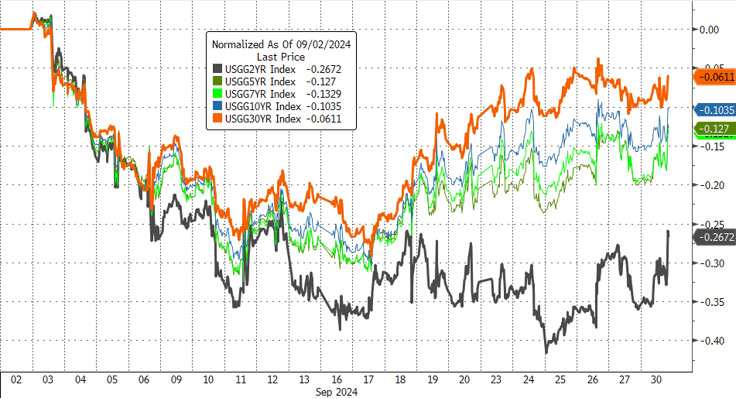

2yy DAILY: 3.659% or thereabouts appears to be important

momentum has corrected and NOT so overBOUGHT (but not extremely oversold) and is now holding …

… so front end of USTs reacting TO the Chair speech …

For release on delivery 1:55 p.m. EDT (12:55 p.m. CDT) September 30, 2024 Economic Outlook

… As I mentioned, our decision to reduce our policy rate by 50 basis points reflects our growing confidence that, with an appropriate recalibration of our policy stance, strength in the labor market can be maintained in a context of moderate economic growth and inflation moving sustainably down to 2 percent.

Looking forward, if the economy evolves broadly as expected, policy will move over time toward a more neutral stance. But we are not on any preset course. The risks are two-sided, and we will continue to make our decisions meeting by meeting. As we consider additional policy adjustments, we will carefully assess incoming data, the evolving outlook, and the balance of risks. Overall, the economy is in solid shape; we intend to use our tools to keep it there…

… in other words do NOT price in another 50bps cut and so, 2s were / are romancing levels of ‘support’ as the day, month and quarter came to a close as the week just getting going … a quick pause for visual / snarky review …

ZH: Powell Pours Cold Water On Rate-Cut Euphoria; USA Sovereign Risk Ominously Surges In September

US Macro data is on a charge higher in September, surging to its strongest since late-April...

Source: Bloomberg

…Stocks and bonds took a hit today around 1400ET when Powell said that he "doesn't feel like The Fed is in a hurry to cut quickly."

Additionally, Powell said "sometimes people pay too much attention to The Fed's SEP [Dot Plot]," noting that the SEP shows two more 25bps cuts this year (less than the market).

That sent rate-cut expectations lower (hawkishly), with less than 3 cuts now priced in for 2024...

…While all stock indices were higher, so Treasury yields were lower across the board in September (with the short-end outperforming significantly) despite a decent surge higher in rates today (2Y +10bps)...

Source: Bloomberg

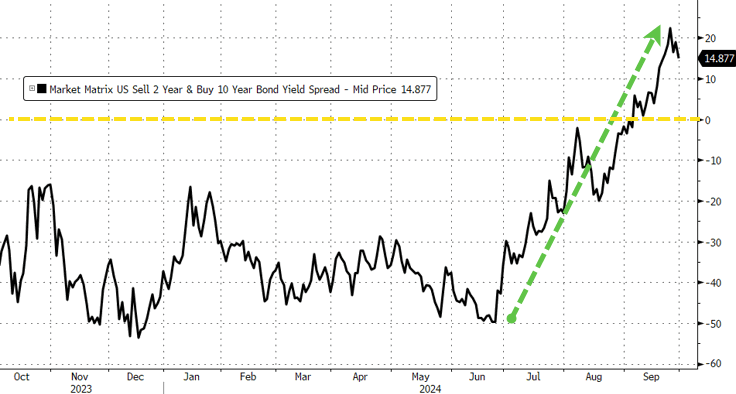

The yield curve steepened dramatically in September with 2s10s dis-inverting notably (before flattening a little in the last few days)...

Source: Bloomberg

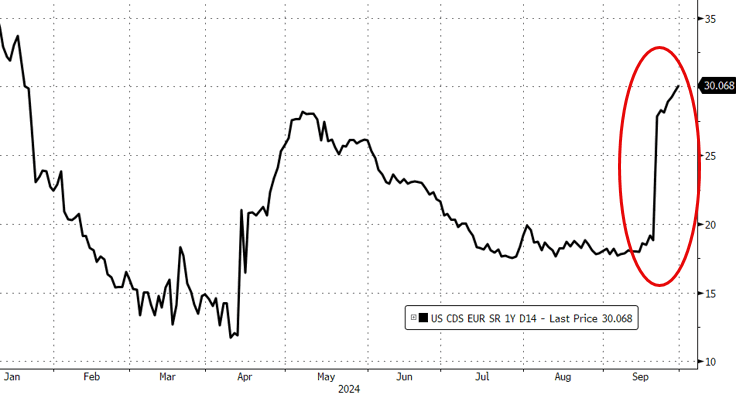

… What will The Fed do about soaring gold and crypto and USA sovereign risk spiking like Zimbabwe...

Source: Bloomberg

Has anyone else noticed this? Is this why The Fed cut rates?

… Meanwhile, morning markets are as IF nothing happened and ports are shut down am hearing local Costco already out of … ‘important paper goods’ again.

Great.

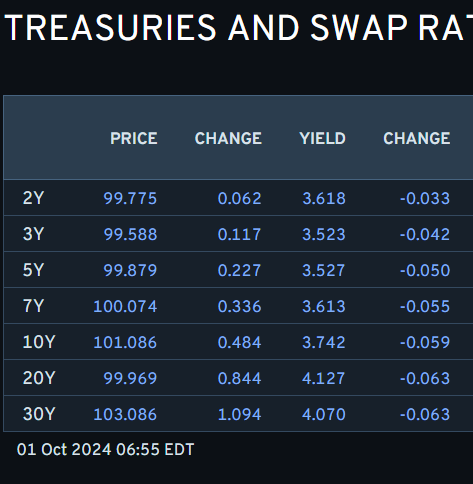

Here we go again … can only HOPE (not a strategy) this resolved quickly and while we collectively wait, here is a snapshot OF USTs as of 655a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Equities mixed ahead of US data and comments from Fed officials … USTs are firmer and back to pre-Powell levels, Bunds also gain but were unmoved by the EZ PMIs which were revised modestly higher but the overall growth narrative remains weak … USTs are firmer and back to pre-Powell levels after the marked bear-flattening the Chair induced on Monday evening. USTs to a 114-21 peak, approaching Monday’s best which itself is a tick below Friday’s 114-25 peak. Docket ahead is headlined by Final Manufacturing and then, more pertinently, the ISM Manufacturing PMI before remarks from Barkin, Bostic & Cook.

Reuters Morning Bid: Stocks kick off Q4 at record, euro inflation undershoots

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Love when others chime in on US politics … everyone’s got an opinion. My dad used to say // remind me daily // opinions are like YOU KNOW WHAT - holes … everybody’s got one …

ABNAmro: US Elections - The Fed will be alright, but… | Insights newsletter

Any attempt to reduce the Federal Reserve’s independence is unlikely to get very far. The judicial branch has already been greatly politicized, paving the way to do the same to the executive branch. A weakening of the separation of powers may further concentrate power and capital, harming societal welfare.

…The Fed’s independent functioning and its ability to set appropriate policy seems relatively well protected, making it unlikely that a president could exert strong control over monetary policy. The risk to the independent functioning of the judicial and executive branch is far larger, as the judicial system’s independence is already eroding, paving the way for changes to the executive branch.

#Got5s? French bank making a call … kinda … in a way and a couple visuals which make me stop and think …

BNP: Quant trades of the week: Receive US 5y, long EURCHF and pro-risk via real estate

KEY MESSAGES Market themes

Our risk sentiment and equity positioning metrics suggest scope for risk assets to continue to perform over the week ahead..

MarFA™ is signalling overshoot in many assets after pro-growth events in the past two weeks (Fed rate cut and stimulus in China). Many mispricings align with this new information and we consider should not be faded.

For this reason, we screened mispricings by testing for co-integration and momentum. Among those, we favour long US real estate, receive US 5y yields and long EURCHF.

…US duration: Improving data and CTA positioning Improving data driving yields higher: Improving US activity data has started to surprise to the upside, on average, putting some sustained pressure on US rates. This week, we expect payrolls to continue the trend with a 150k reading (versus a consensus at 140k). As expectations adjust higher, of course, we could start to see renewed data misses.

CTAs remain long duration with moderate leverage: Over the week our CTA model estimates some reduction in CTA positioning in back-dated US rates. Overall positioning remains long with scope for trend signals to increase (if rates rally further), while leverage remains light-moderate.

Trade ideas: US rates Initiating USD 5y receiver: US rates have continued to come under pressure in the past week. MarFA™ Macro now sees US SOFR 10y, 20y and 30y swaps as around 16-17bp (2.7-3.0 z-scores)too high versus fair values.

US 10y Treasuries look 14bp (2.4 z-scores) too high, with yields generally supported by rising inflation/growth expectations. US 10y breakevens (BE) look 10bp (2.2 zscores) high and USD 5y5y inflation swaps are around 7bp too high, according to the model…

… on TO everyone’s favorite stratEgerists from Germany where on offer are a quick review of fund pricing to JPOW and a monthly recap …

… Powell’s remarks led to some doubts over whether the aggressive pace of the easing cycle priced by markets would materialise. While maintaining data-dependence, he emphasised that the economy remains solid, noting that “this is not a committee that feels like it’s in a hurry to cut rates quickly”. He also reiterated the rates signal from the most recent SEP, saying that “if the economy performs as expected that would mean two more cuts this year, for a total of 50bps more”. So some conditional pushback relative to market expectations that had moved to fully price 75bps of further cuts by year-end.

In response, Fed funds futures tempered the rate cut expectations, with the amount of easing priced by December falling to 70bps, down from 77bps at the start of the day and 73bps before Powell spoke. Off the back of this, Treasury yields extended what had been a modest increase earlier in the day, with 2yr Treasury yields closing +8.2bps higher on the day at 3.64%, while 10yr yields were up +3.0bps to 3.78% …

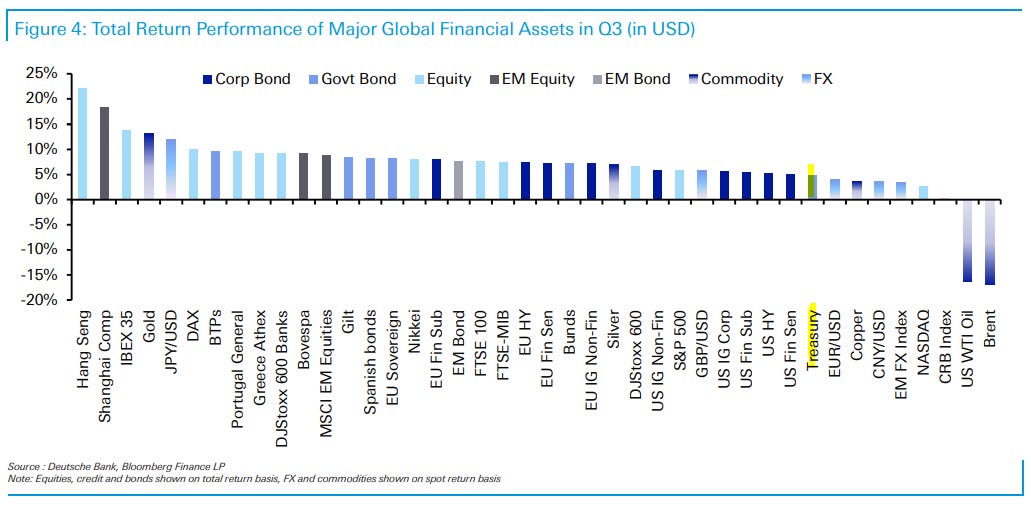

Markets put in a strong performance over Q3, with global equities and bonds both advancing. But the headline numbers masked some massive turmoil in the middle of the quarter, as fears of a US recession, the unwinding of the yen carry trade and questions about tech valuations all led to a sizeable risk-off move. At one point, the VIX index of volatility even hit its highest intraday level since March 2020, at the height of the initial wave of the pandemic. But this turmoil proved remarkably brief, and a dovish pivot from central banks (including a 50bp rate cut from the Fed), along with stronger US data and fresh China stimulus led to a significant recovery. In fact by the end of Q3, the S&P 500 had posted its strongest YTD performance of the 21st century so far…

…Which assets saw the biggest gains in Q3? … Sovereign Bonds: With investors pricing in more rapid rate cuts, it was a strong quarter for sovereign bonds. US Treasuries (+4.9%) and Euro sovereigns (+4.1%) both advanced. For US Treasuries, September also saw them advance for a 5th consecutive month for the first time since 2010…

… how do you like yer eggs? why, just like I like the chair of the Fed, thank you very much …

… Elsewhere, investors have to pay attention to the utterances of Federal Reserve Chair Powell. Powell indicated yesterday that there would be two quarter-point rate cuts over the remainder of the year. The Fed had to scramble to catch up with inflation with its half-point rate cut, in a somewhat undignified manner. It still has to scramble (despite protestations it was late to cut rates), but can now scramble with a little more dignity …

… And from Global Wall Street inbox TO the WWW,

… Q3, September and, well, 2023 so far in a single tweet / visual …

at bespokeinvest

This is the strongest YTD gain through three quarters (+20.8%) for the S&P 500 since 1997.

The unwinding of leveraged positions, including carry trades, amplified short-lived bouts of extreme equity market volatility and exchange rate movements in early August.

Equity markets underwent some drawdowns but overall managed to pull ahead fairly unscathed. Credit markets were even less affected, amid an overall environment of loose financing conditions.

Markets remained hypersensitive to macro news, especially news that lowered the odds of a soft landing. Bond yields declined on any signs of slowdown, particularly at the short end.

…Global bond markets price in easier monetary policy

Global bond markets moved in tune with expectations of an easier policy stance. Inflation continued its course towards targets, while macroeconomic readings indicated that growth momentum might be faltering. Hence, fixed income markets started pricing in earlier and larger rate cuts in most advanced economies, causing a rather synchronised decline in short-term yields globally (Graph 1.A). This macro backdrop also exerted downward pressure on long-term yields, albeit a more moderate one (Graph 1.B). As a result, the negative term spreads in advanced economies continued to narrow, even turning positive in some economies (Graph 1.C)….

… we all knew it and now the NY Fed writes ‘bout it …

Expectations can play a significant role in driving economic outcomes, with central banks factoring market sentiment into policy decisions and market participants forming their own assumptions about monetary policy. But how well do central banks understand the expectations of market participants—and vice versa? Our model, developed in a recent paper, features a dynamic game between (i) a monetary authority that cannot commit to an inflation target and (ii) a set of market participants that understand the incentives created by that credibility problem. In this post, we describe the game, a type of Keynesian beauty contest: its main novelty is that each side attempts, with varying degrees of accuracy, to forecast the other’s beliefs, resulting in new findings regarding the levels and trajectories of inflation…

… In summary, in economies where central banks lack commitment mechanisms for policy objectives, beauty contests between monetary authorities and markets exacerbate the credibility problems at play. Improving the accuracy of data about market expectations likely mitigates this problem, but monetary authorities can still appear to be less committed to low inflation at some points in time.