Reuters: Biden hopes for ceasefire in days as Israelis, Hamas take part in Qatar talks Biden (keeping in mind please these comments were offered at an ice cream shop with our fearless leader holding a scoop of vanilla on a sugar cone … sending a message … ahead of the primary in Mich … am certain it was NOT lost on those ‘uncommitted’ … )

My hope is by next Monday we’ll have a ceasefire … Ramadan is coming up, and there’s been an agreement by the Israelis that they would not engage in activities during Ramadan, as well, in order to give us time to get all the hostages out …

… AND for somewhat less good news …

Bloomberg (via Yahoo): Japan Two-Year Yield Rises to Highest Since 2011 on BOJ Bets …

… The yield rose 1 basis point to 0.165% after government data showed inflation slowed less than economists estimated last month…

This morning, ahead of todays liquidity event (aka 7yr auction) which comes on the heels of both 2s and 5s …

ZH: Ugly 2Y Auction Tails As Size Jumps To Record $63 Billion ZH: Yields Hit Session High As Bonds Slump After Record 5Y Auction Tails

… AND yields are down a touch this morning despite / because 'all the news’ and so, a quick look at 7yr yields where MY eyes are drawn TO an (interim)UPTREND which is why i’ve etched that sketch in to begin …

7yy DAILY: bullish momentum with some levels of ‘resistance’ to watch within UPTREND

7yy WEEKLY: as you’d expect, weekly momentum quite a different look — BEARISH — within uptrend there is a level to watch … up nearer 4.42%

… #Got7s? … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher this morning as key duration benchmarks sit atop support levels, searching for fresh breezes. Japan's January CPI reading left something for everyone (level high, trend lower), DXY is lower (-0.1%) while front WTI futures are too (-0.5%). Asian stocks were generally higher with Chinese exchanges leading the way, EU and UK share markets are mixed while ES futures are little changed (+0.07%) here at 6:55am. Our overnight US rates flows saw better buying in the 5y-7y sector alongside some curve flattening interest in futures (TY/US block earlier). The desk again noted a distinct lack of conviction from investors here. Overnight Treasury volumes were somehow decent at ~115% of average.

… Another super strong trend is the next one showing JGB 2yr yields which just broke above their early November move high after the latest CPI data. There's a bad print in there but we'd like to draw attention to daily momentum in the lower panel. It's been pinned at 'oversold' levels all month as rates have roughly doubled. It's a good lesson that it pays to wait for closes to confirm momentum flips when you see them emerging (as here yesterday morning).

…. and while NOT quite the l/t visual of JGBs I was hoping for, now, sans a Terminal, welp, it’s about all I’ve seen so far … and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: DXY pressured by JPY post-CPI; Fed's Schmid says no-need to pre-emptively adj. … Session’s focus for fixed income is supply, EGBs stuck near unchanged levels while USTs are a touch firmer

Continued economic resilience has driven a significant paring back in market expectations for Fed & ECB rate cuts. Market expectations are now consistent with our own call for a June start to rate cuts

But what if wage growth – the current obsession of central banks – proves more persistent?

While central banks are likely to gain more confidence in the wage and inflation outlook by June, we think they will need to take a leap of faith in order to avoid the risk of being too late with rate cuts

Regional updates: Economic stagnation is leaving its mark on the eurozone labour market, while in the Netherlands, the period of technical recession has come to an end

In the US, signs of rising financial stress suggest there will still be some slowdown in growth

The Lunar New Year is bringing some green shoots in China, amid ongoing piecemeal stimulus

Global View: June rate cuts will require confidence – rather than certainty – on wages …

… Growth is looking a little better than expected, but driven mostly by the US

… What if rate cuts don’t go according to plan?

…Wage growth is tantalisingly close to target levels in the US; still a way to go in the eurozone

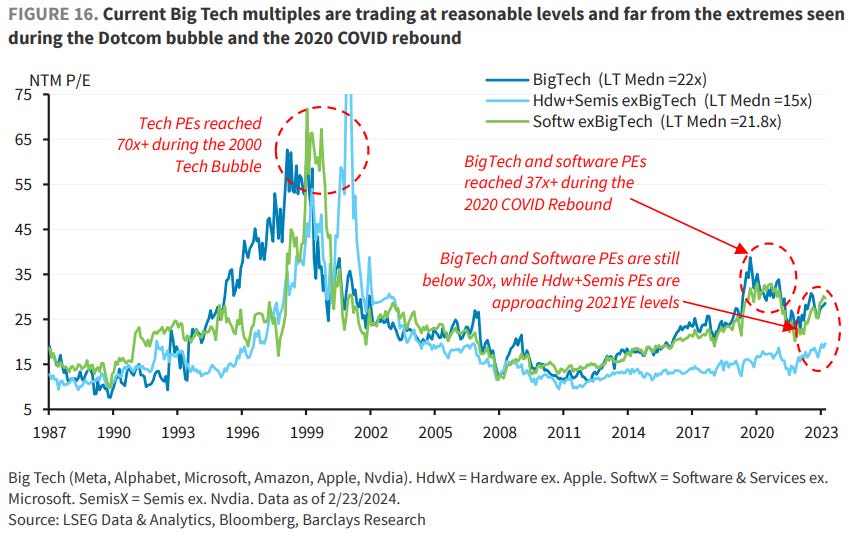

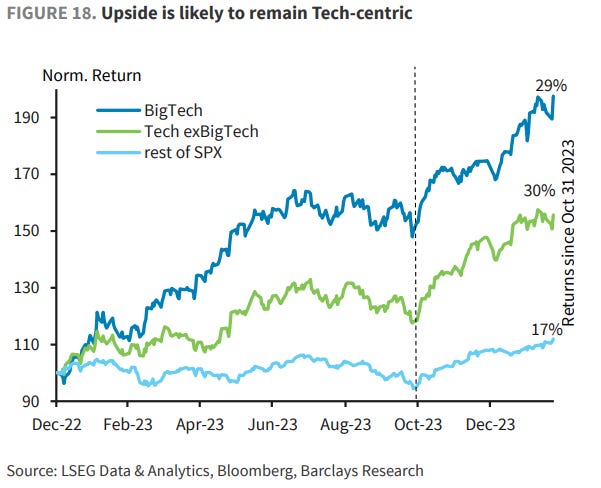

BARCAP U.S. Equity Strategy: Raising 2024 Price Target and EPS Estimates (when the facts change … bla bla bla …)

The US economy continues to defy rates headwinds in 2024, much as mega-cap Tech continues to defy even the most bullish earnings targets. We revisit our own estimates for this year, raising our S&P 500 price target to 5300 from 4800, and our FY24 EPS estimate to $235 from $233.

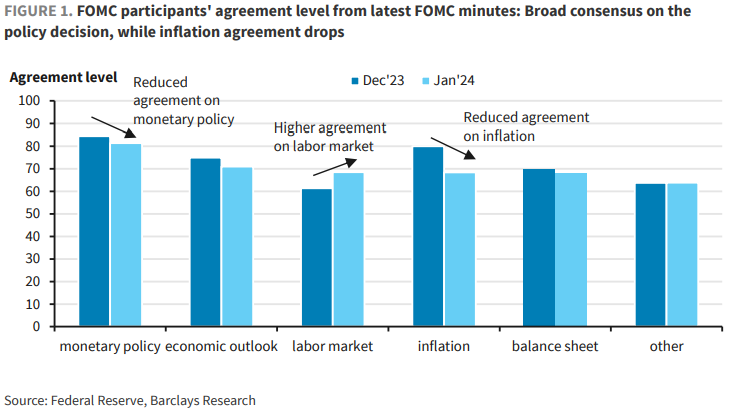

BARCAP FOMC Minutes NLP Analysis: Still near a policy consensus, despite less agreement on inflation

Measures of agreement among FOMC participants on key topics, based on natural language processing (NLP) analysis of meeting minutes, suggest that FOMC participants remain broadly on the same page in terms of policy. Even so, consensus on inflation has diminished as participants highlight differing developments.

BARCAP: January new home sales increased amid signs of continued demand

January new home sales increased 1.5% m/m, to 661k, alongside a 13k downward revision to the prior month. The print highlights higher demand amid steadying mortgage rates. Meanwhile, the median new home price increased, while months' supply was constant at 8.3 months.

Friday’s ISM could point to more cyclical upside: In Too Hot, dated 15 February, we focused on the strength of US data YTD. Hot data is bullish for the cyclical picture but does introduce some tension for equities from upside risks to rates. This week we have a number of Fed speakers and a lot of cyclical data: durable goods, regional Fed surveys, Chicago PMI, Conference Board, and most notably, Manufacturing ISM. Our Economics team expects an above-consensus ISM print of 49.8. In our 2024 outlook, we flagged that the new order/inventories ratio within the ISM has been trending higher for six months. Historically this ratio has led the headline index and points to the potential for a trend back above 50 into expansionary territory.

DB: Fed Notes - (Mid-cycle) Adjusting the Fed's narrative for rate cuts (when the facts change … bla bla bla …)

Recent Fedspeak has sent a clear signal that, although the policy rate has likely peaked and rate cuts are expected to commence this year, officials are not in a rush to lower rates. We have heard much less from Fed officials about how they are thinking about the path beyond the first rate cut.

In this short note we argue that it might be useful to frame the Fed outlook as a two-stage process. In stage one, the Fed delivers a mid-cycle adjustment with a few 25bp rate cuts. In stage two, the Fed undertakes a (potentially lengthy) pause, with further rate reductions requiring evidence of weakening growth or adverse developments in financial conditions.

1. Two shifts in an overall constructive risk picture. Our core views remain centered on a mix of solid US growth and slowing global inflation. That mix is still supportive for risk assets and despite periodic pullbacks, many equity markets (most notably the US, Japan and India) have continued to make new highs. Around this broad path, we would highlight two new developments. First, markets have continued to scale back the extent of rate cuts expected this year, with higher US inflation data for January adding fuel to that shift. We think data over the next couple of months should calm fears of stalling inflation progress. As a result, front-end rate pricing may now have swung too far, though the opportunities still look clearer in Europe. Second, there are tentative signs of improvement in the global manufacturing cycle and perhaps in non-US growth more broadly, which may have scope to extend in the near-term at least. Relief of US inflation fears and better global cyclical news are both potentially “risk-supportive”. If they occur together, they could create a short-term tailwind for cyclical equities and FX, and for non-US equity markets, although we would see this mostly as a further broadening in equity strength rather than a rotation away from the US.

…3. Ranging yields vs trending equities. With Fed pricing now at the lower end of the range of the last 3 months, there is only limited premium against softer inflation or growth data, so entry levels for rate receivers are clearly more attractive. Given the excessive sensitivity of the Euro area rates complex to strong US data, the back-up in EUR rates looks even more compelling to fade since we expect that the ECB will need to cut earlier and more than the Fed this year. UK rate markets are also pricing a lot less easing than we expect in 2024H2. While entry points have improved substantially, the core tenets of our soft-landing view—firm growth and gradual disinflation—work in opposite directions for long rates positions. From a timing perspective, that makes it especially important that upcoming data, especially inflation prints, break in a more benign direction…

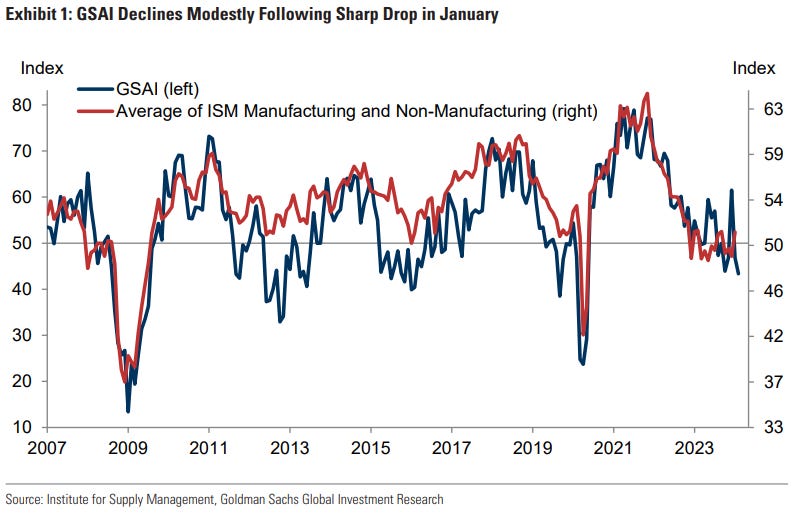

Goldilocks GSAI: Falls Further into Contractionary Territory (in case you were wondering…and the visual as to WHY one might care…)

GS US Economics Analyst: The Price Is Still Too High for Office-to-Multifamily Conversion (oh, okay)

The wide adoption of hybrid work caused a structural decline in office demand. The office vacancy rate increased by 4pp over the last three years to 13.5%, the highest level since 2000. We expect the vacancy rate to rise even further in the next 10 years to 18%, as more firms reduce their demand for office space when their current leases expire. As a result, many existing buildings, especially those that are old and low-quality, may become economically nonviable as offices, raising the question of what can be done with the underutilized space…

…Using a discounted cash flow model, we show that current acquisition costs for struggling offices are still too high for conversion to a multifamily building to be financially feasible once we account for the high additional costs of conversion and financing. For the top 5 metropolitan areas that are most affected by remote work, we estimate that office acquisition prices would need to fall almost 50% for conversion to be financially feasible. This suggests that most of these offices will likely remain underutilized in the near term.

We estimate that the annual conversion rate from office to multifamily will remain low and only increase slowly to 0.7% in the next four years, delivering about 20 thousand additional multifamily units per year. Because the conversion process is slow and costly, available office space is likely to remain excessive and many buildings are likely to remain underutilized. As a result, we expect new office investment to remain sluggish in the next few years, resulting in a 0.2pp drag on fixed private investment growth, which will only be offset modestly by a 0.05pp boost from increasing multifamily construction.

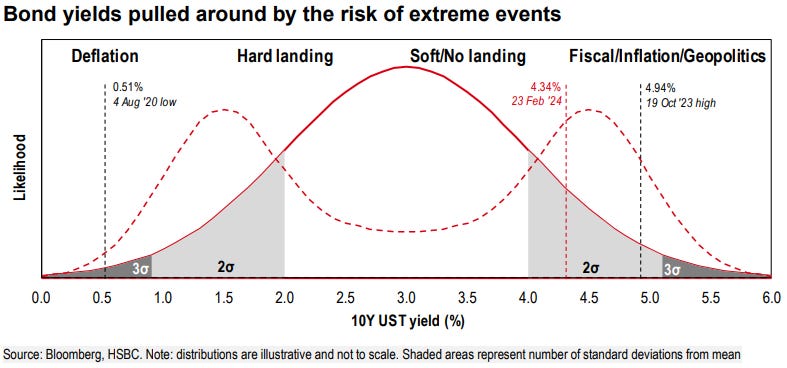

Whether we know it or not we are hedging the risks in our everyday lives. Given a fifty percent chance of rain we might wear a coat or carry an umbrella but given a 10% probability we could well take the risk and leave the brolly at home. When it comes to more serious things, like insuring ourselves and our families against health and life risks – those events with a much lower probability – we are prepared to buy insurance. The difference between the two examples is the impact. We take the risk of getting a bit wet but take what protection we can against life-threatening risks…

… Our diagram below, which is purely for illustrative purposes, presents the likely distribution of yields given a few scenarios. The x-axis starts at zero, has a midpoint of 3.0% and captures yield levels up to 6%. The likelihood of these yields being observed is measured on the y-axis. So, for example, the most likely occurrence – in the illustration it is a soft landing – is at the distribution’s peak.

Through the last decade bond yields roughly followed a normal distribution (that’s the one with the single hump) but the last five years have seen a skew to the right, and one which is not unimodal. We illustrate a bimodal distribution (the dotted line) of a bond market caught between the two extremes. It certainly feels like this sometimes.

Our purpose is to consider how far yields could be pulled either side of an assumed baseline, assuming that policy rates will either be unchanged or go down (#42. Going binary, 11 December 2023). We know from the median path of short rate projections in the “dot plot” that the Fed’s view is consistent with this, so an obvious tail risk is that policy rates go up again, informing the scenarios on the right side of the chart.

For a baseline we imagine 10-year yields would be nearer to the 3.0% midpoint in our chart than the 4.3% in the market today. This is because the policy rate, currently at 5.25-5.50%, is projected to fall towards the 2.5% longer-run equilibrium in the dot plot, and the pure expectations yield1 on the 10-year is pulled down by the lower equilibrium.

The yield on bonds can move a long way from the baseline because of the role of term premium and assumptions on neutral rates. Adding and subtracting term premium, along with changing the assumptions on the equilibrium, is what gets us into the tails of the distribution, above 5% and below 1%.

For example, even if policy rates were on hold for the next two years, and the longer-run equilibrium was assumed to be 150bp higher, at 4.0%, the pure expectations 10-year yield would likely be between 4.5% and 5.0%. Lower yields come from scenarios that include faster and deeper rate cuts, and for this we have COVID-19 data points, with 10-year yields reaching 51bp in August 2020.

To generate scenarios for yields above 5.0% and below 1.0% requires only an extension of our imagination, given the market has traded at these extremes in the last five years. Whether the scenarios play out is hypothetical; it’s the change in the probabilities that matters.

In the bond market a 5-10% increase in the probability of an extreme event means yields could move 10-20bp, assuming the actual event would result in a yield shift of 200bp in each direction. This is what’s been happening recently. At the start of the year futures markets expected US policy rates to be cut by March. Only a few weeks later the easing was repriced for June. Now, after one strong inflation print, there is the tail risk that policy rates may have to go up again.

Markets are being wagged around by the right tail. The usual suspects have been ultra-loose fiscal policy, geopolitical risk, and renewed inflation pressure at a time when it was supposed to have been controlled. We don’t want to belittle these risks but, because we have been experiencing them in recent years, presumably they are already partly in the price.

It’s a neat narrative, this description of why yields could go higher, but it risks blinding us to all the other forces that are out there, not least that yields are already quite high. What about the tail risks on the other side? Another round of financial instability, downside surprise from a data release, even a shift away from the fiscal largesse narrative, would see the left tail wagging…

MS macro DAILY recap (getting the feeling I’ve missed something from Hornbach, Wilson & co …)

USTs end mildly cheaper in supply-laden session; European duration grinds cheaper, ECB's Lagarde cautions on inflation; EUR/USD rises as US-Europe yield differentials tighten; KRW is muted, despite incentive plan; 10y China yields hit new local low; DXY at 103.79 (-0.1%); US 10y at 4.280% (+3.1bp).

… Overall, the housing sector has seen a strong start to 2024, with homebuilder sentiment as measured by the National Association of Home Builders up by 4 points to 48 in February. The 30-year fixed mortgage rate has generally been in retreat since its recent peak in October, providing some relief to the resale market as well.

UBS: CTAs' Positioning and Flows - Biweekly Update

Time to take some profits in equities. Bond selling program on hold

… In rates, CTAs have increased the pace of their bond selling program in the second half of February (sold $40/50mln Dv01 in aggregate). All regions were negatively affected, especially the US where half of the outflows occurred. As a result, CTAs have switched from net long to net short duration in the middle of last week.

Summary New Home Sales Steady in the New Year New home sales rose 1.5% in January, but positive headline growth disguises a less impressive sales volume. January's 661K-unit sales pace is lower than December's initial reading of 664K, which itself was revised down to 651K. October and November sales were also revised down, softening the rebound in sales registered at the end of last year. That said, the new home market is trending in the right direction, and sales were up 1.8% over the year. The steady state of new home sales likely reflects the current mortgage rate environment. Although we have seen significant improvement in mortgage rates over the past few months, the average 30-year fixed mortgage rate stabilized in January at around 6.6%. New home sales are counted at the time of the contract signing, and as such, are more reflective of prevailing mortgage rates than resales are. The median price for a new home rose 1.8% over the month, but prices are still down on an annual basis. The glut of new home supply should help weigh on price growth to an extent, but sellers too are taking advantage of stabilizing interest rates. With mortgage rates falling below 7% heading into the new year, the improving affordability picture has prompted sellers to pull back on offering buyer incentives and price cuts according to the February HMI survey conducted by the National Association of Home Builders. Headwinds seem to be on the horizon for buyers, as mortgage rates have turned back up in recent weeks, with the 30-year average rate rising to 6.9% in the week ending February 22. We expect the new home market to remain in flux until the timing of the FOMC's first rate cut becomes more clear.

The NFIB survey of small businesses asks 10,000 firms if they plan to increase selling prices over the next three months. The recent acceleration in the share of firms saying yes suggests that CPI inflation could increase over the coming months, see chart below.

Bloomberg (via ZH): Stock Rally Driven By A Less Hopeful Start To Year, But...

… Markets have enjoyed the tailwind from economic and earnings expectations being exceeded. The S&P is up ~6.7% year-to-date versus the seasonal average of 1% (to end of February, with data going back to 1980).

That means further equity gains will become more of a grind as results need to deliver more and more to surprise to the upside, with the ongoing risk of what some actual bad news would almost do certainly to prices.

Every day this week, investors will get data on the economy. New home sales today, then capital investment, GDP, consumer incomes and spending, manufacturing, and auto sales are on the list. All of this will feed into the outlook for what the Federal Reserve might do with interest rates this year…

… But 2020-21 was different. Banks were paid to push the money into the economy (remember PPP loans?) and M2 skyrocketed 40.7%. This led to the surge in inflation that followed in 2021-22. Since then, M2 has actually declined 3.2% in 2022-23, taking the steam out of inflation, but so far hasn’t affected economic growth.

But in the last two months of 2023, M2 started growing at a moderate pace again, up at a 4.1% annualized rate. If the Fed keeps it up, not just for one month but as a trend, that would be good news and might even reduce the risk of a recession later this year.

While we watch M2, others have been eyeing the relationship between long and short interest rates. In October 2022, the 3-month Treasury yield rose above the 10-year yield, and has stayed there. This is called an “inverted yield curve” and historically signals that the Fed is tight and a recession is often on the way.

But in an “abundant reserve” monetary policy, higher short-term interest rates no longer signal “tight” reserves. In fact, with reserves so abundant, the Federal Funds Rate is no longer determined in a market, but is actually set at the whim of the Fed. Technically, this is price fixing.

So, the yield curve doesn’t mean what it once did. Longer-term bond yields now are hugely affected by what investors think the Fed might do with rates, rather than how those rates reflect underlying economic trends. The Fed has convinced itself and the markets, that it can move rates up and down with the economic data perfectly, but this is hubris. The Fed has held interest rates below inflation roughly 80% of the time since 2009, leading to distortions in markets and the banking system.

Having said that, with short-term rates no longer excessively low, and the money supply down in the past 18 months, we believe the economy is starting to falter.

Retail sales have declined in three of the past four months. Manufacturing production, excluding the auto sector has declined four months in a row. Meanwhile, home building got hammered, with both housing starts (-14.8%) and completions (-8.1%) dropping sharply while new home sales are down 5.3% in the past four months.

We advise watching the path of M2 to tell how much additional faltering it will do in the year ahead.

Can someone please explain to me in plain English exactly why we should currently ignore the recession signal from the yield curve? Ideally with facts and not just opinions. Seems to me like the yield curve is doing what it typically does when the Fed is tightening policy ...

The Ice Cream Man cometh? I never imagined 'ice cream man' from childhood would much later in lifetime become El Presidente. WTH/WTF is all this supposed to communicate anyways, that Brandon's relatable? After the fall of Kabul, the Taliban showed us their thoughts....

{kind=link}

Very interesting edition !!!

The Ice Cream Man cometh? I never imagined 'ice cream man' from childhood would much later in lifetime become El Presidente. WTH/WTF is all this supposed to communicate anyways, that Brandon's relatable? After the fall of Kabul, the Taliban showed us their thoughts....