Bloomberg: Goldman Flags $100-Plus Brent If Hormuz Shut Another Month

Bloomberg: Oil Rises After Biggest Drop Since 2020 as Hormuz Stays Blocked

CNBC: U.S. has violated ceasefire agreement, Iran parliamentary speaker says

… AND a few thoughts …

First off, I’m reminded that there are days where there’s lots to offer and there are days like today, where I’ve less than ‘lots to offer’ and so, yer time being money, I’ll be real brief. I’m reflecting back to a time where I was in a different seat and this day, 6yrs ago, was another of those HOLY COW moments … Allow me to be the first to wish you a happy Fed Nationalized the Bond Market Day! On this day in 2020 …

ZH: The Day The Fed Nationalized The Bond Market: The Complete Summary Of Everything The Fed Did Today

April 9, 2020, 2:46 PM UTC Bloomberg: Fed Is Seizing Control of the Entire U.S. Bond Market In a dramatic move, the central bank extends its reach into munis, fallen angels and more.

… “Our emergency measures are reserved for truly rare circumstances such as those we face today,” Fed Chair Jerome Powell said in a webcast Thursday. “When the economy is well on its way back to recovery, and private markets and institutions are once again able to perform their vital functions of channeling credit and supporting economic growth, we will put these emergency tools away.”..

… AND with that in mind, actions from 6yrs ago remain top of mind to those still in a seat, lets jump in …

Based on price action (and somewhat lower demand into yesterday’s bid for bonds more in a sec), we’ll likely need some sort of concession (aka #DipOrTunity) for this afternoons $22bb 30yr auction. Here’s a look at yields, nearer ‘support’ …

… and as yields are nearer supportive TLINE (4.95%), momentum has shifted and become overBOT, meaning a ‘concession’ would be extremely welcomed development …

#GotBONDS? You draw yer lines and I’ll keep drawin’ mine and the triangulation above is a guide that’s proven useful … Sure rates could drop as momentum presses further into overBOT territory … Ahead of this afternoons supply, would that be ‘position A’? Prolly not.

Again as rates have moved lower, in concert with other asset classes celebrating the art of the latest deal, demand for yesterday’s supply in face of the bid, DIPPED and so, not the ‘stellar’ auction seen for 3s …

…The internals also disappointed, as foreign demand slumped from March with Indirects awarded 65.32%, down from 74.45%, and below the recent average of 68.78%. Directs offset much of this drop, rising to 23.88%, almost double the 12.83% in March and the highest since January. Dealers were left holding 10.8%, down from 12.7% the previous month, but in line with the average of 10.05%.

Overall this was a slightly subpar auction, especially after yesterday’s stellar 3Y auction, but in light of the bid drop in yields across the curve and the lack of concession, it priced roughly where it should have and the market has barely reacted as one would expect.

Overnight, the much-hyped Iran deadline passed with a ceasefire headline—cue the selloff. Equities slipped as “peace” removed the panic bid but not the uncertainty premium; oil, of course, stayed bid anyway, because why not. Treasuries? Unmoved—10s hovering, 30s steady, 2s pinned—like a market that’s seen this movie before and already knows the ending…

…Ceasefires may stop bullets, but they rarely stop basis points.

… NOT terrible … Get those bond bids in early and often!

Onwards and upwards TO the reason many / most of you are likely here … whatever it may be on Global Wall’s mind but first … here is a snapshot OF USTs as of 700a:

… for somewhat MORE of the news you might be able to use … a few curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Crude at highs but below USD 100/bbl amid concerns on US-Iran ceasefire fragility … Fixed benchmarks pull back from highs, US PCE ahead … USTs are currently flat, and mildly outperforming vs peers – currently trading within a 111-04+ to 111-10 range, and have entirely reversed the initial ceasefire-related optimism. Much of the action facilitated by the geopolitical factors mentioned above, but the complex is also weighed on by hawkish-leaning FOMC Minutes and heading into a 30yr auction later today. On the data front, markets will await weekly claims, February’s PCE data (exp. +0.4% M/M vs prev. +0.3%) and core PCE (exp. +0.4% M/M vs prev. +0.4%); final Q4 GDP stats. From a yield perspective, the 2yr has rebounded back towards 3.785% (vs Wednesday’s trough at 3.713%).

Yield Hunting Daily Note | April 8, 2026 | Ceasefire Rebound, Liberty Funds Raise, Brookmont IPO, ECC Baby Bonds

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS of Global Wall you might be able to use …

A large British operation on recent FOMC mins and INCREASING ‘flation concern …

The minutes indicate increased concerns about elevated inflation. Some participants wanted to convey a hawkish message, but many remained of the view that rates should be lowered if inflation declines. We retain our expectation of a 25bp cut in September 2026 and again in March 2027.

Best in show on FOMC mins and SMRA portfolio survey …

BMO FOMC Minutes: “Strong Case” for two-sided language on interest rate path

The Minutes for the March 18 FOMC Meeting said, “Some participants judged that there was a strong case for a two-sided description of the Committee’s future interest rate decisions in the postmeeting statement.” Recall that the January statement said ‘several’ participants would have supported such a two-sided description. The upgrade from ‘several’ to ‘some’ offers a hawkish undertone to the Fed’s guidance, as does the fact that this camp now sees a ‘strong case’ for acknowledging the risk that the next Fed move is a hike, not a cut. Given that Powell took a neutral stance on the implications of the war at the press conference, it was unsurprising to see the Minutes emphasize the growing risks on both sides of the Fed’s dual mandate.

The dovish risk: “In particular, most participants raised the concern that a protracted conflict in the Middle East could lead to a further softening in labor market conditions, which could warrant additional rate cuts, as substantially higher oil prices could reduce households’ purchasing power, tighten financial conditions, and reduce growth abroad.” The hawkish risk: “Many participants pointed to the risk of inflation remaining elevated for longer than expected amid a persistent increase in oil prices, which could call for rate increases to help bring inflation down to the Committee’s 2 percent objective and keep longer-term inflation expectations firmly anchored.” Note that ‘most’ were worried about the dovish risks, whereas ‘many’ were worried about the hawkish ones. This skew makes sense given that the dotplot retained the broader rate-cutting bias for 2026 and 2027.

Echoing the messaging from Fed-speakers over the last few weeks, the Minutes said, “Most participants reiterated, however, that it was too early to know how developments in the Middle East would affect the U.S. economy and judged it prudent to continue to monitor the situation and assess the implications for the appropriate stance of monetary policy.” Given that the ‘vast majority’ of Fed officials judged that upside risks to inflation and downside risks to employment were elevated, steady policy rates will likely prevail until there is a more compelling skew to the perceived balance of risks…

…SMRA Portfolio Survey – the arithmetic measure ticked down to 100.7% from 100.9%. The asset weighted gauge was unchanged at 100.5%. It was noted that, “the responses to this week's SMRA/OE Portfolio Manager Survey were collected prior to the cease-fire agreement between the US and Iran, and the resulting large market adjustments.”…

…Recall that our approach to navigating the conflict in the Middle East has been to focus on timing the inflection point at which investors cease trading every headline in favor of moving on to the next macro narrative. It is still too soon to declare that trading the war is over. Nonetheless, the ceasefire and subsequent drop in oil prices imply that such a transition in trading behavior has moved closer. For the Persian Gulf to be deemphasized in terms of the impact on global financial markets, shipping traffic through the Strait of Hormuz needs to be convincingly restarted and the ceasefire needs to continue without further aggression. Reports of progress toward a peace deal would also afford investors the capacity to more diligently assess the implications for growth, inflation, and valuations. It isn’t lost on us that expecting stability and a de-escalation of tensions in the Middle East has yet to be a prudent approach, which emphasizes the cautious aspect of any signs of budding optimism…

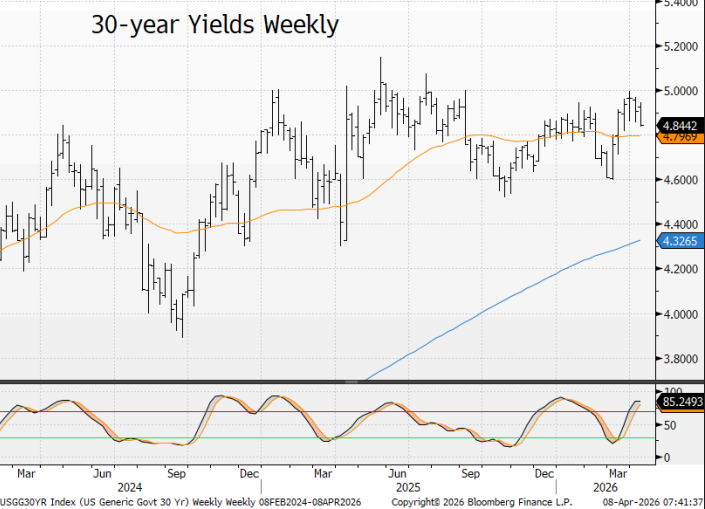

…30s – The 30-year point was the decided underperformer on the curve following the news of a two-week deescalation, likely a function of the uncertainty regarding not only whether the next two weeks lead to an official end of the conflict, but also where oil/gas prices will eventually bottom. First resistance is the Bollinger Band bottom at 4.827%, closely followed by the 100- and 200-day moving averages at 4.803% and 4.796%, respectively. If traded through, we see a void of resistance until the next bullish hurdle at 4.75%. In terms of support, the first order of business is filling an opening gap at 4.862% to 4.870%. 4.893% is the Bollinger mid, closely followed by a prior key trading level in sector at 4.90%. Through there is the Bollinger Band top at 4.958%.

…That backdrop of lower energy prices meant that inflation fears eased dramatically, which in tun led to a dovish repricing of central banks, especially in Europe. For instance, the 1yr US inflation swap plummeted by -12.9bps to 3.13%, and the 1yr Euro inflation swap fell by a huge -38bps to 3.11%. In turn, that saw investors price out the likelihood of rapid rate hikes, with the probability of an ECB hike this month down from 68% before the ceasefire announcement to 32% by yesterday’s close, and a further decline to 29% this morning…

…US Treasuries saw more muted moves, given yields had already fallen late in Tuesday’s session and oil prices were edging higher later in the US session yesterday. So both 2yr yields (-0.1bps at 3.79%) and 10yr yields (-0.2bps at 4.29%) were little changed by the close, having been 6-8bps lower on the day early on. We also got the minutes of the March FOMC meeting, which showed the uncertainty on how officials should respond to the war’s impact. It said that “most participants” were concerned that “a protracted conflict in the Middle East could lead to a further softening in labor market conditions, which could warrant additional rate cuts”. But it also said that “Many participants pointing to the risk of inflation remaining elevated for longer than expected amid a persistent increase in oil prices, which could call for rate increases”…

Ceasefire and NO CUTS with sturdy labor markets along with sticky ‘flation …

…Bottom line, it is very difficult to economically justify Fed cuts given that (1) the unemployment rate is broadly stable, (2) inflation is likely to be sticky above 2% and (3) policy rates are unlikely to be restrictive. Moreover, one can argue that the upside to fiscal policy would make rate cuts even more difficult to justify. The main risk to the view remains both tails on AI: bubble or a significant impact on the labour market.

STOCKS … a precap of earnings — things OK, beats not as beat’eee

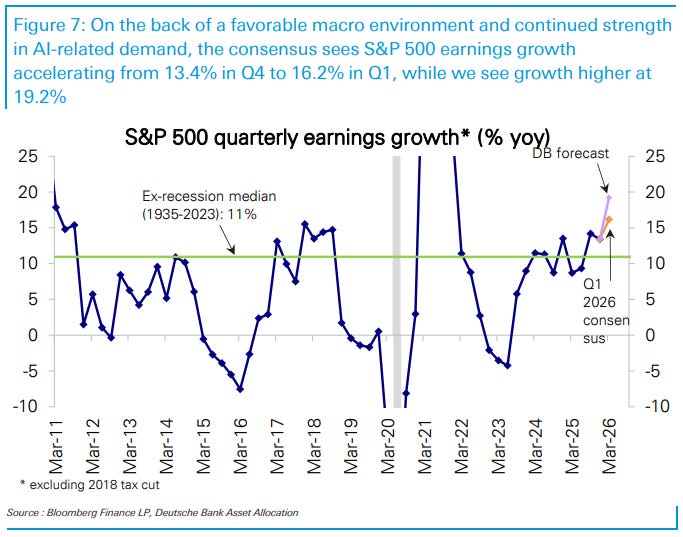

08 April 2026 DB: Asset Allocation - Q1 2026 Earnings: Looking For A Four-Year High In Growth But Modest Beats

The bottom-up analyst consensus for Q1 earnings is exceptionally strong, seeing growth for the S&P 500 accelerating into the mid-teens (16%), a level very rarely expected at the start of any earnings season. While this sets a high bar, we see it justified by a favorable macro environment with cyclical growth drivers picking up and a significant tailwind from a lower dollar, combined with the familiar boom areas growing even faster. Indeed, we expect growth to come in even stronger at 19%, a four-year high, but for the beat to be modest. We see growth continuing to broaden across sectors, with 10 out of 11 in positive territory, but to be clearly led by MCG & Tech (36%) and the Financials (20%). Equity investor positioning meanwhile is significantly underweight and in line with an imminent collapse in earnings growth. Positioning is notably low for sectors in the market cross hairs currently, like Financials and Tech, especially Software.

After all that, little changed to slightly weaker? Really? Yep …

US-Iran ceasefire saw oil decline and equities rally; FOMC minutes stayed hawkish; Treasuries reversed early gains as truce doubts re-emerged; Europe led the rates rally; EM FX rebounded; RBI held at 5.25%; DXY at 99.04 (-0.8%); US 10y at 4.30 (+0.2bp)…

…US Treasuries finished little changed to slightly weaker after an overnight bull-steepening gave way to a late-session fade (2y: 0bp; 10y: +0.2bp; 30y: +2.0bp). The initial rally tracked the collapse in oil and the relief bid after Washington and Tehran agreed to a two-week ceasefire tied to reopening the Strait of Hormuz, but the move retraced as headlines raised questions on how durable the de-escalation would be. The $39bn 10y reopening was acceptable rather than strong, tailing slightly at 4.282% versus 4.280% when-issued, while bid-cover at 2.43 pointed to only middling demand…

In economic terms, the Gulf ceasefire has not held. Iran has closed the Strait of Hormuz in response to significant Israeli strikes against Lebanon. The optimistic bias in markets means that only some of yesterday’s risk market gains have been surrendered. The demonstration of relative power in the Gulf is relevant when considering long-term risk premia around global supply chains.

Revised US fourth quarter GDP will be released, along with personal income and spending data for February. Although the data predates the soaring price of gasoline, there is still useful content. The way tariffs impact spending power is similar to the impact of higher oil prices. US consumers met the tariffs by cutting savings to maintain spending. That should be the (short-term) response to the oil price shock.

The March Federal Reserve minutes might politely be described as “even-handed”. There was concern expressed about labor market weakness, although whether rate cuts can remedy that is not necessarily clear. Immigration and tariff policies have both had a bearing on employment, and monetary policy has little impact there…

Not seen much from this COVERED WAGONS shop since Porcelli took over … still thinking 2 cuts and 10s to end year at 4.25% — an inherited f’cast or something new and different? You decide…

Monthly — April 8, 2026 Wells Fargo: U.S. Economic Outlook: April 2026

Geopolitical disruption has turned into a near‑term inflation shock. The ongoing Iran conflict has pushed oil prices higher, lifting headline inflation, eroding real income and spending, and delaying the timing of Fed easing in our forecast.

March consumer inflation will break disinflation. Higher energy prices have fed quickly into prices at the pump, ending the two‑year disinflation trend. With oil elevated and no clear resolution in the Middle East, we expect firmer inflation ahead, and forecast headline PCE peaking at a year-ago pace of 3.7% in Q2 and core PCE remaining sticky in a 2.7–3.1% range through year‑end.

Consumer spending is resilient but looks shaky. While spending has so far absorbed higher gas prices, we expect a more visible hit over the next month as energy costs spill into other categories. Households will increasingly prioritize expenditures on gas and food, crowding out discretionary demand and slowing overall consumption. We now see real personal consumption expenditures rising 2.0% on average this year, softer than previously expected.

Income growth was already cooling before the energy shock. Real income excluding transfers has slowed over the past year as job growth moderates. Looking through labor strikes and volatile weather, private hiring found some sense of stabilization in the first quarter. But we still expect further softening ahead amid geopolitical uncertainty and AI‑driven efficiency gains, keeping downward pressure on wage growth ahead.

Policy trade-offs point to prolonged Fed patience. With inflation re‑accelerating and labor markets still gradually cooling, the Fed’s dual mandate is pulling in opposite directions. The Fed will exercise an abundance of patience as a result, and we have pushed out the start of easing but still expect 50 bps of total cuts this year, now penciled in as 25 bps moves at the September and December FOMC meetings.

…Monetary Policy & Interest Rates

We forecast two 25 bps rate cuts this year (Sep. and Dec.), followed by an extended hold at 3.00%-3.25%. Our 2026 year-end 10-year Treasury yield forecast remains unchanged at 4.25%.

While we still expect 50 bps of total cuts this year, we now expect easing will come later with 25 bps cuts at the September and December FOMC meetings. The labor market remains modestly on the wrong side of full employment and the energy price shock adds a new source of downside risk. Furthermore, monetary policy is already in restrictive territory when comparing the spot federal funds rate (~3.625%) to the SEP's median longer-run estimate (3.125%). Higher energy prices may bleed into core inflation, but this should be mitigated by slower inflation in tariff-sensitive goods. Taken together, we think the next move from the FOMC is still more likely to be a cut than a hike, even if the risks are skewed toward later and/or less easing.

Finally you say Yogi Berra says, and you’ve got MY attentions …

Apr 8, 2026 Yardeni: As Yogi Said: ‘It Ain’t Over Till It’s Over’ & ‘It’s Déjà Vu All Over Again’

The fog of war has been replaced by the fog of the ceasefire between the US and Iran. Negotiators for the two countries will meet in Islamabad on Friday. They met many times before without averting the war. The pounding of Iran by the US and Israel has failed to topple Iran’s regime, which still seems to have firm command and control of the country despite the decapitation of its leadership during the first day of the war. The Islamic Revolutionary Guard Corps remains intact, capable of firing missiles and drones, and has effectively taken over the Strait of Hormuz. The American negotiators will still insist that Iran abandon its nuclear program and surrender its stash of enriched uranium. But now they also need to get the Iranian regime to reopen the Strait as a free passageway for navigation in accordance with international law.

Given all the above, today’s latest relief rally in the stock market might have reflected more short covering than outright buying. Still, it was impressive to see the S&P 500 rebound back above both its 200-dma and 50-dma (chart). Moreover, during the 9.1% pullback since January 27, the 50-dma has remained above the 200-dma. We still think that the S&P 500 bottomed on Monday, March 30, at 6343.72. It is up 6.9% since then and down only 2.8% from its record high on January 27.

At the start of this year, we expected the stock market to be choppy in the first half, though we didn’t anticipate the war. It is likely to remain choppy until ships can sail freely through the Strait.

… Moving along TO a few other curated links from the intertubes. I HOPE you’ll find them as funTERtaining (dare I say useful) as I do … …

Terminal DOT COM OpED contained view of stocks vs bonds …

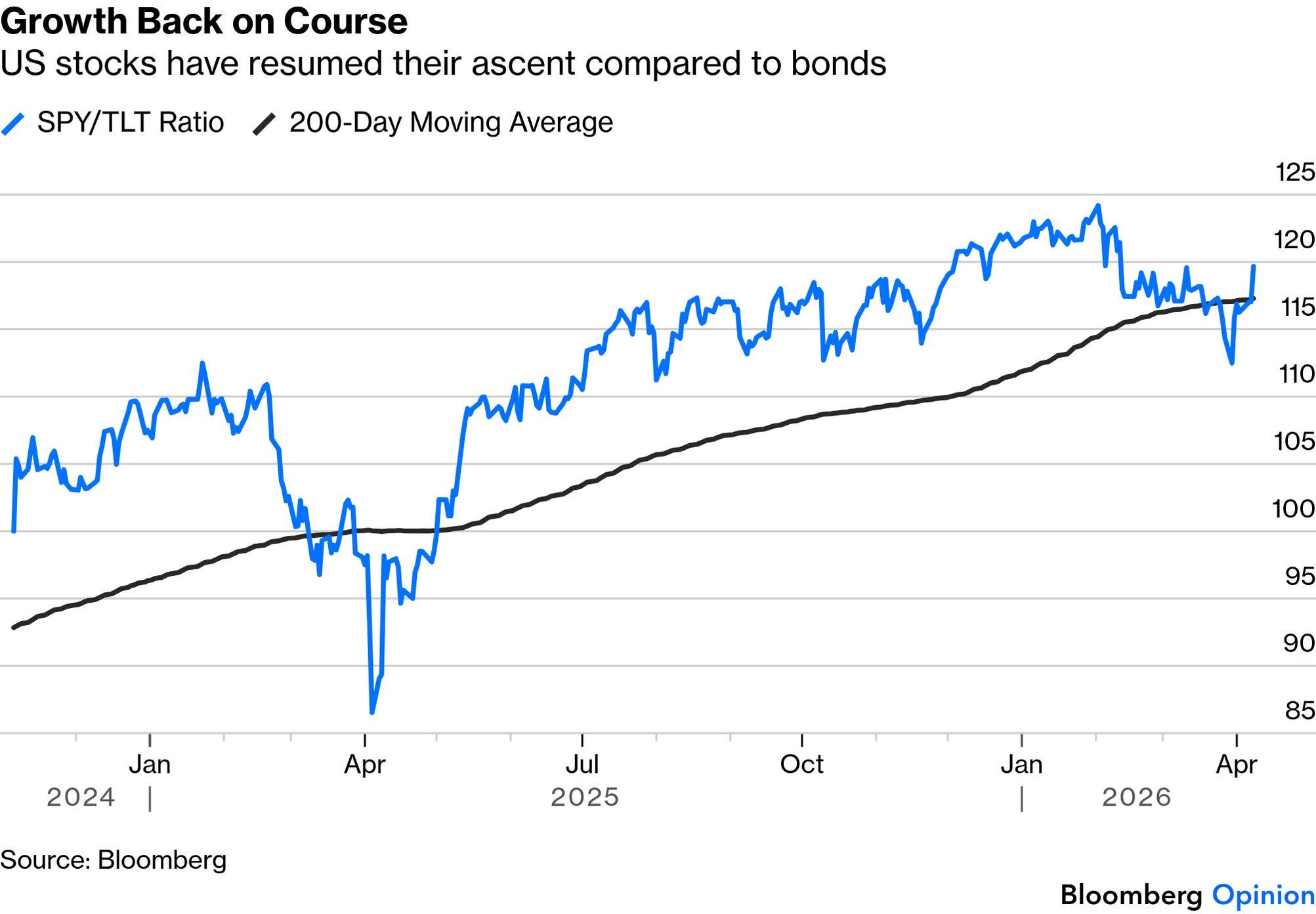

April 9, 2026 at 4:00 AM UTC Bloomberg: Hormuz doubts don’t stop a market celebration The idea that Iran could charge a toll on shipping would have been unthinkable a month ago.

…By implication, market hopes for growth are also back on course. The war caused a brief dip in the long-running upward trend for US stocks compared to bonds (proxied below by the most popular exchange-traded funds tracking the S&P 500 and long-dated Treasuries). That’s done:

But hopes for rate cuts from the Federal Reserve haven’t been instantly reinstated, because the impact of the ongoing disruption to the supply of oil and other basic materials is still unclear. The swaps market still expects inflation of more than 3% over the next year (it was below 2.25% at the start of 2026), and futures are priced for the Fed to take no action on rates this year — two cuts had been fully priced before hostilities broke out:

Put this together, and the Wednesday rally is a straightforward reaction to the big reduction in “left-tail risk,” meaning the worst possible outcomes are much less likely. But the rates market shows a belief that costs have increased, and will likely rise further as a result of the extremely murky compromise that has brought the ceasefire. That points to lower profit margins ahead…

From those who are theoretically IN THE KNOW …

April 8, 2026 Blackstone: Today’s Private Credit Isn’t the GFC

In 2008, banks were levered anywhere from 25 to 40 times, primarily funded by short-term deposits and heavily exposed to subprime housing.1 The underlying assets were 90%+ loan-to-value mortgages, layered with complex derivatives that obscured the risk.2

Simply put, this in no way resembles what is happening today.

In private credit, Business Development Companies (BDCs) typically borrow less than 1x their own capital.3 They use structures that don’t rely on deposits or overnight capital. And they lend to companies, not subprime homeowners, usually only around 40% of what the business is worth.4

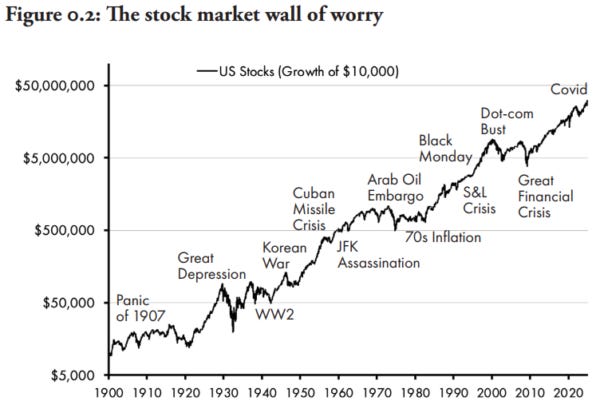

Wall-O-Worry … a GREAT chart and reminder to think … LONG - TERM …

Tue, 07 Apr 2026 05:01:42 +0000 DISCIPLINE FUNDS: Three Things – Let’s Make a Deal!

…2) Another Lesson in Geopolitical Investing?

I spend way too much time here discussing geopolitical events that seem to never end up mattering in the long-run. And yes, it’s a story as old as investing. One of my favorite charts in my new book was this chart of scary global events that have resulted in little to no long-term impact. Or rather, I should say, they had a meaningful short-term impact, but if you had the ability to look beyond them they had little impact on your long-term returns.

Naturally, this is my favorite thing about the Defined Duration strategy. In this approach assets are specifically aligned to time horizons that correspond to your financial needs. The stock market is best thought of as a 15+ year instrument that will earn 6-7% per year on average. But if you’re constantly getting worked up over 15 minute or 15 month moves in the stock market then it probably means you have an asset-liability mismatch in your portfolio.

This is one of the main benefits of asset-liability matching portfolios or what some institutional investors call Liability Driven Investing. When you match your short-term spending needs to short-term assets you don’t need to worry about what your long-term assets are doing. But there’s a component of real portfolio alpha in here as well. When you fund your portfolio exclusively and strategically from short-term instruments you are explicitly allowing the long-term assets to stay fully invested. This means they’re being allowed to generate the higher expected returns that we rely on them for. So there’s a double benefit in the ALM approaches – not only do you have a behavioral edge because you can see the actual liquidity in your portfolio, but you’re explicitly allowing the risky part of your portfolio to remain risky and oftentimes even pushing it riskier because you created so much near-term certainty in the portfolio that you actually feel comfortable taking more risk than you otherwise would…

In the long-term we’re all … just lookin for a #DipOrTunity …

April 08, 2026 LPL: Long-Term Opportunities Always Present Themselves

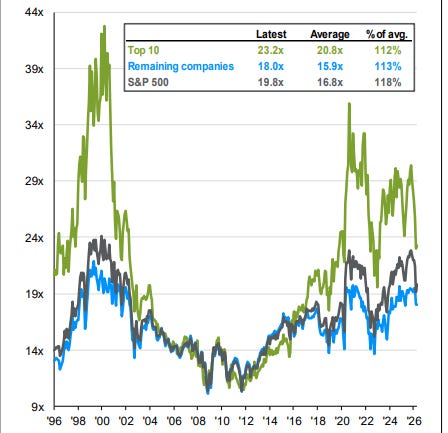

…Valuations Improving Under the Surface

The reason that the economic outlook is so important is because fundamentals drive markets over the long-term. But there are factors that investors should consider when making investment decisions today. The most important of which is valuations and earnings growth.

Following the April 2025 market bottom, stocks rallied strongly into 2026. This left everyone feeling better about their portfolios. But it does come with consequences. As stocks went up, valuations increased. The multiple that investors were willing to pay for forward earnings for the S&P 500 peaked at 22x.

Much like the rallies of the last few years being led by a handful of stocks, this year’s sell-off has seen similar action. The Magnificent Seven stocks (Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla) are down 10% as of Friday’s close, while the other 493 stocks are basically flat. As a result, valuations have improved.

S&P 500 Valuations Are Attractive

…Navigating the Short Term and the Long Term

While the situation in the Middle East remains fluid and until there is a resolution that opens the Strait of Hormuz that investors have confidence in, we would anticipate volatility to continue. For investors that can ignore the impact of short-term headlines, the equity market backdrop is improving.

Sell-offs will happen each year, and when they do, if there is no lasting impact on economic growth, valuations become more attractive. This time, we see improving fundamentals through rising earnings estimates. The first quarter 2026 earnings season begins in earnest next week. There is certainly the possibility that companies will take the opportunity to tamper down the enthusiasm that is being seen in analysts’ expectations. But everyone thought that would happen last year due to tariffs, and companies handily beat estimates throughout the year.

While near-term uncertainty is likely to persist, the combination of improving valuations and rising earnings expectations supports a constructive backdrop for the equity outlook. In our view, disciplined, diversified portfolios remain well positioned to navigate headwinds and participate in future market leadership.