while WE slept: USTs incrementally firmer/flat; FOMC recaps and ... 2s 'rangy', NIRPs BACK, BRENTs +20.52% since 6/1, Fund managers: U/W USD, recession call gone, rates higher for longer ...

Good morning … debated NOT sending anything today and only sending some sorta commentary over the weekend BUT with markets open and likely to be extremely quiet as the ‘hamptons hedge’ likely went into effect just after the FOMC inspired activity Wednesday, well … consider this something of a place holder — a few things to read / consider IF you, like me, are at your desk this morning…Let’s jump right in.

Equity futures are LOWER, Oil and UST yields are a touch HIGHER ‘as Trump weighs attack on Iran’ … in OTHER news, Japan’s key consumer inflation gauge accelerated (2yr high, BBG) and UKs consumer confidence improved (again, BBG) as UK ReSale Tales DROPPED (BBG).

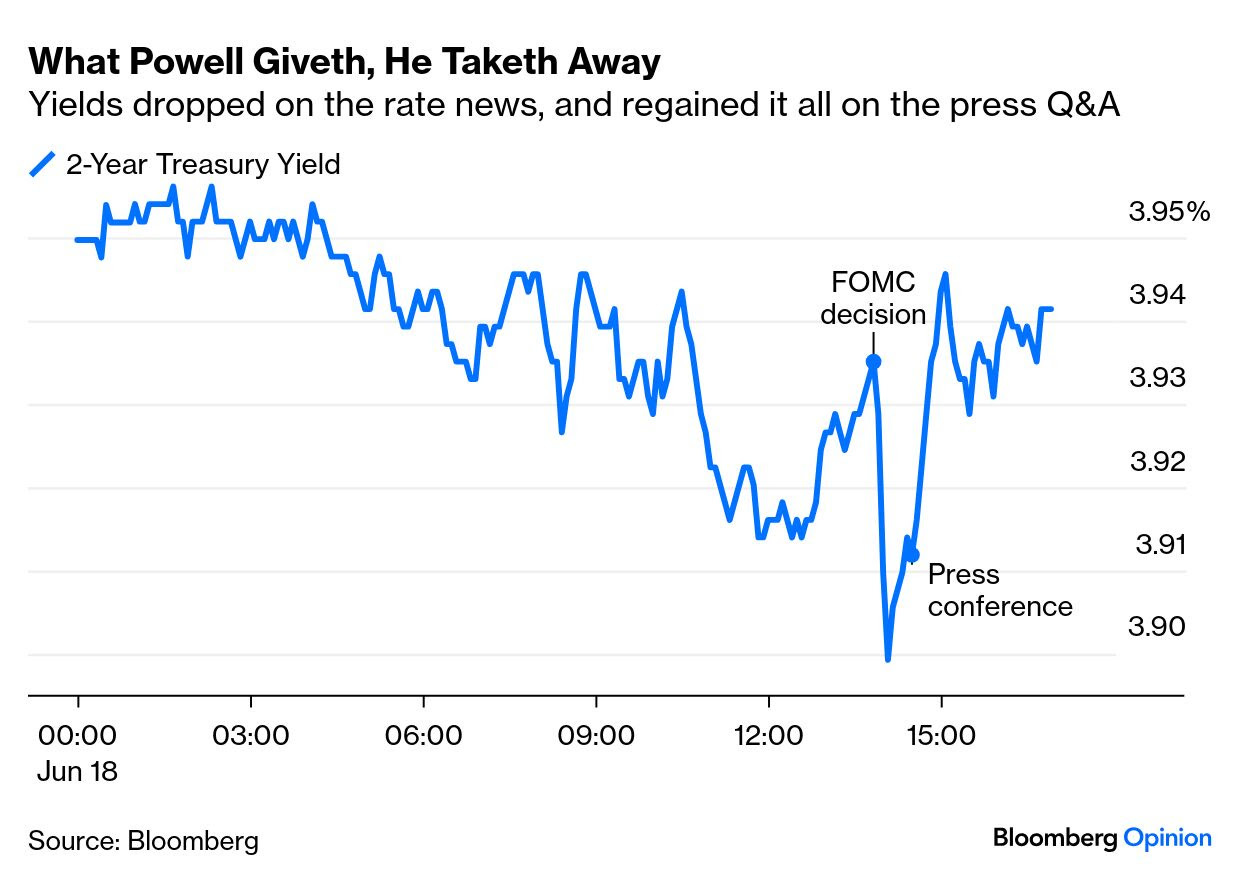

First up, a post-mortem CHART which is FOMC related … This DAILY chart of 2yr yields from a note (below) from one of the best techAmentalists in the biz …

US 2y yields: We continue to be neutral on yields, with 2y yields looking rangy at the moment, The first key support level is at 3.88% (55d MA). A weekly close below 3.88% would open the door for a move towards stronger support at 3.75% (7 May low), and 3.66% (200w MA).

Resistance on the other hand is likely at 4.02% (200d MA) and 4.07-4.08% (Dec 2024 low, March 2025 high.

For now we think 2y yields will hold in the 3.80% to 4.07-4.08% range.

… read on below for more on this, a weekly and a look at 10s as well as bonds … Fed did NOT do ANYTHING and it would then appear Global Wall reading of the ‘tea leaves’ would suggest more of the same (ie nothing) to continue.

They (CitiFX, best techAmentalist in the biz) watching momentum (on verge of a more bullish WEEKLY cross and need some confirmation (if, say, rates were to start falling) …

I can and will try to have a look at the charts over weekend but the fact that CitiFX is not only watching stochastics but also the 55dMA as well as the 200wMA, tells me (and so, you) what one needs to know.

Rangy feel, indeed. Check yer narratives at the door unless you are looking to be thoroughly disappointed. For now.

In any case, taking a quick look at whatever is helping shape shift and formulate the prices above — data. Early Wednesday, it was housing …

ZH: Housing Starts & Permits Plunge To Weakest Since COVID Lockdowns

… and Claims, too, where survey week SAYS …

ZH: DOGE Is Working: Jobless Claims In 'Deep TriState' Surge To 4 Year Highs

… but the feature of the day was …

ZH: Trump Slams "Stupid" Powell: "I Think He Hates Me. I Call Him Every Name In The Book To Try And Get Him To Cut"

… clearly flattery continues to get ‘47 nowhere …

ZH: Stocks Pump'n'Dump As Powell Pessimism Trumps Iran Optimism

… turning the page to OTHER CBs out since the FOMC and there where one, specifically, caught my attention …

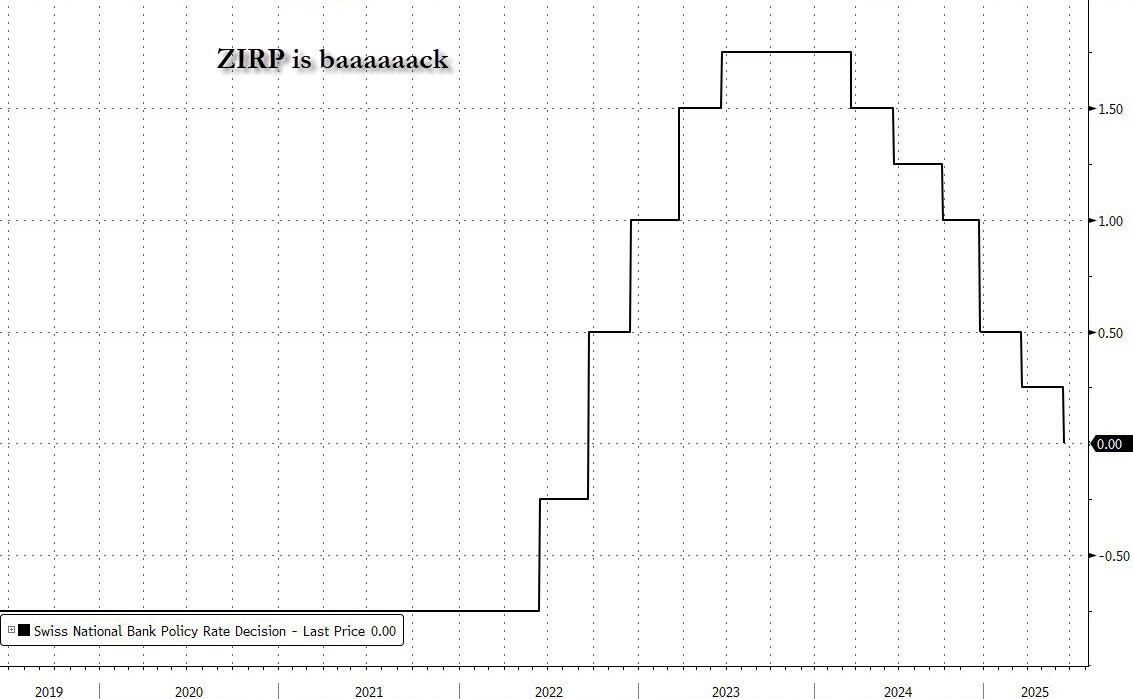

ZH: NIRP Is Back As Swiss National Bank Cuts Rates To Zero, Introduces Stealth Negative Rates

Five years after covid sparked a once in a generation inflationary surge and forced all central banks to push their interest rates well above the zero (and in some cases negative) lower bound which defined the post-QE era, overnight the Swiss National Bank became the first to show that the world of higher rates is over and ZIRP is coming back, after the central bank cut its rate from 0.25% back to 0.00% for the first time since 2022.

But it's not just ZIRP that is back: NIRP is also here courtesy of the Swiss, because while the SNB may have cut its interest rate to zero, the way it penalizes banks’ excess reserve holdings means lenders will face negative rates if they park too much cash at the central bank.

Ah yes, the magic of the zero lower bound is once again with us!

According to a statement by the SNB published on Thursday morning, Swiss banks can hold up to an unchanged 18 times their minimum reserve requirement in sight deposits at the SNB for free but anything over that they will be charged interest of -0.25% as the discount from the policy rate remains unchanged at 25 basis points.

The goal behind the “tiered remuneration”, according to Bloomberg, is to incentivize lending between banks so that enough liquidity is exchanged on the Swiss money market. For lenders holding more than their limit it’s cheaper to pass on excess reserves to institutions which are under their thresholds, because they have to pay them less than the central bank.

For all lenders which don’t have a minimum reserve requirement the threshold is set at a paltry 10 million francs ($12 million) in sight deposits, the SNB said.

The system, which the SNB has had in place since it lifted its key rate above zero in 2022, means that the average money-market rate — known as Saron — has usually been a few basis points below the central-bank rate.

Which means that starting Friday, negative funding costs for banks are therefore likely, as board member Petra Tschudin told reporters in Zurich. She added that she expects only “very little” sight deposits to be remunerated at the negative rate. That chimes with experience from some three years under the regime, where typically only a tiny fraction of them were hit by the lower rate.

Still, little or not so little, negative rates are back in at least one country... and soon in many more.

While Switzerland’s main banks lobby called the SNB’s decision “understandable,” it criticized its consequences.

“It’s clear that a zero interest rate environment diminishes the incentive for responsible saving and places additional pressure on retirement provision,” the Swiss Bankers Association said in a statement. “As in previous periods of low interest rates, banks and their customers once again bear a significant share of the monetary policy burden.”

Similarly, the insurance association welcomed the SNB not going negative, but stressed that “even the return to a low interest rate environment already poses a challenge” to the sector.

SNB President Martin Schlegel acknowledged the discomfort the new rate environment creates for banks and signaled that there’s an elevated bar for further cuts.

“We would not take the decision to go negative lightly,” he said. “But I want to stress that the profitability of banks is not within the national bank’s objectives.”

Finally, while some argue that negative rates are a way for capital deficient central banks to restock their coffers after years of high rates pushed them all into technical insolvency, given the small share of deposits affected, it’s unlikely that the SNB will make a lot of money from charging lenders. Between 2015 and 2022, the central bank earned almost 12 billion francs from negative rates, though it then paid out 14.5 billion francs from when rates turned positive through the end of March of this year.

AND … I’ll quit while I’m behind, crawl back under the rock from which I cam but first … here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Oil pushed lower after Trump gives two weeks to decide on Iran strikes … USTs incrementally firmer/flat as it returns to Cash trade following Thursday's holiday. Contained overnight, but was then pressured in the European morning, potentially as traders continue to digest and factor in the latest geopolitical optimism. Downside limited so far, and USTs remain above Thursday’s 110-22+ base.

Yield Hunting Daily Note | June 18, 2025 | Fed Day, TEAF Into TYG, NXC/NXN Into NXP, Pioneer Funds

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … First UP, all things FOMC related …

The FOMC kept rates unchanged, with participants divided between zero and two cuts this year, amid downward revisions to growth, upward revisions to inflation and unemployment, and elevated uncertainty. Powell was mildly hawkish, indicating no rush to cut rates…

…We retain our baseline expectation that the FOMC will deliver a single 25bp rate cut this year, in December, with the economy slowing, the unemployment rate edging up, and the tariff-related inflation bump showing signs of having peaked. We see risks tilted toward delayed rate cuts.

June 18, 2025 BMO: Fed keeps 50 bp cut message; core-PCE 3.1% 2025

… Overall, it wasn't a particularly surprising Fed update and the market has retained the bid that has been in place throughout the day. From here, investors will focus on the press conference where we expect a marginally hawkish skew to the wait-and-see messaging …

18 JUN 2025 BNP US June FOMC: It’s been a long road, getting from there to here

KEY MESSAGES

Having now kept interest rates unchanged for six months, Chair Powell seemed to indicate that the Fed could well stay paused through the summer, making October the next “live” meeting. We continue to expect policy to remain on hold past the end of the year.

The FOMC seems polarized between one faction that favors some rate cuts late this year and another that prefers none. While the median “dot” reflects the former’s views, Powell argued forcefully at the press conference for the latter, and we see that camp carrying the day in the end.

The apparent disconnect between Powell’s policy discussion and the median “dot” suggests a need to reform the projections process as part of the ongoing policy review.

… US interest rates strategy – a flat FOMC: While the FOMC dots suggested two median cuts in 2025, Chair Powell repeatedly said “no one holds these rate paths with any conviction”, moving the markets away from interpreting the dot plot or even the SEP too literally. Much like the May FOMC, Powell’s remarks conveyed a sense of wait and watch, disappointing those who think the Fed is looking to actually deliver two cuts (or more) this year. The biggest curve steepener positioning bias in the last 10 years (see Steepeners - big, but not as beautiful, dated 9 June) is likley to be disappointed by the June FOMC meeting outcome.

Beyond the FOMC, we doubt that this meeting paves the way for any follow-up market reaction or any new direction or framework for markets to contend with. We think rates markets will continue to focus on realized economic data on labor market and inflation, both of which have held up relatively steady. Focus will also be on fiscal headlines and the supply/demand picture in Treasuries. We continue to suggest 6m2s10s conditional bull flatteners.

The Fed kept rates steady and mostly maintained existing signals about the policy outlook. The dot plot was closely divided with just one official keeping the median at two cuts. That said, there was a hawkish shift as seven officials projected no cuts this year, up from four in March. Beyond, fed funds projections moved 25bps higher in 2026 and 2027, motivated by a stickier inflation profile.

Chair Powell’s press conference did not take the opportunity to reinforce the potential near-term dovish signal from the dot plot. Instead, Powell indicated that the labor market and economy remain solid and that they continue to anticipate inflation will rise due to tariffs. He also emphasized that uncertainty remains historically elevated, a reason to downplay rate projections, and that all of the fed funds paths in the Summary of Economic Projections could be reasonable.

The Fed’s median forecasts for inflation and the unemployment rate now closely align with our own for this year. While we expect the Fed to be somewhat slower to cut rates than the median projection in the SEP – we maintain our call for the first rate cut in December followed by two more reductions in Q1 2026 – our expectations are now closely aligned for 2026. Risks to this view are skewed slightly towards earlier cuts, though as the dispersion of the 2025 dots indicates, there is clearly no strong consensus at this point.

18 June 2025 ING: Fed still leans in the direction of cuts, but timing will be delayed

While the policy interest rate was left unchanged, Fed officials are still suggesting rate cuts are likely this year. However, we are doubtful that a majority will be convinced on the case for cuts before December, by which time they may feel the need to move by a more aggressive 50bp cut

…We forecast a 50bp cut in December Nonetheless, the squeeze on spending power from higher goods and energy prices could lead to cuts to discretionary spending that impacts the service sector and slows inflation faster there. At the same time the jobs market is cooling and wage inflation is weakening. There is also evidence of softer housing-related inflation on the way with new tenant rents already turning negative. Housing accounts for around 40% of the core CPI basket by weight and that process will help inflation to return to 2% in 2026.

Consequently, we think December will be the likely start point, but that may well be a 50bp cut, especially if jobs and GDP growth slow as we anticipate. This would be a similar playbook to the Federal Reserve’s actions in 2024, where they waited until being completely comfortable to commit to a lower interest rate environment. Then they did a 50bp move in September followed by 25bp cuts in November and December.

Market rates distill a mild bearish tint from Chair Powell’s tone The impact gap lower in market rates post the Fed announcement was not backed up by anything in particular. The dots were mixed versus what was expected by the market, but not dramatically deviant. The statement was not overly dovish. It was more balanced than the market was letting on. Clearly there is an intention to cut rates down the line, but we knew that ahead of time. At the same time, the inflation projections are higher than before.

The curve in consequence had snapped steeper, and before Chair Powell spoke, much of the initial push lower in the 10yr yield was reversed (to above 4.38%), while the 2yr also had with a tendency to edge back up again. The 10yr breakeven inflation rate also edged up (well clear of 2.3%), while the 10yr real yield broadly held steady to a tad higher (towards 2.05% area). The tone of the commentary was broadly in tune with an edge higher in market rates in net terms.

Effectively the Fed has acknowledged that the contemporaneous economy is doing reasonably well, with risks, and has batted the whole thing back to the macro data to come in the coming months…

June 18, 2025 MS: June FOMC Reaction: Holding Out for Summer

The SEP and press conference were largely as expected. Forecasts incorporated tariffs, and Chair Powell kept his wait-and-see tone. Like us, he expects inflation to pick up in the summer. Divergence in forecasts led to a split in the dot plot. We still expect the Fed to be on hold this year.

Key expectations

The SEP showed expectations for lower growth and higher inflation this year, as expected. The median projected Fed Funds rate for 2025 was unchanged, indicating two cuts, but the average increased. There is more divergence in views, with seven members projecting no cuts this year.

Chair Powell maintained his wait-and-see stance, noting he expects to see a pickup in inflation from tariffs "over the course of the summer." Our views are in line; we expect to see tariff impacts in coming inflation prints, with inflation peaking in August.

The Fed's projections for inflation and growth moved more toward ours for 2025. We continue to project slightly higher inflation and lower unemployment than the SEP showed. We maintain our view that the Fed will be on hold throughout 2025, with back-loaded cuts in 2026.

Our rates strategists continue to suggest UST 3s30s curve steepeners and term SOFR 1y1y vs. 5y5y curve steepeners as downside risks to upcoming labor market and inflation data should elicit a greater steepening than would upside risks elicit a flattening.

Our FX strategists maintain their short USD recommendations against EUR and JPY as the 3s30s UST curve steepens and correlations favor USD-negative currency hedging.

Our agency MBS strategists keep their neutral positioning, with the base case for 2025 providing carry and 2026 providing spread tightening.

The Federal Reserve kept interest rates unchanged yesterday, maintaining the target range at 4.25–4.50%, and signaled that it is not in a hurry to adjust rates.

… The inflation projections presumably now take on board FOMC participants' base case of the go forward for tariffs and trade policy. With the House and Senate both now having chimed in with tax cut plans, FOMC participants' views on fiscal policy should be converging with the legislative debate, and that should be reflected in the projections too. Overall the participants appear to see the policy mix as negative for growth, and estimate below trend growth in 2025 and 2026 before returning to trend in 2027.

… However, 2026 revised up 25 bp to 3.6%, which was in line with our expectations, and up 25 bp to 3.4% at the end of 2027. Overall, despite upward revisions to the core inflation projections to 3.1% this year (we expected 3- 1/4%) the FOMC still seems comfortable with two 25 bp rate cuts as appropriate. Indeed, the median no longer sees inflation returning to target over their forecast horizon. Overall, the FOMC displayed more comfort with the inflation profile this year, at this juncture, than we anticipated.

June 18, 2025 Wells Fargo: Elevated Uncertainty Keeps FOMC on Hold Again

…Outlook for Monetary Policy Remains Highly Uncertain The dot plot and Powell's comment imply to us that the outlook for policy remains highly uncertain due, at least in part, to the uncertain outlook for U.S. trade policy. Higher tariffs will likely weigh on real GDP growth, which could be offset by policy easing, while also raising inflation, which would likely induce the FOMC to remain on hold if not tighten policy. As we discussed in our most recent U.S. Economic Outlook, we think the FOMC will look through any one-off price increases caused by tariffs and instead concentrate on the growth-eroding and unemployment-increasing effects of higher import duties. We currently look for the FOMC to commence an easing cycle in September, and look for 75 bps of rate cuts by the end of the year. That said, we readily acknowledge that the FOMC may refrain from cutting rates if inflation expectations rise and/or wages accelerate. Chair Powell also said in his press conference that policymakers "think they will learn a great deal on tariffs over the summer." We also will be focused intently on economic developments in coming months.

… AND all other things Global Wall is sellin’ for trading flows …

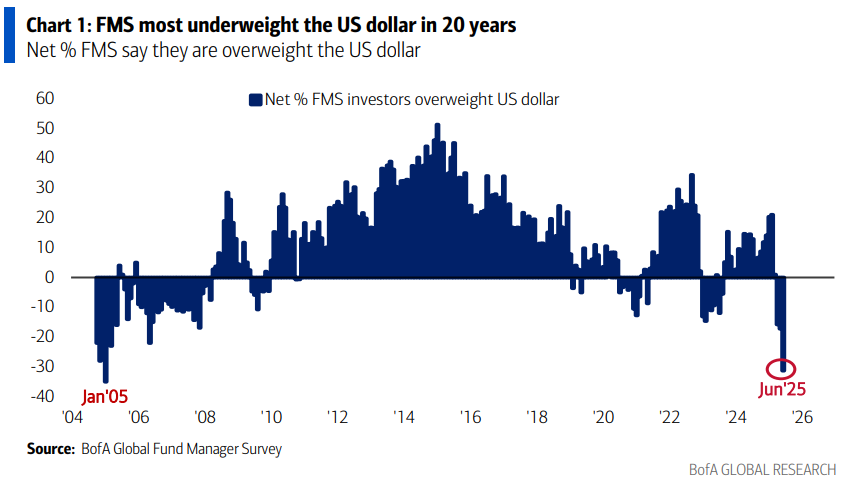

The bank of the land out with latest GLOBAL manager survey and I’m just now stumbling across it …

17 June 2025 BAML: Global Fund Manager Survey The Buck Stops Here

The Bottom Line: investor sentiment recovers to pre-Liberation Day “Goldilocks bull” levels as trade war & recession fears abate; cash level drops to 4.2% (was 4.8% in April) but not worrying low; BofA Bull & Bear Indicator up to 5.4; most extreme view…investor UW in US$ largest in 20 years (Chart 1)…biggest summer pain trade is long the buck.

… FMS recession expectations have collapsed in the past 2 months, falling from net 42% of FMS participants saying a global recession was likely in the following 12 months in April, to net 36% now saying it is “unlikely”.

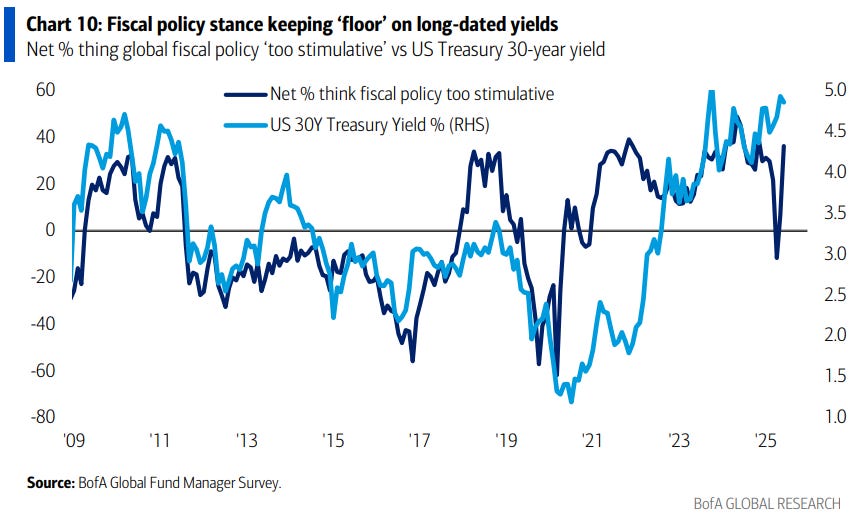

… The past 3 months have been dominated by the prospects of further fiscal support in the US and Europe (i.e. Germany), lifting longdated government bond yields across advanced economies.

FMS investors’ perception of easy global fiscal policy hit a 7-month high (net 36% say that global fiscal policy is “too stimulative”).

Note FMS perception of fiscal policy stance turned restrictive in April for the 1st time since Dec’20.

…On rates outlook, net 21% of FMS investors expect higher bond yields (i.e. long-term interest rates) in the next 12 months, highest % since Aug’22.

… and from flows TO a WEEKLY from the best in the biz … this was sent late Wednesday … and they are still lookin to enter 2s10s steepener, 10s30s flattener and now will added SFRM6/M7 steepener IF … the price is right …

** Given Thursday’s market holiday and Friday’s likely limited participation, we’re publishing our weekly early and will return to our regularly scheduled strategy pieces on Monday morning. **

In the week ahead, the market will face a variety of competing influences with the backdrop of geopolitical uncertainty linked to the Israel/Iran conflict. A key unknown as it pertains to geopolitics is whether investors will return to viewing Treasuries as a safe-haven asset in tumultuous times or if the primary drivers will be supply and reflationary angst. The recent price action suggests that the market is oscillating between these two narratives with a nod to the fact that the risk of a broadening conflict in the Middle East has, at times, led to flight-to-quality overshadowing the inflationary pressures from higher oil prices. Moreover, as investor attention rotates away from deficit/supply concerns, we’re left to ponder how comfortable the market is with the 70-80 bp of term premium currently priced into the 10-year sector as adequate compensation for the eventual increase in auction sizes in 2026 and beyond. There is a case to be made that the current level of US rates has adjusted to the realities of larger deficits and is in the process of moving on.

The next few weeks will put this notion to the test as Congress moves forward with attempts to reach a budget deal that Trump will endorse. With more headlines sure to come before the bill is signed, we’ll be watchful of how sensitive US rates are to the political drama at this stage. Our bias is to assume that the market has already exhausted the supply trade and is readying to rotate back to the fundamentals of the real economy and monetary policy. The Israel/Iran conflict is a clear complicating factor for assuming that the incoming data will once again set the tone for US rates, although we suspect that there is a limited period of time that geopolitical developments will dictate the sentiment in financial markets – the next few sessions will likely see the near-term peak.

With the Fed behind us, the array of data next week will offer context for the performance of the real economy as Q2 unfolds. Friday’s core-PCE move is expected to reveal a benign +0.1% monthly gain during May – a pace consistent with the Fed’s inflation objective. The impact of the new tariff regime has yet to be fully reflected in US inflation and is unlikely to be seen until after the summer given Trump’s tariff pauses that we anticipate will be extended in the absence of sufficient bilateral deals. The pace of consumption in May is a greater wildcard at the moment given the mixed retail sales figures. Recall that real personal spending spiked in March at +0.7% and moderated to a more subdued +0.1% move in April. That being said, the Atlanta Fed’s GDPNow tracker is running at 3.5% for Q2 – a solid offset to Q1’s modest decline.

The final coupon auctions of June will, once again, provide the market with yet another opportunity to fret over flagging foreign sponsorship for US Treasuries. To be fair, it appears that investors are worried about the buyers’ strike that never was. We’re optimistic that 2s, 5s, and 7s will receive sufficient demand to provide the market confirmation that investors remain willing underwriters of US debt – at least for the time being. As the final coupon auctions of June, attention will quickly shift toward month-end considerations. SLR will be topical as the Fed meets to discuss lowering capital requirements for banks and there remains an open question regarding whether Treasuries are excluded. The supply side of the Treasury market remains relevant, even as we suspect the evolution of the real economy will define the trajectory of rates in the near- and medium-term…

…Trading View … More cuts starting in summer 2026 implies less in 2027 and upward pressure on the SFRM6/M7 curve, which is currently at some of its flattest levels in over a year. We'll look to enter the trade on a move back toward the local flats.

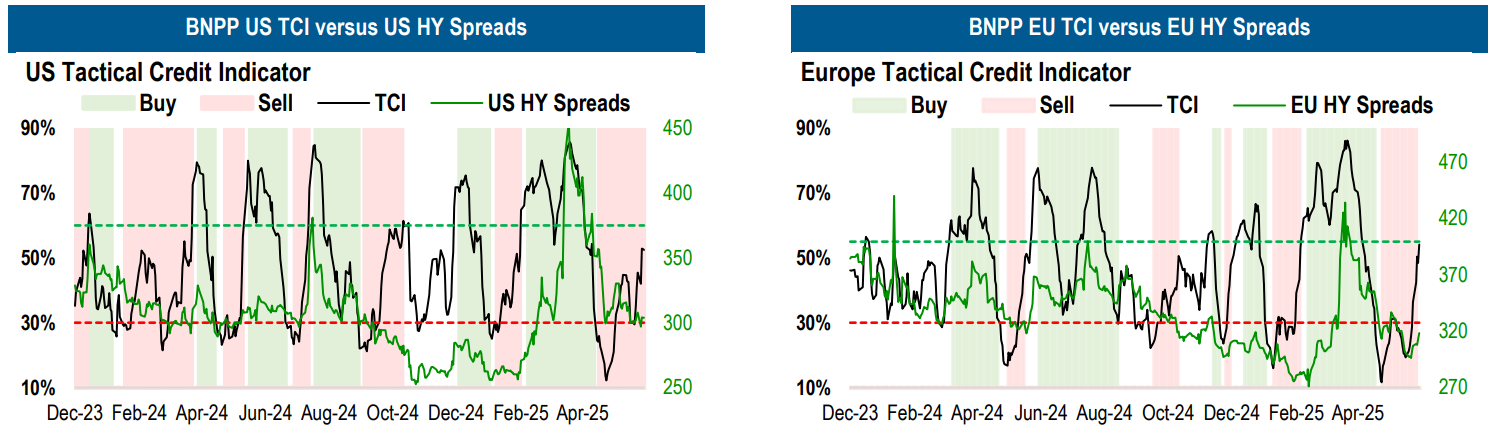

Next up, a note from France TO any / all those involved (tactically) in CREDIT … SELL in the US and HOLD / be neutral in the EZ …

BNPP Tactical Credit Indicator (TCI) – it’s all about the technicals. Credit market technicals explain a significant part of spread moves in the short term. Risk reward becomes favourable when sentiment is bearish, positioning is short and supply/demand flows inflect positively. This is because these conditions create more potential buyers and a lower hurdle is set for good news…

What’s the latest BNPP US TCI signal? Sell. What’s the latest BNPP EU TCI signal? Neutral.

…interrupting these regularly scheduled global MACRO reads for a quick rundown of the techAmental status of things …

US rates have continued to trade within a range in recent weeks. While we expect this to continue in the short term, we note that weekly momentum has crossed lower from 'overbought' territory. This keeps us watching for a break in support levels in US treasury yields.

US 2y yields: We continue to be neutral on yields, with 2y yields looking rangy at the moment, The first key support level is at 3.88% (55d MA). A weekly close below 3.88% would open the door for a move towards stronger support at 3.75% (7 May low), and 3.66% (200w MA).

Resistance on the other hand is likely at 4.02% (200d MA) and 4.07-4.08% (Dec 2024 low, March 2025 high.

For now we think 2y yields will hold in the 3.80% to 4.07-4.08% range.

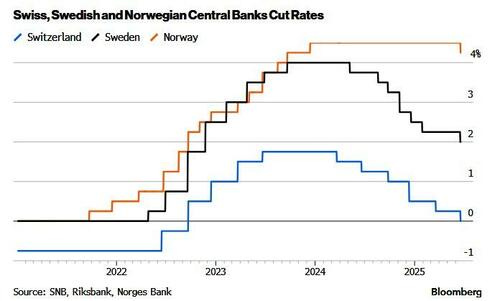

A great recap of ALL global CB activity past 24-48hrs since we last met …

20 June 2025 DBDaily: Surprise cut from Norges; BoE on hold, dovish vote; SNB cut to 0%

… and same shop, with some additional CONTEXT of Earl and CBs …

… Even with the falls this morning, Brent crude has now risen +20.52% since the start of the month, which would make this the biggest monthly jump since November 2020, back when the vaccine announcements offered a path out of the pandemic. So this is still a substantial move …

… In other central bank news, there was a surprise from the Norges Bank yesterday, who cut rates by 25bps, despite widespread expectations for a hold beforehand. Unlike a lot of other central banks, they hadn’t yet cut rates from their peak after the tightening cycle of 2021-23, so it was an important move, and the statement said they felt it was “appropriate to begin a cautious normalisation of the policy rate.” With the decision coming as a surprise, that led to a noticeable weakening in the Norwegian Krone, which fell around a percent against the US Dollar. Otherwise, the Swiss National Bank also cut rates by 25bps yesterday (the sixth consecutive move), but that was in line with expectations. They are now back at zero with the SNB seemingly more likely than not to move into negative territory in the autumn to try to stem the rise in the Swiss Franc and to try to prevent ultra-low inflation from being embedded. There was some relief they didn't do this yesterday though …

A few words ‘bout global CBs …

20 June 2025 ING Rates Spark: Central banks are just as wise as the rest

Markets aren't oblivious to geopolitical risks, but need more to change course. Data shows that Dutch pension funds are adding interest hedges as they prepare for the reforms. Only after transitioning do we anticipate a significant unwind in longer-dated hedges …

…Friday’s events and market view While geopolitical tensions simmer, the week will end on a quieter note in terms of scheduled events. The ECB will publish its economic bulletin and its data on money supply. More interesting could be the consumer confidence reading against the backdrop of international events. The US sees the release of the Philadelphia Fed Business index and the Conference Board’s Leading index. No primary market activity is scheduled.

The upcoming week could provide more insight as we will receive the flash PMIs for June, and on the geopolitical front, all eyes will be on the NATO summit in the Hague. European bond markets will also look to the updated issuance plans for the third quarter from Germany and the EU's funding plans for the second half of the year, and whether they will already reflect some of the prospective increased spending on infrastructure and defence.

From an operation that resides in the very place where NIRP is makin’ it’s comeback …

European powers begin nuclear talks with Iran, and the US has signaled that it does not intend to decide on military strikes against Iran for two weeks. That means two weeks of uncertainty for financial markets, but investors are still inclined to see the Middle East conflict as a local, not a global, economic issue….

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

It would appear the Feds job getting incrementally harder and not just because of it’s current (and mutual) hatred for the executive branch but … the QUALITY of the data …

To calculate CPI inflation, BLS teams collect about 90,000 price quotes every month covering 200 different item categories, and there are several hundred field collectors active across 75 urban areas.

When data is not available, BLS staff typically develop estimates for approximately 10% of the cells in the CPI calculation. However, in May, the share of data in the CPI that is estimated increased to 30%, see chart below.

In other words, almost a third of the prices going into the CPI at the moment are guesses based on other data collections in the CPI.

… TruFLATION dot COM anyone …?

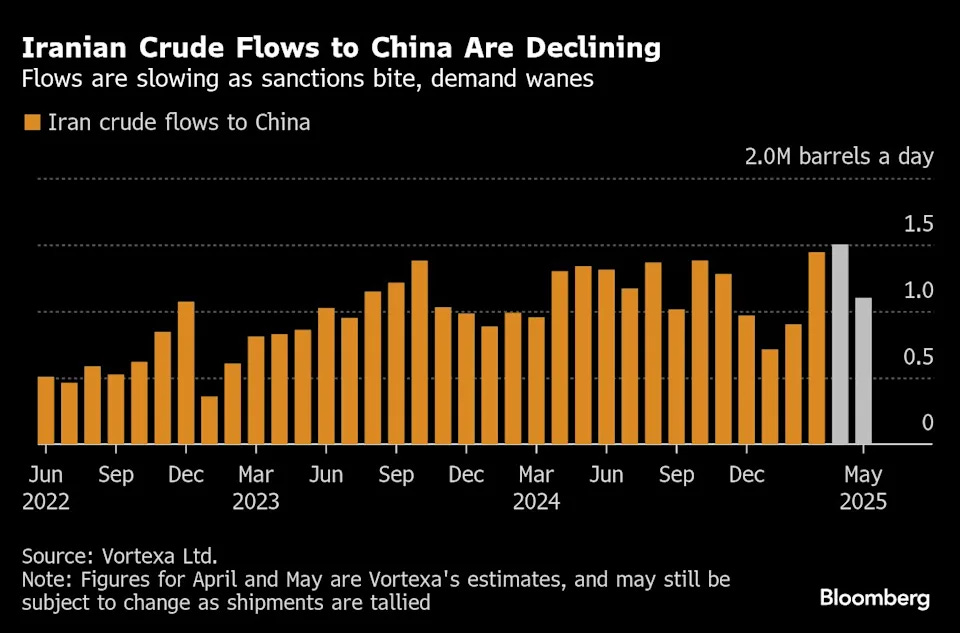

That saying — what what they say AND what they do — comes to mind as we try and track flow of Iranian oil …

June 19, 2025 at 8:13 PM EDT Bloomberg: Xi Shows No Sign of Rescuing Iran as Trump Ramps Up Pressure

… While Xi’s government has provided diplomatic support for Vladimir Putin’s war in Ukraine and shipped dual-use goods to Moscow, China has also been careful not to directly provide weapons in order to avoid US sanctions. Beijing similarly urged de-escalation after its “ironclad friend” Pakistan and India engaged in their worst military confrontation in half a century.

“China may be offering economic relief and rhetorical support to Iran, but actual military intervention is not anywhere near the table yet,” said Wen-Ti Sung, nonresident fellow with the Atlantic Council’s Global China Hub. “China does not want to risk getting entrapped by Iran’s war with an Israel that has the Trump administration behind it.”

An OpED from The Terminal …

June 19, 2025 at 5:00 AM UTC Bloomberg: War and food prices could heat up Powell's summer Uncertainty has given the Fed reasons to pause rate cuts. Here are a couple of more.

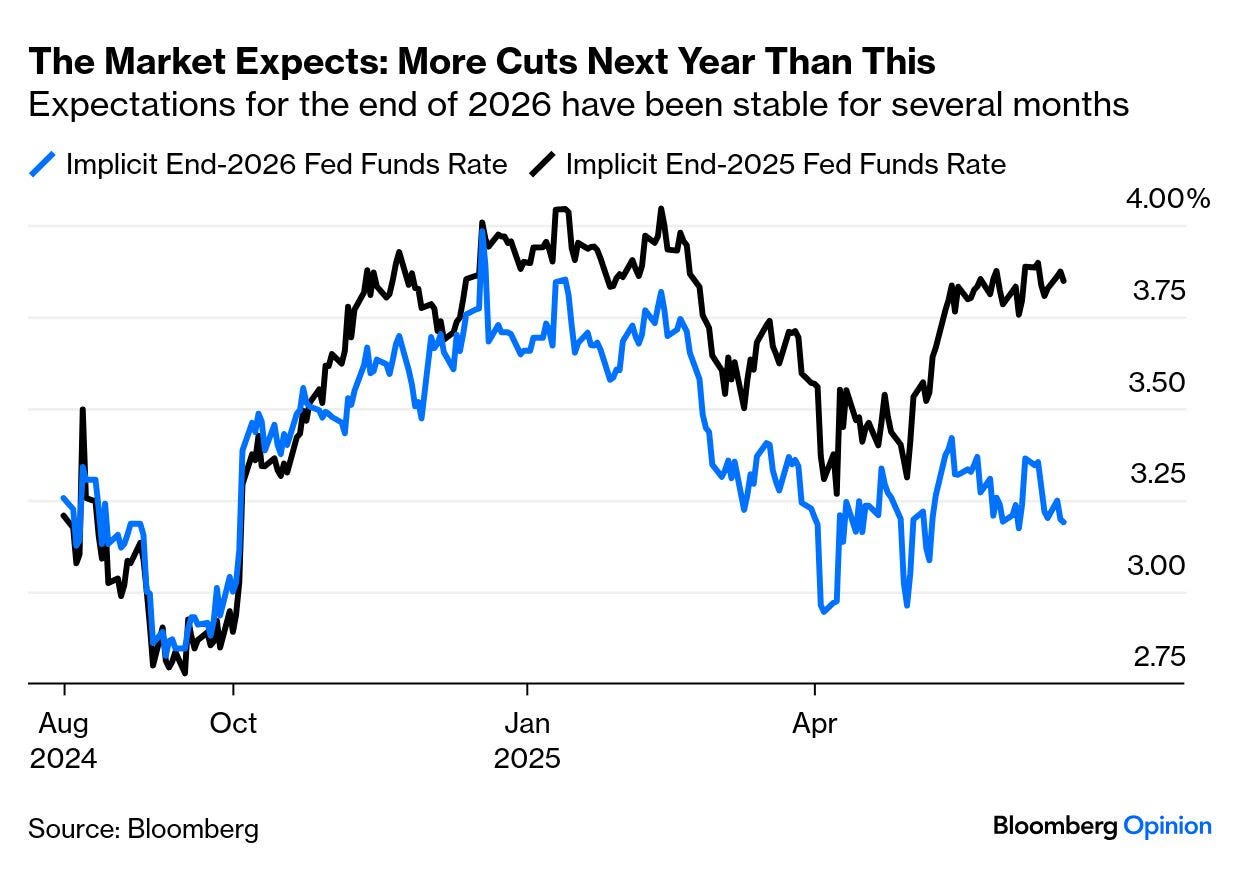

… As might be expected, forecasts diverge more as we look further into the future. The rates market, as gauged by Bloomberg’s World Interest Rate Probabilities function, has consistently predicted that fed funds will be somewhere between 3.0% and 3.25% by the end of next year. That implies a couple of more cuts by then than the Fed currently predicts, which in turn suggests that traders are more worried about growth than the central bankers are:

When it came to economic projections, the dots showed the central bankers growing slightly more negative about growth prospects for next year, while also expecting slightly higher inflation — so stagflationary at the margin, and neutral when it comes to the direction of the next rate move.

Somehow, all of this was taken as dovish enough to prompt a lot of people to buy two-year bonds, which are sensitive to the fed funds rate. But the press conference by Chair Jerome Powell, which started 30 minutes later, reversed almost all of it:

The critical passage from the Powell remarks that moved bond yields back upward was this one:

Ultimately the cost of the tariff has to be paid, and some of it will fall on the end consumer. We know that’s coming, and we just want to see a little bit of that before we make judgments prematurely.

Until the Fed is really confident that tariffs haven’t triggered a significant bump in inflation, in other words, it’s going to have to stay on hold. The risk of a commodity price spike created by the Middle East conflict adds to the arguments to wait and see. To quote Standard Chartered Plc’s Steven Englander, we should “take the summer off.” Englander also suggests that Powell is implicitly arguing for fewer than two cuts this year:

Given the absence of references to softer activity, and how frequently he referred to price increases from tariffs, we think it is possible that Powell was among those who saw zero or one cut.

The Fed chair is only very rarely outvoted, so it’s significant if he is now one of the hawks.

AND a few more thoughts on the FOMC meeting …

Jun 18, 2025 WolfST: Fed See Hotter Inflation for Longer, Higher Unemployment, Slower Growth, “Dot Plot” Shifts More Hawkish but still Sees 2 Cuts in 2025. QT Continues

… Higher interest rates for longer. Today’s median projection for the end of 2025 remained at 3.875%, same as in March, so only 2 cuts of 25 basis points each in 2025, reflecting the Fed’s efforts to grapple with the “uncertainties” – a word that is now standard and plentiful in every Fed communication, from Powell on down.

But there was a shift to no-or-one cut: 7 participants see no cut at all in 2025, up from 4 in March, and 2 participants see only one cut, down from 4. So the the total seeing no or one cut rose to 9 participants. One more participant in that group would lower the median projection to just one cut.

Projections by the 19 FOMC members for the midpoints of the federal funds rate by the end of 2025 (bold = median):

7 see 4.375%: No cuts 2 see 4.125%: 1 cut of 25 basis points 8 see 3.875%: 2 cuts of 25 basis points 2 see 3.625%: 3 cuts of 25 basis points.

Higher forever? The “longer-run” federal funds rate: The median projection for the “longer-run” federal funds rate in 2028 and beyond remained at 3.0%, same as in the SEPs in March and December, and up from 2.9% in September, 2.8% in June, and 2.6% in March last year.

In other words, in 2028 and beyond, the Fed sees the midpoint of the federal funds rate (3.0%) to be 1 percentage point higher than PCE inflation rate (2.0%).

Lastly, but NOT leastly, a few words on GLOBAL CBs from ZH asking / concluding — just how DE/disinflationary ARE TARIFFS, exactly, anyways …

ZH: Liquidity Floodgates Open As 3 Central Banks Unexpectedly Cut Rates In Under 24 Hours

Trump has repeatedly expressed his displeasure with the ECB cutting rates 8 times since the end of the central bank's hiking cycle one year ago; he certainly won't be happy that three other European central banks joined the easing fray overnight as the global economy once again careens toward the abyss.

In the span of less than 24 hours, three rate cuts by three central banks in Europe underscored the dramatic global shift toward policy easing as monetary officials seek to manage "the fallout from Trump’s unpredictable trade policies" as Bloomberg puts it, but really that's just a diversion for the real cause: global economic slowdown now that the last traces of stimulus from the post-covid monetary and fiscal bonanza fade away.

Central bankers in Switzerland and Sweden had suggested as recently as March that they were likely done easing, but the Swiss National Bank instead trimmed borrowing costs by 25 basis points on Thursday - and becoming the first major bank to cut rates back to zero (and in some cases, negative) - following a similar move by Sweden’s Riksbank a day earlier. And an easing pivot by Norway, also on Thursday, was altogether more dramatic, with another quarter-point cut that none of the economists surveyed by Bloomberg predicted.

With policy decisions from at least 18 central banks managing more than 40% of the global economy scheduled for this week, the easing across much of Europe contrasted with a wait-and-see approach predominating around the world. Also on Thursday, the Bank of England held rates but the much more dovish than expected decision (6-3 voted to keep rates unchanged, while expectations were for a 7-2 split) sent the pound sliding.

Meanwhile, the Federal Reserve, and Bank of Japan both held, the first however because it has a political vendetta against Trump...

... and the second because it has no idea how to grow rice anymore and the local population has been crushed by surging food prices which somehow a stronger yen is expected to make better.

All that comes against the backdrop of a July 9 deadline that could see the US reintroduce punitive trade tariffs across the world. Combined with continued uncertainty over the war in Ukraine and a potential US strike on Iran, it’s left some policymakers unwilling or unable to move.

Meanwhile, the reasons for the rate cuts in Sweden, Norway and Switzerland are all linked to inflation, even if the situations diverge.

Swiss consumer prices fell 0.1% from a year ago in May and new SNB forecasts published Thursday show inflation will average just 0.2% this year. That’s primarily due to the haven franc, which has appreciated against the dollar and euro since Trump took office.

Price pressure in Sweden, whose currency has soared against the dollar in 2025, has eased after a temporary spike at the start of the year and as a nascent rebound in the largest Nordic nation has fizzled out. That’s allowing space for more stimulus, Riksbank Governor Erik Thedeen said Wednesday.

The krona has been the best performer this year in the G-10 of major currency holders, surging 15% against the dollar, and also helping to reduce the risk of imported inflation.

In Norway, price growth has been stickier over the last year, partly due to a weaker performance of the krone. Even so, the local core CPI last month matched this year’s lowest level, at 2.8%. The Norwegian central bank now sees headline price growth next year at 2.2%, down from 2.7% seen in March, while this year’s inflation is still seen at 3%.

The three institutions are also at very different stages in their policy paths: Norway’s Thursday move is its first post-pandemic reduction in borrowing costs, while Sweden and Switzerland carried out their seventh and six moves respectively.

Uniting them, however, is the fact that they all may cut again. Riksbank’s Thedeen and Norges Bank Governor Ida Wolden Bache both told reporters as much, while SNB President Martin Schlegel wouldn’t exclude such an option, even if that would push the Swiss rate into negative territory.

Which again begs the question: just how deflationary are tariffs anyway?

Finally, heading in to the weekend, couldn’t really say it better than this and so, Investing DOT COM with what folks will be noodlin’ this weekend …

Investing.com: Investors Face Plethora of Market-Moving Events as Stocks Trade Near All-Time Highs!