First UP, am happy to report that despite the occurences in private credit yest …

Bloomberg: Blue Owl Limits Investor Withdrawals, Stirring Private Credit Concerns

Bloomberg: Blue Owl’s Woes Expose Private Credit Risks for Retail Investors

Bloomberg: Blue Owl Sold Private Loans to Pension Giants and Own Insurer

(Bloomberg) — Blue Owl Capital Inc. (OWL), facing a looming deadline to return cash in one of its private credit funds, found four buyers for a $1.4 billion portfolio of loans to help pay out investors: Three of North America’s biggest pension funds and its own insurance firm…

… the markets seem to be CALM, at least for now. It is with that calm in mind, I’m drawn to following visual as the day begins and the week comes to a close …

… kindly note DAILY momentum overBOUGHT and so a close above 4.075% would suggest to me a pause in the bond market rally of late…

… #Got10s? I will have a look at WEEKLY over weekend but for now and with this level (4.075%) in mind (as well as the geopolitics of the moment — Earl putting UPWARDS pressure on yields while, well, WAR might offer some counterbalance / F2Q bid), I can’t help but think of 4.075% TLINE in more technical terms …

'Tis but a scratch … Moving right along, 10s and private credit aside, we also had DATA:

ZH: Initial Jobless ClaimsTumble Back Near Multi-Decade Lows

ZH: US Trade Deficit UnexpectedlyWorsens As Exports Slump Again In December

ZH: US Pending Home Sales Hit Record LowDespite Falling Mortgage Rates

WolfSt: Pending Home Sales Plunge to Record Low in the Data, from Already Low Levels, on Big Drops in the South & Midwest

… Not sure if the data mattered / matters as much as the Blue Owl situation OR today’s data and SO … I’ll quit while I’m behind and hope to have something more over the weekend…

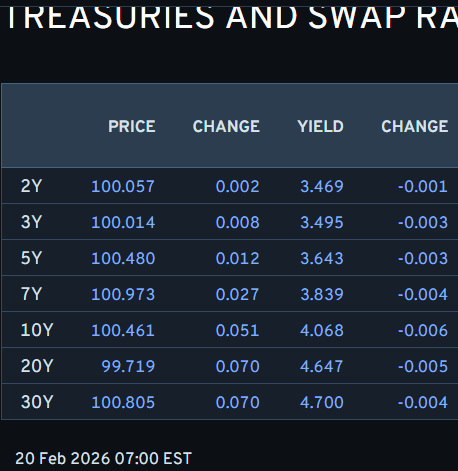

Onwards and upwards TO the reason many / most of you are likely here … whatever it may be on Global Wall’s mind but first … here is a snapshot OF USTs as of 700a:

… for somewhat MORE of the news you might be able to use … a few curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures are flat; US President Trump reportedly weighs a limited strike to force Iran into a nuclear deal … USTs are near enough flat in thin 112-29+ to 113-02 parameters. Specifics for the space are somewhat light thus far as we count down to a packed 13:30GMT data docket and await any further insight on US-Iran tensions before potential SCOTUS opinion(s) at 15:00GMT.

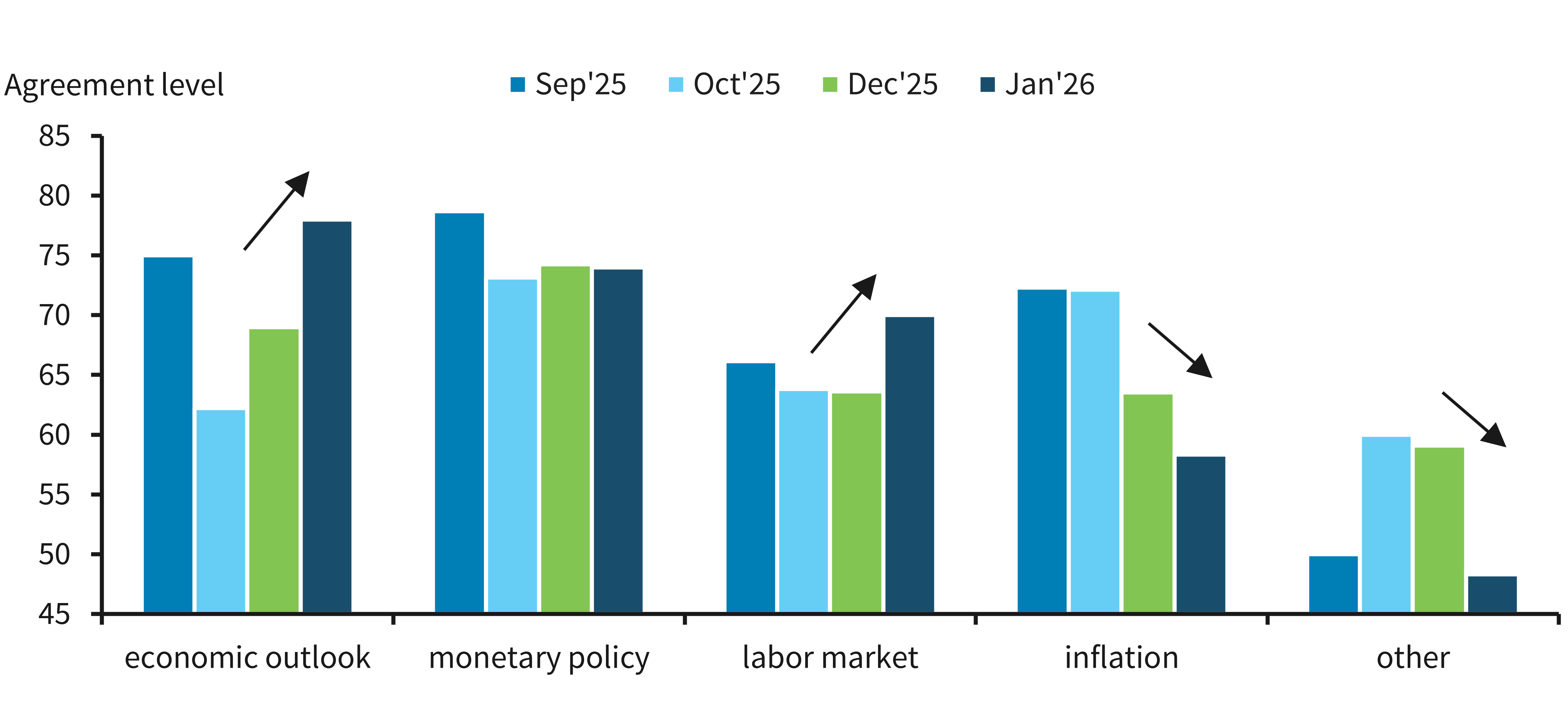

Our NLP analysis of the January minutes suggests that participants became less aligned on inflation, with inflation agreement at the depressed level of mid-2019, offset by increased consensus on the economic outlook and labor market. Division remains on the future course of monetary policy.

…Figure 1. FOMC minutes agreement indicators suggest more agreement on the economic outlook and labor market, but divergence increased on inflation

…On net, it was a bond-bearish round of data that has contributed to the modest weakness in US rates. However, the selling pressure has been contained with yields 1-2 bp higher across the curve. From here, this afternoon's 30-year TIPS auction will round out this week's supply as investors await tomorrow's core-PCE/GDP reports…

…Thursday’s price action left us pondering whether the 10-year has simply swapped one trading range for another. Recall that from mid-December until mid-January, 10-year rates were stuck in a range of effectively 4.10% to 4.20% – a period that was also characterized by declining vol and questions of when and how the range would break. In the wake of Trump’s Greenland comments in Davos, the range decidedly broke in favor of higher yields, momentarily topping 4.30%. The selloff ultimately proved short-lived and by early in the next week, 10-years were back in the alltoo-familiar 4.10% to 4.20% zone. Follow-through from the last rally brought 10s to 4.016% only to see the bullish move fail to breach 4.00%. Today’s session reinforced the relevance of 4.10% as key support for 10s, giving rise to our concern that the ~10 bp range that was so persistent around the calendar turn has just been set slightly lower as investors await the next meaningful shift in the fundamentals and/or monetary policy bias.

A similar case can be made for the 2-year sector – swapping 3.50% to 3.60% for a marginally more bullish 3.40% to 3.50%…

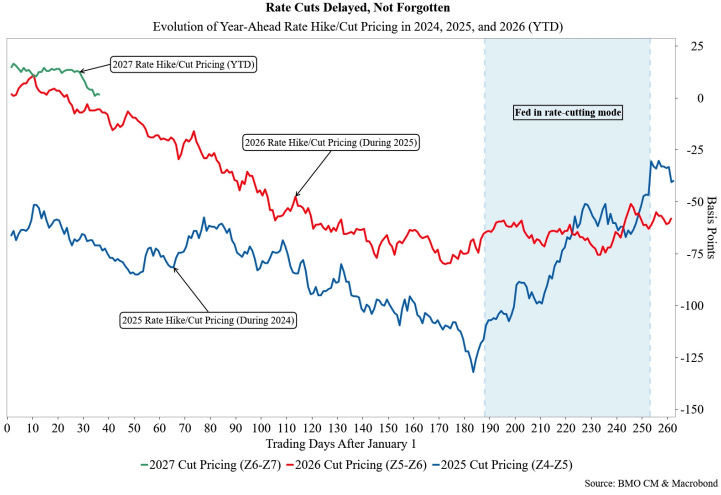

February 19, 2026 BMO Normalization Delayed, Not Forgotten

A familiar aspect of the evolution of monetary policy expectations so far in 2026 is that while rate cuts have been delayed, they haven't been forgotten. After holding rates steady in January, the market-implied odds of a March rate cut have dropped to 6% from 25% two weeks ago, but the assumption remains that the Fed will deliver 2-3 rate cuts by the end of the year. The market has a long history of simply rolling forward rate cut pricing with the passage of time, consistency of Fed messaging, resilience of the labor market, and stickiness of inflation. In the current episode, it was the strength of the January payrolls report that has kicked the can for rate cuts further into the future. In this context, the chart below helps illustrate the market's tendency to replace more hawkish Fed pricing in the near-term with more dovish Fed pricing in the medium/long-term.

…If the performance of these two curves in 2024 and 2025 offers any guide, there is ample scope for the Z6/Z7 curve to flatten in 2026 if the US economy is, once again, resilient enough to delay rate cuts until later in the second half (and 2027). In fact, a flatter Z6/Z7 curve will likely be the path of least resistance unless the Fed transitions back into ratecutting mode before the end of Powell's term as Chair. The flattener also stands to benefit from a scenario in which the incoming Chair doesn't deliver rate cuts as quickly as the market is assuming during their first several meetings in the role.

To be sure, given the closer proximity of fed funds to the neutral rate of interest, we don't see as much downside potential for Z6/Z7 in 2026 as what might be implied by the 80+ bp of flattening in Z4/Z5 and Z5/Z6 in the last two years. Nonetheless, a move to the -25 to -50 bp zone is within the cards so long as rate cuts continue to be delayed into 2H26, and terminal estimates remain anchored near 3.0%, leaving the broader cutting bias intact…

A note on POSSIBLE SCOTUS ruling (on fiscal and the flation) as well as the view of economy from 30,000 feet above …

…The latest developments saw President Trump seemingly issue an ultimatum to Iran, suggesting that 10 to 15 days was the maximum he would allow for talks to continue and that Iran must make a “meaningful deal” or else “bad things would happen”. Those comments came as the US has deployed aircraft and naval ships to the Middle East ahead of a possible strike on Iran. Later in the day, the Wall Street Journal reported that while President Trump had not yet decided on military action, he could authorise a limited strike within days, and this would then be followed by a broader US campaign against the regime if Iran failed to comply.

So that led to a sell-off in markets, with 60% of the S&P 500 down on the day, as investors pulled back over fears of geopolitical conflict. The Nasdaq (-0.31%) and Magnificent 7 (-0.21%) also declined. Bonds were caught between the inflationary consequences and the risk-off mood, with 2yr (-0.3bps) and 10yr (-1.6bps) Treasury yields moving slightly lower. Against this risk-off backdrop, gold (+0.37%) poked back up above $5k before closing at $4,999/oz while silver (+1.69%) also outperformed. The VIX volatility index (+0.61pts) crept back above 20 to close at 20.23.This morning, US and European equity futures are back up a couple of tenths and Gold and 10yr USTs are largely unchanged…

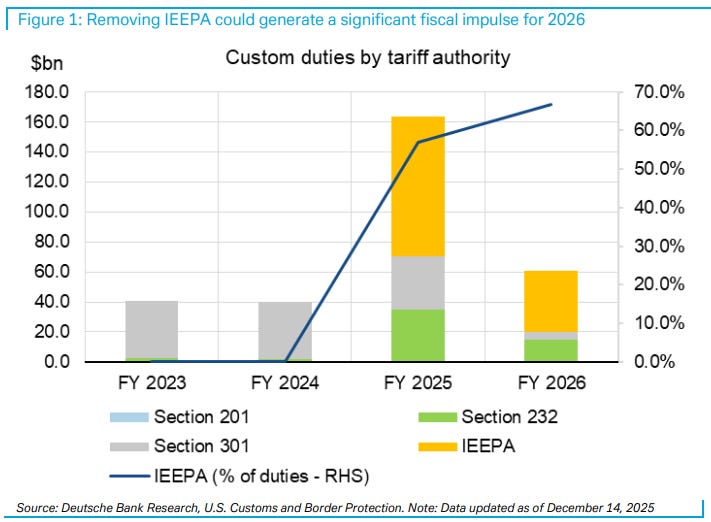

19 February 2026 DB IEEPA ruling: A risk for fiscal & inflation

In its recent fiscal outlook, the CBO projects receipts from customs duties of USD418bn (1.3% of GDP) this year, assuming an average import tariff rate of ~15%. Actual revenue from import duties has however been lower than implied by statutory tariffs, with the most recent three-month run rate at ~USD28bn, or 336bn annualised (1.1% of GDP). Moreover, betting markets imply a ~75% probability of a Supreme Court ruling against IEEPA tariffs. The latter account for the majority of the import duties collected over the past year, with CBP data implying that ~60/70% of the FY25 & FY26 duties was collected under IEEPA authority (Figure 1). This suggests that without IEEPA, tariff revenue could be expected to be around 0.5% of GDP, at least if the revenue is not replaced by other tax/tariff measures or spending cuts--implying a positive fiscal impulse for this year.

As far as the inflation impact is concerned, a possible removal of IEEPA tariffs would be significant in principle, not only because of their high share in overall duties, but also because, apart from section 232 auto tariffs, consumer goods tariffs are typically imposed under IEEPA and are hence more directly relevant for CPI inflation than remaining ‘sectoral’ tariffs. In practice, the assessment is complicated by the fact that a significant part of the price effects have already occurred. Whether a ruling against IEEPA could lead to actual price cuts or a flatter inflation trajectory going forward is likely to depend on the modalities of possible replacement tariffs as well as on whether already collected duties will be refunded. While betting markets only see an outside chance of the latter, on balance, the SCOTUS IEEPA decision remains a downside risk for 1y CPI and a bearish risk for front-end real yields.

…United States Growth: We project solid growth in 2026 (2.4% for Q4/Q4), with H1 even stronger (2.75% average). Tailwinds include easy financial conditions from Fed cuts, fiscal support (larger tax refunds), and reduced trade uncertainty. Risks are skewed to the upside, but some cautions remain: weak hiring, fragile lower-income households, and potential AI-driven layoffs.

Labor market: There are growing signs that the labor market has stabilized. The unemployment rate has dipped to 4.3%, and we expect it to stay near these levels into year end. Payroll gains have recently exceeded a much lower breakeven level (~50k jobs/month) on constrained immigration. Demand and hiring are expected to firm with growth, but layoff risks persist.

Inflation: Disinflationary forces are expected, with shelter decelerating and core goods reversing tariff bumps. However, unwinding shutdown distortions keeps core PCE mostly flat at 2.6-2.7% through end-2026. Risks are skewed to the downside: lower tariffs (e.g., due to limitation of IEEPA powers) could reduce goods prices, softer energy/shelter could lower broader inflation, and productivity gains could put greater downward pressure on unit labor costs.

Fed: Policy rules suggest rates should be at or above current levels on our forecast. Nonetheless, we expect the Fed to cut rates once this year in September, placing the fed funds rate at 3.25-3.5% by year end, slightly accommodative. This rate cut reflects building disinflation evidence and a potentially more dovish FOMC under Warsh’s leadership. QT has stopped, and Reserve Management Purchases have reinitiated. Returning to balance sheet shrinkage – a stated goal of Warsh – likely requires regulatory changes first.

Risks: Recession risks are close to or slightly below historical averages. Upside risks are also present from additional fiscal support and the potential for AI to lead to a stronger-than-expected productivity boom. Policy risks include impingement on Fed independence or renewed concerns around debt sustainability…

February 20, 2026Macro still being driven by GEO …

Oil rises to $72/bbl as US-Iran tensions continue; geopolitics weigh on risk assets; strong 30y TIPS auction; strong Australia employment data; Peru elects interim president; Colombia continues push for minimum wage hike; potential IEEPA ruling Friday; DXY at 97.9 (+0.2%); US 10y at 4.07 (-1.0bp)

…Despite upward pressure from oil prices, Treasury yields close roughly 1bp lower across the curve, supported by a strong TIPS auction and a risk-off rotation from equities…

US President Trump suggested that Iran had 10 or 15 days to do a deal, or face (unspecified) negative consequences. The US military presence in the Gulf means investors have given more weight to these remarks. Oil prices have moved higher—not dramatically, but enough that it might be visible to the US consumer in a few weeks. That has a bearing on inflation perception and the US affordability crisis.

Affordability is not the cost of living, and not necessarily about economic reality. Today’s December US personal income and spending figures should show ongoing consumption. After tariff induced volatility early in 2025, consumer spending growth stabilized as savings rates were reduced to pay for tariffs.

The US PCE deflator is expected to stay just below 3% on both headline and core readings. The Fed minutes signaled a divergence around inflation (and thus policy), but this is about future inflation. Current increases in inflation are factored into Fed thinking…

Not usually a fan of trade deficit / explanations but this one seemed different …

February 19, 2026 Wells Fargo: Gold Explains Some, Not All, of Sharp Widening in December Trade Deficit

Summary

A large $17.3 billion widening in the December trade deficit reflects a $5 billion drop in exports and a more than $12 billion jump in imports. The size of these moves overstate the impact on Q4 GDP growth and the extent of recent demand.

The trade of non-monetary gold accounted for more than half of December’s widening. Since this is excluded from GDP it blunts the impact of net exports on GDP.

Prior to today’s report we had anticipated a 0.7 percentage point boost from trade on Q4 real GDP growth. That lift is now poised to shrink. In fact, we might even see a slight drag on growth from trade due to stronger than anticipated imports.

All told goods imports finished the year down and were way down when excluding the lift from a sharp increase in high-tech related imports.

So are we now a country that simply imports less than it did before? We think the pullback in imports last year is overstated and is at least partly a result of wait-and-see around tariffs in 2025. Looking ahead there will inevitably be more rejiggering in supply chains, but we see scope for a modest ascent in imports in spite of tariffs in the year ahead.

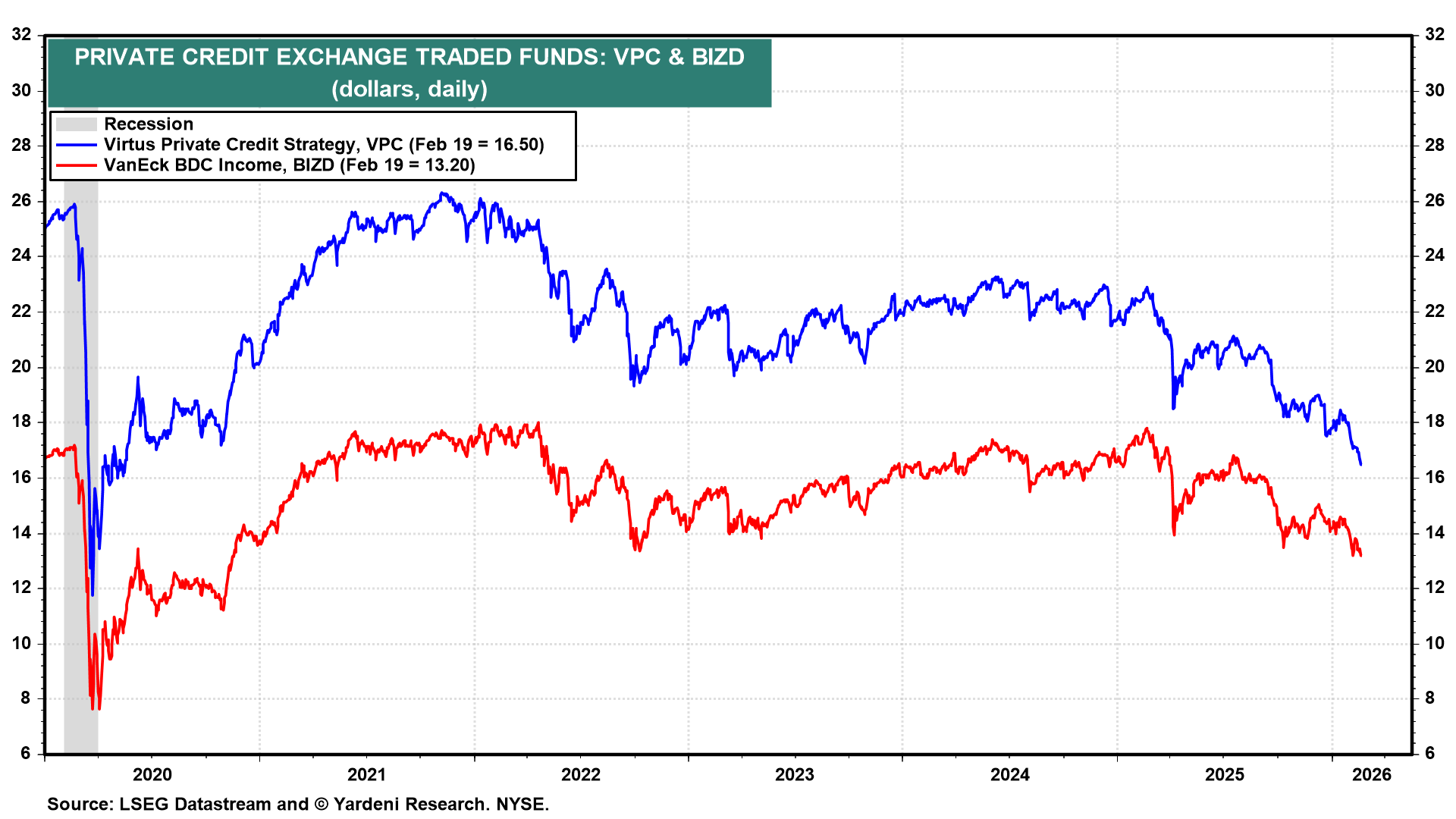

Finally, a few thoughts (and couple excellent visuals) from the good doctor … think PRIVATE CREDIT …

Feb 19, 2026 Yardeni 4724: The Year Of The Fire Horse

Happy Lunar New Year! Last year was the Year of the Wood Snake, according to the Chinese Zodiac. In Chinese culture, the Snake is often seen as a symbol of wisdom, intuition, and transformation. The Horse is one of the most beloved zodiac signs. It is a powerful symbol of energy, freedom, and rapid success. Because the Horse is a social and high-spirited animal, its year is usually expected to be fast-paced and full of movement.

While the Chinese year 4724 has just started, 2026 has already been a wild ride in the stock market, with a dramatic rotation of market leadership from the Magnificent-7 to the Impressive-493. Despite the weakness in the Mag-7, the S&P 500 has held up remarkably well. It is continuing to do so despite the increasingly likely prospect that the US will attack Iran in a matter of days, which has raised the price of a barrel of Brent crude oil from around $60 at the start of the year to over $70 (chart).

Concerns about private credit have also been increasing. Today, Blue Owl Capital shares tumbled after a decision to restrict withdrawals from one of its private credit funds raised fresh concern over the risks bubbling under the surface of the $1.8 trillion market. We’ve been monitoring the falling prices of ETFs that invest in the shares of private credit companies since late last year (chart). We don’t expect a Lehman Moment in the private credit market, but it is included in our “what-could-go-wrong” scenario, to which we currently assign a 20% subjective probability. We include geopolitical risks in this bucket, too…

… Moving along TO a few other curated links from the intertubes. I HOPE you’ll find them as funTERtaining (dare I say useful) as I do … …

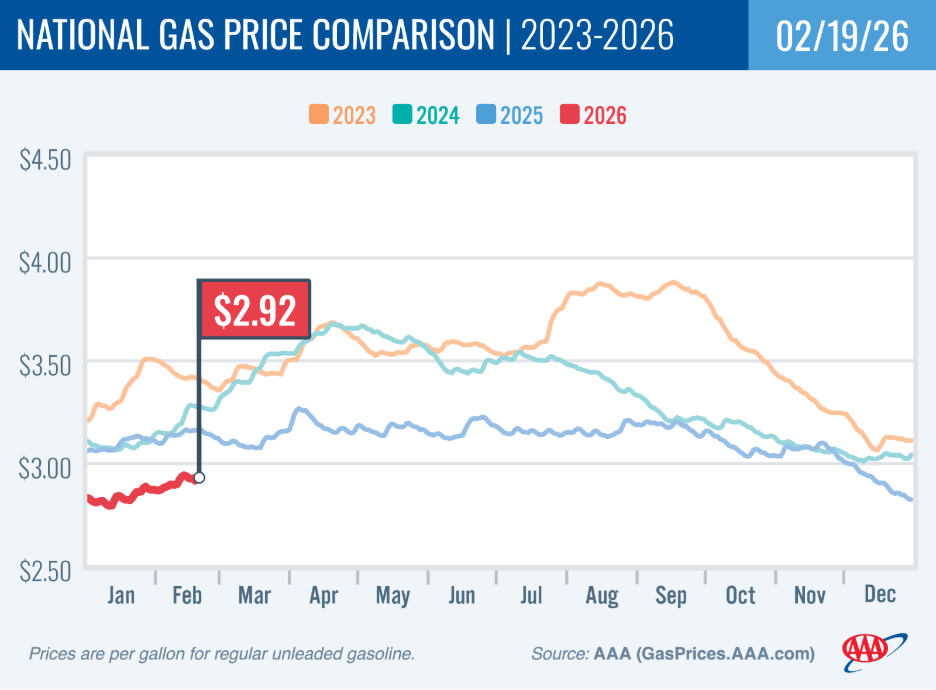

Gas pumps sleeping with one eye on Iran …

February 19,2026 AAA: Pump Prices Holding Steady For Now

WASHINGTON, DC (February 19, 2026) – The national average for a gallon of regular gasoline dropped slightly from the previous week to $2.92. Pump prices are expected to start their seasonal climb soon, as spring approaches and summer-blend gasoline production begins. Tensions between the U.S. and Iran are another factor that could drive up crude oil prices. Right now, gas prices are the lowest they’ve been for this time of year since 2021.

…next UP, the good Doctor SLOK says it was a strong BOND AUCTION …

February 20, 2026 Apollo: Strong 30-Year Treasury Auction

The latest 30-year Treasury auction shows continued strong buying of US duration with public tendered demand at the highest level on record, see chart below. Indirect bidders, who are normally a proxy for foreign demand, took 69.8%, well above the historical average at 64%. Primary dealers, who have to buy what others don’t, were left with only 5.9%. The bottom line is that Treasury auction metrics show that there continues to be very solid demand for the long end in US Treasuries.

… welp, so much for the END OF THE WORLD is coming, CHINA SELLING, we’re all gonna die, narratives … I mean, yeah, sure, we’re all gonna die BUT … China’s been selling for over a decade so … as long as rates are steady and high enough to attract buyers, then more power to ‘em (Uncle Sam and cousin Scott) …

There are fates far worse than Death or Recession....