FitchRatings: Fitch Downgrades the United States' Long-Term Ratings to 'AA+' from 'AAA'; Outlook Stable Tue 01 Aug, 2023 - 5:13 PM ET

Fitch Ratings - London - 01 Aug 2023: FitchRatings has downgraded the United States of America's Long-Term Foreign-Currency Issuer Default Rating (IDR) to 'AA+' from 'AAA'. The Rating Watch Negative was removed and a Stable Outlook assigned. The Country Ceiling has been affirmed at 'AAA'.

… and on THAT note, my comments which followed the very next morning led with …

Good morning … 2011 called and it wants it headlines back?

… AND we’re back. Before I jump in to any FOMC recapAthon followed by Global Walls victory lapAthon, I’d like to take a quick look at 2yy and see what, if any message migth be derived from the day that just was …

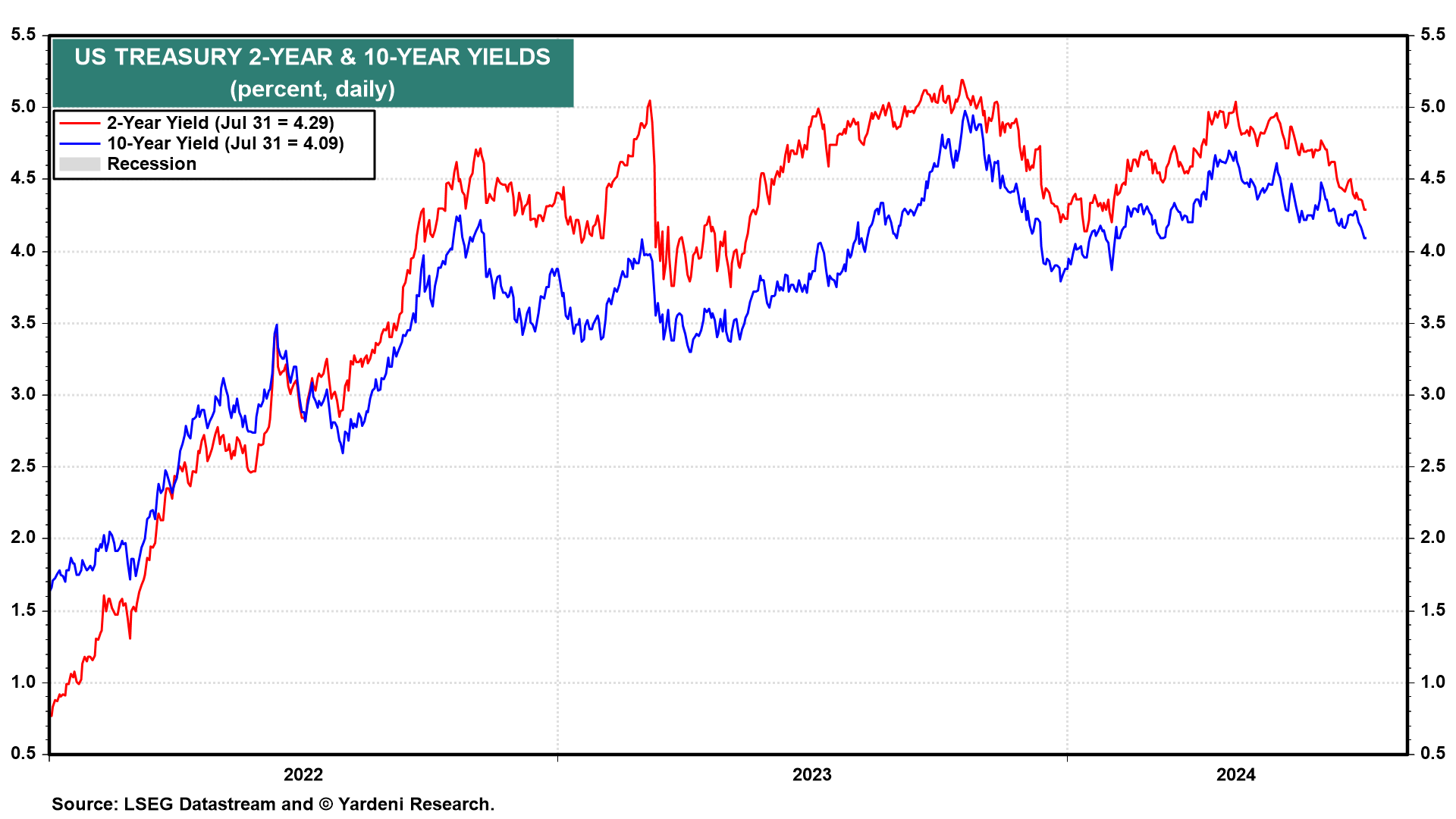

2yy DAILY: 4.15% (2024 lows) next?? H1 UPtrend (now removed from charts) morphed into a clear and current downtrend in yields … a rolling over, if you will …

… despite momentum (overBOUGHT), there’s still plenty of magnetism and Fed HOPE / pricing which is pulling yields down, curve steeper …

2yy MONTHLY: headed back down BELOW 2.50%? (log chart like Tavi Costa’s HERE suggesting 2.00%?? a stretch, maybe but…)

… an interesting setup, for sure …

… NOW, this price action was one part data, another part issuance / supply, another large part GEOPOLITICS (NYT here) and finally, a last part FOMC related.

Here, then, are a couple / few links to consider as equity markets held in remarkably well given the absolute clarity offered from the Fed — the likes of which I NEVER saw in my 25+yrs in a FI sales / trading / strategy seat …

SOME thought Fed shoulda coulda woulda CUT yesterday and are absolutely shocked they did NOT. Others, well, are willing to embrace whatever factoids come patiently wait for cuts / hikes (?) to be dictated by further turn of the data.

See whatever you wanna see and I’m on board with data shape-shifting and leaning to the worse (and so, towards a cut(s)) but at the very same time, willing to acknowledge how positive the data still IS, and JPOW acknowledged it as such, several times.

… The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent …

… on the one hand, yes, purposely VAGUE but on another hand, specifically saying NO WAY not cutting rates here / now …

WSJ: Fed Statement Tracker (neat interactive link IF you are bored…)

Hmmm … Gotta continue with a data, issuance and FOMC recap …

ZH: ADP Employment Report Weakest Since January As Wage-Inflation Slows

ZH: Quarterly Refunding: Treasury To Hold Bond, Note Sales Steady For "Several Quarters", Will "Modestly Increase" Bill Offering Size

ZH: Hawkish FOMC 'Still Waiting For Greater Confidence' On Disinflation

ZH: "The Fed Did Not Tip A September Cut, By Any Stretch": Wall Street Reacts To The FOMC Statement

… and I missed this but apparently the bond king, Gundlach clearly a member of Team Rate CUT …

NEWSQUAWK: US Market Open: Gilts lift and GBP lags ahead of a potential BoE cut; earnings in focus … Gilts lead fixed income pre-BoE, EGBs unaffected by Final PMIs and downbeat commentary from HCOB on Germany … USTs firmer, and towards the top-end of 112-02+ to 112-10+ parameters, a peak which matches Wednesday’s post-Powell high.

Reuters Morning Bid: Fed nods to cut, chips rebound, BoE up next (VISUAL of FF futures pricing BELOW 4% in 12m vs curr rate of 5.33%)

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Powell: “‘Certainty’ is not a word that we have in our business.” But a September cut is likely. As expected, the Fed voted unanimously to keep monetary policy on hold. While the policy statement remained relatively balanced, Powell's replies in the press conference were decidedly more doveish, clearly preparing the ground for a 25bp September cut, while leaving room to further delay the easing cycle if inflation proves more sticky.

BARCAP: June ECI moderation a welcome sign for FOMC

The Employment Cost Index for civilian workers moderated to 0.9% 3m in June after a short-lived spurt to 1.2% during Q1. The private sector index followed suit. This should bolster confidence that wage growth is on track eventually to settle in a range consistent with a sustained return to the the FOMC's 2% target.

As we had expected, communication out of the FOMC meeting hinted at growing confidence that conditions may be in place to cut rates in September, but left the forward guidance unchanged. Chair Powell remained noncommittal to a September decision, even if a September cut is a likely baseline.

… We retain our baseline projection that the FOMC will cuts rates twice this year, at the September and December meetings. Our baseline is predicated on inflation remaining moderate (core at 0.2% m/m) in July and August and the economy gradually slowing. However, if inflation is stronger than in our baseline, we think the first rate cut could be postponed to December. For 2025, we expect the FOMC to cut rates three times, in March, June, and September, with upside risks to rates if inflation does not continue to move toward 2%.

BMO: ADP 122k, 10-year Yields Push to 4.118% (lowest since March 12th)

… . Overall, it was a bond friendly update on the jobs market and while the correlation between ADP and private-NFP isn't the most compelling, the release offers hints of more 'balance' on the labor front.

… Before 8:30am ET, Treasuries were rallying in the wake of ADP, and since the Refunding Announcement, the bid has been retained and we've seen 10-year rates touch as low as 4.11%. From here, investors will see the Chicago PMI and Pending Home Sales later this morning before the FOMC Statement and Powell’s press conference this afternoon.

From here, the market will be focused on any hints from Powell at the press conference although the relatively narrow range being held in rates suggest the market is taking the update as a nonevent. The front-end of the market has cheapened slightly on the release of the FOMC statement -- simply pricing out the slight risk of a cut. That being said, 10-year yields dipped as low as 4.089% earlier in the session. We continue to anticipate yields will be lower ahead of payrolls.

BMO: FOMC: Inflation "somewhat elevated" and "dual mandate" emphasized

… " On net, there were no major surprises and the messaging is very consistent with expectations for the first cut to be at the September 18th meeting…

BNP: US rates: Treasury stalls the inevitable while T-bills take the stage

Treasury announced another (widely anticipated) pause to coupon and FRN auction sizes with a gradual rise for TIPS. We do not rule out further increases in coupons over the medium-term.

Our funding estimates suggest Treasury will continue to rely heavily on T-bill issuance to meet near-term deficit needs.

Treasury kicked off cash management buyback operations heading into September tax season while boosting the maximum purchase size of its liquidity buyback operations.

We think Chair Powell’s press conference gave a clear sign that a rate cut will be on the table in September, with the tone more dovish than the statement.

While not yet worried, the Fed is signaling greater concern about the labor market, with the statement enshrining attentiveness to risks to “both sides” of the dual mandate.

In our view, the FOMC is close to gaining sufficient confidence on the inflation front and will likely reach that point by September based on our forecasts.

We expect 25bp rate cuts in both September and December, and 100bp of cuts (at a quarterly pace) in 2025. Signs of a deterioration in the job market (not our base case) would warrant a steeper rate cut trajectory, in our view.

… We update our bill supply forecast to incorporate Treasury’s latest borrowing estimates. We now see net bill issuance for the year at $385bn, or about $120bn lower than our forecast in June. Our projections for rest of this year are: $130bn for September, -$97bn for October, and $90bn for Q4.

The July FOMC meeting was close to expectations. The statement and Chair Powell's press conference showed an increased focus on the employment side of the Fed's dual mandate as the labor market has cooled and the Committee gains confidence that inflation is moving sustainably back to 2%.

Powell signaled that a September rate cut is a reasonable base case without pre-committing to that outcome. He noted that officials started to discuss rate cuts at today's meeting and indicated that a continuation of recent data trends would be consistent with a reduction being "on the table at the September meeting."

As we expected, Powell provided limited information about what the cutting cycle could look like beyond the first reduction. That said, he did open up the possibility of cutting rates at consecutive meetings by acknowledging scenarios with "several" cuts this year. At the same time, he noted that a 50bp reduction is not being considered by the Committee.

We continue to see the first 25bp cut in September followed by two more reductions in November and December (see "Keeping the expansion alive with 75(bps) before '25"). Assuming incoming data support a reduction at the next meeting, we anticipate that Jackson Hole could provide signals about how the Committee is thinking about the broader cutting cycle.

… In terms of the market reaction, rates initially saw a slight sell off as the FOMC statement kept existing rates guidance unchanged, but this reversed sharply during and after Powell’s press conference. By the close, markets were pricing 29bps of cuts by the September meeting, so a non-negligible chance of a 50bps cut, and 72.5bps of cuts by year-end (+3.3bps on the day). This repricing was matched by a rally in Treasuries, with 2yr yields down -10.2bps on the day to 4.26%. Further out the curve, 5yr yields closed below 4% for the first time since early February (-12.0bps to 3.91%), while 10yr yields were -10.8bps lower at 4.03%. Most of the rally came after Powell started his press conference, though longer-dated yields were already slightly down pre-FOMC after encouraging details from the Treasury’s QRA announcement. See our rates strategists’ take on the latter here.

The FOMC meeting supported what had been an already very strong day for equities. Both the S&P 500 (+1.58%), as well as the NASDAQ (+2.64%) and the Mag-7 (+3.51%) posted their best days since February amid a rebound for tech stocks. This was led by a +12.81% jump for Nvidia. That equated to a $327bn rise in the company’s value, eclipsing the previous record for a daily market cap increase ($277bn) that Nvidia set back in February. Still, the equity advance was fairly broad, with 6 of the 10 high level sectors within the S&P 500 rising by more than 1%. The Russell 2000 (+0.51%) underperformed despite trading as much as +2.5% intra-day as Powell spoke, but that still left the small cap index up +10.10% for July as a whole.

The more positive tech sentiment continued with Meta’s results after the US close…

… July got off to a strong start for markets, with a cross-asset rally over the first half of the month. That meant that the S&P 500 advanced in 10 of the first 11 sessions, closing at an all-time high on July 16. Similarly, the 10yr Treasury yield fell from 4.40% at the end of June, to 4.16% by July 16…

…What really turbocharged those expectations for rate cuts was the latest US CPI report on July 11. That showed the weakest monthly core CPI since January 2021. In addition, it followed a series of better inflation reports, meaning that the 3-month annualised rate of core CPI fell to just +2.1%, the lowest since March 2021. That led investors to significantly dial up their expectations for rate cuts this year, and the amount of cuts priced in by the Fed’s December meeting was up +28.4bps over the month to 72.5bps. By the end of the month, futures were fully pricing in a cut by the September meeting, and Fed Chair Powell said at the July FOMC press conference that “a reduction in our policy rate could be on the table as soon as the next meeting in September.”

… Which assets saw the biggest gains in July? Sovereign Bonds: With rate cuts moving into view, it was a very strong month for sovereign bonds. Both US Treasuries (+2.2%) and Euro Sovereigns (+2.4%) had their strongest month of 2024 so far…

…Which assets saw the biggest losses in July? Magnificent 7: It was a tough month for the Magnificent 7, with the group down by -0.6% in July, marking a sharp reversal after gaining +37.0% in the first six months of the year…

The FOMC statement showed an important change in the characterization of inflation and the labor market, emphasizing risks to the dual mandate. In line with our expectations, they have shifted their language from "highly attentive to inflation risks" to "attentive to the risks to both sides of the dual mandate." The statement acknowledged further progress on inflation – adding inflation is "somewhat elevated." They also highlight job gains have "moderated" and the "unemployment rate has moved up". Emphasis on the cooling labor market was an important shift to a more balance tone that we think sets the Fed up to cut in September. They emphasized that the Committee is now attentive to "both sides of its dual mandate"…

Powell states the Fed feels close to cutting. Inflation data is adding to his confidence, while risks to the labor market are becoming more real. Our inflation forecasts point to a September cut, three in total this year. Our rates team keeps UST 2s20s steepeners, enters Sep/Nov FOMC OIS flatteners.

Key Takeaways

Rates decision: The FOMC held the policy rate unchanged in a range of 5.25-5.50%, where it has remained since July 2023. Substantial progress in inflation was highlighted, with greater focus on risks to both sides of their mandate in the statement and presser. Powell stated the FOMC feels close to cutting and there was a real debate about cutting at this meeting.

Outlook: We continue to see three cuts this year, starting in September, informed by our core PCE forecasts that reach a three-month annualized pace of 2.1% ahead of the meeting. Inflation continues to move convincingly lower, and the Fed cuts every meeting through mid-2025.

Rates: Our rates strategists see Powell's suggestion that "there was a real discussion back and forth of what the case would be for moving at this meeting" as supporting a continued steepening of the yield curve in an increasingly bullish way. They enter pay fixed September FOMC OIS vs. receive fixed November FOMC OIS.

FX: Our FX strategists expect USD to soften against JPY as additional Fed cuts are priced. They close their long AUD/NZD trade recommendation as NZD appears more likely to benefit from lower front-end US yields than AUD.

MBS: Our MBS strategists increase conviction in long basis near YTD tights and shift G2/FN longs into 5.0s and 5.5s.

Munis: Confidence in cuts should encourage a curve rotation into longer maturity SMA strategies, and to a lesser extent, mutual funds. Tax-free money market yields could stay sideways to higher.

US Treasury announced planned auction sizes, in line with our expectations for nominal coupons, FRNs, and TIPS. Guidance indicates current coupon sizes will be maintained for "at least the next several quarters," leaving realized deficits the primary determinant of bill supply.

Key takeaways

The Treasury refunding meeting delivered no change to nominal coupon and FRN auction sizes, with incremental increases to TIPS, in line with our expectations.

In our view, key was the guidance that nominal coupon and FRN sizes are still not expected to be increased for "at least the next several quarters."

Liquidity support buybacks were scaled to their maximum, likely incorporating dealer feedback, while the first cash management buyback is set for September.

Further study by TBAC on the optimal bill share reveals a view that the lower bound is more important than the upper bound.

We continue to believe further clarity on deficit trends, and thus issuance needs, will come after the outcome of the November US presidential election.

RBC: U.S. Fed puts September rate cut on the table

… Bottom Line: Data releases over the summer suggested that the U.S. economy is broadly on track for a soft landing, in line with the Fed’s expectations. GDP growth remained somewhat resilient over the first half of the year, labour markets have normalized but are still strong, and inflation has come lower. Risks for a faster/larger deterioration in labour market have gained some weight remain well balanced against risks of higher inflation. Looking forward, focus will be on the next two CPI and employment releases before September, where we expect improvements will continue. We think that will prompt a first rate cut from the Fed at its next meeting, alongside the release of the dot plot that should offer more clues on the path of interest rates beyond.

Strategas: WHAT’S THE CHEAPEST PART OF THE TREASURY CURVE?

The market is moving long Treasuries (see Strategas positioning reports), while auction demand has been stable to improving (see Strategas auction reports). Collectively, this is helping Treasuries to build on a slow-moving rally that began in late April.

The rally should gather some support tomorrow and again on Friday. On Wednesday, the Fed seems set to make another incremental move towards a September cut, while Treasury looks likely to hold coupon auctions steady until the end of 2024. Meanwhile, the July jobs report is due to come out on Friday, with expectations that labor demand weakened slightly to start Q3.

With this as a backdrop, the market is pricing in almost 70 bps of rate cuts for 2024, and almost 100 bps of cuts before the end of Q1 2025. This has helped the curve to bull steepen, and has richened the 2 to 7 year part of the curve disproportionately vs the wings.

This results in a curve that is mostly rich between 2s and 7s. In contrast, we find the cheapest point to now be the 20 year bucket, with 1s and 10s also cheap vs our model.

… The Federal Reserve has been late to cut rates, and it is delaying things even more. Despite disinflation forces, and strong deflation in some sectors, there was no rate cut yesterday. Fed Chair Powell did signal a September rate cut, but that is of limited comfort to lower income households struggling to service their debt burdens.

US unit labor cost and productivity data are due. These numbers matter in theory, but are not much use in real time. There have been productivity gains from increased investment and flexible working (which are evident at a corporate level). However, economic productivity is derived from GDP, and if GDP is under-reporting activity (as it probably is) it will tend to under-report productivity…

The Employment Cost Index rose 0.9% over the second quarter, which was a touch softer than consensus expectations. Moreover, having increased at an annualized rate of 3.7% in the three months ending in June, the second quarter's figures show employment cost growth closely approaching a pace consistent with the FOMC's 2% inflation objective once accounting for productivity growth.

Summary As was widely anticipated, the FOMC left the fed funds rate unchanged at the conclusion of today's meeting, but it opened the door to potentially easing policy at its next meeting on September 18. While inflation remains above the FOMC's 2% target, it has fallen significantly since the Committee last raised rates a year ago. At the same time, the labor market has cooled sufficiently and now resembles its pre-pandemic state. In its post-meeting statement, the FOMC noted the improving balance between its employment and inflation goals and emphasized it is growing more mindful of the risks to the labor market by noting it is "attentive to the risks to both sides of its dual mandate", rather than previously only noting its attention to inflation risks.

We suspect today's decision, post-meeting statement and Powell's press conference statements reflect a compromise among the Committee members. While some more dovish members were likely inclined to reduce the policy rate at today's meeting, more hawkish members are likely wanting to see more data. To thread the needle, we think Chair Powell arrived at a compromise: hold rates steady at this meeting, but send overt signals to the market and broader public that the base case is for rate cuts starting soon. We look for the FOMC to cut the fed funds rate by 25 bps at its next meeting, with a further 25 bps cut in December and an additional 100 bps of easing in 2025

Yardeni: Powell Says Economy Is Normalizing & September Rate Cut Is On The Table

… The 2-year and 10-year US Treasury yields slid by about 6 basis points during Powell's press conference today, with the 10-year ending the day around a 4-month low (chart). The bond market was also comforted by the Treasury Department's quarterly refunding announcement; the fiscal agent said it wouldn't be increasing the size of bond auctions for the foreseeable future. Tax revenues from the growing economy continue to boost the government's coffers.

The stock market liked what it heard from Powell, as well as the recent batch of Q2 earnings reports. The Roundhill Magnificent-Seven ETF (MAGS) rose 3.4% …

… And from Global Wall Street inbox TO the WWW,

AllStarCharts: Here’s What’s Actually Driving Things (USTs and JPYUSD…)

… Bitcoin is at $1.3 Trillion and total Crypto market cap is just under $2.4 Trillion.

Again, this is compared to the $130 Trillion bond market. Not to mention the quadrillions that represent the forex markets.

The bond market moves all the other markets. It starts here.

And so it’s been hard to ignore the relative strength we’ve seen in the US Treasury Bond market compared with the Japanese Yen.

As they’ve both recovered some, the strength has been within the US Bond Market all along:

So why should we care?

Why does this matter?

Higher Bonds+ Higher Japanese Yen = Lower Interest Rates + Higher Stock Prices

Think about all these rate sensitive groups like Regional Banks and Biotechs.

You notice how well they’ve been doing lately?

The market is good about sniffing this stuff out.

There’s a lot of implications from this Chart above. I just had to show it to you.

It’s the centerpiece of our upcoming discussion this Thursday night.

August 1st is the first chance we get at reviewing all the monthly candlesticks together.

Apollo: Slower Global Growth Putting Downward Pressure on Commodity Prices (lower commods = lower ‘flation and so = Team Rate CUTS)

China is slowing, Europe is slowing, and the US economy is also in the process of slowing down over the coming quarters.

As a result, commodity prices are falling.

Prices for energy, which make up almost 60% of the S&P GSCI, are declining because of weaker demand from China and more energy supply in the US.

Agriculture prices are falling, in particular soybean, driven lower by weaker global growth. But there are exceptions such as coffee, cocoa, livestock, and orange juice, where low supply is important.

Industrial metals prices are falling because of weaker global growth. For precious metals, gold prices are rising as households in China diversify away from falling Chinese property prices and falling Chinese stock prices. Central banks are also buying gold.

Our latest commodity outlook chart book is available here.

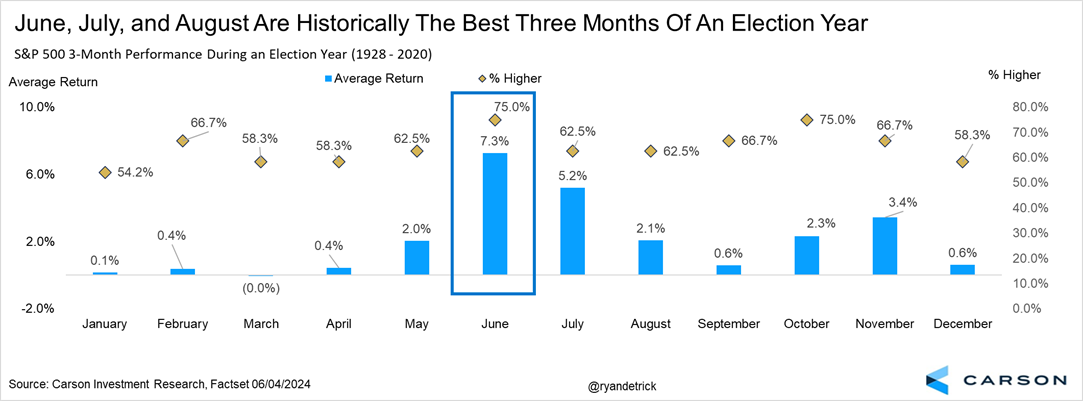

Carson: Beware of August? Maybe Not in an Election Year

…Let’s get right to the point, August historically isn’t a very good month for stocks. Most people know this and it is factually true, as stocks are down on average during this month since 1950 and the past 10 years, something only February and September can also say. But here’s the catch, and there’s always a catch, stocks have historically done quite well in election years in August.

Here’s a chart we’ve shared a lot lately and it was one reason we expected a surprise summer rally when so many were telling us about yield curves and LEIs as reasons to be bearish. The bottom line is June, July, and August are historically the best three months for investors in an election year and this year has again rewarded them so far.

… We do expect that the Fed will cut rates twice later this year, once in September and again in December, but we see these cuts accompanied by a slowing economy, higher unemployment, and modest progress on inflation. The morphine is wearing off and the aftereffects of money printing, excessive and misguided spending from Washington, and companies getting a bit over their skis in terms of hiring are starting to show.

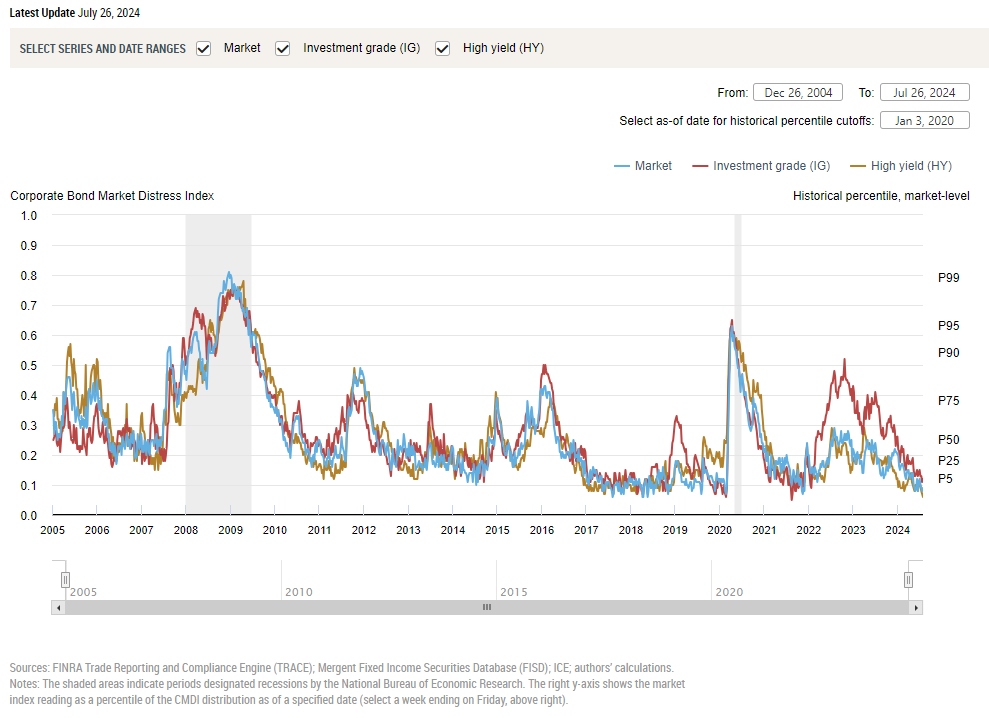

FRBNY: Corporate Bond Market Distress Index (CMDI)

ING: Federal Reserve: Setting the scene for a September cut

The Fed kept monetary policy unchanged, but offered enough for the market to keep faith with the 18 September FOMC meeting rate-cut call. Inflation is looking better behaved, the jobs market is softening and consumer spending is cooling, and with the policy rate well above neutral we look for 75bp of cuts this year with the potential for more in 2025

at JessicaMenton (of BBG with a snazzy jazzy chart of stonks on FED DAY)

Buy signals flashed across Wall Street as traders grew optimistic about rate cuts coming soon after Fed Chair Powell left the door open to lowering borrowing costs in September. $SPX jumped 1.6% — its best Fed Day session since July 2022

The FOMC is getting ready to begin easing policy, but whether they start already in September will depend on the incoming data. In particular, we need to see two more benign inflation prints.

at Optiongirl

Notice the decline today in 10 year yields has broken the uptrend from April 2023 (blue line).

{kind=link}