while WE slept: USTs in tight range w/modest gains on above avg volumes; Fed f'casts almost ALWAYS wrong 'bout path of FF; 'Bond seasonals turn positive in mid-May...'

Good morning … with the reFUNding kicking off today and duration supply (hopefully creating of it’s own demand) starting in earnest, tomorrow, I’ll begin with a look at the front end, to the best of my now limited capabilities …

3yy: pictures worth 1000 words and so … lighten up on longs? FADE with tight stops? that much is up to you but unless we’re ‘bout to price in rate CUTS (again) a concession of some sort might be needed …

… and with trend / channels / narratives constantly being challenged a couple things to consider …

Bloomberg: Global Bond Rally Faces Supply Test as US Refunding Kicks Off

Powell’s less hawkish remarks and weak jobs fuel bond gains

US to sell $125 billion in 3-, 10- and 30-year debt this week

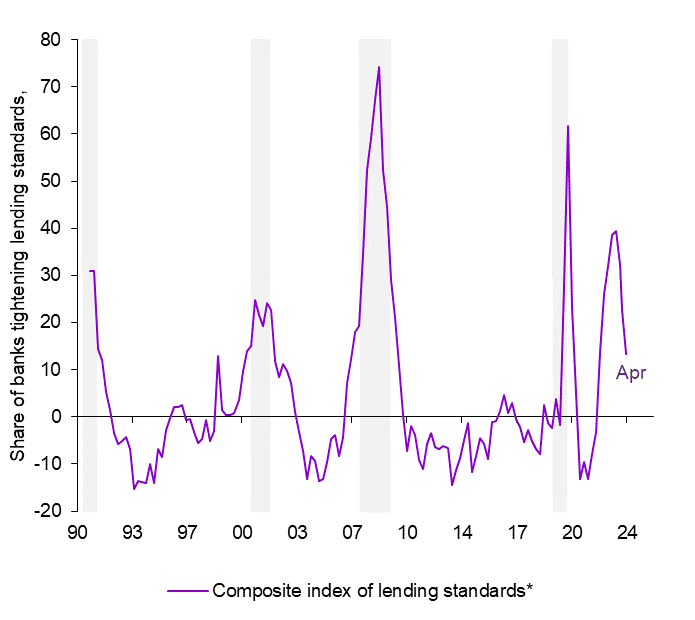

CalculatedRisk: Fed SLOOS Survey: Banks reported Tighter Standards, Weaker Demand for almost All Loan Types

ZH: Where Is "Growth" Coming From? Fed Says Banks Tighten Credit Standards While Loan Demand Drops Further

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are treading a tight but higher range in London after some modest gains (despite belly selling via block flies) in Tokyo-time after the RBA hold (not hawkish as expected). Cash flows in London have featured light selling interest from real$ in the belly, some bank buying in the long-end, but overall limited conviction prevails post-NFP. A $125bn refunding package kicks off with 58bln in 3s at 1pm today, which may garner some concession (already seen some on curve?). Overall volumes are ~120% the 30d average, bouncing back after yesterday’s doldrum-like experience. Gilts are leading the nominal catch-up rally (10s -8bps), with Oil lower (-0.4%) and equity futures mixed (DAX +0.7%, Nasdaq -0.2%). USDJPY is a tad stronger at 154.50.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures mixed, AUD bid post-RBA and geopols continue to dominate; Fed's Kashkari due … Bonds are firmer and extending on the prior day’s gains; Gilts outperform on their return from … USTs are bid but holding a handful of ticks shy of Friday's 109-09+ payrolls peak & the 10yr yield is holding just above 4.45% by extension. Attention turns to the week's supply, with geopols also a key theme.holiday

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

ABNAmro: Bottoming out global manufacturing continues | Insights newsletter

Global manufacturing drops back a bit in April. EMs continue to outperform DMs. Supply side still stronger than demand side. Input price component rises alongside higher commodity prices.

While a full-blown stagflationary US economy remains unlikely, the combination of waning demand and sticky inflation remains a risk for equities. We think the primary headwind comes from margin pressure driven by negative operating leverage, and highlight sectors, industry groups and stocks that are most exposed.

Stagflation rears its ugly head. Our economists believe that stagflation fears are likely exaggerated, particularly after the Fed downplayed the risk of rate hikes. Still, inflation sticking around while growth decelerates would be a net negative for equities. We believe the primary headwind for stocks would stem from negative operating leverage: companies that were able to raise prices alongside inflation are likely to get hit by deteriorating price elasticity as final demand falls, since input cost inflation tends to be stickier….

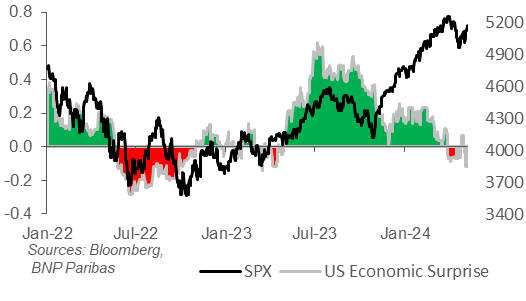

Cooling off: We characterized the regime for US equities back in February as Too Hot. Too hot to be bearish on SPX earnings with a strong nominal growth tailwind. But also too hot for an unchecked equity rally as rates and the pricing out of Fed cuts acted as counterweights. There are now signs of data cooling. Friday’s soft labor market data was a positive surprise for equity markets after a run of five consecutive beats. The NFP miss was eye-catching, but not isolated. It comes against a run of cooler (mainly survey) data. ISM services and manufacturing both missed. Chicago PMI, Conference Board consumer confidence and NFIB small business confidence are all bumping along near post-2020 lows. Economic surprise indices are now turning negative. Equity markets can quickly pivot from worrying about data being too hot to worrying about data being too cold. However, invariably there is a point in between where it feels just right.

Fig. 1: Economic surprise indices turning negative as a Too Hot narrative gives way to something cooler

DB Monthly charts: The waiting is the hardest part

This monthly chartbook highlights our top charts for understanding the current state of the US economy and the outlook for 2024-25. The document features several sections including discussions of: the near-term economic outlook; a better balanced labor market; the bumpy road to price stability; our baseline view for the Fed; and longer-term issues related to growth, inflation and fiscal deficits and debt.

Goldilocks: Senior Loan Officers Report that Credit Standards Tightened and Loan Demand Weakened at a Similar Pace to the Previous Quarter

BOTTOM LINE: The Federal Reserve’s April 2024 Senior Loan Officer Opinion Survey—conducted for bank lending activity over the first quarter of this year—reported that standards for commercial and industrial (C&I) loans tightened at a similar pace to the prior quarter, while a smaller share of banks reported tightening standards for commercial real estate (CRE) loans. Demand for C&I loans in 2024Q1 weakened on net by around the same as during 2023Q4. On the household side, banks’ willingness to lend to consumers improved substantially. Credit standards tightened on net for most residential real estate loan categories but by less than in the previous quarter. The portion of banks tightening credit standards decreased for credit card applications but increased for auto loans. Demand weakened for all residential real estate loan categories and weakened for credit card loans and auto loans on net by slightly more than in the previous quarter.

Economic activity still appears to be growing, as domestic demand remained strong in Q1. However, some early indicators at the start of Q2 (e.g., ISMs, consumer confidence, handful of jobs-related data) have signaled some cooling … On that front, the April Senior Loan Officer Opinion Survey (SLOOS) showed continued tightening of lending standards, albeit slightly less than January's SLOOS surveys. The latest SLOOS survey covered the period from March 25 to April 8 and was made available to Fed officials at the April 30-May 1 FOMC meeting. The SLOOS data do not include an aggregate lending standards measure, but we created one based on a weighted average of individuals loan categories. We estimate a net 13.4% of banks tightened standards on loan-weighted-average basis—down somewhat from 22.6% in January (and 32.2% in October). However, the SLOOS survey captures rates of change—not levels. In other words, a drop in the proportion of banks tightening lending standards does not mean that credit has suddenly become easier to get. If most banks were already close to maximum tightness, the proportion of banks reporting a further tightening has to fall eventually to zero. Demand for credit also remained weak. All in, the takeaway is that there's been some slower incremental tightening in credit conditions, but an outright loosening in credit is nowhere in sight …

A composite index of lending standards* (through April) showed a decline in the proportion of banks tightening lending standards

… US March consumer credit will be released, in the wake of the Federal Reserve’s survey of bank lending standards. That survey suggested consumers were being offered easier terms for credit cards, but demand was limited. Rising real incomes (especially for middle income households) may limit the necessity of applying for credit…

… And from Global Wall Street inbox TO the WWW,

Apollo: The Forecasting Record of the Fed and the Market

The Fed started publishing the dot plot in 2012, and comparing the Fed’s forecasts with the forecasts from Fed funds futures yields three important conclusions, see charts below:

1) The Fed’s and the market’s forecasts about the future path of the Fed funds rate are almost always wrong.

2) The forecasts are very similar, and the Fed has managed to anchor market expectations about where it thinks the Fed funds rate is going.

3) The direction of the forecasting mistake is always identical, suggesting that the market is taking its cue about the future path of interest rates from the Fed’s dot plot.

The good news is that the Fed is able to anchor market expectations, and thereby reduce volatility in financial markets.

The bad news is that when the Fed’s forecast is wrong and the FOMC has to move from three cuts in 2024 to say, one cut, it will hurt Fed credibility.

The US economy’s lower interest-rate sensitivity, combined with strong structural and cyclical tailwinds to growth, brings us to the conclusion that the Fed will not cut interest rates in 2024.

Bloomberg (via ZH): Berkshire's Growing Cash Pile Has A Hidden Message On Stocks (visual of ‘The Buffet Indicator’ always slows me down in my tracks)

… Wall Street, of course, equates higher return with higher risk, but here is one of the best investors of all time decrying the very notion that one needs to do something egregiously risky to earn the additional dollar of return over and above what is available to passive investors who buy the entire market.

Stocks rallied on Friday after the markets interpreted the April non-farm payrolls data as providing just the right backdrop for the Federal Reserve to cut rates eventually. Considering that since of the end of 2022 alone, the S&P 500 has surged about 33% and the Nasdaq almost 50%, one would think that all the good news out there and more is already reflected in their price tag.

Over the long term, stocks can’t yield returns in excess of corporate earnings and economic growth, but investors have been in no mood to listen — and they may yet stay complacent in the short term. The S&P 500 now promises an earnings yield of less than 5%, well below the historical average. The Nasdaq 100 is, of course, trading even loftier, offering a prospective earnings yield of less than 4%.

At the moment, investors are paying a lot for stocks on the premise of promise. That is what Buffett may characterize as too much risk.

Bloomberg: Jane Street and Citadel Securities Race Deeper Into Bond Markets

After conquering stocks, electronic market makers are finally gaining ground in fixed income.

If the financial markets have a religion, we think we know what it is: a deep and abiding faith in the ability of an omniscient Federal Reserve to ride to the rescue if and when the economic weather turns bad…

…Ultimately, if the Fed is going to be successful on inflation, it’s going to need a monetary policy that’s tight enough to hurt real economic growth, as well. That should scare the stock market, and yet the stock market as a whole remains lofty relative to interest rates and profits. This only makes sense if investors believe the Fed will be able to react quickly to economic weakness once it kicks in, without reigniting inflation. Count us skeptical.

… Bond seasonals turn positive in mid-May, providing an additional tailwind. H/t at JayKaeppel

WolfST: Buffett Invests in T-bills instead of Stocks, Waits for Bad Stuff to Happen, Cash is King at 5%-plus

When the Oracle of Omaha gets dark-ish on stocks at these prices, he isn’t taken seriously, suddenly. It’s only when he hypes stocks that everyone jumps in behind him.

DiMartiana Booth w/Kieth@Hedgeye on YT on Fed Day last wk certainly worth a watch & listen!

Great article !!!

A lot of Truth, here.....