while WE slept: USTs higher / flatter (2 of G7 in recession) on LIGHT VOLUMES; USTs hit / bounce from 23.6% fibbo and pushin' higher; BNPL (Fed's watchin...)

Good morning … A relatively quiet night with little to report this morning other than, well a couple major G7 economies dipping into a technical recession …

CNBC: Japan is no longer the world’s third-largest economy as it slips into recession Reuters: UK economy falls into recession, adding to Sunak's election challenge

… and apparently at least Japanese situation was a ‘surprise’’ (see MS below) and … other than that, ALL IS WELL … remain calm …

… all is well … but just in case, #GotBONDS? Now an effort to find something worth buying and at a ‘reasonable’ price with a ‘reasonable’ setup …

30s: back < 4.42% AND with BULLISH (DAILY) momentum

… Momentum NOTED is stochastics … some use other guides (RSI) and this has worked well for ME and is what those I respect, follow. I NOTE this appears to be a bullish setup AND at an interesting price level BUT looks attractive within a more bearish WEEKLY (longer term) context. Make of that whatever you will

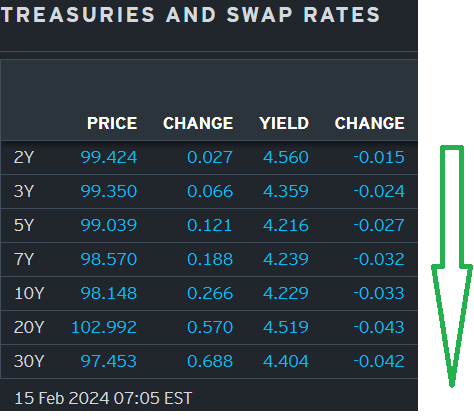

… here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher and the curve is flatter after two G-7 nations fell into technical recessions (UK and Japan) while Germany teeters on the edge of one. DXY is lower (-0.1%) while front WTI futures are lower too (-0.8%). Asian stocks rallied, EU and UK share markets are mostly higher (SX5E +0.75%) while ES futures are showing +0.1% here at 7am. Our overnight US rates flows saw good demand for paper overnight with today's flow focus on 10yrs and longer- as the curve flattening reflects. Even so, volumes were weak overnight at roughly half of average according to London colleagues.

… One might guess that Japan's just-revealed technical recession pushed the NIRP exit timeline even further out... In turn, the latest MOF data on Japan's net foreign bond flows (see second attachment) shows still-healthy demand for foreign bonds out of Japan with the 4-week MA a good reflection of that flow.

(HOPE my edit clarifies … 4wk MA suggesting THEY are still buyin’) … and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities firmer, GBP softer and Bonds lifted post-GDP; US Retail Sales, IJC & Central Bank speak due … Bonds are firmer after UK GDP data, numerous speakers ahead

Reuters Morning Bid: Tech-led U.S. 'exceptionalism' underlined (where VISUALS of both UK and Japan recessions are of note…)

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

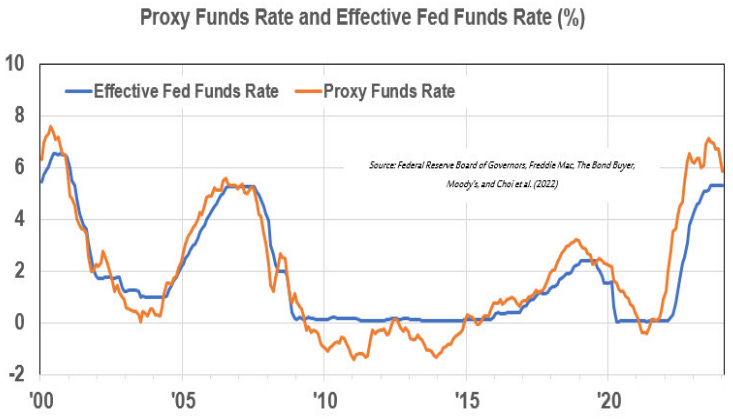

Argus: Proxy Fed Funds Rate Has Declined Since July

The grip of monetary policy on the U.S. economy appears to be loosening, even though the Federal Open Market Committee is unlikely to cut the fed funds rate next month. The full effect of monetary tightening may have peaked in July according to our analysis of the Proxy Funds Rate, an analytical tool tracked and updated monthly by the Federal Reserve Bank of San Francisco. At the end of January, the rate was 5.8%, compared with the official fed funds target of 5.25%-5.5%. The proxy rate peaked at 7.1% in July. The rate recognizes that central bankers use multiple tools (not just short-term interest rates) to meet their "dual mandate" of stable prices and maximum sustainable employment. The Fed uses forward guidance to communicate the direction of monetary policy and influence longer-term interest rates and broader financial conditions. The Fed also can expand its balance sheet through the large-scale purchase of Treasury and Mortgage Backed Securities, which is known as quantitative easing, or reduce its holdings, which is known as quantitative tightening. The Proxy Funds Rate uses the analysis of 12 financial variables, including Treasury rates, mortgage rates, and borrowing spreads, to translate the full range of policy actions into an analogous level of the funds rate, That can help assess whether policy is tighter or easier than the official funds rate suggests. In a November 2022 San Francisco Fed Economic Letter, the developers of the proxy rate noted the following: "As the FOMC increasingly used forward guidance and the balance sheet, the proxy rate has tended to lead the actual funds rate, reflecting the fact that financial markets are forward looking." The letter also noted that "combined policy tools have a more complex effect on the economy than the federal funds rate indicates." This suggests to us that Fed watchers should become even more diligent.

… On Macro: for first time since Apr’22, investors not predicting recession (Chart 1), global growth optimism highest since Feb'22 (net -25%); asked for path of economy this year, 2/3 of investors say "soft landing," 1/5 say "no landing," 1/10 say "hard landing."

DB: Cut it out? Conditions for eliminating easing in '24

The recent slew of stronger economic data, firmer inflation and hawkish-leaning commentary from Fed officials has triggered a material reduction in the number of rate cuts priced by the market this year. These developments have moved market pricing much closer to our baseline view of the first cut in June, 100bps of total reductions in 2024, and a nominal neutral rate around 3.5% (see “Outlook update: Back in (the) black and (so far) done dirt cheap” and the chartbook version here).

This piece considers what economic conditions could lead the Fed to not cut rates at all this year. Canonical policy rules suggest that no rate cuts this year broadly requires the following three conditions: 1) a reversal of recent inflation progress, with core PCE ending the year at 2.7% or higher; 2) an upward reassessment of the nominal neutral rate to values closer to our view (i.e., ~3.5%); and 3) continued solid data for growth and the labor market with the unemployment rate at 4% or lower.

While this condition for inflation is far from our baseline (we have core PCE ending the year at 2.2%), recent data suggest the probability of this outcome may not be trivial. We conclude the report with a broader discussion about risk management considerations for cutting rates this year.

… The last 24 hours have been surprisingly calm after the turmoil of the previous session. 2yr US yields rallied back -8.0bps after rising +18.3bps the day before, encouraged by some dovish Fed speak. 10yr yields fell -5.8bps after the +13.5bps spike the previous session while December 2024 Fed pricing increased +8.9bps after a full 25bps had been taken out on Tuesday. The S&P 500 closed +0.96% higher, retracing nearly three-quarters of Tuesday’s losses…

■ We expect US Treasuries outstanding to rise by about $1.72tn this calendar year, less than the $2.37tn increase in 2023, but with a markedly higher reliance on coupon issuance ($1.85tn in 2024 vs. $1.03tn in 2023). The notional coupon supply to be absorbed by private investors is the highest on record.

■ Money market funds were the largest buyers of USTs (mostly bills) in 2023,and will likely remain sizable net buyers this year, although much less so than in the previous year. There will likely be a continued bid from pension funds in 2024, as improvements in funded status further boost duration demand. While commercial banks may increase UST holdings, we expect dealers to modestly slow down their pace of inventory accumulation.

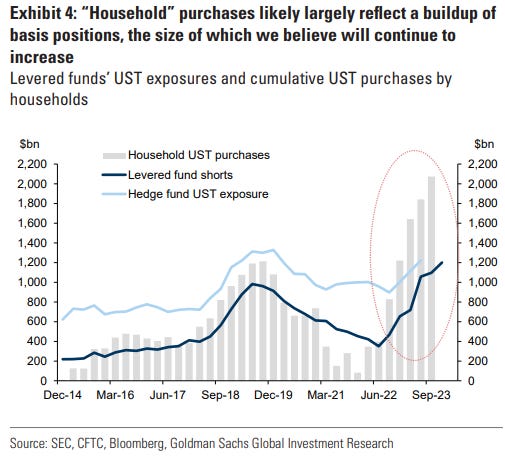

■ The “households” category (which includes levered funds) should add ~$770bn in UST in 2024, more than any other individual category, albeit by less than in 2023. A continued shift towards a more price-sensitive buyer base along with the ongoing erosion of excess liquidity should translate into increased pressures on funding spreads and further cheapening of UST versus swaps and futures at longer maturities.

… we observe that other large, primarily domestic “residual” categories, which likely bought a combined $1.15tn last year, will continue to be big buyers this year. First, the “household” category, which includes levered funds, has been buying over $1tn of USTs for the past two years. This partly reflects a buildup of basis positions, where levered funds repackage duration risk in the form asset managers appear to desire (Exhibit 4; see here and here for details) …

… Our overall Treasury demand projections for 2024 are summarized in Exhibit 5.

We explore sensitivities of various markets' performance to rates vol. Whether rates vol normalizes or stays at current levels, we find that fixed income has a better skew of expected risk-reward than stocks.

Key takeaways

Our fixed income > equities preference assumes rates vol normalizes, but uncertainty over the path of policy has meant realized vol remains high.

But with rates vol close to the averages of the 1995 Fed pivot episode - which we think is a good lens for today - maybe this *is* normal.

Lower rates vol coincides with better returns and lower vol for stocks and bonds, but sensitivities vary, e.g. stocks are impacted more by 30Y than 2Y vol.

Equity vol is dislocated from rates vol this cycle. If rates vol stays here, equity vol may need to play 'catch up'; if rates vol falls, it may not fall much.

Bonds have good risk-reward if vol normalizes and good relative vol-adj returns if it doesn't - especially if stocks respond to *why* rates vol stays high.

Rates vol around the 1995 Fed Pivot was not that far off from where we are now

UBS (Donovan): What’s in a name? It’s recession time

… US retail sales do not adjust for price changes, so auto sector price discounts may lower the headline number. Otherwise, it is foolish to short the hedonism of the US consumer; this week’s consumer price data release confirmed that middle income homeowners have strong spending power. However, aside from restaurant spending, the retail sales does not capture spending on having fun.

Figure 1: Repayments spiked and then fell back towards pre-pandemic levels

As shown in the figure above, daily deposits into the Department of Education's account at the Federal Reserve, are running around $262 million per day (we show a five day moving average). Annualizing these daily payments, we estimate that total annual payments are running about $68 billion annually, not far from expectations prior to the resumption of payments, and even after ongoing announcements of income-driven repayment programs. Overall, that represents roughly 0.3% of disposable income, another incremental headwind for households…

The resumption of payments will impact households differently… Lower income households look the most vulnerable…

...But, we continue to expect the BoJ to hike policy rate in April Today's outcome probably leaves continued negative output gap (excess supply), down from -0.7% of potential GDP in Q3 to -0.9% in Q4, in our estimate. The weak economy could be regarded as a factor that hinders the BoJ to start policy normalisation. However, we continue to believe that the BoJ will raise policy rate by 10bp to 0.0% in April as the BoJ is forward looking. As long as they can argue that consumption will pick up with a faster nominal wage growth and slowing CPI inflation, we think they can start a dovish rate hike (see details here).

Wells Fargo: Should We Worry About American Debt?: Time to Reconsider?

Summary

The debt of the federal government has mushroomed in recent years. The $27 trillion of marketable U.S. government debt at present is equivalent to roughly 100% of GDP, which is its highest ratio since the end of the Second World War.

Chronic budget deficits have led to the inexorable rise in federal government debt. Outlays have averaged about 21% of GDP over the past 50 years while revenues have averaged only 17% over that period.

Reducing the deficit is simple, at least in theory. Lawmakers simply must raise taxes, rein in spending or some combination thereof. In reality, however, reducing the deficit is very difficult. Raising taxes is a political non-starter at present, and reining in spending involves its own challenges.

The entitlement programs of Medicare, Medicaid and Social Security account for nearly one-half of federal spending at present, while defense spending and interest payments on the debt represent another 13% and 11%, respectively. Therefore, more than 70% of federal spending is essentially "untouchable" from a political perspective. Even if lawmakers completely zeroed out all non-defense discretionary spending, the federal government would still be incurring a deficit.

The good news is that a debt crisis does not appear imminent. Investors continue to finance budget deficits by buying Treasury securities at reasonable interest rates. Given the depth and liquidity of the market for U.S. Treasury securities, the status of the United States as the world's largest economy and strongest military power, and the role of the U.S. dollar in the international monetary system, there simply is no substitute for Treasury bills, notes and bonds.

But there are some costs that the rising amount of federal debt imposes. The rising debt service burden can potentially constrain other areas of federal spending, and private investment spending could potentially be "crowded out" by elevated interest rates.

The Congressional Budget Office projects that the debt-to-GDP ratio of the federal government will rise from about 100% at present to 180% in thirty years. It is an open question whether investors will feel sanguine about the fiscal outlook for the federal government indefinitely. It is impossible to determine when a "hard stop" could occur, but an ever-rising debt burden clearly increases the probability of such an event occurring at some point in the future.

… And from Global Wall Street inbox TO the WWW,

Bloomberg:

Kimble: Treasury Bond Yields Reverse Higher Off Key Fibonacci Level!

The past few months have given investors the feeling that the 3 year (monster) rally in treasury bond yields is over.

But the lull may be over. And it’s looking like bond yields (interest rates) may be rallying again.

Why? Well today’s chart 4-pack looks at treasury bond yields across all time spectrums (2-year, 5-year, 10-year, and 30-year).

As you can see, whether short or long-term, ALL bond yields pulled back and tagged the 23% Fibonacci retracement level at each (1) and created monthly bullish reversal patterns.

Liberty Street Economics: How and Why Do Consumers Use “Buy Now, Pay Later”? (aka NY Fed … they are watching … and have a snazzy wordcloud to prove it)

… Reasons for BNPL Use Vary by Level of Financial Stability

…Our results also have implications for future BNPL use. They suggest that the largest barrier to consumer take-up is their first use, and that after this initial use consumers tend use BNPL again. With about 80 percent of households not using BNPL in the past year, there may still be a great deal of room for increased adoption of the product. This will be particularly important to watch in the coming months, as many shoppers used BNPL for the first time this past holiday season.

and financially fragile BNPL users (on the right) when asked why they use BNPL. “Payments” dominates both, with “interest” and “credit” also prominent for stable users and “easy” and “money” also prominent for fragile users.")