while WE slept: USTs lean 'green' as Iranian leader to speak (?), Fed ahead; 'always rent dont own Earl' (DB); DB asks / answers who REALLY owns USTs (and ING weighs in, too); CUT bets on SOFR fly...

ReSale TALES did NOT disappoint. Whether bullish or bearish and regardless of whatever asset class … Top line, seasonally adjusted, and adjusting for inflation OR, if you rather, focusing in on the ‘Control Group’ (feeds into GDP and so, what the Fed watches), a recap of it all …

ZH: US Retail Sales Tumbled In May As Gas Prices Fell, Car-Buying Stalled

… The conclusion of ZH and most of what is ‘out there’ on Global Wall — below — is that the bad news is ‘Merica spending less and getting less for their dollar but the good news is GDP to be positively impacted in Q2 (unless, of course, you are an Atlanta Fed GDPNow devotee … that has been updated and decreased from 3.8% to 3.5% … )

… and ahead of this afternoons and the weeks featured events — The Fed — I thought a few words and a visual from Nick Colas / DATATREK far better use of your time and this space than my humble efforts and so …

Jun 17, 2025 Central Bank Gold Survey, Inflation Expectations, Retail Sales

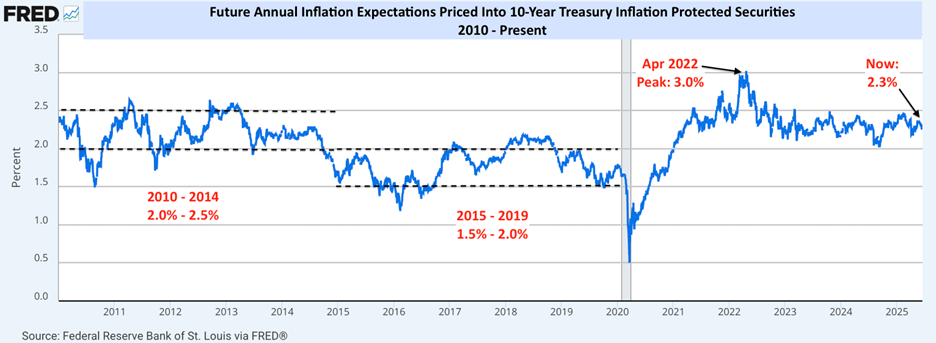

…Topic #2: A brief look at market-based inflation expectations ahead of tomorrow’s Fed Chair Powell press conference, as he always mentions this measure in his comments about future monetary policy. The following chart shows annual forward inflation expectations priced into 10-year Treasury Inflation Protected Securities (TIPS).

Takeaway: Longer-run forward Inflation expectations are currently 2.3 percent, which is much better than April 2022’s 3.0 pct, and back to the range from 2010 – 2014 (2.0 – 2.5 percent). As such, they are broadly supportive of the Fed’s current “wait and see” view on changes to policy rates. This level also reflects incremental confidence in the US economy versus 2015 – 2019, when inflation expectations ran in a band from 1.5 – 2.0 percent…

… With this little in mind ahead of the FOMC (and whatever other turn of events thrown our way), I’ll quit while I’m behind — nothing tomorrow as markets are closed — and be back in the inbox Friday but for now … here is a snapshot OF USTs as of 646a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Sentiment improves as US refrains from any Middle-East involvement, FOMC ahead .. USTs were exhibiting a modest bearish bias throughout the morning, given the improvement in the risk tone seen as the US is yet to get directly involved in the Iran-Israel conflict. However, this has been limited in nature with USTs only lower by at most 4+ ticks, and now has now edged just above the unchanged mark as broader peers rise. The upside seemingly stemming from a bit of a haven bid, amid reports that the Iranian Supreme leader is to speak shortly, via ISNA. The docket today is headlined by the FOMC, but before that May’s Building Permits/Housing Starts and Weekly Claims are due; latter expected at 245k (prev. 248k).

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … Think ReSale TALES recaps / victory laps along with a little bit more …

First up, an FOMC preview and a few words on conflict’s impact on rates, from ‘over there’ …

18 June 2025 ABN AMRO: FOMC Preview – It’s the data, not the sentiment

We expect the Fed to keep rates on hold today. Recent data has surprised in a dovish direction, but projections and the dot plot will shift more hawkish. The ‘hard’ data from the projections likely gives a better signal of the Fed’s rate trajectory than the ‘soft’ data from Powell’s press conference

18 June 2025 ABN AMRO: Impact of Israel-Iran on inflation and interest rates

Muted reaction so far of energy prices to Israel-Iran escalation - The escalating conflict between Israel and Iran has raised concerns over the last few days about potential disruption to global energy supply. As a result, a risk premium has been priced into oil prices, which has oscillated between 5 and 10 dollars p/b depending on the prospects for escalation versus de-escalation. The relatively muted reaction of prices reflects that the impact on energy supply has been limited so far. At the same time, outside of potential impacts of the conflict, supply is growing more quickly than demand and that is expected to remain the case this year and next…

…Impact on the US & Fed – We estimate inflation could increase by about 0.4-0.5pp in case Brent rises to $90, while a price of $140 would raise inflation by about 1.3pp. The growth impact would likely be limited. Like the rest of the world, the US dependency on oil has significantly decreased and inflation means that $100 oil is not as restrictive as it was a decade ago. In fact, higher oil prices may make Trump’s currently unviable ‘Drill, baby, drill’ plan a viable business case, partly compensating the drag on growth from higher oil prices.

While central banks typically try to see through the inflation impact from oil price changes – they are of course excluded from core inflation measures – this inflationary oil price shock comes on top of the tariff inflation shock, in a context where households are already expecting inflation to rise substantially. An increase in petrol prices would certainly bring an additional impulse to that. Our base case sees the Fed holding rates until the second quarter of 2026, due to higher inflation, a risk of inflation expectations de-anchoring, and a limited downturn in the labour market. An oil price shock would simply increase the amplitude of the path we already foresee, and is therefore unlikely to sway the Fed from this path…

Here’s a balanced review of the ReSale TALES data from across the pond …

Retail sales fell 0.9% m/m in May, led by declines in auto sales, food services, and building material stores. The control group bucked the trend, rising 0.4% m/m, led by strengthening of nonstore retailer sales. Overall, these mixed readings provide a slight boost to our GDP tracker.

…On net, the numbers boost our tracking estimate of Q2 GDP growth by 0.1pp, to 1.3% q/q saar, and our tracking of consumer spending by 0.2pp, to 1.9% q/q saar. However, implications are mixed across components, with the stronger-than-expected control group reading boosting our estimates for the PCE goods components, weaker food services marking down our estimates for PCE services, and declines in building materials and supply stores weighing on our tracker for residential investment. The decline in the autos component had been reflected in our tracking since May auto sales were reported earlier this month, and has no direct relevance for GDP tracking…

…Today's retail sales estimates boosted our tracker by 0.1pp relative to where it had stood at the close of last week, to 1.3% q/q saar. The boost to consumer spending on (non-auto) goods from the stronger-than-anticipated control group reading was partially offset by the drag from weak food services. Weak spending at building material and supply stores, which factor into the "improvements" category of residential investment, also provided an offset. Meanwhile, separate estimates of import and export prices did not influence our trackers for these two trade components, pending next week's advance estimates nominal goods trade in May.

Best in the biz on ReSale Tales (and a closing recap / commentary) …

June 17, 2025 BMO: Retail Sales Disappoint, Import Prices Unchanged

Retail Sales in May slipped -0.9% MoM vs. -0.1% prior and -0.6% forecasted. Ex-auto/gas, the move was -0.1% MoM vs. +0.1% April and +0.3% consensus. There was strength in the Control Group, however, at +0.4% vs. -0.1% prior and +0.3% anticipated. The 3-month average annualized pace for control-group sales slipped to 4.1% from 4.8% in April, but remains above March's 3.7%. Import prices in May were unchanged, which was an improvement versus the -0.2% forecast and +0.1% in April, bringing the YoY pace to +0.2% vs. +0.1% prior and 0.0% expected. Import Prices ex-petro gained +0.2% vs. +0.4% prior and +0.1% consensus. Overall, it was a mixed set of data that has been met by a muted response in the US rates market…

… Treasuries rallied on Tuesday amid a mixed round of economic data and growing geopolitical concerns focused on the Israel/Iran conflict. Retail sales and Industrial Production disappointed in May. On the other hand, Import Prices were firmer-than-anticipated, and control-group sales came in at +0.4% in May versus the +0.3% consensus – marginally better for the spending outlook. Investors continue to debate the relevance of the realized data in light of the potential ramifications from the trade war. We’re wary of downplaying the trajectory of the real economy, monetary policy, and geopolitics at the moment for several reasons. First, the pre-tariff departure point for inflation will be key in determining the extent to which the 2022 extremes are revisited. Our base case is that the impact of the new tariff structure will most certainly bring core-PCE off the current low of 2.5% but fall far short of the 5.6% peak from 2022. In this context, tomorrow’s updated SEP will be particularly informative as it will reflect the Fed’s current assessment of the tariff fallout. Further conflict in the Middle East will lead to energy inflation, but it’s unlikely to trickle into core …

… When combined with today’s selloff in risk assets and flight-to-quality flows, it appears that Treasuries’ safe haven status is back (for one session at least) …

An interesting / funTERtaining chart, as always, from fan favorite German bank stratEgerist out suggesting rent rather than own Earl …

17 June 2025 DB CoTD: Always rent rather than buy oil.

As a lover of long-term data, Oil has always fascinated me as over the long run it’s never been able to compete with financial assets as an investment. As an example, in my last annual long-term study (link here), we showed that over the last 150 years, oil has provided a real return of ‘only’ +0.5% p.a.. US equities are at +6.58% p.a. and 10yr USTs (and equivalents) are at +1.84%. Interestingly Gold is only at +0.77% over the same period. However copper (-0.56% p.a.) and wheat (-1.10% p.a.) are even lower…

…oil can have major implications for markets and economies over several months or years, but don’t expect it to deviate too much from inflation over the long run, especially when its price is as close to the long-run average as it is currently.

… Speaking of German bank strategists and their charts …

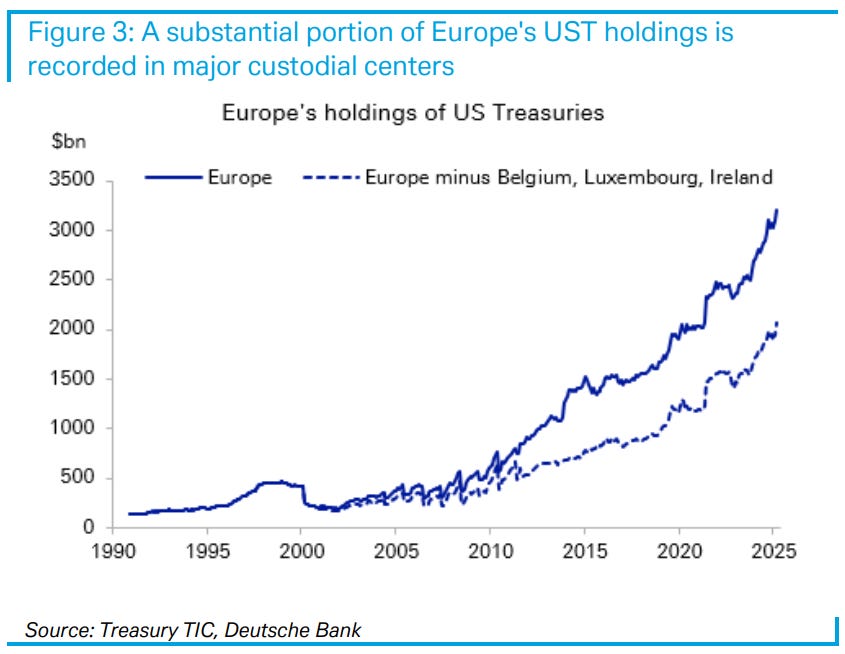

17 June 2025 DB: Who really owns U.S. Treasuries? Adjusting for custodial bias in the data

In this note, we attempt to adjust foreign holdings of U.S. Treasuries to correct for custodial bias in the Treasury TIC data. Using the ECB's fund reallocation framework and AI-assisted analysis, we reassign holdings from custodial centers such as Luxembourg and Ireland to their likely beneficial owners. Our results suggest that Europe's exposure to U.S. Treasuries may be overstated, while Asia and rest of the world's exposures are likely understated. Additionally, U.S. hedge funds and multinational firms operating through tax havens suggests that some Treasuries classified as foreign held may in fact be owned by U.S. entities, leading to a higher reported level of foreign ownership.

…1. Europe's reported holdings are likely overstated: A substantial portion of European custody-based holdings (e.g. in Luxembourg, Belgium, Ireland) belong to non-European investors, including U.S. entities. We estimate that one-third or more of European UST holdings may ultimately belong to non-Euro Area investors.

From this same shop is an early morning read setting the table for today’s FOMC meeting …

… Whilst the Middle East is the main focus for markets right now, today will also see the Fed announce their latest policy decision. A lot has happened since their last meeting in early May, including the dialling back of China tariffs, the Moody’s downgrade of the US credit rating, as well as the significant escalation in the Middle East. So given that uncertainty and the potential for fresh inflationary spikes, they’re widely expected to keep rates on hold again, and it means the focus will be on the dot plot for where they expect rates to go next. Our US economists think it’ll only signal one rate cut this year, which would be a hawkish shift from March, when they still signalled two cuts. However, they think it’s a close call, and they expect the Fed to mostly maintain existing signals about policy. For more info, see their full preview here …

See / say whatever you want and this next note / headline focusing on the ReSale TALES decline in REAL (ie inflation adjusted terms) and resonates with me …

June 17, 2025 First Trust: Retail Sales Declined 0.9% in May

Retail sales declined 0.9% in May (-1.2% including revisions to prior months), lagging the consensus expected -0.6%. Retail sales are up 3.3% versus a year ago.

Sales excluding autos declined 0.3% in May (-0.5% including revisions to prior months), versus the consensus expected +0.2%. These sales are up 3.5% in the past year.

The largest declines in May were for autos, building materials, and gas stations. The largest increase was at nonstore retailers (internet and mail-order).

Sales excluding autos, building materials, and gas rose 0.1% in May. If unchanged in June, these sales will be up at a 1.0% annual rate in Q2 versus the Q1 average.

Implications: … Strip out these three categories and you get “core” sales, which ticked up 0.1% in May. These sales are up 5.0% in the past year but have been slowing in 2025: up at a 3.3% annualized rate through May (which includes the bump from tariff front-running). This underscores the deeper issue at hand for the economy: monetary policy tight enough to bring inflation down is also tight enough to bring growth down …

… Looking at the big picture, retail sales are up 3.3% on a yearto-year basis and sit just below all-time highs. However, “real” inflation-adjusted retail sales are up 0.9% in the past year and are still down from the peak in early 2021. This highlights the ugly ramifications of inflation: consumers are paying higher prices today but taking home fewer goods than they were four years ago. Going forward, we expect retail sales to remain choppy as consumers respond to the global trade reordering currently underway. In other recent news, the Empire State Index, which measures manufacturing sentiment in the New York region, declined to -16.0 in June from -9.2 in May. On the trade front, import prices were unchanged in May while export prices declined 0.9%. In the past year, import prices are up 0.2% while export prices are up 1.7%.

Amsterdam suggesting ReSale Tales highlights caution … certainly one way to view the data and more than fair … and also an FOMC precap along with update on the sell / buy ‘Merica trade (in as far as recent TICS data) …

17 June 2025 ING: US retail sales highlights consumer caution

US retail sales have fallen for two consecutive months, unwinding most of the the pre-tariff spending splurge. Households are worried about what tariffs may mean for spending power and are increasingly cautious on the jobs market outlook. This points to an ongoing cooling in consumption

… The control group, which excludes volatile items such as gasoline, autos, food service and building materials wasn't as bad, posting a 0.4% MoM increase after a 0.1% decline in April. This metric has historically been more aligned with broader consumer trends, including services, and offers some hope that the second quarter won't be a write-off for consumer spending – note the chart below shows that retail sales accounts for only 42% of total consumer spending.

Retail sales as a % of total consumer spending

Consumer caution to weigh on growth In aggregate today’s report is disappointing since we have to remember that these are all nominal dollar growth rates. In price adjusted volume terms (which is what GDP is measured in) it paints a weak picture that reflects subdued consumer confidence readings. Households are nervous that tariff-induced price hikes will squeeze spending power while respondents have become much more cautious on job prospects and this suggests that consumer spending will continue to cool through this year.

Retail sales value versus volume

17 June 2025 ING Rates Spark: A Wednesday afternoon of drama from the US

It's Fed day. There lots going on and lots to mull over, but in the end not expected to amount to a whole lot. Still it's a big Wednesday. The Fed, of course. A 20yr auction (tailed last time). And the TIC data for April - see more on that here

17 June 2025 ING: So, how bad was the Sell America trade in April really

We panicked prior to the tariff pause in April as US Treasuries behaved like a risky asset under pressure. There was lots of speculation as to who was selling and how heavy it was. We'll know more soon. But as we get the data, remember that large dips negative in these data are typical. If we were to get that, we'd really need to see the May data before extrapolating

…But most other foreigners have in fact been decent net buyers of Treasuries

However, most other foreign holders have been net buyers. The chart below shows all other holders lumped together. They have accumulated a net $3trn over the same period.

Foreign net buying of Treasuries has dominated in the past decade Measured in $ billions, cumulative since 2015

Source: Macrobond, ING estimates

The other contextual aspect to be aware of is the heavier lift being undertaken by domestic investors. While foreigners have added some $2.5trn to holdings, domestics have added almost $9trn. Hence, domestic holdings have increased to 50% of total debt, while foreign holdings have fallen to 33% (the Federal Reserve holds the rest).

Domestics have been by far the biggest buyers of Treasuries Measured in $ billions, cumulative since 2015

Source: Macrobond, ING estimates

What to expect from the latest data, and how to interpret it

Now back to the latest readings. These data are quite volatile, so to make some sense of it we look at multi-month periods. An obvious starting point is to look at what has happened so far in 2025. In the first quarter there has been net buying across the board (with the exception of the Fed). See chart below.

There has been net buying of Treasuries so far in 2025 Measured in $ billions, for first quarter 2025

Source: Macrobond, ING estimates

…So where does this leave us? The market is concerned that we’ll see some large negative numbers as validation of the “Sell America” trade. Indeed, we might. But remember, negative numbers in this series are not atypical. Such is the volatility of these series that China theoretically could see -$20bn, Japan could see -$20bn and the rest could see -$30bn and that would not be beyond statistical norms. But it would still be bad, as the market is fearing the worst, and would find that such data helps as a validation.

That said, the market should also quickly begin to attached a focus on the May data, as the mood music since April has in fact swung, in the sense that there has arguably been a bit of a “Buy America Back” phase since (see more here). A string of net outflows would be required to really validate concerns. And if we don’t? Well then nothing to see here.

Our view? We doubt the published data will take out statistical extremes, as the intense selling of Treasuries was also done by domestics, was aggravated by basis trade squaring, and the whole Sell America theme calmed thereafter.

Swiss review of the data with a definite and consistent bias …

Yesterday’s US data flurry gave hints about trade tax effects. Headline retail sales were weakened by poor auto sales. Some consumers bought cars early, anticipating trade taxes, and so did not show up at car dealerships in May. Import prices rose, suggesting that foreign companies were not absorbing trade taxes (so US companies and consumers will pay). Japan’s May trade data did show a 4.7% m/m drop in passenger car export prices, suggesting Japan’s automakers were absorbing some of the tariffs. Only auto prices showed this shift, which should appear in June’s US import price data.

The Federal Reserve meets. Every one of the 95 forecasts in the consensus expects rates to be unchanged. US President Trump advocates rate cuts, but this is a distinctly minority view. The trade tax increase is big, and the Fed wants greater certainty about its impact before changing policy…

…Trump’s social media posts have suggested increased hostility toward Iran, raising the possibility of the US striking (presumably) Iranian nuclear facilities. Markets are still inclined to view this as a local conflict, with limited global economic consequences.

Covered wagons have something to say ‘bout ReSale Tales … all is NOT lost … and on mfg …

June 17, 2025 Wells Fargo: Back-to-Back Declines for Overall Retail Sales, Core Spending OK

Summary A 3.5% drop in sales at auto dealers pulled overall retail sales into negative territory in May, and a downward revision reversed a modest April gain to a modest decline. Control group sales eked out a scant gain of 0.4%, but with half the store types reporting declines, retailers are struggling.

Sales Were Half Good… … For 20 years, e-commerce has been taking share from general merchandise stores and other brick & mortar retailers, that gained momentum during the pandemic, and so far e-commerce appears to be benefiting from the trade war, at least at this early stage. The category posted increased sales for the fourth straight month, this time a 0.9% gain, and is up 8.3% over the past year …

… Only half of all retailers reported a pickup in sales activity last month. The control group measure is a favorite in that it's a good indication of overall goods spending. It excludes somewhat volatile categories (such as gasoline and building materials) and sales at larger retailers (such as autos and restaurants). By this measure, underlying sales rose 0.4% and continue to run at a decent, if underwhelming, clip (chart). While control sales are a good proxy for goods consumption in GDP, given it gets at more of an underlying trend pace of spending, sales at these excluded retailers are still counted in consumption/output, they are just tallied from separate source data …

June 17, 2025 Wells Fargo: High-Tech Silver Lining for Otherwise Cloudy Manufacturing Sector

Summary The May industrial production report was a bit of a snoozer. What you need to know: manufacturing activity continued to tread water with tariff policy still weighing on activity rather than spurring it.

Finally, Dr. Bond Vigilante ahead of this afternoon’s DOTS …

The stock market held up remarkably well today considering that President Donald Trump abruptly left the Group of Seven meeting in the Canadian Rockies this morning. On his way home, he warned Tehran's residents to get out of town immediately. He also warned Iranian leader Ayatollah Ali Khamenei that he is an "easy target" and "our patience is wearing thin." In a subsequent post, he then demanded "UNCONDITIONAL SURRENDER" by Iran. His comments today suggest that the US might enter the war against Iran by dropping bunker-busting bombs on the country's nuclear facilities. The S&P 500 Aerospace & Defense stock price index is soaring in record-high territory (chart).

Under the circumstances, the participants of the Federal Open Market Committee (FOMC) have lots to discuss during their two-day policy meeting that ends tomorrow. What's not on the table is a rate cut anytime soon, in our opinion. That leaves Fed watchers focused on how Fed Chair Jerome Powell spins the range of views following the FOMC meeting at his presser tomorrow afternoon.

Fed watchers also will be focusing on the committee's latest Summary of Economic Projections (SEP). Odds are that its median economic forecasts will show slow economic growth with a slight increase in the unemployment rate and a modest short-term uptick in inflation--all mostly consequences of President Donald Trump's tariffs and now the war between Israel and Iran. The SEP is likely to signal a couple of small cuts in the federal funds rate in coming months. But Powell will certainly reiterate that the FOMC is in no hurry to do so…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

An allstar chimes in on bonds (via TLTs) …

at Sam_Gatlin

Bonds are hanging on for dear life at a multi-year support line. FOMC could be interesting tomorrow...

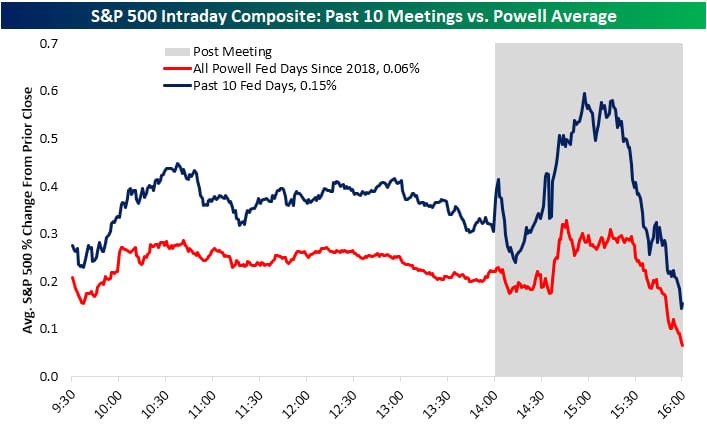

The chart below shows how the S&P has done on an intraday basis across all Powell Fed days since 2018 along with just the last ten meetings.

Positions matter and nobody ‘out there’ does better job of detailing it than EBB …

June 17, 2025 at 8:30 PM UTC Bloomberg: Traders Pile Into Bets That Next Fed Chair Will Slash Rates By Edward Bolingbroke

US rates traders have amassed a record futures bet that the Federal Reserve will take on a more dovish tilt right after Chair Jerome Powell’s term ends in May 2026.

The trade saw record volumes on Monday and swelled further Tuesday. The wager is that whomever President Donald Trump appoints to follow Powell will lead the central bank to cut interest rates almost immediately. The Fed’s first scheduled meeting under the new chief would come in June 2026.

For months, the president has been pressing Powell to lower borrowing costs, even as Fed officials have signaled that they plan to hold tight and monitor how Trump’s tariffs will ripple through the economy and impact inflation. The central bank is widely expected to keep rates steady Wednesday, and potentially pencil in less easing this year given the risk that levies will lift consumer prices.

The futures wager has been building in the market linked to the Secured Overnight Financing Rate, or SOFR, which closely tracks the outlook for Fed policy. It has gained momentum since Trump said this month that he would name a successor “very soon.”

“Trump could choose a replacement that is clearly more sympathetic to easier monetary policy, even though that may make it harder to get his pick through the congressional ratification process,” Steven Barrow, head of G-10 strategy at Standard Bank, wrote in a note.

Analysts including Will Denyer, an economist at Gavekal Research, cited the risk that an early nomination by Trump could lead to almost a year in which investors will focus on the pronouncements of the “shadow” Fed chair, along with signals from Powell.

“The cacophony could inflict another shock on market confidence in US policymaking,” Denyer wrote.

Monetary policy, to be clear, is set by a committee of Fed officials. The chair doesn’t unilaterally set policy rates.

The bet in rates futures involves selling the March 2026 SOFR contract and simultaneously buying the one expiring in June 2026 — the equivalent of a three-month spread trade, and it’s causing disruptions across futures covering the first half of next year.

The heavy selling in the March contract is causing it to cheapen by an outsized amount relative to other maturities, in particular those expiring in December 2025 and June 2026. As a result, the fly position — or the relative spread — around the March 2026 futures has spiked to the widest since January.

Volumes in the futures position hit a record 108,649 contracts on Monday, equivalent to approximately $2.7 million per basis point in risk. Open interest in both the March 2026 and June 2026 futures has reached the largest in the current policy cycle, partly as a result of demand for the trade.

Trading in many of these contracts is anonymous, making it difficult to identify the firms involved and the exact details of the trade.

On Wednesday, the focus will be on Fed officials’ forecasts, and the expectation is that the median participant will likely anticipate one quarter-point cut in 2025. In their previous economic projections, released in March, the median forecast was for two quarter-point cuts by year-end.

Traders, for their part, are pricing in that Federal Open Market Committee members will deliver roughly 43 basis points of total easing by year-end, with a quarter-point reduction seen as soon as September, but more likely in October…

Some additional / final thoughts on ReSale TALES …

Jun 17, 2025 WolfST: My Thoughts about those Retail Sales

… Seasonal adjustments include an adjustment for the number of “selling days.” In May 2025, there was one more selling day (27 days) than in May 2024 (26 days). So seasonal adjustments subtracted that extra selling day compared to May a year ago. Which is why seasonal adjustments were a little harsh in May. But ecommerce retailers, restaurants, and many other retailers were open seven days a week, including Memorial Day, so they were open 31 days in May, same as last year, and these seasonal adjustments can get confusing and uncertain quickly.

… The CPI for gasoline dopped by 2.6% in May from April and by 12.0% year-over-year (purple).

So people actually bought more gallons of gasoline than they did last year, as gasoline prices have fallen faster than the amounts consumers spent on gasoline. Anyone having to deal with the worsening traffic congestions on their way to work has first-hand experience that more people are driving more and clogging up the streets and highways more.

What we’re looking at here is not a sign of consumers cutting back, but of prices falling because the price of crude oil has plunged – and that’s a good thing for the rest of the economy:

https://youtu.be/pjQwTFa48xY?si=--64UnhMbjXMAYRZ

DoubleLine's Jeffrey Gundlach: Powell knows there's upside risk to inflation