Good morning … I’ve not yet had time required to put pen to paper (finger to keys) and conjure up some monthly and quarterly yield context and with holidays tonight at sundown, not sure when that will be. HOPE it to be soon but … family first and so I’ll move on and ask for some patience if ‘posting’ spotty next few days and will lean on what was noted yesterday before bombs dropped into Israel …

2yy vs 3.659 and, frankly, Israel TO Iran bombing campaign be like …

… hard to NOT pause and reflect a moment on flurry of geopolitical headlines and tape bombs from yesterday …

ZH: Iran To 'Imminently' Launch Ballistic Missiles On Israel; White House Warns ZH: It Begins: US Port Strikes Erupt, First Shutdown In 50 Years Sparks Fears Of Supply Chain Crisis

… that was not all as there were also some economic inputs to the global MARKETS calculus, too …

ZH: US Manufacturing Surveys Signal Stagnation, Employment Weak ZH: Job Openings Unexpectedly Jump Over 8 Million On Record Surge In Construction Job Openings

… and as I said, without time to do some justice to facts all ‘round, i’ll move right along and TO a snapshot OF USTs as of 705a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US futures modestly lower, USD and Fixed pull back ahead of data … USTs are flat and Bunds give back some of its recent strength, Gilts follow peers and took another leg lower following an auction .. USTs are essentially flat/incrementally lower and holding at a 114-18+ base, having faded from Tuesday’s geopolitically-driven 115-00 peak. Today's docket is packed with ADP National Employment alongside Fed speak from Barkin, Bowman, Hammack & Musalem.

Opening Bell Daily: Striking rich. Dockworkers earning $150,000 are willing to hobble the economy for a 77% raise … Thousands of longshoremen across the East and Gulf Coast are on strike for a new union contract.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

… with ports strike ON a look at those who are reporting for work or actively looking and what they may / may NOT find …

BARCAP: August JOLTS: More openings, less dynamism

Job openings rebounded in August, soothing concerns about deteriorating labor demand. Although dynamism diminished, the widening gap between hiring and separations likely keeps the Fed on course for a 25bp cut in November, though Friday's employment report still looms large.

… with port strike ON a look at domestic Mfg …

BARCAP: Manufacturing ISM: Not more than meets the eye

The ISM manufacturing composite held steady at 47.2 in September, at the lower-end of the lackluster range that has prevailed since late 2022. The flat PMI conceals mixed developments across components, including a slide in the employment component. Input prices slid into deflation, likely reflecting lower oil prices.

… tying it all together, same shop …

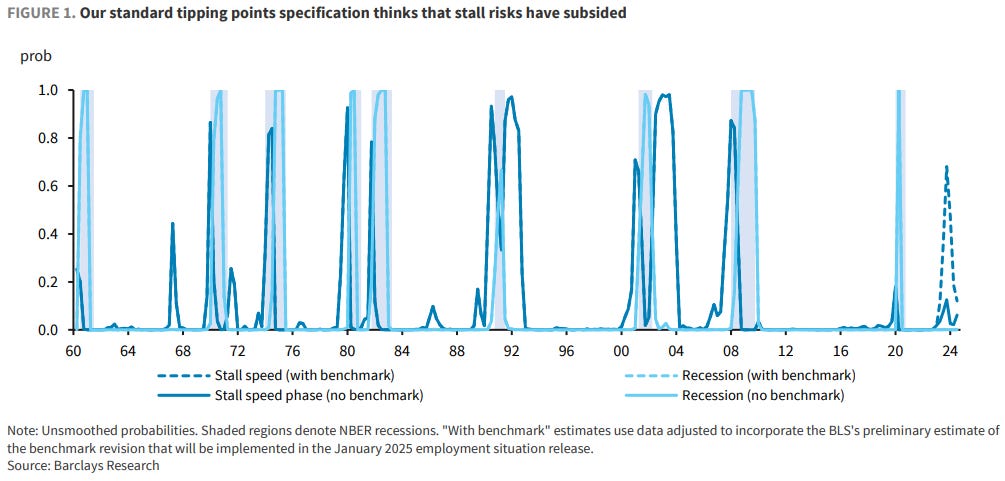

BARCAP: US Recession Risks: Tipping points model: It was all yellow

We update our "economic tipping points" model, which identifies when the US economy is either in a recession or susceptible to one. Although this model places recession probabilities at low levels, it has flagged a higher susceptibility over the past year, especially in formulations that work from the unemployment rate.

…New Results: Employment rate specification Perhaps not surprisingly, our specification using the employment rate places a much higher likelihood upon being in a stall. Somewhat more surprisingly, the deterioration is not sufficiently rapid for the model to place any meaningful likelihood on the possibility that recession is imminent…

…As shown in Figure 12, this specification correctly identifies all of the recessions in our sample period, with no false positives. However, it does exhibit at least some uncertainty about whether the episode in 1990-91 was a true recession, given the slow pace of decline in the employment rate in that case. All of these recessions were preceded by some run-up in the stall probability, though these lesser spikes are not as definitive as in our preferred specification (indeed, this is part of the reason why that specification is preferred …

… here’s a better than decent note on impact of gigantic cuts and QT (as well as recap of bond mkt and data yest) …

We’ve touched on issues related to Fed QT in recent notes, highlighting market expectations for the timing of the end of runoff and the potential implications of the recent pick-up in mortgage activity. From the perspective of funding markets, SOMA manager Perli’s speech last week noted that the set of indicators the Fed is using to monitor the transition to “ample” reserves isn’t flashing concern though the recent rise in market repo rates bears watching. (We’ll see how the dust settles from tight quarter-end funding conditions and the first real SRF usage yesterday.)

Reserve conditions aside, the key balance sheet policy question raised by recent shifts in the Fed outlook is what 50bp cuts to the fed funds rate could mean for QT. When asked about this in his recent press conference, Chair Powell stated that larger cuts to the fed funds rate need not have any bearing on QT, in that both rate cuts and balance sheet runoff are a “form of normalization.”

What are the limits to this? We think the key is whether the Fed expects to be cutting the funds rate not just back to but below neutral, so that it is actively easing rather than just "dialing back policy restraint." That squares with the evolution of Fed policy in 2019. As illustrated in the chart, the FOMC wound QT down then as the median SEP projection reflected cuts over the next year to a level below (nominal) neutral. A similar combination – rate cuts that are expected to bring policy into easy territory – would spell a premature (i.e., pre-ample) end to QT today. Another 50bp from here could but need not meet that test.

… Over on the rates side, a rally for bonds was accelerated by the Middle East headlines, though by the close Treasury yields were only slightly lower than before the news broke. On the day, 2yr yields were -3.6bps lower to 3.61% while 10yr yields were down -5.0bps to 3.73%, their sharpest daily decline in three weeks. This morning in Asia 10yr yields have edged back up to 3.74%.

Bonds had already rallied earlier in the day after the latest US data, which added to the signs that the labour market was weakening. It’s true that job openings were stronger than expected in August at 8.040m (vs. 7.693m expected), but the other details in the report generally pointed in a more negative direction. For instance, the quits rate of those voluntarily leaving their job was down to 1.9%, the lowest since June 2020, and below its pre-Covid levels. So that was a fresh sign that people’s confidence in the labour market is still weakening, and the hires rate also fell back a tenth to 3.3%, in line with its joint-lowest since the Covid-19 pandemic. That was backed up by the ISM manufacturing too, which remained at 47.2 in September (vs. 47.5 expected), whilst the employment component weakened to 43.9 …

… interrupting JOLTS jobs update and MFG recaps, a quick update on US elections from a UK shop (? I know, right?)

What’s New This Week: Vice President Harris unveiled her economic agenda (here) that made a small business tax credit and pushing back against grocery price gouging and rising housing costs a few of the main focal points. The Vice-Presidential debate is tonight (9pm ET) and will see JD Vance and Tim Walz face off. Since Trump hasn’t yet agreed to a second debate with Harris, tonight’s VP debate may carry more weight as the last opportunity for each party to tout their policies on a nationally televised stage. The House last week passed a short-term spending bill that funds the government through the election – this avoided a government shutdown just a month out from the election…

…Market View: We see Harris as a slight favourite but think the highest probability scenario is a split government if Harris wins, thanks to the Senate leaning towards Republicans, limiting her legislative reach. Trump is more likely to win in a sweep if he wins, resulting in higher fiscal deficits, additional tax cuts, and a return to America first style trade and foreign policy. For markets, (page 4-5) we see a Trump win as higher yields, steeper curves, and stronger USD. On a Harris win we see lower rates and a lower USD, but we think that’s largely a function of pricing out our Trump-scenarios rather than necessarily pricing in Harris. The key event calendar quiets down a bit after the Sep 10th debate (p 5).

… and so orange man bad for bonds, now, then … okie dokie … some GLOBAL RISKS on the radar screen …

UBS: Global Risk Radar: Middle East conflict extends to Lebanon

The current conflict in the Middle East has continued to escalate. Israel launched airstrikes against Hezbollah targets in Lebanon, and started “limited, localized, and targeted ground raids” today, according to the Israel Defense Forces.

In our base case, we expect global markets to be occasionally affected by the escalation in the Middle East, but do not assume the conflict will escalate to all-out war between Israel and Iran, including their respective allies. But the possibility of veering into the downside risk case of a multi-front war between Israel and Iran and its proxies is more likely now, and bears the risk of direct US involvement and disruptions to energy supply.

We highlight the importance of diversified portfolios to limit the exposure to individual risks, but recommend staying invested to benefit from an overall supportive macroeconomic backdrop. Oil, gold, and high-quality credit can help stabilize portfolios.

… Investment implications … In our base case, we expect global markets to be occasionally affected by escalatory actions in the Middle East, but at this point, we do not assume that the conflict will escalate to an all-out war between Israel and Iran, including their respective allies. This also assumes that energy flows from the Middle East continue without sustained interruptions.

That said, the possibility of veering into the downside risk case of a multi-front war between Israel and Iran and its proxies has increased, and bears the risk of direct US involvement and disruptions to energy supply. The US is a key supporter of Israel, and while the Biden administration has become more critical in light of the high civilian casualties in Gaza, it would likely come to Israel’s defense if needed. Direct participation by the US in the fighting may rattle financial markets more sustainably, as this could further endanger US assets and its allies in the region. Oil remains a key transmission mechanism from the conflict into global markets. While Iran has an interest in keeping energy flows unobstructed in the region, given its own dependence on oil exports, any impediment to Iranian flows may change the calculus and lead to disruptions. Oil supply has not yet been affected, however, and the market tends to price out geopolitical risk premia. A disruption to major oil supply routes like the Strait of Hormuz or damage to critical oil infrastructure could see Brent crude prices break above USD 100/bbl for several weeks. …

Markets have responded to escalating violence in the Middle East. Overnight missile attacks by Iran against Israel differed from those in April—there was less warning, and faster missiles were used. Israeli Prime Minister Netanyahu has pledged retaliation. Investors have seen this as a more serious escalation, and oil prices have risen. However, even at higher levels oil prices are still near the lows for the year. This limits the economic consequences for now.

US financial markets are anticipating Friday’s employment report (despite the report’s frequent revisions, and increasingly strained relationship with labor market reality). The ADP payrolls report is released today, but the significance of this has dwindled. The number of economists forecasting the data has fallen by a third in recent years. Federal Reserve Chair Powell’s suggestion of two quarter point rate cuts this year, as the Fed plays catch up to the economy, blunts the impact of labor data…

… back TO somewhat MORE on JOBS and domestic MFG …

Summary Job openings and turnover data for August served as a reminder that in level terms, the U.S. labor market is holding up, but it is still in a fragile position. Job openings partially rebounded to 8.04 million in August, and the ratio of jobs per unemployed workers ticked modestly higher to 1.13. The bounce in these measures offers some comfort that labor demand is not yet deteriorating in a non-linear way. That said, beneath the surface, turnover in the labor market (i.e., new hiring and workers quitting their current jobs) has stalled out to levels reminiscent of the early to mid-2010s. The good news is that layoffs & discharges remain historically low, but given the background of materially weaker demand for new workers compared to last year or even just six months ago, separations need to stay low to avoid a marked slowdown in net hiring. All eyes will now turn to Friday's September employment report to see if August's rebound in payrolls and the unemployment rate were the first signs of the labor market stabilizing or just a temporary breather in the softening trend.

Wells Fargo: Flat ISM Signals Hurdle of Uncertainty for Manufacturing

Summary A flat reading on the ISM manufacturing index tells us business capex plans are on hold amid uncertainty over the path to lower interest rates and the presidential election outcome. The details show inflation is a fading problem, while jobs are a growing worry

… and finally, an excellent annotated visual of stocks from Dr (Bond Vigilante) Yardeni …

Yardeni: Stock Market Flinches On Widening Middle East War

Stock prices and bond yields dipped while oil prices jumped this morning. In Washington, a senior White House official said the US is actively preparing to defend Israel against another direct missile attack by Iran. The official added that such an attack would carry severe consequences for Iran, which is under pressure to retaliate for recent Israeli military actions against Hezbollah, its proxy in Lebanon. The markets' initial reactions moderated by early afternoon after what seems to have been a limited strike on Israel by Iran with no serious casualties.

A widening Middle East war has been our number one risk scenario over the past year for the bull market in stocks. For now, we are sticking with our subjective probabilities: 50% Roaring 2020s, 30% 1990s-style meltup, and 20% reprise of geopolitical turmoil reminiscent of the 1970s. As we've often noted in the past, geopolitically-induced selloffs tend to be buying opportunities (chart).

Meanwhile, here in the US, today's economic indicators were mostly unsurprisingly benign. Job openings ticked up in August, while quits fell. The national M-PMI remained weak in September. Construction spending unexpectedly fell in August amid a sharp drop in outlays on single-family housing projects…

GDP for the second quarter came in at 3.0% (see chart below), the Atlanta Fed’s GDP estimate for the third quarter currently stands at 3.1%, and jobless claims are at 218,000.

It is difficult to argue that the US economy is slowing down.

… POSITIONS matter and none better to get / stay informed by than EBB

Bloomberg: Traders Unwind Long Treasury Bets as Smaller Rate Cuts Weighed

(Bloomberg) -- Bond traders are beginning to cash out of their bets for a further rally in US Treasuries as they scale back on expectations the Federal Reserve will deliver another half-point interest-rate cut.

… and while positions are important, what of rate cuts, falling rates and corp PROFITS? I’m glad you asked, as John Authers helps leaning on others visuals, to offer an answer …

Bloomberg: Mideast conflict reaches the oil price — briefly

A big difference between now and the 1973 Yom Kippur War is supply.

… But then there’s the issue of rate cuts. Historically, they almost invariably overlap with falls in profits. As this chart from Societe Generale SA’s chief quantitative strategist Andrew Lapthorne shows, there is no precedent in the last 40 years for profits continuing to grow while the fed funds rate is falling:

This seems like a completely contradictory message, expecting sharp US rate cuts yet also continued strong earnings growth, as these cuts would historically be consistent with a 20% or more decline in reported profits and so a 30%+ drop in forward earnings.

That’s hard to reconcile with the latest data from Bloomberg’s World Interest Rate Probabilities function, which currently suggest enduring confidence that the fed funds rate will come to rest below 3%, having spent more than a year at 5.5% …

… and about those rate cuts and falling with impact on corp profits … seems to SOME that all is NOT happening quickly enough …

Bloomberg: The US Economy’s Landing Isn’t as Soft as We Think

Auto-loan hazard lights are flashing for US lenders.

For all the talk of a soft landing in the US, there’s one corner of the economy where the hazard lights are flashing: the $1.6 trillion motor-vehicle lending market, which accounts for around a quarter of non-mortgage consumer credit. For the past three years, bad debts have been rising. As of June this year, loans 30 days or more past due were back at levels not seen since the country was recovering from the Great Recession in 2010. Among subprime borrowers, delinquency rates are now even higher than during those times. Is that a sign of deeper stress, or will it be contained?

To answer the question, we need to dig into individual lender portfolios. One of the first to highlight the risk was Credit Acceptance Corp., a specialist auto financier headquartered near Detroit. On its earnings call in July, Chief Executive Officer Ken Booth warned that loans originated in 2022 were performing below expectations and that the company’s 2023 vintage was slipping as well. The company’s stock price fell 15%…

… and since September seasonals worked so well and October generally more positive for markets although slightly less so during pres cycle …

…On Average, Stocks Hit a Short-Term Bottom Right Before the Election

… Summary

In general, October has proven more of a treat than a trick for stock markets, but in U.S. presidential election years the month can be a little scary for investors as markets struggle to come to terms with the uncertainty of the election results. Fed rate cuts in September boosted stocks during what has been a historically weak month for stocks, but after five straight positive months, we would not be surprised if we see at least a consolidation in October as markets take a breath ahead of the election.

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) continues to maintain its tactical neutral stance on equities. However, we do not rule out the possibility of short-term weakness, especially as geopolitical threats in the Middle East escalate. Equities may also readjust to what we expect will be a slower and shallower Fed rate-cutting cycle than markets are currently pricing in, although both post-election and fourth-quarter seasonality are favorable for stocks.

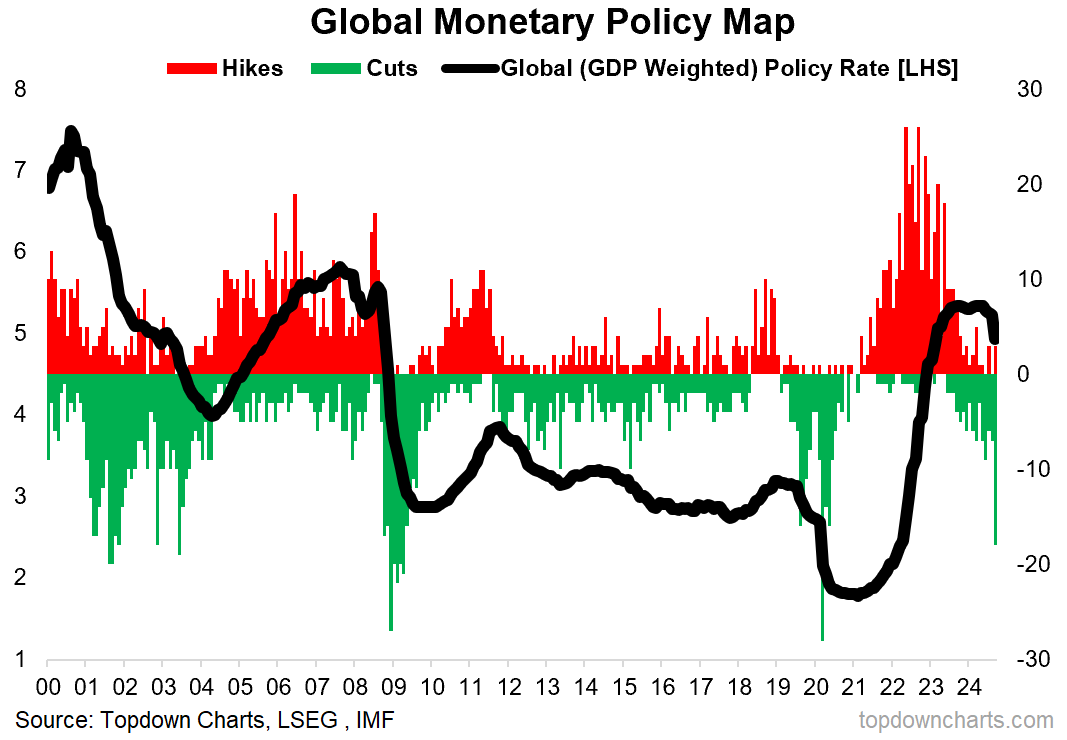

… perhaps most important thing is what may be of global central planning policy and on that, a chart …

First it was panic rate cuts (remember 2020?), then it was panic rate *hikes* as the worst inflation shock since the 1970’s hit …and now? Central banks the world over are hastily pressing the undo button on one of the most substantial, widespread, and rapid tightenings of monetary policy in recent decades.

Indeed, September saw the highest number of rate cuts (and largest drop in global policy rates) outside of the 2008 financial crisis, 2020 pandemic, and early-2000’s recession/bear market.

So what’s really happening with all this, and why now? And most importantly — what are the implications for investors? Let’s take a quick look.

First, the constructive non-sensational take: this is simply an unwinding of previous tightening as the rate of inflation continues to decelerate and ostensibly inflation is no longer an issue …therefore such a tight monetary policy stance is no longer warranted, and it’s just an adjustment and normalization of rates.

But let’s also explore the bear case: globally we have seen a softening of PMIs, clear deterioration in labor market data, and late-cycle signals …in other words, the risk of recession is high and rising and central banks see this —preemptively easing into a potential downturn…

… finally somewhat more on JOLTS …

WolfST: Balance of Power Changed, Employers Re-exert Control, but also Cling to their Workers

Fewer workers quit (rattled by layoff headlines?), so fewer vacant slots to fill and less hiring. But actual layoffs are at historic lows.

… all THAT said and in mind, on the port strike …

AND … THAT is all for now. More later, at some point — dunno when.

Yes enjoy family & holidays! I've heard some stories from Long Shoremen working out of the port of Oakland, CA in the 80s & 90s, that'd make the goons in with the mink coats in the meat locker in Goodfellas blush

Have a good holiday :)

Yes enjoy family & holidays! I've heard some stories from Long Shoremen working out of the port of Oakland, CA in the 80s & 90s, that'd make the goons in with the mink coats in the meat locker in Goodfellas blush