while WE slept: USTs higher on light vol; DOTS darts <GO>; "No Landing = Stocks Beat Bonds"; ... and, "Time to worry again about rising interest rates? Stay tuned!" (a MONTHLY look at 10yy)

Good morning … Welcome to the pre-Fed and DOTS darts <GO> edition and it is one which should ought to be EPIC, right? Today’s note is surely NOT.

Debating DOTS <GO> and whether there’s one less cut dot making median now centered around higher for longer, is truly an exercise in futility. YET, plenty of what follows (below, Global Wall) are going to be … ‘thoughts on the dots’ — literally the title of a DB research note … could be summarized by this one picture (credit The MacroTourist / Kevin Muir)

Do we need to know with such an intense level of DOTTED granularity how many think they think something OR can we just … Oh, I dunno … say have a look at …

2yy DAILY:

… or perhaps even ‘Earl …

OIL: BID BUT … a bearish turn in momentum, again the timing of which may be too late for today but helpful IF a meaningful turn lower in energy …

… I know, it’s all X-Earl so then …

CRB: um … higher and rising= no bueno …

… and put the pieces of the DOTTED puzzle together — perhaps even trust our OWN throwing of the DOTS darts — without such fanfare?

Nah. We’re all stoopid and need the ivory towers and their dots which THEN will be followed by dart throwing guesstimates on WHOS WHO in said dots … based on how Global Wall interprets certain commentaries and headlines which will follow.

Shakin’ my head cuz I don’t get it … maybe cuz I’m out of that seat now (for better or worse) … I’ll move right along.

And as I do, I’ll note, Starts, Permits SURGED …

ZH: Housing Starts And Permits Surged In February (Despite Plunging Rate-Cut Odds)

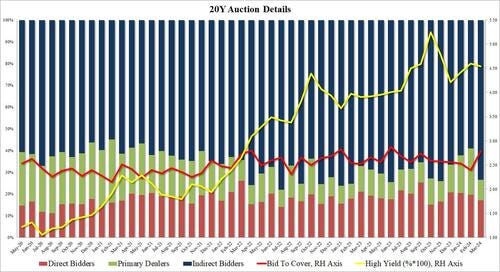

… and after the data surged, we then got … higher rates (aka concession) to help find demand for 20s, right? NOPE …

ZH: Stellar 20Y Auction Sees Surge In Foreign Demand, Biggest Stop Through In More Than A Year

… The internals were also stellar with Indirects awarded 73.5%, a surge vs the 59.1% last month, and just shy of the highest on record. And with Directs awarded 17.2%, below last month's 19.7% which also was the six-auction average, Dealers were left holding just 9.3%, one of the lowest Dealer awards on record.

Overall, this was a stellar auction, and news of the blowout demand helped send yields to session lows across the curve, which in turn also helped propel duration equivalents (read tech names) to session highs, with the S&P rising to session highs just as the auction broke for trading.

Nevermind … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher amid light 75% trading volumes with Japan out for Vernal Equinox Day, though FX markets are running with USD-strength (JPY -0.4%) amid a small commodity pullback (Cl -1%, HG -0.75%). Our London traders noted their session began with better selling in 20s which carried over out the curve, causing a slight steepening. The selling was partially offset by demand in 2s-5s from real money, however conviction levels pre-Fed are patently low. S&P futures are flat here at 7am, EGBs outperforming USTs ~1-2bps after Lagarde re-iterated the ‘more info by June’ mantra. 2s10s curve -0.3bps, 2s5s10s fly -0.25bps richer.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities softer, DXY firmer benefiting from a weaker Yen, Bonds bullish post-UK CPI; FOMC due … Bonds hold a bullish bias following softer UK CPI, as attention turns to the FOMC

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … and arguably having spilled all this ink on upcoming DOTS, cannot think of a much bigger waste of their time because just after the press conference, the snoglobe will be settling and Global Wall will head right back to work rewriting the script. And so a bigger waste of time you’ll ALMOST have a harder time finding … me reading it all and excerpting some of it AND then you continuing to read this? Well … I’m sorry but here goes …

ABNAmro: Macro Watch - Wage growth: How far does it need to fall? | Insights newsletter

The key to disinflation continuing will be a timely normalization in wage growth

We estimate wage growth needs to fall to ranges of 2.7-3.0% for the eurozone, 2.2-2.8% for the Netherlands, and 3.3-4.0% for the US in order for to inflation to fall to – and stay at – 2%

But central banks will likely cut rates before wages fall this far – otherwise they could be too late

This is due to the lags with which monetary policy affects the economy

Wage growth is driven by future inflation expectations, labour market tightness, and the catch-up of nominal wages and the price level. We take stock of developments in these channels

Wage growth in the eurozone still has a significant way to fall, and Q1 data will prove key

Businesses likely have space to accommodate some further increases in wages, meaning wage growth does not immediately have to fall back to target-consistent levels

We include an Appendix in which we explain the various measures of wage growth

BARCAP U.S. Equity Strategy: Buybacks Pick Up Into Year-End (decent note ‘bout an important source of demand)

4Q23 earnings supported strong cash generation, helping to offset lower net debt & equity issuance. Companies drew down cash reserves in 4Q23 for the first time in roughly a year, funding a small number of large M&A transactions but also incremental buybacks and capex.

BNP US Equities: Quarter-end selling, much ado about nothing

Quarter-end selling is likely to become a topic of attention in the coming week. US equities have now rallied >10% QTD relative to fixed income (SPX +8.3%, LBUSTRUU -1.8%). This move could trigger significant rebalancing flows into quarter-end. Our model estimates ~$80bn of equity selling flow. However, we would be very cautious about reading much into the possible market impact.

… As we arrive at another Fed decision day, markets have posted further advances ahead of the announcement, with both the S&P 500 (+0.56%) and Europe’s STOXX 600 (+0.26%) moving higher. However, there were growing warnings under the surface, particularly on the inflation side, as Brent crude oil prices closed above $87/bbl for the first time since October. So it’s clear there are several price pressures in the pipeline, which has led to fresh doubts about whether we’ll get rate cuts by the summer after all. Moreover, there are increasing signs that investors are pricing this in, with US 1yr inflation swaps inching up to 2.64%, their highest level since October, even as bond yields eased off from Monday’s 3-month highs…

… Given those developments on the inflation side, there’s been growing speculation about whether the Fed might signal fewer than three cuts in today’s dot plot. Indeed, it’s worth noting that back in December, 8 of the 19 officials already had two rate cuts or less for 2024, so it would only take two other officials to shift hawkishly for the median dot to move up to two cuts. In their preview (link here), DB’s US economists expect the median dot to remain at three cuts in 2024, but they think the Fed will raise their 2025 and 2026 dots slightly to show less easing further out. That will be significant if so, as the post-pandemic dot plots repeatedly moved the dots up or held them steady at every meeting, up until December, when the dots finally moved lower compared to the meeting before. So if this March dot plot does move the dots higher again, it will make the dovish shift in December look more like a blip than a turning point…

The SEP dots are a key point of focus for tomorrow’s FOMC meeting, with attention in particular on prospects that the median 2024 and longer-run dots could shift up. Both medians are fragile, in that it would take only two upward revisions to the underlying projections to move them. This piece runs through our thinking on the likelihood and market impact of upward shifts in these dots.

We argue that the likelihood of a 25bp shift up in the median 2024 dot is roughly even but that a move higher would likely have only modest effects on yields. Given elevated uncertainty, a shift probably doesn’t convey much about the likely policy path this year, and paradoxically the probability of delivering three or more cuts may actually be higher with an SEP that shows just two.

The median longer-run dot is also a close call but given building evidence of higher r-star as well as recent Fed communications warming to the prospect, we expect it to move up slightly. However, the market is already pricing a much higher longer-run fed funds rate than in the SEP, and against this backdrop the historical response to longer-run dot surprises suggests a move tomorrow would have relatively little effect on 5y5y and other far-forward rates.

Goldilocks: Rethinking Neutral: The Fed’s Next Big Debate (…and the hits they keep on comin…)

■ We argued last cycle that the long-run neutral rate was not as low as widely thought, perhaps closer to 3-3.5% in nominal terms than to 2-2.5%. We have also argued this cycle that the short-run neutral rate could be higher still because the fiscal deficit is much larger than usual—in fact, estimates of the elasticity of the neutral rate to the deficit suggest that the wider deficit might boost the short-term neutral rate by 1-1.5pp. Fed economists have also offered another reason why the short-term neutral rate might be elevated, namely that broad financial conditions have not tightened commensurately with the rise in the funds rate, limiting transmission to the economy.

■ Over the coming year, Fed officials are likely to debate whether the neutral rate is still as low as they assumed last cycle and as the dot plot implies. Their thinking is likely to be influenced by distant forward market rates, which have risen 1-2pp since the pre-pandemic years to about 4%; by model-based estimates of neutral, whose earlier real-time values have been revised up by roughly 0.5pp on average to about 3.5% nominal and whose latest values are little changed; and by their perception of how well the economy is performing at the current level of the funds rate.

■ We expect Fed officials to raise their estimates of neutral over time both by raising their long-run neutral rate dots somewhat and by concluding that short-run neutral is currently higher than long-run neutral. While we are fairly confident that Fed officials will not be comfortable leaving the funds rate in the 5s indefinitely and will not go all the way back to 2.5% purely in the name of normalization, we are quite uncertain about where in between they will land. For now, we are penciling in a terminal rate of 3.25-3.5% this cycle, 100bp above the peak reached last cycle.

… Market perceptions of the neutral rate—specifically distant forward interest rates at a horizon where investors do not have strong views on the cyclical state of the economy—have risen substantially since the pre-pandemic years, as shown in Exhibit 1. While no market measure perfectly captures the economic concept of neutral, common market-based approximations now suggest a nominal neutral rate of around 4%, a 1-2pp increase from the pre-pandemic years…

… For now, we are penciling in a terminal rate of 3.25-3.5% this cycle, 100bp above the peak reached last cycle. This reflects both our view that neutral is higher than Fed officials think and our expectation that their thinking will evolve.

Goldilocks: The Fed and Neutral—Refocusing on the Risks (…and the hits they keep on comin…)

■ Longer-term rates have fallen in recent months as market focus turned to the upcoming easing cycle. We observed last year that market pricing of the neutral rate seems to be linked more to Fed shifts and the behavior of the economy in response to policy settings than to new macro information.

■ The market has already been reassessing the policy path in recent weeks, but much of that focus has been on the near-term outlook—so while the market has priced out near-term easing, it has not revised higher its view of where short rates will settle in the deeper future. That has started to change over the last several days.

■ We think the risks are now higher than they have been that this repricing higher in longer-dated rates continues. This week’s Fed meeting could, as it has in the past, serve to refocus investors on the question of whether neutral rate pricing should be higher.

■ If the median Fed dot shows fewer cuts, or if the long-run dot does begin to drift up, we think there is a risk that a more hawkish than expected outcome at this week’s FOMC meeting would challenge market views of the potential future funds rate distribution.

■ In that kind of scenario, the risk is that the market changes its view of the longer-term policy path as well and that long-end rates keep better pace than usual with the front. Implied vols on 10- and 30-year swaptions are lower than they have been in some time, so longer-dated payer swaptions may offer good protection against the risk that the market again reassesses its views on where longer-run rates might ultimately end.

Recent reassessment of the policy path has been more focused on the near- than the long-term policy path

Goldilocks: Office Mortgages Are Living on Borrowed Time (hmmm, seems like another one for Team Rate CUT — someone keeping track? I mean the CMEs FedWatch Tool always keeping track, I suppose, as is, the front-end of the curve and the yield curve itself, right? anyways, seems like nuttin’ to see here folks, back to our cars, shows over…)

■ In the face of a substantial debt maturity wall for the commercial mortgage market, a historically high amount of debt has been extended and modified rather than refinanced, particularly for office loans. The amount of outstanding commercial mortgages set to mature by year-end 2024 has grown from $658 billion at the start of last year to $929 billion today. This trend has helped mitigate a default wave and a sharp pick-up in losses on CRE loan portfolios. While extensions and modifications are not unusual phenomena in the CRE market, particularly during times of rising financial distress and tight lending conditions, the low likelihood that funding costs revert to pre-COVID levels begs the question: how long can this trend continue?

■ We expect the wave of modifications to persist in the near term as refinancing stays uneconomical for most commercial real estate borrowers, while foreclosures remain an unappealing proposition for lenders in an illiquid property market. That said, the risks of this trend breaking have undoubtedly risen. The ongoing downward pressure on office property prices and net operating income growth could push borrowers to strategically default, while the ability of balance-sheet constrained lenders to continue to amend and extend loans could diminish over time. Nonetheless, we think systemic risks remain low even if liquidations take the upper hand over modifications. In our view, the risk of negative feedback loop of distressed sales and lower property prices is largely contained to the office sector. Moreover, banks have generally raised allowances for CRE loan losses, while the exposure of banks to real estate remains lower than past periods of crisis.

Single-family starts post a punchy 117K gain in February, though multifamily activity remains fairly weak. The housing market index reached an eight-month high.

…It is now the turn of the Fed, with a policy decision and the roulette wheel of opinions that Fed Chair Powell’s press conferences represent. We also get the fabled dot plots—an attempt to offer misleading precision as to the views of individual FOMC members. Discussions about slowing the pace of quantitative tightening are likely to be elaborated with the minutes.

The press conference will set expectations for rate cuts, leaving markets at the mercy of Fed Chair Powell’s whimsical communication style. Financial “markets” are not a single entity pricing in rate cuts—many bond investors will never have speculated in Fed funds futures, for instance…

UBS: Big Tech Rally on Borrowed Time (Golub…folks love them some Golub)

While 2024 EPS growth and revisions for Big Tech remain above market, earnings momentum is projected to decelerate, a potential headwind.

EPS Growth: Big 6

Wells Fargo: Bank of Japan Exits Negative Interest Rate Policy

Summary

In a historic—albeit well-anticipated—policy shift, the Bank of Japan (BoJ) formally ended its ultra-easy and nonconventional monetary stance at today's monetary policy announcement.

The BoJ hiked rates for the first time since 2007, exiting negative interest rates and saying it would encourage the uncollateralized overnight call rate to remain at around 0.00% to 0.10%. The central bank also formally ended its Yield Curve Control policy, but said it would continue to buy Japanese government bonds.

The large pay increase announced by Japan's largest labor union federation as part of the Spring wage talks was clearly a key factor behind today's policy shift, and the central bank judged “it came in sight that the price stability target of 2 percent would be achieved in a sustainable and stable manner” over time.

The BoJ did not offer clear guidance of further monetary tightening. However, so long as trends in Japan's economic growth and wage and price inflation remain reasonably constructive going forward, we expect the central bank to lift the target range for the uncollateralized overnight call rate by 10 bps, to 0.10% to 0.20%, at its October monetary policy meeting. We also see the risks as tilted to further monetary tightening in 2025.

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: Inflation is Back Baby! (#MagazineCover alert, Bob Farrell rules? something?)

…Interest rates went out yesterday at their highest levels since November.

Do you really believe that the 10-year yield keeps going up because interest rates are going down?

lol

There are people who actually believe that.

So for us, who actually take the time to look, we know that it's the exact opposite.

Commodities are heading higher. And Interest Rates are rising with them.

Here is Gasoline looking to complete a huge base, and about to go much much higher.

Meanwhile, the Bond market is already pricing in higher inflation.

Most investors are not ready for this.

And by "most investors", I mean almost no investors.

We have the data.

There is a huge squeeze setting up and investors not prepared for these inflationary pressures are about to get steamrolled…

Bespoke: What's in Store from the Fed? (funTERtaining info graphic on the S&P by Fed chairman…)

… The Fed is currently meeting to make a decision on what to do with the Fed Funds Rate. Any moves the Fed decides to make will be announced tomorrow at 2 PM ET, followed by a press conference from Chair Powell a half hour later. Historically, a decent-sized chunk of the stock market's move has come from its reaction on Fed Days.

We have a database of the stock market's intraday action across all Fed Days since 1994. (Prior to 1994, interest rate decisions made by the Fed were not announced until weeks after its meetings.)

Using our database, we've made a composite chart showing the S&P's average intraday path on Fed Days broken up by Fed Chair. (See below.)

As you can see, Ben Bernanke saw the biggest stock market gains on Fed Days while he was Chair, with the S&P up an average of 0.55% across all Bernanke Fed Days. Alan Greenspan and Janet Yellen both saw average Fed-Day gains in the high-teens (in basis points). Finally, while his days as Fed Chair are still ongoing, Chair Powell has thus far seen the smallest upside market move on Fed Days since he became Chair. While there have certainly been outlier days, the hallmark pattern of Powell Fed Days has been an initial pump-fake rally in the 30-45 minutes after the 2 PM ET rate decision followed by significant selling in the final 60-75 minutes of the trading day.

Of course, past performance is no guarantee of future results. Let's see what tomorrow's Fed Day brings!

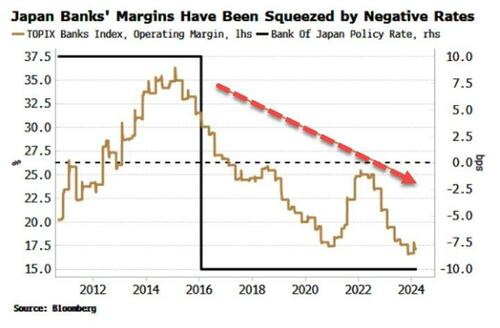

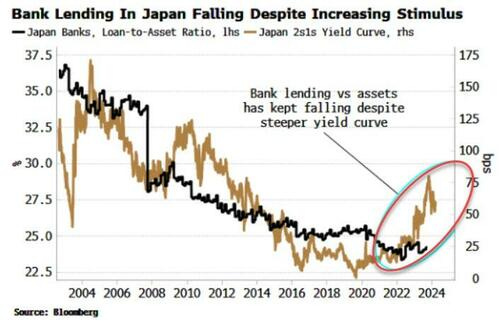

Bloomberg(via ZH): Why The BOJ's Rate-Hike Is Actually Good For Markets (little bit diff / interesting take…)

… In Japan, banks’ operating margin began falling soon after the BOJ took its policy rate negative in 2016.

That’s also been reflected in bank lending. The yield curve is traditionally a good signifier of banks’ profitability and hence their propensity to lend. But banks’ loans relative to their assets in Japan have continued to fall despite the steepening of the yield curve over the last two years. Negative rates are the likely culprit.

If negative rates have been restrictive, then exiting them is set to be stimulative – especially if, as is the case in Japan, the rise in rates is likely to be gradual and modest despite rising price growth, underscored by BOJ governor Ueda’s comments after today’s rate decision that “there is still some distance to 2%” inflation.

Why the inertia? Decades of low inflation have left the BOJ with a blind spot to price growth that is becoming problematic. Headline CPI in Japan is falling but remains at all-time highs outside of consumption-tax hikes, while core-core CPI is stuck near its peak. Under the surface, there are signs that inflation is becoming more embedded, with almost all inputs to the CPI basket rising over the last year, much higher than at any other time ex-consumption tax rises…

… But Japan’s large net creditor position (the world’s biggest) means that a trickle of currency hedging by domestic holders of foreign assets could turn into a flood. The backdrop of a weaker yen has encouraged investors to become underhedged. Life insurers, one of the largest currency hedgers, are representative, letting their hedge ratios drop to under 50% over the last few years.

FX hedging will push the yen stronger, eliciting yet more hedging. It is this dynamic that drove USDJPY to rapidly drop 20% through the first half of 2016 (which can be seen in the rise in the hedge ratio around that time in the above chart). The 500-1 odds offered on USDJPY touching 130 by the end of Q2 – a level it was at little more than a year ago – sound very generous.

If inflation becomes ingrained, then eventually the yen will succumb to it, but in the shorter term, hedging flows as well as capital repatriation are likely to be the currency’s bigger driver. That also means an added fillip to unhedged foreign holders of Japanese assets.

Bloomberg: Inflation fears bloom for the Fed's rite of spring (Authers’ OpEd for a single visual, reminder)

Overheating in the economy is now seen as a bigger risk than recession in yet one more strike against rate cuts.

… Comparing the performance of the biggest exchange-traded funds tracking the S&P 500 and Bloomberg’s index of 20-year or longer Treasury bonds (universally known by their ticker symbols SPY and TLT), there were a few months at the end of 2023, as the Fed prepared the way to pivot from higher rates, when bonds at last managed to outperform. Those have now been more than canceled out as the S&P reaches new highs relative to bonds:

KIMBLE: 10 Year Bond Yield Testing Key Resistance This Month!

The 10-year treasury bond yield is very closely watched by banks, consumers, and active investors. It is used as a measuring stick for interest rates on loans, bond auctions, etc.

When the 10-year treasury bond yield goes higher, so do interest rates on mortgages, personal loans, and car loans. And the government pays higher interest on some of its treasury-bill auctions.

Today we look at a “monthly” chart of the 10-year treasury bond yield and highlight a key price resistance level that may dictate the next move for interest rates.

As you can see, the 10-year bond yield bounced off the 23.6 Fibonacci level at (1) and is testing a key resistance level – its prior highs – at (2).

Should the 10-year bond yield breakout at (2), look for it to rally to the 4.9% level.

Time to worry again about rising interest rates? Stay tuned!

AND … what those who were thinking about 7 rate cuts coming in to the year are might be thinking …

Was gonna mention that Bloomberg-SW piece yesterday but it popped soon after you Sent so figured you'd catch it; yup so interesting a take required me a reread!

I have a hard time accepting that 'Dot-Mania' is a reality today :(

MacroTourist is a funny bastard, I only enjoyed a few early COVID months before he went Paywall :(

MOAS-mother of all stimulus pre CARES-Act, may've been 1 of the most prescient calls in modern financial history. If only I had Been 1 with the Bubble :(

Was gonna mention that Bloomberg-SW piece yesterday but it popped soon after you Sent so figured you'd catch it; yup so interesting a take required me a reread!

I have a hard time accepting that 'Dot-Mania' is a reality today :(

MacroTourist is a funny bastard, I only enjoyed a few early COVID months before he went Paywall :(

MOAS-mother of all stimulus pre CARES-Act, may've been 1 of the most prescient calls in modern financial history. If only I had Been 1 with the Bubble :(