Good morning … Wei Li / BLK on Bloomberg TV yesterday …

“We think markets are a bit excessive in pricing the depth of the rate-cut cycle,” Li said. “The cutting cycle is starting, but maybe not as deep as markets seem to be pricing.”

… And for more from the BBG.com story, scroll to the bottom. But before you scroll,

WSJ (Timiraos): Fed Prepares to Lower Rates, With Size of First Cut in Doubt. The central bank usually prefers to move in increments of a quarter point. This time, it’s complicated.

… That this week’s decision is a close call could reflect honest uncertainty over the right choice, English said. “It’s not like you have half the committee at 50 and half at 25, and they’re shouting at each other. You have a bunch of people who are genuinely uncertain what the right thing to do here is,” he said. “In the end, Powell can probably build a reasonable consensus around either.”

Blk and WSJ have spoken — make of them whatever you will and for now, a look at 2s

2yy: support up nearer 5.25 while ‘resistance’ closer to 2.25% (TLINE) and this within context of momentum — overBOUGHT — and as one can see curing the C19 experience, it can take quite awhile for this to work through system and it would appear … we’ve only just begun with rate cutting cycle about to begin … tomorrow …

… drop on the far LEFT was SVB and the banking crisis of 2023 while the drop on the RIGHT is the pricing in of rate cuts … I know, you know, but … Momentum (stochastics) can remain overBOUGHT for while and doesn’t mean an imminent tick higher in yields has to be next move … time at a price …

… here is a snapshot OF USTs as of 702a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: DXY flat but USTs firmer, Timiraos in focus into US data … Bonds are firmer as markets digest another Timiraos piece, which further highlighted that the Fed has doubts regarding the magnitude of a cut … USTs are essentially flat; overnight focus was on the latest WSJ Timiraos piece which highlighted that when the Fed has doubts around the size of its first cut it generally favours 25bps; however, “this time, it’s complicated”. This could potentially be the reason USTs caught a slight bid to a 115-21 high, where it currently resides.

Reuters Morning Bid: New highs, rotation, as Fed meets with retail healthcheck

Opening Bell Daily: What inflation? Corporate America is moving on from inflation, just like the Fed. Fewer S&P 500 companies are mentioning high prices during earnings calls as the Fed readies its first rate cut.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

France weighs in on 25 vs 50 debate with an important — IMAGE / perception — is EVERYTHING debate

BNP US rates: How markets may perceive a 50bp cut at September FOMC

As markets have priced in more 2024 rate cuts and an increased probability of a 50bp move at the September FOMC meeting, the US curve has bull steepened. If the Fed does cut by 50bp, this may continue as the likelihood of 50bp again in November might rise.

Continued bull steepening is more in question if markets perceive a more aggressive Fed as reducing the likelihood of a harder landing, particularly if this is communicated by officials. Yields have fallen substantially over the past two months. Market-implied end-2025 fed funds has reached the Fed’s longer-term median (2.75%) and the 2y UST has nearly reached 200bp through fed funds.

We continue to view risk/reward as favouring long positions and steepeners for a large move in yields (harder landing). However, current valuations increasingly need to be justified by a softening US economy, in our view, which makes us reluctant to hold outright longs and more cautious on steepeners.

Instead, we favour more limited downside expressions such as our 6m1y receiver spread and 10y SOFR versus 10y ESTR; we also take profits on our 5s30s UST steepener as it depends on a harder landing. A softer landing may see carry erode profitability over time.

…Uncertainty at the meeting versus future action: We note that the degree of uncertainty surrounding the size of the cut at this week’s policy meeting is relatively uncommon. Traditionally, market pricing reflects a high degree of certainty concerning Fed actions at the current meeting. Information gleaned by markets is usually regarding future policy action and comes from the FOMC statement, the SEP (if applicable) and the Fed chair’s press conference. If this messaging (especially if explicit in Powell’s press conference) highlights a desire for the Fed to be proactive in attempting to remove restriction and preserve a soft landing, markets may react with more caution. US yields may retrace back to our end-Q4 forecasts (3.75% 2y UST, 3.80% 10y UST) …

…Close trade: 5s30s UST steepener at 52.25bp. Entry: 28.25bp on 11 July. Total P&L = +18.9bp (including -5.1bp carry + rolldown) or USD378,000.

One of Germany’s fan favorite market commentators on what a quiet Monday means for Wednesday …

DB CoTD: Will a no news Monday mean 50 on Wednesday?

… Our analysis, including insights from our AI tool that we showed in Friday’s CoTD here, suggests recent media hints towards a 0.50% cut are weaker compared to the lead-up to June 2022's famous 0.75% hike.

Nevertheless, current market pricing suggests a cut closer to 0.40%. As DB’s Matt Raskin points out here, and as we update in today’s CoTD, the surprise component of the Fed’s rate move two days out is now the largest in over 15 years, regardless of whether they go 25 or 50. Matt believes that we’ll either see further press-led communications that steer the market back to 25bps today or that ultimately the Fed will deliver 50bps on Wednesday.

So the conclusion is that a quiet day today in terms of informed Fed speak in the press will likely tip the scales towards 50bps on Wednesday. So the next 12 hours are crucial in terms of press watching and will probably cement final pricing.

If you've been following DB's macro research over the last few days, you'll be aware of the view that if there was no informed Fed sources massaging the market back down to 25bps by the close of play last night, then the consensus here is that this would imply the Fed is leaning towards 50bps tomorrow night. For most of yesterday the market was pricing in around 40bps of cuts which as Matt Raskin pointed out in a great chart we highlighted yesterday (link here), left this meetings' pricing the furthest from both a 25 and 50bps move two days out from the meeting since for over 15 years. So a very rare level of uncertainty. As we type this morning, the pricing has ticked up further to 43.5bps, or in other words a 74% chance of a 50bp move. Overnight, we’ve had another WSJ article from Nick Timiraos, although it didn’t steer things in either direction and the headline indicates the ongoing uncertainty, saying “Fed Prepares to Lower Rates, With Size of First Cut in Doubt”.

In recent times, the closest parallel to this uncertainty is the decision in March 2023, amidst the regional bank turmoil. Before SVB’s collapse on March 10 last year, it was widely expected that the Fed would proceed with a rate hike on March 22. But as the turmoil grew worse, there were serious doubts about whether the Fed would still go ahead, and there were similar debates happening about whether a dovish decision might signal that things were worse than markets thought. Ultimately, the Fed did proceed with the hike, but on the Monday before the decision, futures were still only pricing it as a 73% chance, and right before the announcement it had only drifted up to 80%. So there was a little bit of doubt as to what they’d do, although not to the extent that we’re seeing today.

Of course, there are quite a few residual nerves today about going for 50bps. Indeed, on all the recent occasions when the Fed have accelerated up to 50bp cuts, bad things have then happened. That was the case when they opened in 2001 and 2007 with 50bp cuts, whilst the first Covid cut in March 2020 was also an initial 50bp move (followed up by a 100bp cut less than two weeks later). But although the precedents aren’t good, it’s worth bearing in mind that correlation isn’t causation, and it’s hardly like the GFC only happened because the Fed opened with 50bps. So it’ll be fascinating what history has to say about this time…

And a British operation weighs in on the 25 vs 50bps debate:

Don’t fight the Fed The FOMC announcement is due Wednesday. There will be a lot to digest. The traditional policy statement will be released at 2:00pm (EDT), along with the projections materials (including a new dot plot), and then Chairman Powell’s press conference at 2:30pm. The main takeaways we expect from the FOMC include:

We expect the FOMC to announce a 50bps rate cut on Wednesday

2024 median dot to show 75bp more in cuts to 4.125% (implying 50 in Nov & 25 in Dec?); close to equal split for the next preferred option: 50 or 100 more this year

2025 median dot to show another 125 bps to 2.875% in easing (vs 100 as of June)

2026 median dot at 2.875% (neutral) versus 100 as of June (2.750%) given earlier aggressive start to easing cycle

Dovish statement to indicate ongoing cuts & shift balance of risk on jobs to downside

SEP: Tad lower inflation & GDP, with higher (mark to market) unemployment in 2024

AND Paul Donovan weighs in … anyone else detect a note of sarcasm / jealousy? …

It is hedonism day in the US, with the release of August retail sales data. Two limits to the data. This is a value measure, and US goods prices have been falling for four months now. This underrepresents consumption at a time when people are still favoring fun over goods. Instagram reels of holidays and congealing restaurant meals cost money (and of that spending, only the congealing restaurant meals are captured in retail sales).

Does this matter to the Federal Reserve? A single data point should not matter to a well-run central bank, but it could matter to the Fed. Hopefully, alternative data sources (like credit card data) will allow the Fed to take a broader view than provided by a number that has been revised every single month this year.

US industrial and manufacturing production numbers are due, but the US is more important as a global consumer of last resort than it is as a global supplier of manufactured products.

… And from Global Wall Street inbox TO the WWW,

The Terminal.com with a warning from BLK …

Bloomberg: BlackRock Warns on Bonds, Saying Fed Rate Cut Bets Are Overdone

Quarter-point reduction enough given ‘robust’ job market: Li

Two-year Treasury yield approaches lowest since September 2022

AND from Authers …

Bloomberg: Bets Are In, But the Fed’s Still Running the Casino

If expectations are met at 50 basis points, the pressure will pile on for even bigger cuts. Powell has reason to call the market’s bluff

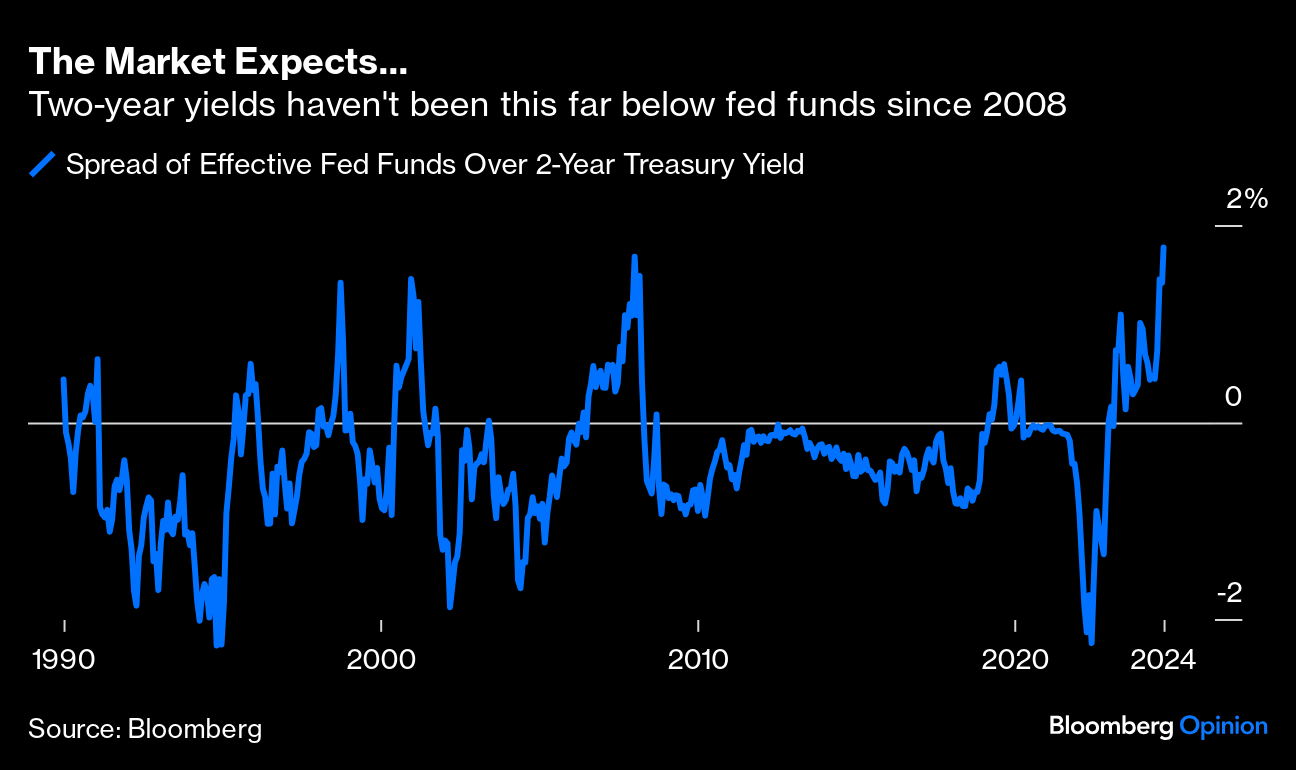

…At the end of last year, only one governor envisaged cutting rates as much in 2024 as the market now predicts. For next year, the market is way out of line with June’s dots — even though the data isn’t telling that different a story from three months ago. The Fed can change its mind, as it did between December and June. But it might well want to push back against confident expectations of easing, which will be easier without a jumbo cut this week. There’s also an argument that it should heed the bond market. The gap between the fed funds rate and the two-year bond yield is nearly two percentage points. It hasn’t been this wide since early 2008:

So what will the FOMC do? As it surely expects to cut by more than 50 basis points eventually, this is a question of risk management. Would they better guard against risks by starting moderately, or going straight to a jumbo cut? Joe Lavorgna of SMBC Nikko argues for 50:

From a risk management approach, it would be more prudent for the Fed to go big than to go small. A 50 bps September cut would still leave the funds rate about 100 bps above the highest estimate of the natural rate. A 25 bps fine tuning is not enough. Why go incrementally if inflation is trending lower and there is concern that the labor market may be on the cusp of a more meaningful slowdown? If monetary policymakers are confident that they will be cutting again, a larger initial rate cut gives them more optionality.

Lavorgna points out that the Fed started the 2001 and 2007 rate-cutting cycles with 50 basis points. However, the stock market had just imploded in 2001 with the S&P 500 down 16%. In 2007, the credit market had just collapsed, with the high-yield bond spreads having surged by 250 basis points in three months.

This note reiterates / illustrates another key tenet and is worthy passing along …

FirstTRUST: It’s Money, Not Spending, that Causes Inflation

…Some people wrongly assume that government borrowing creates money. But think about it. Who does the government borrow from? China, Japan, retirees, and banks all buy Treasury bonds. They buy them with dollars that they earned exporting to the US, working for incomes, or taking in deposits.

If any entity buys the debt of the US they no longer have the cash, the government does. Like Peter and Pauline, it is just a transfer of cash from one account to another. It doesn’t increase spending. If China buys debt, then they can’t buy imports with those same dollars. If banks buy debt, then they can’t make loans with that same money.

What is true is that if the Fed (or any central bank) creates new money (say with QE) and buys government debt, this injects new money into the economy. That IS inflationary. But it’s the money creation that caused the inflation, not the spending itself.

…Rate cuts and asset performance Historically, market performance has varied depending on whether rate cuts are initiated amid material economic weakness (a hard landing scenario) or more moderate conditions (a soft landing). Some examples:

Intermediate- and longer-term bonds have performed well, especially in hard landings. Cash rates are likely to come down as the Fed lowers its short-term policy rate. Bonds of intermediate and longer duration can benefit from price appreciation and historically have tended to perform well during cutting cycles (see Figure 1), particularly if the economy weakens.

Figure 2: Yield curves have tended to steepen after the Fed starts cutting rates…

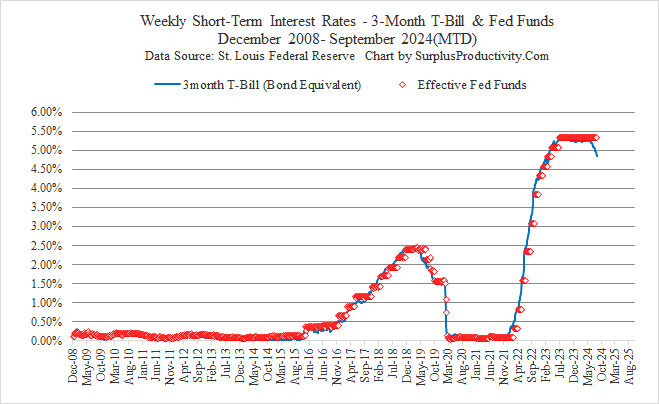

Do these visuals of FF and short (3mo TBILL) rates ever get old on the eve of the first (of many?) cuts … i’m passing along this one which is def in SURPLUS …

September 16th, 2024 - Volume 10 (2024), Missive 212 (Monday)

This week’s Fed cuts are too long in coming

The curves believe the change in heart is only half-hearted

Banks will fight against lower rates

Those who do, can. Those who don’t are passed over for those who are willing and able. These garbled statements are not the product of some centuries old philosophy, but rather our poor attempt to qualify what a quantifiable mess the approach to monetary policy has been these past few years and an economy that has lost almost all patience with the financial sector’s ability to come through. All of this begins and ends with surplus productivity, of course, which by itself isn’t the issue. The problem stems from this force being allowed to spread across the entire economic landscape, not only unencumbered by the Fed, but also amplified by it through the mistaking of price volatility for price inflation. Now as the upward price volatility subsides in the product market, the downward price volatility in the resource market, specifically that of the labor market, is on much fuller display; something not easily remedied by an institution that works through a displaced financial sector in order to achieve economic goals.

The short-term Treasury market knows the Fed has pushed rates way too high for way too long.

It always comes to a bit of shock to many when they realize the Federal Reserve is an institution set-up to use the economy’s financial sector in order to achieve economic goals and not the other way around. Just like the fallacy of printing money (controlling the supply of money has nothing to do with the actual quantity of currency and everything to do with the quality of currency, more on that for a future missive), the Fed isn’t charged with being a ‘lender of last resort’. What they are in charge of is ensuring

AND the good prof. Jeremy STOCKS FOR THE LONG RUN Siegel weighs in …

WisdomTree: Prof. Siegel: Market Strength as Rate Cuts Loom

… Regarding the Fed's anticipated actions, the market expects a steady series of rate cuts. My read of the Fed Funds Futures market shows the expectation of seven rate cuts in a row between now and next June—one cut at each meeting when you factor in the risk premium and hedging features these futures contracts possess (which actually show more than nine 25 basis point (bp) cuts).

This would ideally align with the long-run equilibrium real funds rate that I have been advocating between 3.5% to 4%. I would like the Fed to move quicker, as you all know, but so far, the market is comfortable with the Fed Funds Rate reaching the three handle by the middle of next year. I anticipate them to start with a 25 bp cut this week unless the retail sales report is unusually weak…

…And for the market as a whole, the 10-year U.S. inflation adjusted bond yield reached 1.6% on Friday. With the S&P 500 selling at nearly 20 times earnings and a 5% earnings yield, I see the equity premium as being approximately 3.4%—which is very close to the long-term data in my book Stocks for the Long Run. Both stocks and bonds are expensive compared to historical levels—but each by about the same amount—and still support the case for stocks.

I'm preparing for Disappointment....

Powell/The FED has been uncharacteristically unclear...not sure why...

Except that they maybe as unsure, as we are and that's not so good...