ZH: Stocks Surge, Small Caps Erase All Losses Post-Trump As USTR Says Trump-Xi Meeting Still ‘Scheduled’

+

ZH: Watch Live: Fed Chair Powell Tilts Dovish On Labor Risks, Suggests Imminent End To QT

=

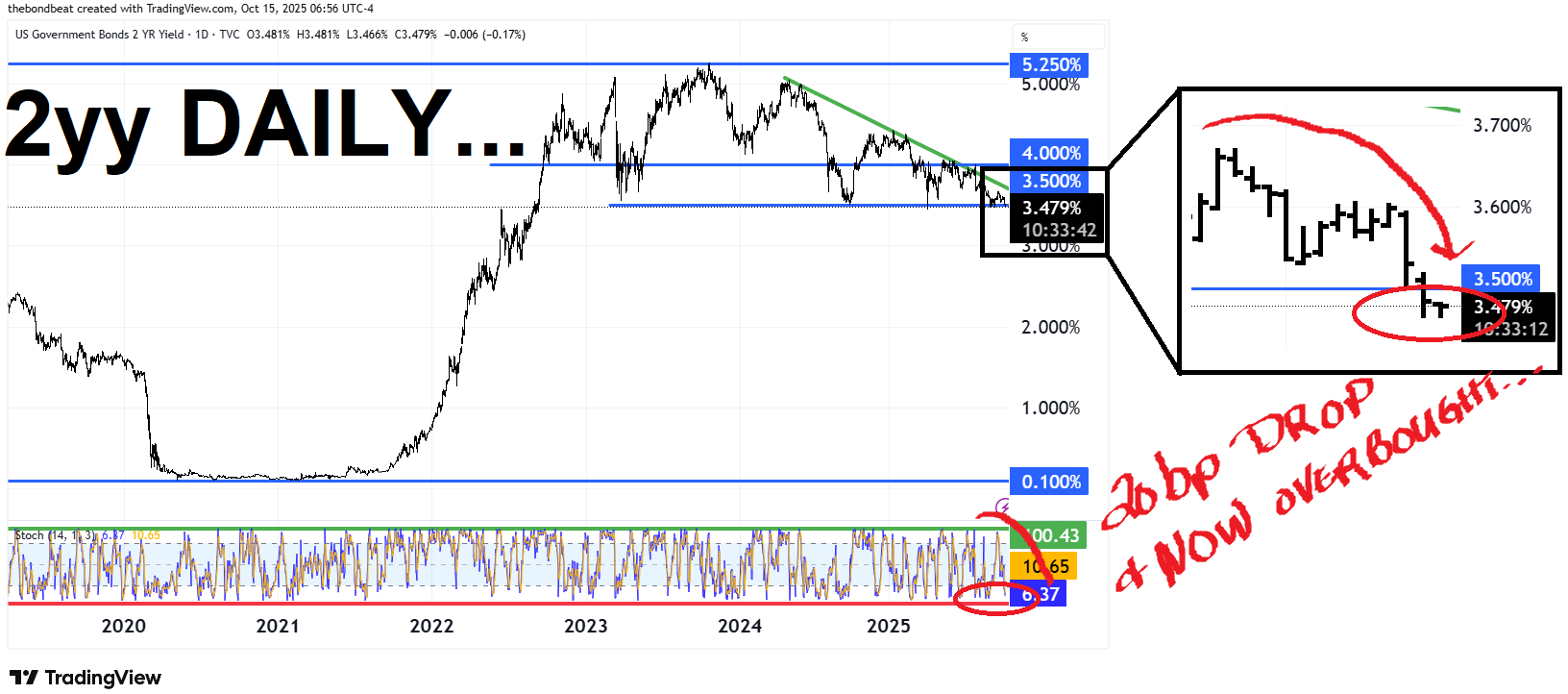

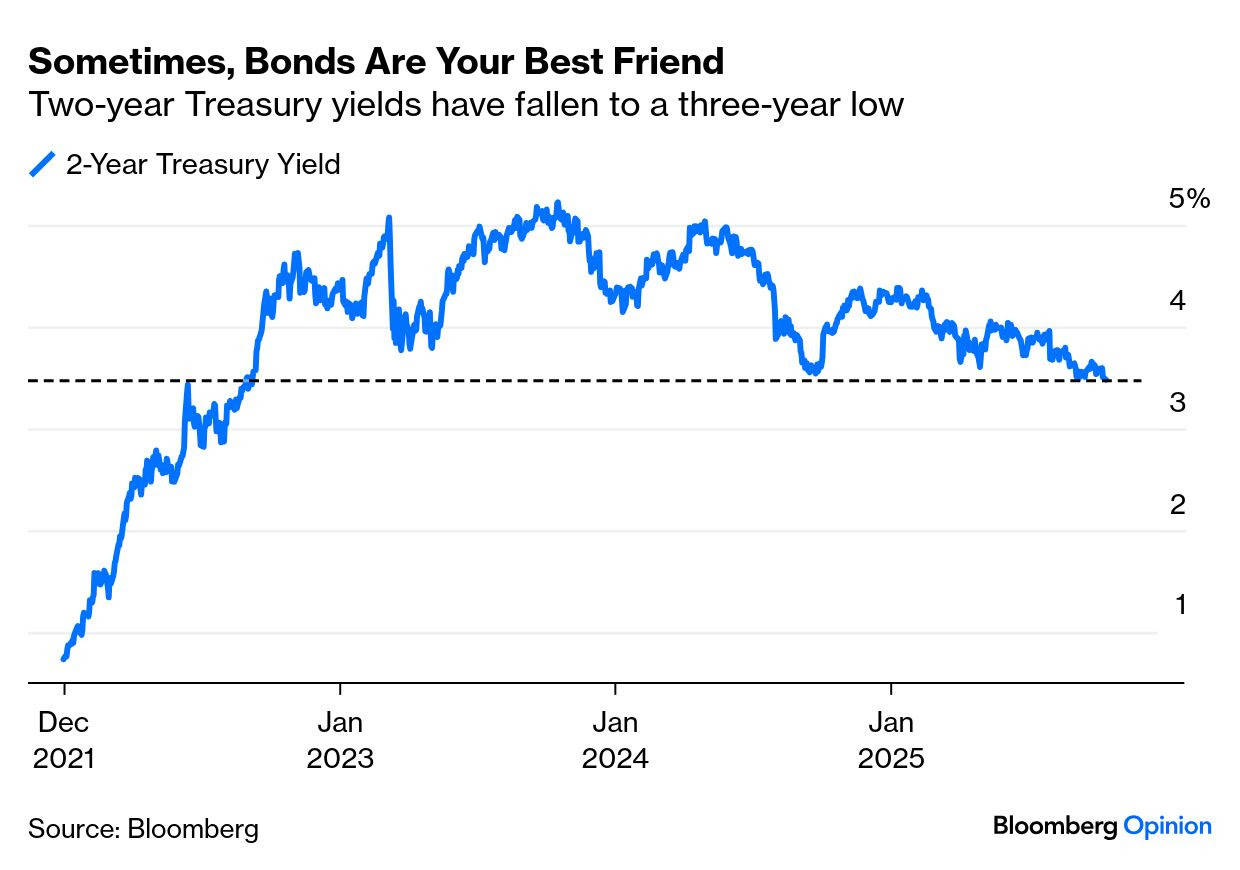

2yy DAILY: below 3.50% (resistance) becoming support …

… as momentum (stochastics, bottom panel) have adjusted from oversold to overbought now while yields have dropped ~20bps … makes sense…

… AND …

October 15, 2025 at 6:17 AM EDT Bloomberg: US Two-Year Yields Near Lowest Since 2022 on Rates, Trade Angst

(Bloomberg) -- Treasuries edged higher on expectations US interest rates will keep falling and as fresh trade tension between the US and China spurred demand for safer assets.

…Treasuries have rallied since the flare-up in trade talks prompted renewed demand for US government debt as a haven. Yields are down more than 10 basis points since late last week and Federal Reserve Chair Jerome Powell on Tuesday suggested the US central bank is on track to deliver another interest-rate cut later this month amid signs of economic weakness.

Bond markets are broadly stronger worldwide. Longer Japanese debt is climbing after firm demand at a 20-year government bond auction, while French notes are stronger on optimism that the French government will survive the country’s latest political turmoil.

…Additional comments from Powell signaling that the central bank may soon stop shrinking its balance sheet also helped lift Treasuries.

According to Michael Brown, senior research strategist at Pepperstone, Treasury yields at current levels suggest investors expect the Fed funds rate to fall to 3% around the middle of next year, from around 4.25%.

As a result, yields are unlikely to fall much further for now, unless another Trump-induced shock triggers a flight to safety, Brown said.

“The most obvious near-term candidate for further gains would be another growth scare if Trump’s 100% tariff threats start to look like more of a realistic possibility,” he said.

Investors are looking to a manufacturing print later Wednesday, along with speeches from Fed policymakers including Stephen Miran, Christopher Waller and Jeffrey Schmid…

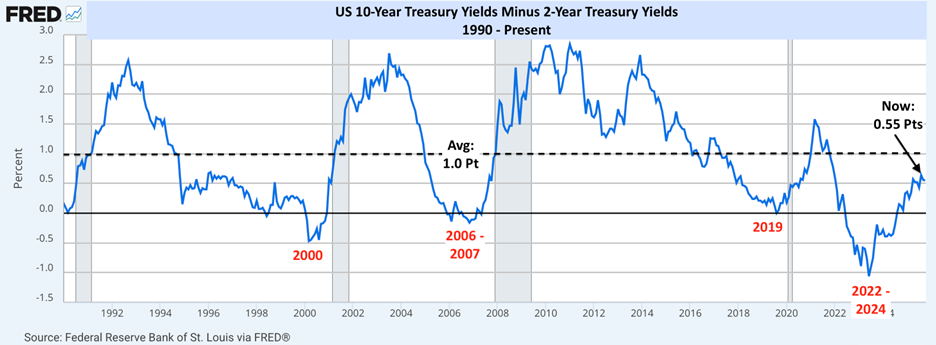

… make of any / all this whatever you want and I’ll add this. Looking at 2yy and rallying as they have, now hitting some sort of short-term resistance, one broadens lens and puts 2s in context of … 10s. DataTrek …

…Topic #2: US 2-year Treasury yields made a new +3 year low today, at 3.48 percent, which spurred us to look at an old favorite, namely the difference between 2- and 10-year Treasury payouts. The following chart shows that data (10-year minus 2-year yields) from 1990 to the present:

Four points on this data:

The 2-10 Treasury spread used to be a time-tested warning of a looming recession. Whenever it went negative, or got close to such readings, an economic slowdown was likely in the works. As noted in the chart, such was the case in 2000 (recession in 2001), 2006 – 2007 (recession in 2008), and even 2019 (surprise Pandemic Recession in 2020).

The underlying logic behind the rate/recession indicator is that 10-year Treasury yields reflect something close to the nominal real rate of interest and 2-years are driven by Fed policy. When the Fed has pushed short rates too high (i.e., above the neutral rate), a recession invariably ensues.

Since 1990, the 2/10 spread has averaged 1.0 percentage point.

At present, it is 0.55 percentage points.

Takeaway: This indicator was hugely popular among the bears in 2022 – 2024, the last time spreads were negative, but a recession never ensued and now spreads are nicely positive again. We suspect the 2-10 Treasury spread will continue to grind higher into year-end as the Fed cuts rates but US economic growth continues apace. That would be one more bullish sign for stocks as we move into the new year.

Bullish steepening is BACK, baby, and won’t take long for Global Wall to remind us … they told us so!! … here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: NQ boosted after ASML results; USTs firmer & USD slips ahead of Fed speak … USTs incrementally firmer, OATs gain as traders digest the latest pension reform suspension … USTs are marginally firmer (+1 tick at 113-14), extending Tuesday’s gains amid lingering haven demand and cautious sentiment following renewed US-China trade tensions after Trump threatened to end cooking oil business with China; support also comes from dovish Fed commentary, with Powell signalling rising job market risks, nearing the end of balance sheet runoff, and justification for a September rate cut, while today’s focus turns to Fed speakers and the Beige Book.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Large language models helping analyse FOMC mins … sure, why not…

14 October 2025 Barclays: FOMC Minutes NLP Analysis: September minutes provide few indications of disagreement about rate path

Our NLP analysis of the September minutes suggests that participants broadly agreed on the assessment of current conditions, inflation and the labor market. Our indicators may be distorted somewhat by a lack of discussion about topics of disagreement and the outlook, where key divisions remain.

What IF we start importing something ELSE from China …

15 October 2025 Barclays China: Softer-than-expected inflation

CPI missed expectation, falling for a second month on food and energy, while core CPI edged up y/y. Auto CPI fell m/m after stabilising in Jul-Aug . PPI narrowed partly on base, with some positives amid the anti-involution push. Soft inflation suggests GDP deflator likely remains in deflation in Q3.

September: -0.3% y/y for CPI, and -2.3% y/y for PPI

Bloomberg consensus forecast (Barclays): -0.2% (-0.2%) y/y for CPI, and -2.3% (-2.2%) y/y for PPI

August: -0.4% y/y for CPI, and -2.9% y/y for PPI

Best in show as the day settled having recently (Monday) booked some profits in long 10s (put hay in the barn NOT gone short or gotten bearish per se)…

October 14, 2025 BMO Close: On the Table, not Horizon

… Treasuries were largely range-bound on Tuesday after an overnight rally that saw 10-year yields dip below 4.00%. The inability of the 10-year sector to retain a 3-handle doesn’t come as a particular surprise given how well 4.00% has held as resistance in the recent past. Nonetheless, the rejection was not as swift or dramatic as one might otherwise have expected – a fact that we’ll attribute to the refocus on the risks to the global economy created by Trump’s trade war. We’ll be the first to concede that our interpretation was that investors had effectively ‘moved on’ from the trade tensions as a primary driver of price action in US rates. Clearly, we were too quick to dismiss the market relevance of the ongoing trade drama between Washington and Beijing. The willingness of the equity market to dramatically selloff on the trade-related headlines was also an underlying motivation that underscored the relevance of the developments and contributed to the initial follow-through in Treasuries.

As stocks improved off the session’s lows, the Treasury market sold off in a bear-steepening fashion. Gone are the days in which higher yields were a reason for lower equity valuations. In their place, Treasuries have regained their status as a ‘safe haven’ asset – or at least it is largely intact. There is a compelling argument to be made that the deficit concerns have contributed (and will continue doing so) to the stickiness of longer end yields in any attempt to stage a more significant rally. Had it not been for the ongoing deficit spending worries, 10-year yields would likely be comfortably below 4.0% at this stage in the Fed’s cutting cycle and ever-evolving macro narrative. After all, term premium remains well above zero (~57 bp) and the Treasury department isn’t expected to increase coupon auction sizes for the foreseeable future – certainly not at the November Refunding.

Powell’s comments on the balance sheet certainly didn’t go unnoticed by the market – if for no other reason than the Chair noted that, “Our long-stated plan is to stop balance sheet runoff when reserves are somewhat above the level we judge consistent with ample reserve conditions. We may approach that point in coming months, and we are closely monitoring a wide range of indicators to inform this decision.” Powell went on to add that, “Some signs have begun to emerge that liquidity conditions are gradually tightening, including a general firming of repo rates along with more noticeable but temporary pressures on selected dates. The Committee’s plans lay out a deliberately cautious approach to avoid the kind of money market strains experienced in September 2019.”

Our take is that this messaging doesn’t imply that an October announcement of the end of QT is in the cards, although a December timeline for an update on balance sheet policy is a distinct possibility. If not December, then at some point in Q1 (i.e. Jan 28 or Mar 18). In any event, swap spreads widened on the headlines as cash outperformed on the assumption that the end of balance sheet runoff is now on the table, if not immediately on the horizon. The curve steepening also extended on the news, with the 2-year sector benefiting as yields declined in outright terms – undermining the bearish skew to the steepening move…

…Tactical Bias …As for an update on our trading book, we booked profits on part of our core long position in 10-year notes (entered 9/25 at 4.18%) at our initial target of 4.02% on Monday.For the remainder of our clip, we’re targeting 3.93%. Our stop level remains 4.18% for the time being. While we remain constructive on the Treasury market from here, we’re viewing a consolidation with yields at a lower equilibrium as the path of least resistance until next Friday’s CPI report. 4.00% is an obvious technical line in the sand, and through there is September’s yield low of 3.988% In the event of a bearish reversal, we’d look for support to initially come in around 4.10%, through which is the 40-day moving-average at 4.149%…

An early morning REID of mkts recapping of the JPOW …

…It was Fed Chair Powell who provided a big offset to the trade fears, as he struck a more dovish tone than expected. The main headline was a surprise discussion around ending the shrinking of its balance sheet in the coming months. While our rates strategists suggest this timeline could be deliberately vague, it puts December on the map in terms of a halt. Indeed, recent history suggests “coming months” with regards to balance sheet changes has resulted in action within 2-3 months. There wasn’t much new on rates and the economy but there was no pushback to a cut later this month and the labour market commentary leant in a dovish direction as well.

The combination of the trade fears and the dovish comments has led to a decent rally for US Treasuries. For instance, the 10yr yield was unchanged yesterday, but overnight it’s fallen -2.1bps to 4.01%, which would be its lowest closing level since early April around the Liberation Day turmoil. Another factor that’s helped to keep a lid on yields has been a fresh drop in oil prices. So Brent crude oil prices (-1.47%) fell to a five-month low of $62.39/bbl, and overnight they’ve seen a further drop to $62.12/bbl. So even as the tariff threats have escalated again, investor concerns about inflation have come down, with the US 5yr inflation swap (-2.1bps) closing at a 3-month low yesterday of 2.54%. Nevertheless, the ongoing decline in nominal and real yields has continued to push up gold prices (+0.79%), which hit a fresh record yesterday of $4,143/oz, and overnight they’re up another +0.91% to $4,180/oz…

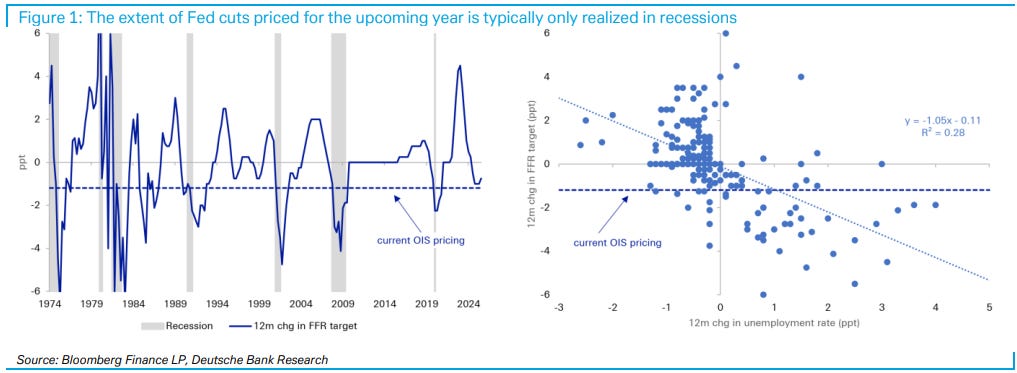

With moves over recent days in response to renewed trade tensions, the market is now pricing roughly 120bps of Fed cuts over the next 12 months.

As shown below (lhs chart), outside of recession, over recent decades the FOMC has only once delivered that much easing over a one-year period. That was in the mid-1980s and came from a starting point with the real fed funds rate about 5ppt above neutral (with an unemployment rate north of 7% and inflation near 3.5%).

Simple regressions help to put things today in context. Historically, a 1ppt increase in the unemployment rate over the prior year has been associated with roughly 1ppt of contemporaneous Fed cuts (rhs chart) and has explained around 30% of the variation in delivered easing. Adding the PCE inflation rate to that regression yields an estimated rule that looks broadly similar to the “first difference” policy rule from the Fed’s MPR; it has a beta of 0.3 on inflation, leaves the beta on unemployment around one, and raises the explanatory power to 40%. Reverse-engineering these regressions suggests current fed funds pricing would be consistent with a 75-100bp increase in the unemployment rate over the next year, in line with the low end of estimates highlighted in earlier work.

Ever wonder how rate cuts impact consumption? No? Too bad. Say you did, today’s your lucky day …

October 14, 2025 MS: US Economics, Securitized Products Strategy, and Consumer Finance: How rate cuts will affect consumption

We expect rate cuts to boost consumption but not enough to offset other headwinds near-term. Models show wide ranges of potential effects, and several factors could limit the support cuts will provide. Durables consumption and low-income consumers likely benefit most from cuts.

We expect the Fed to lower the target range for the federal funds rate by an additional 125bp by the middle of next year, to a terminal range of 2.75-3.0%. Our forecast is relatively dovish, with two more cuts next year than the median dot in the Fed’s SEP and one more cut more than the market is pricing. This is largely because our macro outlook is not quite as bright as the median FOMC member expects. Even with this expectation, the Fed still only gets to the vicinity of neutral (according to most estimates).

Models show unanticipated rate cuts should boost consumption relative to a scenario of unchanged monetary policy, but with wide confidence intervals around the magnitude of the boost. We cannot fully extrapolate model results to our forecast, since our model assumes cuts are unexpected and occur all at once. Still, we find the results to be a useful starting point. The model estimates a potential increase of 20bp - 100bp in the level of consumption over the 2 years after a 150bp decline in the target funds rate.

Several factors could mean the boost to consumption is smaller than might otherwise be expected. The first and in our view most important factor is that rate cuts do not come as a surprise; markets have been pricing in rate cuts for the past year, suggesting that some of the support for consumption may already have been realized. In addition, less restrictive policy is different than saying monetary policy is easy; while monetary policy should restrain consumption by less and less as the Fed cuts, we do not expect policy to be stimulative. Finally, even with cuts, we expect consumer loan rates will still be relatively high, and ~85% of consumer debt is fixed rate.

We still expect softer real consumption growth in coming quarters. We continue to expect softer real spending growth in Q4 and Q1 as real income growth slows, and these forecasts already factor in the additional rate cuts we expect. As we progress throughout 2026, we expect spending to start to reaccelerate, but growth remains moderate overall. Durable goods spending, which is more reliant on credit, and low-income consumers, who have relatively more floating rate debt, will likely benefit more from lower rates. That said, goods spending and low-income consumers also bear the brunt of tariff effects near-term.

Exhibit 1: Total real consumption response to an unexpected -150bp shock in the federal funds rate

… However, today’s housing market is unique when compared to the past several decades. As discussed above, the elevated concentration of fixed-rate mortgages in the US housing market has muddied the proverbial waters of the transmission mechanism of monetary policy within the housing market. Mortgage rates moved higher quickly throughout 2022 and 2023. As that happened, current homeowners who were able to lock in historically low mortgage rates in 2020 and 2021 saw no increase in payments. Instead, those higher rates and the record deterioration in affordability that accompanied them (Exhibit 21) made it increasingly difficult for first-time homebuyers to step into the housing market, and made it far more expensive for those who did manage to buy a home (Exhibit 22).

Exhibit 21: YoY change in affordability shows a record pace of deterioration in 2022/23

Exhibit 22: Evolution of mortgage payments to income by the year a home was purchased

US rates twist-steepen as Fed’s Powell and Collins confirm rate cut expectations & plans to end balance-sheet runoff; risk weakens as US-China trade tensions extend to shipping; French PM Lecornu suspends pension reforms & gains political support; DXY at 99.047 (-0.2%); US 10y at 4.032 (0bp).

…Front-end US rates rally 2bp on comments from Fed Chair Powell and Boston Fed President Collins confirming expectations for two more rate cuts in 2025. With hard economic data still lacking, Treasuries show little reaction to the morning’s moderate downside surprise in NFIB small business optimism at 98.8 (C: 100.6). Market pricing remains near consensus for Fed cuts in both October and December, and Chair Powell does little to dispel this notion. Powell states that the economic outlook appears unchanged since the Fed’s September meeting, reiterating risks to unemployment while acknowledging recent signs of stronger growth. After his speech, the implied likelihood of a December cut climbs another 5% to ~99%, supported by Boston Fed President Collins suggesting room for further cuts as “even with some additional easing, monetary policy would remain mildly restrictive.” Regarding the government shutdown, President Trump says he will reveal a list of federal programs to be cut on Friday.

In his remarks, Chair Powell reiterates the Fed’s long-standing plan to end balance-sheet runoff when reserves are somewhat above ample, which Powell believes could be “in coming months.” This view follows the deputy SOMA manager’s projection for reserves to approach $2.8tr by the end of 1Q26. He acknowledges recent developments in funding markets, but notably qualifies these pressures as “temporary” and occurring on “selected dates” — confirming expectations for balance sheet runoff to continue, albeit with a “deliberately cautious approach” given the strains in September 2019…

Few thoughts from across the pond …

October 14, 2025 NatWEST: Should the short end price temporary policy deviation, or structural change?

Our Treasury forecasts outline a scenario through 2026 in which the Fed eases to neutral (taking this as ~3%), fanning the flames of inflation that we expect to rise for both structural (primarily demographic) and cyclical (existing pro-growth policy and tariff pass-through) reasons. Given the change of reaction function at the Fed, the pro-growth / dovish lean of its members from administrative influence, and a pending change of Chair in May, we see term premia rising sharply through 2026 as markets come to terms with a Fed unwilling to act as the inflation “circuit breaker” via tighter policy.

Broken down into key components, our term premium narrative reflects four inflationary factors: 1) greater pass through of tariffs into consumer inflation, 2) material growth re-acceleration into H2 2026 producing cyclical upward pressure on inflation from an above-target starting point, 3) greater economic proclivity for inflation given demographic trends, and 4) a durable change in the Fed’s inflation reaction function – ie the view that the Fed will tolerate inflation that is consistently higher than the current target level of 2%.

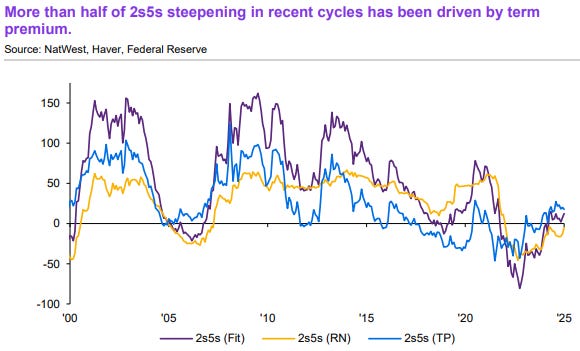

Current market pricing for front-end steepeners (2s5s, 1s5s) imply a view that the Trump administration can suppress short rates during its term, but that policy rates will ultimately have to rise to counter incipient inflation, regardless of who is at the helm of the Fed or White House.

On the other hand, we argue that current efforts by the administration can instead exact a change to inflation policy that can prove durable across political parties given the political convenience. A lasting change in reaction function would dampen short rate reversion to a (rising) nominal r*, or equilibrium level of policy rates, while also suppressing intermediate rates as markets price in a longer duration for low-rate policy.

Aside from the change to the inflation reaction function, in this piece we also discuss two other factors that should dampen intermediate curve steepening. These are bank credit growth via bank deregulation (historically a curve flattener), and financial repression (ie the manipulation of economically sensitive points on the curve such as 5s and 10s to control mortgage and C&I loan rates).

Altogether these three factors impact the curve through both market expectations and term premium. We look at these over policy cycles via the ACM model decomposition of fitted rates into risk neutral (expectations) and term premium components.

LABOR WEAKNESS > ‘flation …

15 Oct 2025 UBS: Labor weakness still beats inflation increases

Federal Reserve Chair Powell reiterated that labor market concerns dominate inflation concerns in current policy. The lack of a functioning US federal government means this economic analysis depends on dubious quality data—private sector polls and potentially distorted anecdotal evidence—but Powell has shown a willingness to depend on such data in making past policy decisions….

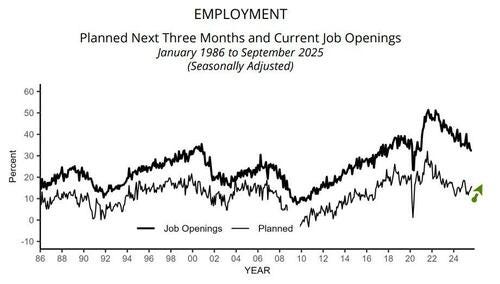

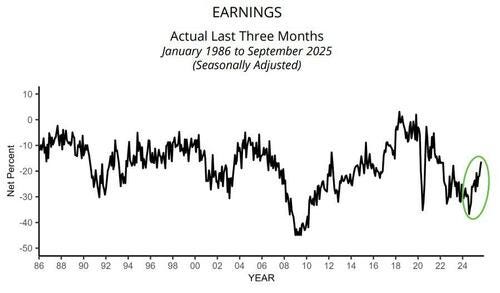

October 14, 2025 Wells Fargo: Small Business Optimism Dips Ahead of Government Shutdown September Brings Increased Uncertainty and a More Pessimistic Outlook

Summary The NFIB Small Business Optimism index fell to 98.8 in September, reversing the gains posted over the previous two months. Although small firms have generally been downbeat for much of the year, the uncertainty index spiked to the highest level since February, suggesting that increased chances of an impending federal government shutdown may have weighed on sentiment.

On the bright side, hiring plans and current sales continued to improve from a low level, pointing to activity remaining resilient over the past several weeks. That noted, firms lowered their expectations for future sales and fewer reported that now is a good time to expand, showing that higher interest rates, sticky inflation pressures and low visibility on the economic policy front remain challenges.

Finally, in the better LATE than never category — today’s CPI punted til next week SO a precap …

October 15, 2025 Wells Fargo: September CPI Preview: Better Late Than Never

Summary The government shutdown may have altered the September CPI release date, but it hasn’t changed the stubborn state of inflation. We estimate headline CPI rose 0.4% last month, underpinned by a jump in energy prices, which would lift the year-over-year rate to a 16-month high of 3.1%. Core inflation likely rose 0.3% for the third consecutive month, holding the year-over-year rate steady at 3.1%. Beneath the surface, we expect goods inflation to stay elevated due to continued tariff pass-through, while an easing in primary shelter costs should help cool services inflation.

We are not concerned about the federal government shutdown affecting the quality of the September CPI data since BLS collections proceeded through the end of the month, as scheduled. But as the shutdown drags on with no end in sight, risks are mounting for October’s report. At a minimum, collection rates stand to be lower with data gathering still suspended, and the risk is rising that the publication of the October CPI report could be skipped entirely.

Setting aside the near-term data challenges, sticky inflation persists. We expect inflation to hold near a 3% annualized pace through mid-2026, as the full brunt of tariffs has yet to feed through to goods prices and consumers’ general resilience limits a further slowing in services inflation…

…The core index is also likely to signal stalled progress in lowering inflation back toward the Fed’s target. Excluding food and energy, we estimate prices rose 0.3%, leaving the year-ago rate at 3.1% (Figure 1).

Figure 1

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

An OpED from The Terminal …

October 15, 2025 at 4:25 AM UTC Bloomberg: What does China want? It’s too soon to tell Whether playing from a position of strength or weakness, Beijing’s timing is excellent. John Authers, Columnist

…Bonds There are still some institutions with clout to rival China’s government, and the Federal Reserve is one of them. Chair Jerome Powell helped Tuesday with a speech laying out plans to reduce QT or quantitative tightening — to lessenthe Fed’s sales of bonds into the market. That means more cash and more liquidity left in circulation, and it helped bond yields drop to fresh lows:

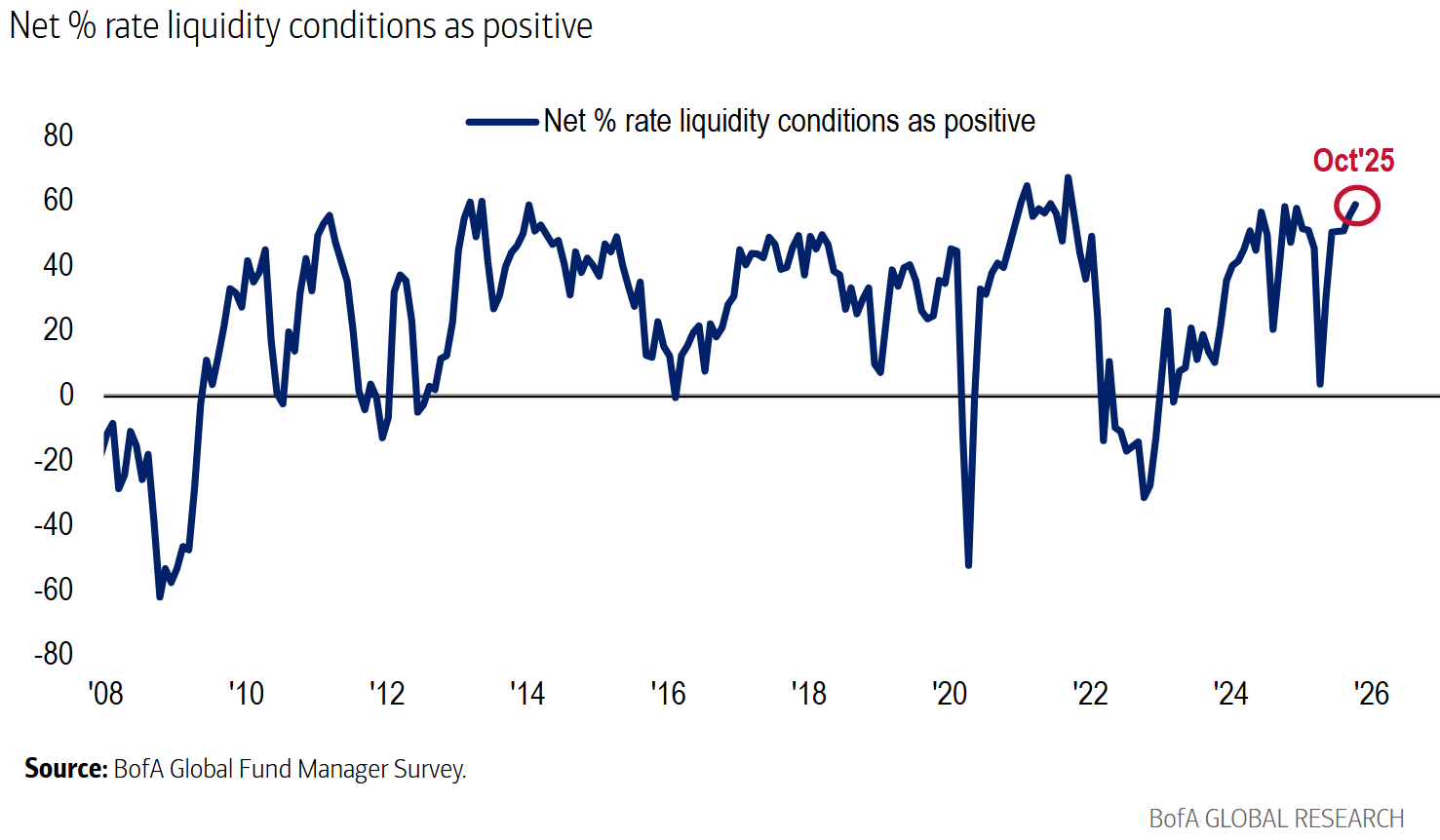

Critically, market participants report that liquidity is plentiful for them. The BofA survey found the percentage of fund managers comfortable with the level of liquidity at the highest since 2021 and near the top of its post-crisis range. The latest Fed news will do this no harm:

It was the bond market that forced the administration’s reversal on tariffs six months ago. Now it’s calm, aided by a Fed that is easing financial conditions (and would probably be doing so even if it were not under political pressure to do so). This makes the US position much stronger than it was then…

ZH: Small Business Optimism Dips In September But Labor Market Signals All Improved

Small Business Optimism Dips In September But Labor Market Signals All Improved

Amid a dearth of macro data due to the shutdowns, this month’s Small Business Optimism survey suddenly becomes noteworthy with the headline sentiment index dipping in September to a three-month low (down 2 pts to 98.8)on less optimism about the economic outlook and greater concern about excess inventory.

Source: Bloomberg

Five of the 10 components that make up the gauge decreased, while three were unchanged.

Owners grew more anxious about inflation, with 14% of owners reporting that rising costs were their biggest problem in operating their business, up 3 points from August.

A net 31% plan to raise prices in the next three months, up 5 points and the largest share since June.

“While most owners evaluate their own business as currently healthy, they are having to manage rising inflationary pressures, slower sales expectations, and ongoing labor market challenges,” Bill Dunkelberg, NFIB chief economist, said in a statement.

But while uncertainty was elevated (the fourth-highest reading in over 51 years)...

Source: Bloomberg

...the employment components showed improvement - positive employment change, hiring plans continuing to increase, compensation for labor higher.

Hiring plans are at their highest level since January.

So to summarize the somewhat strange NFIB data - Earnings expectations are rising as are hiring intentions but the headline confidence number is lower?

Finally, NFIB notes that whatever impact the government shutdown has on small businesses, it will show up in the October survey. Questionnaires were mailed out on October 1.

BMO's call to book profits at 4.02% on their long 10s position makes sense given the technical resistence at 4.00%. The fact that swap spreads widened on Powell's QT commentary shows the market is already pricing in the end of runoff happening sooner rather than later. What's interesting is how BMO's strategists are framing this as consolidation rather than reversal, still targeting 3.93% for the remainder of their clip. The deficit ceiling remains the wildcard that could keep term premium eleveted even as the Fed cuts.

BMO's call to book profits at 4.02% on their long 10s position makes sense given the technical resistence at 4.00%. The fact that swap spreads widened on Powell's QT commentary shows the market is already pricing in the end of runoff happening sooner rather than later. What's interesting is how BMO's strategists are framing this as consolidation rather than reversal, still targeting 3.93% for the remainder of their clip. The deficit ceiling remains the wildcard that could keep term premium eleveted even as the Fed cuts.