Good morning … It’s being said that last week was the best week for stocks in 2024 … it’s ALSO said in context of arriving just after the very worse week for stocks in 2024.

Meanwhile, back in the rates space, 2yy are hovering in / around 5% as all benchmarks taking a slight step back from respective ledges.

This on heels of Friday evening’s latest bank casualty which by now, may just be far enough removed that we’re um … NOT talkin’ about IT … Make of that whatever you will. That all said, it’s hard NOT to begin any sort of morning market comment without some sort of look at Yen move and so …

ZH: 'FX Vigilantes' Strike - Yen Suddenly Crashes To April 1990 Lows Against The Dollar

ZH: "What Is The Sound Of One Hand Clapping" Asks BOJ Head Ueda As The Yen Collapses

… and on THAT note, it does appear BoJ currently in the denying … or really NO COMMENT camp and so … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher and the curve flatter this morning after in-line German state CPIs this morning and possible intervention (Japan was actually out for the beginning of Golden Week) to support the yen after JPY briefly spiked over 160 (see attachments). DXY is lower (-0.25%) while front WTI futures are little changed (-0.2%). Asian stocks were higher, EU and UK share markets are mixed while ES futures are showing +0.2% here at 6:45am. Our overnight US rates flows saw a quiet start to the week with Tokyo shut for holiday. In London's AM hours, the desk has seen better real$ buying in the belly- but on light volumes with few willing to engage on the other side. 2s5s10s is -1bp richer, and we illustrate via today's attachments why this emerging belly outperformance could persist. Overnight Treasury volume was unavailable as the Tokyo holiday messed with our sheet.

… The first looks at Treasury 5yrs and the recent price action around their 4.72% support (derived by a mid-November high yield print that was rejected then). If you squint and look in the lower panel you can see that daily momentum may be flipping bullishly this morning after being pinned at 'oversold' readings for much of this month. 5's therefore appear like they want to turn bullishly, but we'll wait to see if today's close confirms a flip. If momentum turns with a close confirming it, our gaze will then shift toward the 4.35% area and the potential for a re-visit to this former range support...

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures modestly firmer, JPY bid amid suspected intervention, Bonds benefit from Spanish/German CPIs … Bonds are firmer benefiting from dovish Spanish/German inflation metrics … USTs are bid with specifics light so far and direction drawn from EGB action after the regions core inflation numbers from Spain & German. Currently at the top-end of a 107-18+ to 107-27+ range with the 10yr yield below 4.65% but in familiar ranges.

Reuters Morning Bid: Yen bounces on 160 per dollar in busy Fed-led week(VISUAL of “Japan’s history of supporting yen”)

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ (in addition TO what I cobbled together and passed along over the weekend — where it seems to me, calls are once again being ‘updated’ and once that last bond bull on Team Rate CUT throws in the towel (generally speaking), it’s just THEN we’re likely to see a real bid manifest itself ) …

Fed policy, Treasury supply, and the state of the labor market are in focus as markets look for a catalyst to reverse the move in US yields.

We are skeptical that the coming week will provide such an impulse: recent inflation news has reset the timeline to the Fed feeling confident in rate cuts and eroded our prior view that markets should react asymmetrically to weaker growth news.

We take the BoJ decision as a clear signal that the path of least resistance is for continued JPY weakness, but we expect the threat of intervention to keep the trajectory somewhat gradual.

Markets head into a packed week in the US which will shed light onto the outlook for Fed policy, Treasury supply, and the health of the labor market. While last week saw US yields reach their highest levels since early November, US financial conditions have only just unwound the bulk of easing since the December FOMC (Figure 1).

…That said, where earlier in the year we saw a clear asymmetry in market response to growth weakness, the reacceleration in inflation and sustained labor market strength leave risks more balanced, in our view. We think that an upside surprise could see markets take out cuts entirely over the next several meetings for the first time since last October (Figure 3) alongside a higher terminal rate being priced. A clear disappointment would be likely to see the market put cuts back in, but where soft inflation put the burden of proof on accumulated growth data to take yields higher at the start of this year, firm inflation and sustained resilience since then have put a greater burden on a clear signal of loss in economic momentum that reinvigorates conviction in disinflationary pressure.

DB: What next, now that excess Money growth and inflation have converged

M2 cumulative growth above trend, has slowed to the point where at ~12%, it is very close to the cumulative CPI growth above pre-COVID trends. At one point cumulative M2 growth was tracking ~15% above the cumulative CPI pre-COVID trend.

More generally, we see a pattern where there is not much divergence between the nominal M2 pre-COVID based trend overshoots, and nominal GDP (Figure 3), and other nominal variables like retail sales (Figure 17) and hourly wages (Figure 13).

On the real economy side, major real variables inclusive of real GDP (Figure 4); and real PCE (Figure 18) are tracking marginally above pre-COVID trends, while establishment NFP employment (Figure 16), but not household employment (Figures 15) is a little below trend. Within PCE, goods consumption are still above pre-COVID trends, and services looks to have also edged to pre-COVID levels

This tends to work with a central idea, that as a monetary shock works its way through the system, its effects over the longer-term, are ultimately nominal, while beyond the short-term, the long-term real effects are limited (and may even be negative, IF inflation is high enough or sticky enough, to disrupt price signalling).

If you take this picture in its entirety, the COVID money supply surge, imparted by both monetary policy and the related monetization of the fiscal stimulus, is now running its course, and slowly winding down, and this fits with an advanced state of re-equilibration, that should ultimately be helpful for US and global risky assets.

Almost 'text-book' like! The large cumulative shift above trend in US M2 is seen as integral to the lagged rise in US CPI, but now both variables deviation from pre-Covid trend has converged.

Some big swings in yen today (a swift drop from 160 to 155) certainly hinted intervention might have occurred. The MoF's Kanda declined to comment, which is the same message policymakers initially had after the 2022 interventions. An intervention would make sense for several reasons.

A Japanese public holiday means lower liquidity, giving policymakers' actions more impact.

USD/JPY at the intra-day high of 160 was very close to recording the kind of moves that Kanda has expressed concern about (Figure 1). That is, getting close to a move of 10 yen in a month, or 4% in two weeks.

USD/JPY was also diverging quite a lot from relative rates, making an argument that fundamentals were taking a backseat. It's possible to construct a chart where relative rates suggest USD/JPY should be in the mid-150s, but 160 is a stretch (Figure 2).

Policymakers may have thought there was some excessive shorting to squeeze - after all the IMM data show yen shorts at their largest in a decade (Figure 3).

So what now? Our concern around possible intervention prompted us to (prematurely) take profits 11 days ago on our long USD/JPY view, when it was just under 155. Since then we've seen the unmoved BoJ and a very weak Tokyo CPI print, which would argue against USD/JPY dropping back below 155. Policymakers appear to have found 160 excessively high, but if it moved there gradually and in line with a move in rate spreads, it could be justified. And it's important to note that the interventions of 2022 didn't really change the story for yen - USD/JPY continued to trade broadly in line with relative rates (Figure 4). With little happening on the Japan front soon, it'll be the Fed and payrolls this week that matter.

Goldilocks: May FOMC Preview: A Narrower Path to Rate Cuts

The upside inflation surprise over the last three months has delayed the first cut and narrowed the path for the FOMC to cut at all this year. We have not changed our big picture inflation view because the surprises look idiosyncratic, the categories that are still hot reflect lagged catch-up rather than current cost pressures, and the key pillars of the disinflation narrative remain intact. We expect the next few inflation reports to be softer and have therefore stuck with our forecast of cuts in July and November, but even moderate upside surprises could delay cuts further.

… We have revised our Fed scenario analysis to include these two specific upside scenarios. We now include one upside scenario where the Fed does not cut at all because inflation remains too high this year and next, and another where inflation falls but the FOMC cuts just three times, either because inflation doesn’t quite fall enough or because the FOMC raises its estimate of the neutral rate more substantially. Our probability-weighted forecast is now higher at 4.9% at end-2024 (12bp below market pricing) and 3.95% at end-2025 (43bp below market pricing).

We continue to think that rate hikes are quite unlikely because there are no signs of genuine reheating at the moment, and the funds rate is already quite elevated. It would probably take either a serious global supply shock or very inflationary policy shocks for rate hikes to become realistic again. And even then, the FOMC might prefer to hold the funds rate steady at a high level unless the shocks seemed likely to spark a broader and more persistent inflation problem.

Goldilocks: Car Insurance: Another Case of Catch-Up Inflation

Car insurance prices jumped by 2.6% in the March CPI report, contributing 9.4bp to month-over-month core CPI inflation. And over the last year, car insurance prices have increased by 22.2%, contributing 0.8pp to year-over-year core CPI inflation. But these increases mostly reflect lagged catch-up to higher costs, and we expect the pace of increases to slow through the rest of this year as the gap between prices and costs closes.

Car insurance costs increased significantly over the last three years, reflecting higher new and used car prices, higher repair costs, and higher medical and litigation costs. But these cost increases have been passed onto consumers with a long lag, in part because car insurers have to negotiate price increases with state regulators based on recent costs and profitability. Indeed, insurance companies’ losses as a share of premiums were still around 8pp above their pre-pandemic levels in 2023Q4, despite recent declines in used car prices and slower input cost growth overall.

Our model based on the gap between prices and costs and past price increases suggests that car insurance inflation is likely to slow as premiums catch up to costs. We expect the sequential pace of price increases to average around 1% over the next six months and reach roughly 0.5% by the end of the year, which would lower the contribution of car insurance to year-over-year core CPI inflation from 0.8pp to 0.4-0.5pp by end-2024. Car insurance has a much smaller weight in the PCE index, so we do not expect these changes to have meaningful effects on PCE inflation.

MS Weekly Warm-up: Unpredictable Data + Tough Rate Comparisons Challenge Multiples in the Near Term

1Q earnings season has delivered a high beat rate with muted price reactions. We think this is attributable to the pressure on valuations from higher rates, a condition that could remain with us in the near-term unless Powell surprises on the dovish side at this week's Fed meeting.

Valuations Under Pressure Due to Rate of Change Comparisons on Yields…Over the past year, the consensus view on the economic outcome has shifted numerous times which has led to elevated volatility in both front-end and back-end rates. This has near-term implications for equities given the strong relationship between the 6-month rate of change on equity multiples and the 10-year yield that we’ve shown in recent weeks. Looking forward through June, easier bond yield comparisons present a headwind to valuation even if rates stay at current levels. From there, rate headwinds should ease if yields don’t accelerate higher over the summer. We remain constructive on quality and recently published single stock screens focused on this theme for idea generation…

MS Sunday Start | What's Next in Global Macro: Micro Machines

Read the paper, attend a conference or speak to a colleague, and it's reasonable to conclude that this is a 'macro' market. Geopolitics, inflation, central bank policy and the fiscal outlook dominate headlines and are seen as key drivers of what lies ahead. But there’s a risk to thinking this way. For all the sound and fury coming from the macro, 2024 remains an unusually micro market…

… Why is the market more micro? That's especially relevant for credit, where year-to-date pricing that suggests fewer rate cuts and higher interest expense would seem like a pretty straightforward risk scenario.

We'd note a few things. On Morgan Stanley’s forecasts, this year’s higher rates are coming alongside stronger growth (we think that US 1Q GDP was stronger than the 1.6% headline suggests). This helps. We think that credit is much more sensitive to whether central banks can cut, if needed, than to the exact timing and magnitude of this easing, and we still see the Fed, ECB and BoE cutting rates over the next 12 months. Meanwhile, it’s much easier to find credit performing well amid modest rate cuts (three or less) than in major cutting cycles (eight or more).

On interest expense, work by my colleagues Vishwas Patkar and Joyce Jiang shows that, in 4Q23, coverage metrics for sub-IG credit stabilized, as earnings recovered and borrowing costs are actually pretty similar year on year. Stable coverage metrics won’t apply to everyone (i.e., there's dispersion), but the trend is encouraging.

There are also some fundamental differences between credit and interest rates, which can lessen the linkage. Government bonds are suffering from strong data, heavy supply and (very) negative carry. For credit, those are all flipped: solid data are helpful, net supply is modest and carry is positive. We continue to like loans (and junior CLO exposure), which offer high yields and are well suited for a somewhat stronger, higher-for-longer world.

The headlines suggest that macro questions dominate the market. Year-to-date performance and alpha generation tell a different story. It's a surprisingly micro market.

MS: Global Economic Briefing: The Weekly Worldview: Still not solving for deflation in China

Demand deficiency is being met with an expansion of supply. An export recovery helps alleviate deflationary pressures, but only to a point.

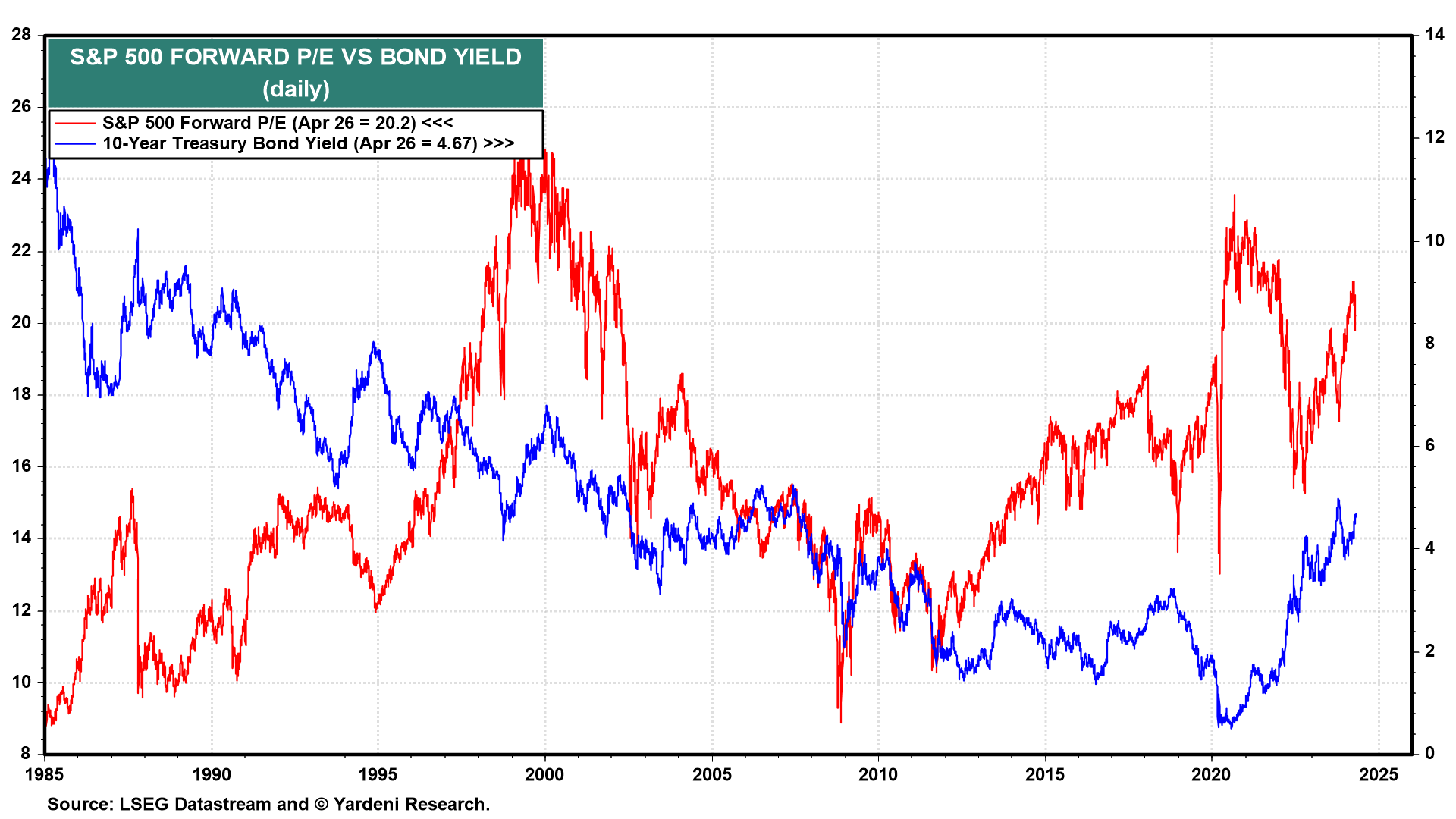

… A more troublesome near-term issue for the stock market is the recent backup in the bond yield (chart). It might have started to weigh on the forward P/E of the S&P 500. The yield is likely to revisit 5.00% in coming days, providing another good buying opportunity for long-term investors.

… And from Global Wall Street inbox TO the WWW,

Barrons: How a Chicken Sandwich Shows a Hidden Power in the U.S. Economy

… Bond markets in the US ended last week on a positive note even though Friday’s personal consumption data showed both spending and inflation above expectations. The initial read for the second quarter on Friday from the Atlanta Fed’s GDPNow tracker was a doozy too, coming in at 3.88%. Recent data are just further confirmation that the US economy is too hot to expect rate cuts anytime soon.

Friday’s muted market reaction to hot data was an artifact of the fireworks on Thursday that took yields higher. But if the second-quarter data continue to come in as robust as last week, the two-year yield will sustainably break above 5%, dragging the rest of the curve up with it.

Just digging into some of the data, March personal spending rose 0.8% m/m, matching last month’s print and above expectations. Consumer spending remains strong, which makes sense given initial jobless claims remain low and continuing claims are now dropping. From the Fed’s perspective, this potential firming of the employment picture gives it little incentive to make a precautionary cut to forestall the unemployment rate from rising.

Then, when you add the inflation data on top -- remember we got a 3.7% quarterly PCE number embedded in the GDP data Thursday -- you can see even fewer reasons for the Fed to cut. Friday’s core and headline numbers came in ahead of expectations for the y/y measures.

The bottom line is that both the employment and inflation side are telling the Fed to hold indefinitely. With base effects from the back half of last year approaching, we really could be on hold until the end of the year. While that is mostly priced in, the market is still hoping for two rate cuts, as evidenced by the 35-odd basis points of cuts priced in by the swaps market. That’s too much. And we may see yields start to creep back up after the market’s oversold conditions find a new baseline. That 5% level is the bogey across the curve from 2 to 30 years.

Bloomberg: Stagflation loses showdown with the Magnificent Seven (Authers’ OpED)

… The Dallas Fed produces “trimmed mean” numbers for PCE, stripping out the main outliers and averaging the rest. The good news from this exercise is that it’s reducing — still a hair above 3%, which precludes rate cuts for now, but suggests disinflation continues, though slowly:

How did markets respond to somewhat disappointing news? By staging a rally. The numbers weren’t a major miss, and anxious whispers had suggested that it could be much higher. That’s good for risk assets. Such optimism also entails that financial conditions remain moderate, with equities not far from all-time highs and credit markets also strong. That leads to one of the strangest phenomena of the moment. The last time markets convinced themselves that rates would be “higher for longer,” back in October, broader financial conditions tightened considerably. This is exactly what would be expected. The whole point of keeping rates higher is to tighten conditions and slow down the economy a bit. Now, market expectations, as gauged by Bloomberg from fed funds futures, are much more downbeat about rate cuts, but this hasn’t moved financial conditions at all:

Implicitly, the Fed’s notorious “pivot” last year, when Chair Jerome Powell made clear that the bank wanted to cut rates and would do so before inflation was back down to its 2% target, remains in force in the market’s mind. Despite the disappointing inflation numbers — which might well be disappointing because of the way the Fed took off the pressure six months ago — the belief is that the “Fed Put” is in place. It’s not going to tighten more than it absolutely has to, and will be there to save the situation if things get bad.

Sam Ro from TKer: Expecting average returns doesn't mean you should expect average years

… Gas prices fall. From AAA: “With domestic gasoline demand decidedly in the doldrums and the cost of oil retreating, the national average dipped two cents since last week to $3.65. … According to new data from the Energy Information Administration (EIA), gas demand fell from 8.66 to 8.42 million b/d last week. Meanwhile, total domestic gasoline stocks decreased by .6 million bbl to 226.7 million bbl. Lower demand and a drop in oil prices could push pump prices lower.”

WolfST: Money Market Funds, T-Bills, Large CDs, Small CDs: Americans Learn to Arbitrage the Higher-for-Longer Interest Rates

There’s no need to still pay a “loyalty tax” to the banks.

… AND with that all in mind, a BIG week ahead on WEDNESDAY (calendars HERE), I thought I’d pass along another calendar in case …

Yardeni: The Economic Week Ahead: April 29 - May 3

This could be another action packed week as the Fed's meeting and the latest S&P 500 earnings reporting season take center stage. Fed Chair Jerome Powell will hold his press conference on Wednesday after the latest FOMC meeting adjourns. He is likely to reiterate that the FOMC is in no rush to lower interest rates, and isn't considering raising them either. That won't be surprising to the markets. Q1 earnings, however, could continue to mostly surprise to the upside this week, as they have so far.

There could be surprises in this week's batch of economic indicators for both inflation and employment:

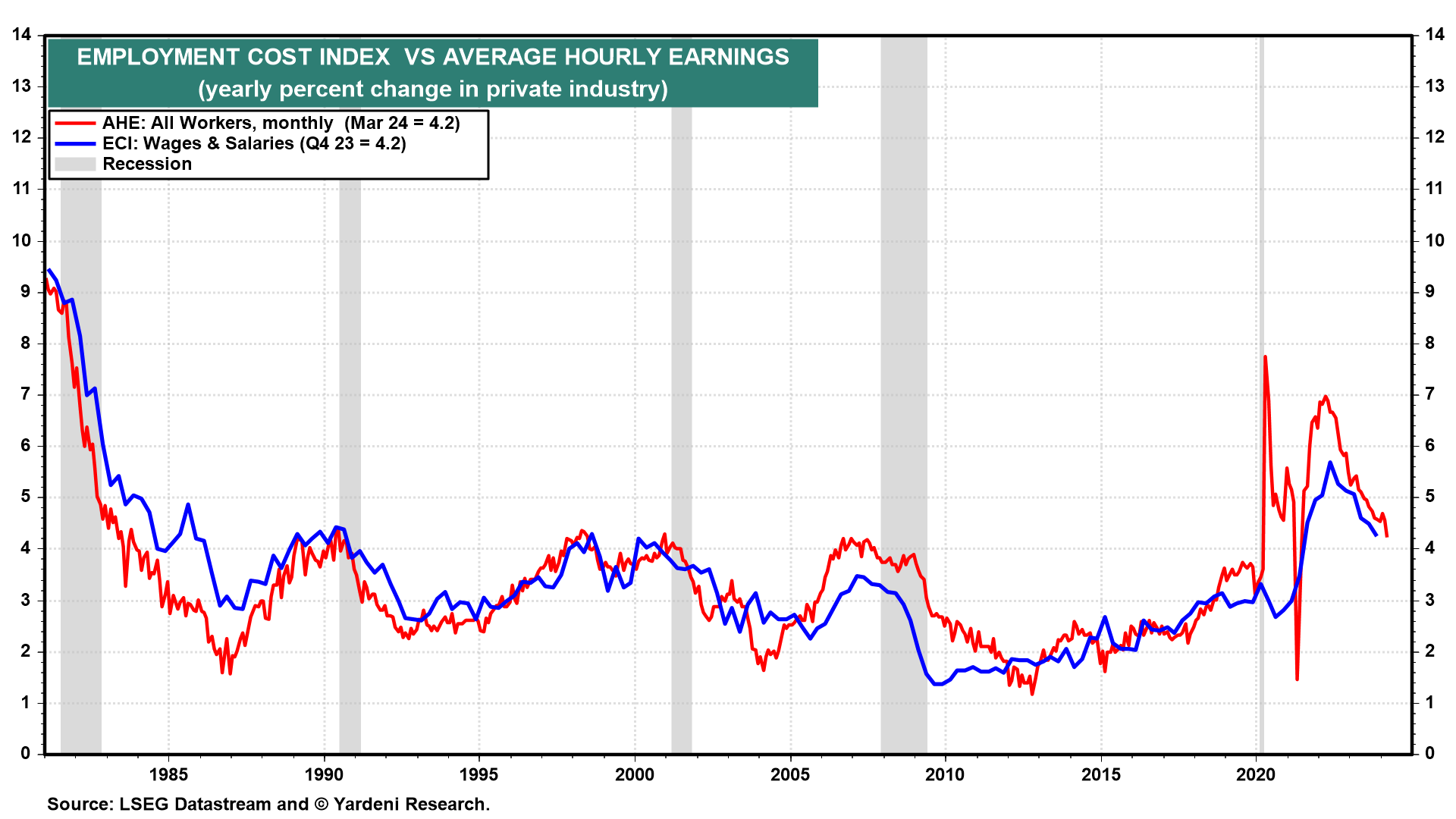

(1) Inflation. Q1's Employment Cost Index inflation rate (Tue) likely continued to moderate as it did last year notwithstanding significant gains for many union members with new contracts. We are expecting a 4.0% y/y increase down from Q4's 4.2% (chart). April's average hourly earnings inflation rate (Fri) should confirm that wage inflation is still moderating.

On the other hand, Q1's productivity growth (Thu) was probably weak following last year's big gains, reflecting solid employment increases and a weak increase in output as indicated by real GDP. Unit labor costs (ULC) probably rose faster during Q1. The bond and stock markets might not like the numbers, though we believe that productivity growth will rebound over the rest of this year, helping to moderate ULC inflation…

{kind=link}

Shocking Number of Excess Deaths, Disabilities, and Injuries Revealed: Edward Dowd, Data Scientist

https://www.theepochtimes.com/epochtv/shocking-number-of-excess-deaths-disabilities-and-injuries-revealed-edward-dowd-5633806?utm_source=Goodevening&src_src=Goodevening&utm_campaign=gv-2024-04-28&src_cmp=gv-2024-04-28&utm_medium=email&est=AAAAAAAAAAAAAAAAd%2BMlfRYVx8jG67YAnnxYA7t1hUABKtuXAPijADrQRk%2BLgXJ43cc%3D&utm_content=2?utm_source=ref_share&utm_campaign=copy

The Shadow State | Documentary............The ESG Movement, Scam........

https://www.theepochtimes.com/epochtv/the-shadow-state-documentary-4877950?utm_source=Goodevening&src_src=Goodevening&utm_campaign=gv-2024-04-28&src_cmp=gv-2024-04-28&utm_medium=email&est=AAAAAAAAAAAAAAAAd%2BMlfRYVx8jG67YAnnxYA7t1hUABKtuXAPijADrQRk%2BLgXJ43cc%3D&utm_content=3?utm_source=ref_share&utm_campaign=copy