to talk with Iranian officials. There have been cautiously positive statements from Iran on the talks, and given market perceptions of the balance of power, that fact (plus the inherent market bias to optimism) has produced lower oil prices…

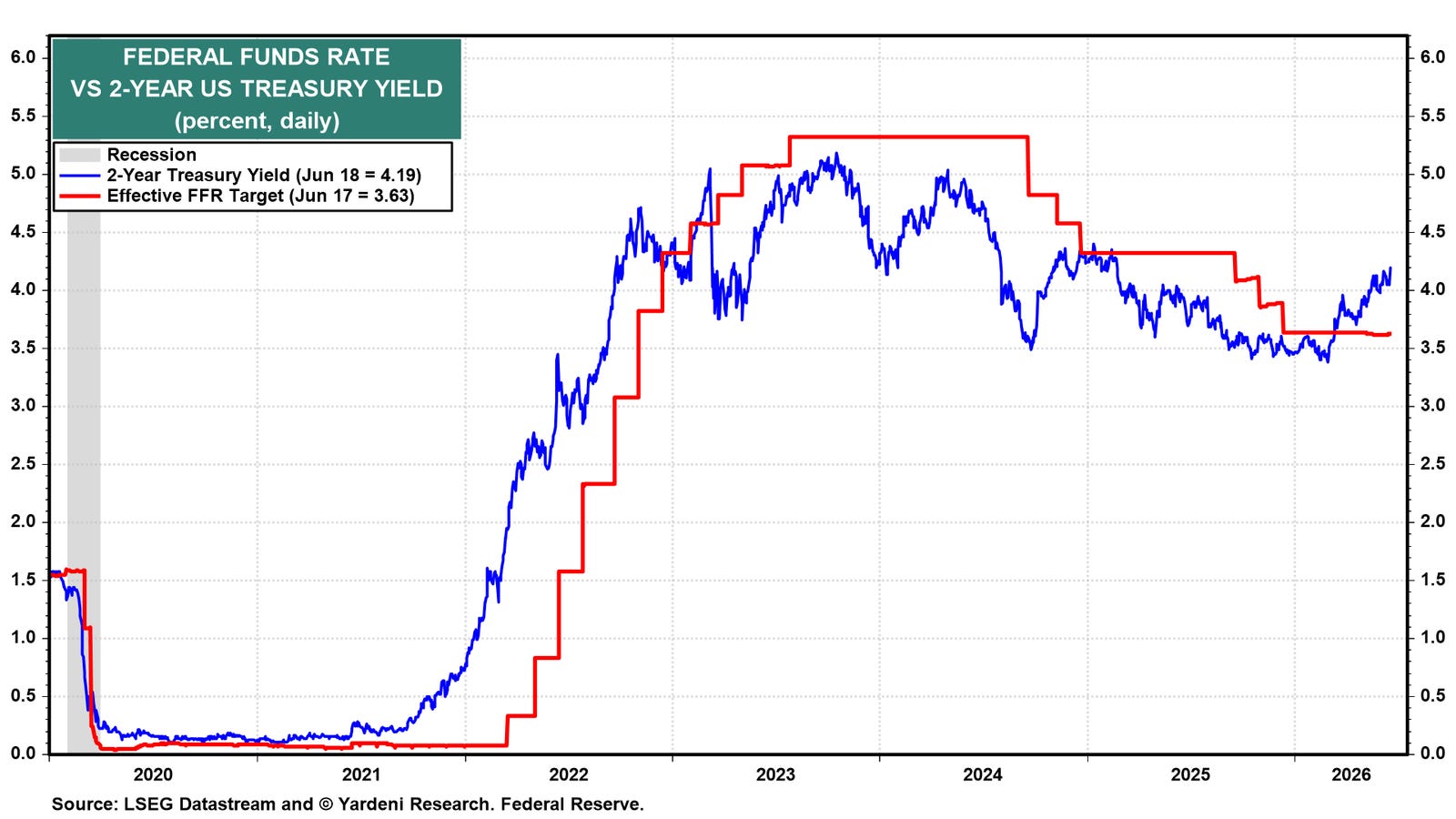

In the week just passed, the bar was set … here’s a look at the bar in context of 2s and FF …

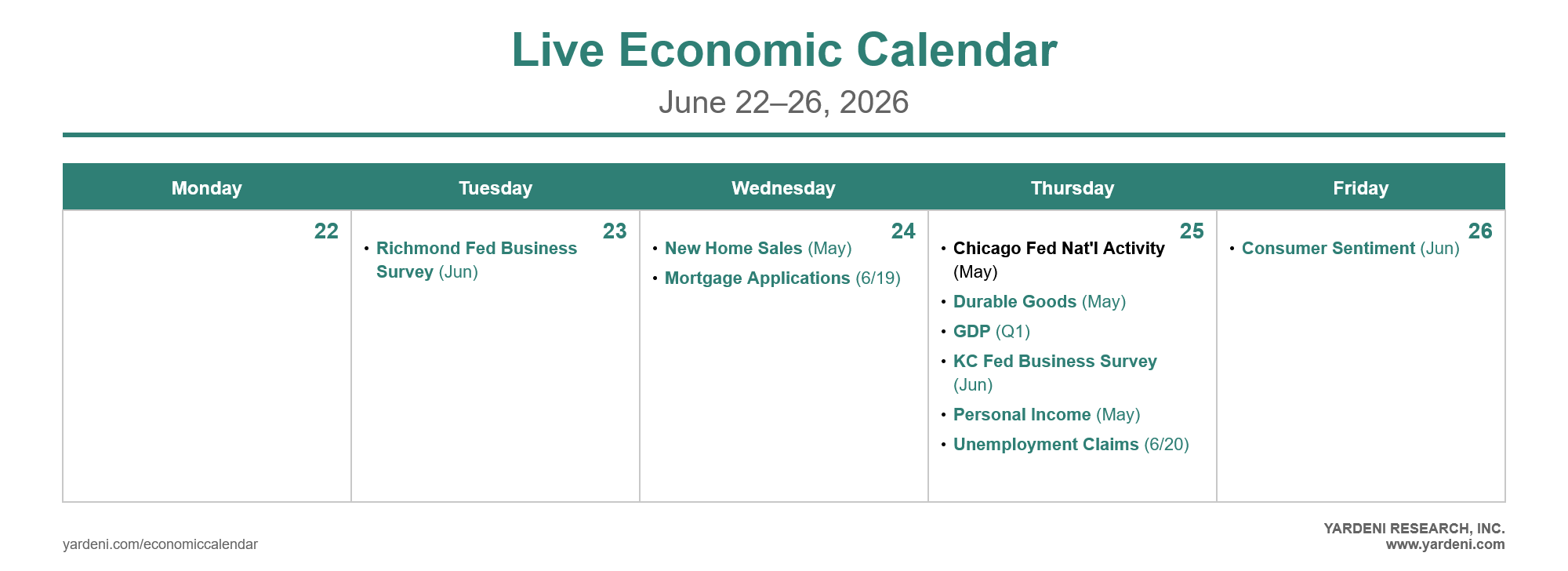

The US economic calendar is mostly quiet this week, but Thursday packs a heavy data load: final Q1-2026 GDP, May PCED, May durable goods orders, and weekly jobless claims…

…Wednesday’s FOMC meeting reset the bar. The June Summary of Economic Projections raised the median 2026 federal funds rate projection from 3.4% to 3.8% and the median 2026 core PCED inflation projection from 2.7% to 3.3%. Nine of 18 dots now pencil in hikes by year-end. The 2-year US Treasury note jumped to 4.19% in response (chart).

Warsh’s first press conference left no ambiguity. He called inflation “a choice,” insisted price stability is the FOMC’s number-one goal, and signaled the Fed will look through any supply-side disinflation from Iran. We continue to expect a first hike as soon as July. That expectation is more hawkish than the markets’, which put the odds of a hike in July at just 38% and one by September at 92%.

Here are the key economic releases most likely to shape investors’ thinking this week…

… Moving along TO a few other curated links from the intertubes. I HOPE you’ll find them as funTERtaining (dare I say useful) as I do … …

First up, the good Doctor SLOK over weekend noted …

June 20, 2026 Apollo: The Market Is Paying a Premium for Companies That Lose Money

Something is broken in price discovery when companies with negative earnings keep outperforming companies with positive earnings, see chart below.

Another great writer and a fella I’d call more than an aquaintance from The Terminal DOT COM …

Sun, June 21, 2026 at 2:03 PM EDT Bloomberg: Fed’s Favorite Gauge Is Seen Showing Faster Inflation

(Bloomberg) -- The latest update to the Federal Reserve’s favorite inflation gauge is unlikely to challenge a growing consensus at the US central bank around the need for interest-rate hikes this year.

… THAT is all for now. Off to the day job…

Thanks for reading The BondBeat! Subscribe for free to receive new posts and support my work.