Asia kicks off the trading week on Monday with investors likely to give a big thumbs down to yet another batch of uniformly disappointing economic indicators from China, while at the same time cheering one of Wall Street's best weeks of the year.

Fueled by growing hopes that the Federal Reserve will kick off its interest rate-cutting cycle with a 50-basis-point cut rather than a quarter-point move later this week, U.S. stocks rose solidly on Friday, which could provide a good springboard for Asia on Monday.

The S&P 500 got to within 1% of its July 15 all-time high and the Nasdaq ended the week up 6%, its best week since October. Volatility across asset classes fell - the 'MOVE' index of implied Treasury market volatility is at its lowest since late July.

That's the backdrop to the start of a hugely important week for markets around the world with the highlight being the Fed's rate decision and revised economic forecasts on Wednesday, but maybe even more so for Asian markets…

…There are those in the more speculative corners of the investment community with a higher tolerance for risk, like hedge funds, who are bound to be looking at China right now as an attractive bet.

Stocks have fallen 15% in a couple of months and are flirting with the lowest levels in nearly six years, deflation hangs heavily over the economy, the growth outlook is darkening, and authorities appear unable or unwilling to unleash the stimulus required to turn all that around…

… here is a snapshot OF USTs as of 659a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities are mixed, USD pressured as the odds of 50bps tick up … Bonds are incrementally firmer but with trade rangebound awaiting speak from ECB’s Lane … USTs are relatively contained as markets count down to this week’s FOMC policy announcement, as it stands market pricing has the odds of a 50bps cut at around 60% and a 25bps move at 40%. Despite the shift in pricing, USTs themselves are essentially unchanged at 115-15 in a thin five tick range.

Opening Bell Daily: China's deflating. China can't shake its deflation problem even as pork prices spike 20% … The world's second-largest economy faces the opposite challenge of the US as local meat prices go haywire.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Up first are some thought ‘bout Chinese data dump over weekend…

ABNAmro: China: August macro data disappoint | Insights newsletter

China Macro: Monthly activity data for August even weaker than expected. More support expected.

The largest bank in / of ‘Merica weekly (with a better than avg technical look at most of the on the runs…)

BAML: Global Rates Weekly Another one bites the cuts

The View: From one come many After the ECB this week, next week sees the FOMC, BoE, BoJ and Norges. We expect the FOMC to cut by 25 bp, the BoE and BoJ to remain on hold. Focus on rinban in Japan.

Rates: Another one bites the cuts US: Growth concerns support constructive duration stance; stay dip buying. Fed likely to cut 25bps next week; dots likely hawkish vs market but not Powell…

…Bottom line: growth concerns support a constructive duration stance; we hold our existing steepener recommendations. Fed will cut 25bps; dots may be hawkish vs market but Powell likely won’t be. For clients who think too many cuts we recommend cross market expressions or bear flatteners in options space.

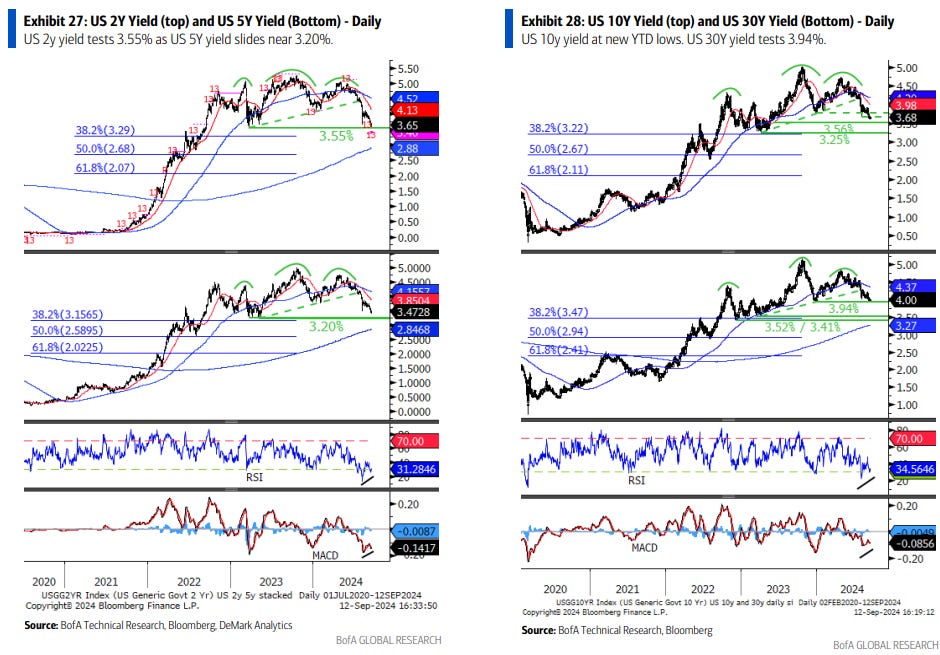

…Technicals: US 2Y & 30Y yield teetering on a cliff edge US 2Y yield tests 3.55% (its 2023 low) and US 30Y yield test 3.94% (it’s 52wk low). These levels, if broken, could extend the decline in US yields in H2.

Our base case view called for peak yield by US Memorial Day and lower yields thereafter. We look at the charts of US yields below and see potential for big tops, rather than ranges, as the pendulum swings from up to sideways and then to down. This is part of the reason why we advocated for being long USTs by Memorial Day and buying dips in H2. Now we see US 2Y and 30Y yield teetering on a cliff edge of 3.55% and 3.94%, respectively, as we approach the Fed meeting next week. US 5Y is getting close to its level of 3.20%. The 10Y yield has already made new 52wk lows, but its 2023 lows are still a bit lower at 3.25%. We’re sympathetic to some short-term signals that suggest yields have come a long way and may see a bounce higher, such as oscillator divergences and a TD Sequential 13. Usually yields form bottom patterns and/or longs capitulate to provide substance to refute tops/favor ranges. For now, our medium-term bias remains.

French say — let the games begin (25bps), favor bullish (5s30s)steepeners …

BNP: Sunday Tea with BNPP: Kicking off the US rate-cut cycle

KEY MESSAGES

While August core CPI and PPI inflation came in hotter than consensus expectations, we think core PCE remains on track to print a soft 0.2% for the month.

We expect the Fed ultimately to cut by 25bp at its September FOMC meeting this week, with the median dot likely projecting 75bp of rate cuts this year and Chair Powell reiterating a willingness to ease by more, if signs of labor market deterioration emerge.

In rates, we continue to see risk-reward as favorable for bull steepening positioning, expressed via 5s30s UST and 6m1y receiver spreads.

In FX, we think there is room for the USD to weaken from its current expensive levels but see little tactical asymmetry going into the coming week. Instead, we prefer positioning short high beta versus low yielders.

From France to Germany now in the house … weighing in on the 'Faust 50' and offering reasons to be happy …

This time last week we suggested that if we were going to get 50bps from the Fed on Wednesday we probably needed a media leak as we approached or entered this past weekend. Thursday's WSJ (link here) and FT (link here) articles certainly weren't smoking guns towards 50bps but they suggested the prospect was higher than where it was after Wednesday's slightly firmer CPI report. It's hard to know how informed the WSJ article was but as you will remember, the same author (Nick Timiraos) wrote a much firmer endorsement of a surprise 75bps hike just before the June 2022 FOMC which completely moved the needle at the time. There was little doubt that this was well informed. As you'll see from my CoTD on Friday (link here), our economists and strategists put both WSJ articles (2022 vs 2024) from this same author into our proprietary AI tool (its not called ChatDBT but I'll refer to it that way) and it told us that "the June 2022 article conveys a strong sense of urgency and conviction regarding the need for a significant rate hike to combat inflation. The September 2024 article, while discussing the possibility of a rate cut, presents a more balanced and less decisive outlook, reflecting the Fed's cautious approach in navigating economic uncertainty". So it confirmed our prior about the fresh WSJ article that although this could be a signal that things were closer than we thought, there is no slam dunk here. We feel this is a good use case for AI as we all have our biases and its nice to see what the unbiased linguistic analysis suggests. I'll be typing everything my wife tells me into this now to ensure I get the true meaning not what my biases interpreted.

DB: Mapping Markets: 5 reasons to be optimistic on markets

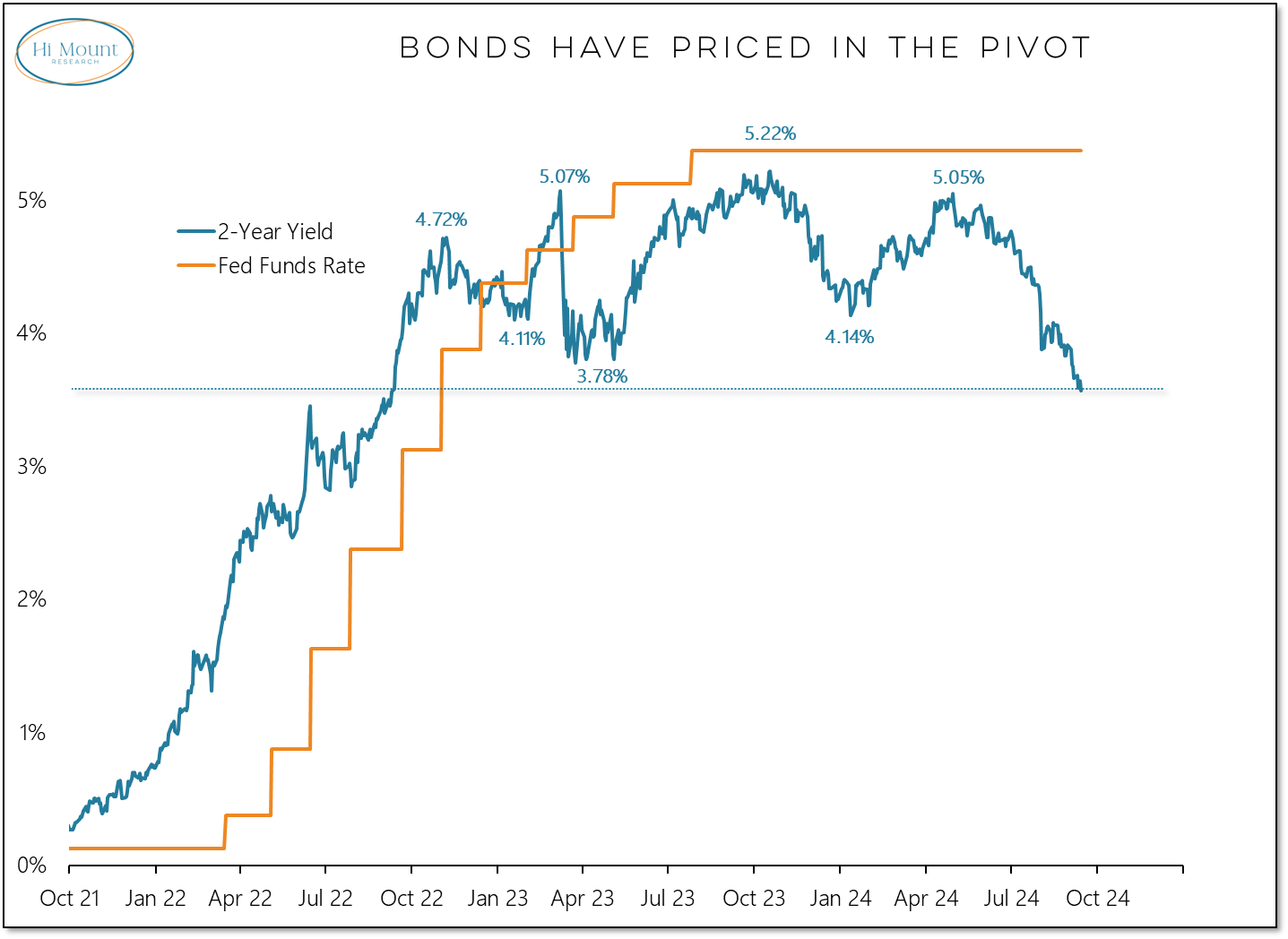

For all the market jitters over recent weeks, we shouldn’t forget that a lot is going well right now. The S&P 500 just had its best week of 2024 so far, and is less than 1% beneath its all-time high. The 2yr Treasury yield hit a two-year low on Friday. And Bloomberg’s global 60:40 index reached a new record.

5 reasons to be optimistic on markets

1. When the Fed cuts rates into a soft landing, that has historically been a goldilocks combination…

2. Global data is continuing to point away from a recession…

3. The prospect of Fed rate cuts has already helped to ease financial conditions, and other central banks have begun the easing process too, so we’re in a synchronised easing cycle now…

4. Risk assets have proved impressively resilient to various shocks this year…

5. Although September is seasonally one of the most difficult months on a seasonal basis, Q4 has historically been one of the strongest periods.

Front-end yields made new cycle lows and the curve steepened after reports from Fed reporters at multiple media outlets indicated the FOMC had not ruled out a larger-sized 50bp cut next week

With the disinflationary process resuming, labor markets softening, the Fed’s reaction function shifting more dovishly, and the current policy stance restrictive, we see the case for the Fed to lower policy rates swiftly to preserve the current expansion...

...We continue to think the Fed shouldease50bp next week and that remains our forecast, but we recognize this is a close call

Even so, with Fed leadership not wanting to see further softening in labor markets and potentially supportive of more front-loaded easing, we think risks skew toward more aggressive easing in coming months

Historically, the Fed has been more likely to under deliver relative to expectations ahead of FOMC meetings during easing cycles, but there are instances in which the Fed delivered more aggressive action than markets had expected in 2001 and 2003

Should the Fed deliver a 25bp ease, we think there is limited room for yields to rise as we would expect Chair Powell to deliver dovish remarks during his press conference, as he has consistently done over the last year

We think this backdrop skews risks toward lower yields over the near term, and we continue to favor steepeners to express our core bullish view. With the risks skewed toward more front-loading of easing, we continue to hold 3s/30s steepeners

,,, Third, the current stance of policy is highly restrictive. The real Fed funds rate is approximately 2.75%, a full 200bp above the Fed’s real longer-run dot. Using either the Fed’s longer-run dot (with data back to 2012) or the Holston-Laubach-Williams r* estimate, policy rates were negligibly restrictive in 2019, and only about 100bp restrictive in mid-1995 before the first cut (Figure 13The Fdfunsrate iconsderably moresticv hantypoi verthlas 30yer). To be fair, in 1995, the Fed had the luxury of shallow cuts because the neutral rate of interest was rising thanks to the IT-driven productivity boom, and it’s hard to say whether we are at the early stages of another productivity boom now. However, even if we adjust these measures of neutral policy rates higher by 50bp, there would still be more than 150bp of easing to bring policy rates back to more neutral levels, so why would the Fed want to spend nearly a year to bring policy back to neutral, and potentially threaten the expansion in the interim?

…. AND in light of this weekends turn of events, a note written / sent earlier on Sunday BEFORE any of Sunday afternoons golf course attempted assassination …

MS: Sunday Start | What's Next in Global Macro: A Debate, but No Resolution

Last week, Vice President Harris and Former President Trump met in Philadelphia for a debate. Investor interest was high, and understandably so. As our Chief Economist Seth Carpenter highlighted last week, visibility remains low when it comes to the outlook for the US in 2025. That’s because the election could put the county on policy paths that take economic growth in different directions. And of course, the last presidential debate in June led to President Biden’s withdrawal, changing the race dramatically. Hence, any election-related event that could provide new information about the probability of different outcomes and the resulting policies is worth watching…

… If the debate provided little new information about the impact of the election on markets, what guidance can we offer? Here are two principles we would adhere to:

Between now and Election Day, expect the economic cycle to drive markets: The high level of uncertainty and the lack of precedent for market behavior in the run-up to past elections suggest sticking to the cross-asset playbook in our mid-year outlook. In general, we prefer to bonds to equities. While our economists continue to expect the US to avoid a recession, growth is slowing. That bodes better for bonds, where yields may track lower as the Fed eases, than for equities, where earnings may be challenged as growth slows.

Lean into market moves that election outcomes could accelerate: For several months, Matt Hornbach and our interest rate strategy team have been calling for a steeper yield curve, driven by lower yields in shorter-maturity bonds. They have been guided by our economists’ steadfast view that the Fed would start cutting rates this year as inflation eases. We doubt that policies in Democratic win scenarios would change this trend, and a Republican win could accelerate it in the near term, as higher tariffs would imply pressure on growth and possibly further Fed dovishness this year. Pricing that path could steepen the yield curve further.

We recommend using the weeks that remain before the election to get smart on the economic and market impacts of a range of election outcomes. For our guidebook, and deeper dives on impacts for the energy sector, healthcare, emerging markets, and more, see here…

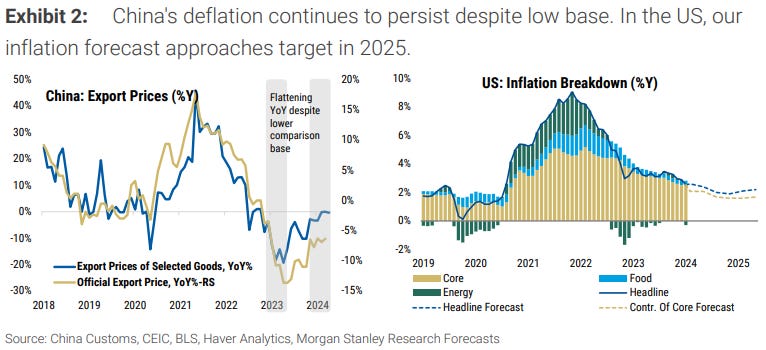

MS also writing ‘bout WHY it may be that China DEFLATION matters …

MS: The Weekly Worldview: Why China’s Deflation Matters

China's deflation has intensified, and things could get worse before they get better. The effects don't stop at the Chinese border.

… We have noted that so far, China’s deflationary cycle has lowered core inflation in the euro area and the US by about 0.1pp and has lowered core goods inflation by about ½pp. That contribution is meaningful in the context of central banks that are trying to squeeze out the last couple of tenths of excess inflation. The ECB revised up its forecast for core inflation by 0.1pp in 2024-25 based on services inflation. In the US, the three-month annualized run rate on core PCE inflation is around 1.9% right now, so the deflationary effect from China is clearly of a relevant magnitude.

Market attention is focused on the Federal Reserve meeting this week. A rate cut is clearly expected (and long overdue), as inflation pressures continue to fade in the US. However, a rate cut of more than 25bps seems unlikely—while the Fed is late in cutting rates, a larger move might be taken as a sign of panic. Higher frequency cuts rather than larger cuts seem most likely.

There are no Fed speakers, with the blackout period in operation, but the ECB is trying to fill the vacuum. Chief Economist Lane is among those speaking. While ECB President Lagarde tried to avoid giving signals on future rate cuts, markets are disregarding this reticence and pricing a steady pace of easing.

The political polarization of the US economy was in evidence on Friday, when Michigan consumer sentiment data rose solely on Democrat optimism. It might be that Democrats are experiencing a different economy from the rest of the US, but it seems more likely that the sentiment is tied to Vice-President Harris’s standing in the opinion polls. Events over the weekend are unlikely to matter to markets, unless they are seen as changing election probabilities.

New York Empire manufacturing sentiment poll is due, and is as vulnerable to political trends as any other survey.

Finally …

Wells Fargo: Part IV: A New Framework to Predict Probability of Monetary Policy Pivots

Summary

The fourth installment of this series develops a new framework to quantify episodes of monetary policy pivots.

We also present a probit regression to predict the probability of a policy pivot during the next two quarters.

In our view, accurately predicting periods of monetary policy pivots is vital, as a rate cut that comes too late or too soon would be harmful to the economy and damage the FOMC’s reputation.

Our framework estimated that there are 26 episodes of policy pivots in the post-1990 period.

Using a threshold of 35%, the probit framework accurately predicted episodes of policy pivots in the post-1990 era.

The latest probability (Q2-2024) of 43% indicates that a rate cut cycle may start soon (within the next two quarters).

Given the historical accuracy of our framework, we believe the toolkit would provide useful insights for decision makers, as it can be updated in real time to gauge the likely duration of the upcoming easing cycle.

We believe accurately predicting the near-term path of the fed funds rate is vital for effective policymaking as well as policy communication. The next installment of the series will present a new approach to predict the fed funds rate two quarters out (up to four FOMC meetings ahead).

… And from Global Wall Street inbox TO the WWW, i’ll begin with a couple links from The Terminal (.com) …

Bloomberg (Dudley OpED): The Fed Should Go Big Now. I Think It Will.

An aggressive 50-basis-point reduction in interest rates makes sense.

… The tension between 25 or 50 has increased notably, thanks to newsarticles that have pushed market expectations toward the larger move. As I noted last Friday at a Bretton Woods Committee conference in Singapore, the logic supporting a 50-basis-point cut is compelling…

…Why, then, might the Fed not go for 50? Here’s the best explanation I can come up with.

First, the expected destination for short-term interest rates matters much more than the pace of reductions. Expectations drive longer-term interest rates, including mortgage rates. With roughly 250 basis points of cuts priced in by the end of 2025, the size of this week’s move shouldn’t matter much.

Second, the Fed wants to make sure it has conquered inflation. It has been fooled before: Early this year, inflation bounced back, forcing the central bank to keep rates higher for longer. Chair Jerome Powell doesn’t want to repeat the mistakes of Arthur Burns, who didn’t stay the course in pushing down inflation in the 1970s.

Third, although the US economy has slowed a bit and the labor market has weakened, there are few signs that it’s in or near a recession. The Atlanta Fed’s GDPNow model projects annualized, inflation-adjusted growth of 2.5% in the current quarter.

Finally, a smaller move might preempt complaints from Donald Trump that the Fed is boosting the economy to improve Kamala Harris’s electoral prospects. Fed officials would presumably prefer to stay out of this year’s election politics as much as possible.

Despite this, I expect the Fed will do 50. I believe Chair Powell favors an aggressive approach: In his speech at Jackson Hole last month, he pointedly observed that a further weakening of the labor market — which seems to be happening — would be “unwelcome.” Monetary policy is tight, when it should be neutral or even easy. And a bigger move now makes it easier for the Fed to align its projections with market expectations, rather than delivering an unpleasant surprise not warranted by the economic outlook.

Bloomberg: Fed Ready to Unshackle US Economy With Soft Landing at Stake

The central bank’s first interest-rate cut is widely expected on Wednesday, but investors are more focused on what will happen immediately after the announcement.

… More recently, however, the economy has downshifted. While layoffs remain low, hiring has stalled, making it harder for those who are unemployed to find work. Job vacancies have come down to the lowest level since 2021. Meanwhile, higher mortgage rates and surging home prices have squeezed housing affordability, causing annual existing home sales to fall in 2023 to the lowest in almost 30 years.

… Bond investors are ready to rejoice this week as the long-awaited start of US interest-rate cuts should arrive on Wednesday. That’s partly fueled by the extremely strong expectations for the size of the reductions the Fed will deliver over the coming year. Futures traders are betting the cash rate will be lowered at least 225 basis points over the coming year. That’s around the most ever priced in, and it is also significantly larger than the easing pace expected just before the past six rate-cut cycles kicked off. Note that we don’t have a ready way to gauge expectations heading into the steep reductions of the early 1980s, because the futures data doesn’t go back far enough.

Further reason for bond bulls to be optimistic is the way that the Fed has previously delivered at least as much as markets anticipated. There may be some reason for caution about whether that dynamic will play out this time — given the lack of any clear signs of a US recession and the aggressive nature of the current bets on cuts. Still, if the Fed gets even close to what is priced in now then bonds should extend their rally quite handsomely.

The odds are 50-50 on a jumbo 50 basis points, but either way Powell won’t be alone at the peak any longer.

… We’ve had this much optimism for cuts before. What’s different this time? The key change is that globally, rate cuts have become the norm rather than the exception. This is the latest edition of our diffusion index, in which rate cuts or hikes by each of the 57 central banks count equally.2 August saw the biggest balance toward cutting since the start of the pandemic:

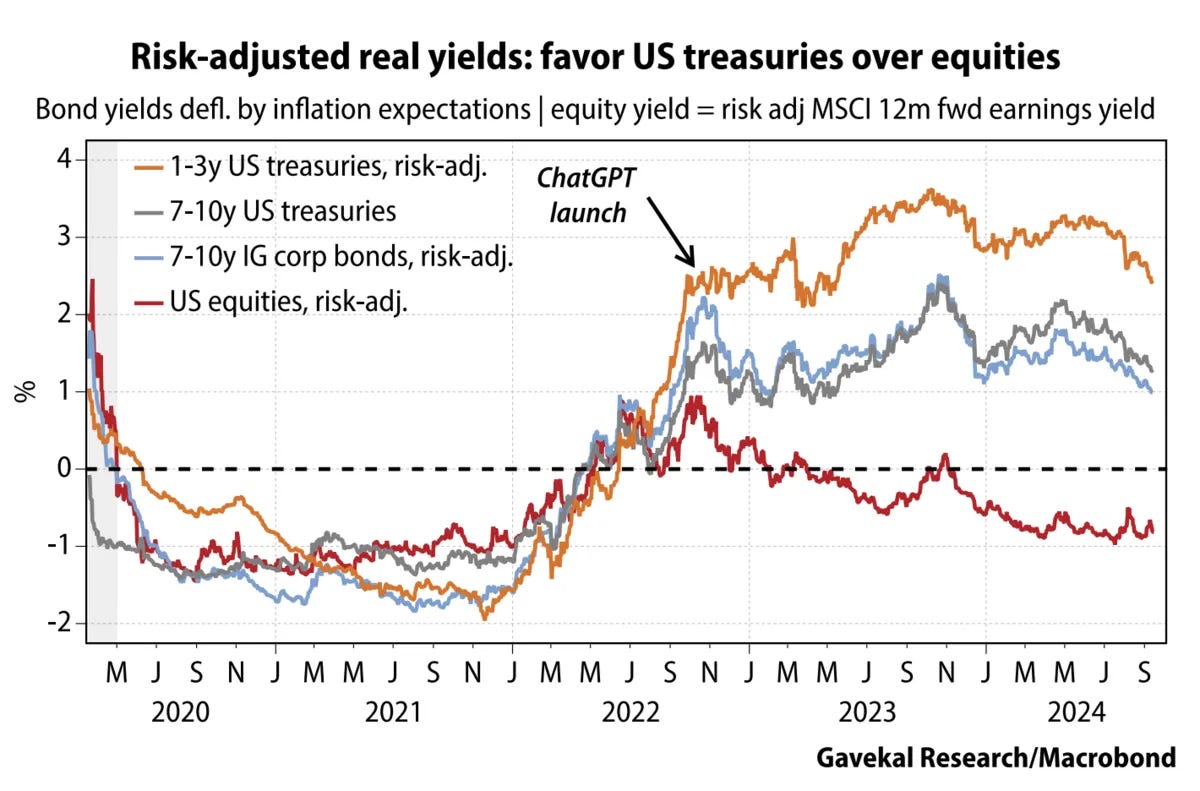

…And the Markets? … This Gavekal chart shows the relative valuations of US bonds to equities. It suggests that the Fed governors should not be bothered in the slightest by any need to prop up share prices:

All else equal, loose policy would weigh on the dollar by making US assets less attractive compared to global alternatives. That’s not, or shouldn’t be, any kind of a problem for the Fed …

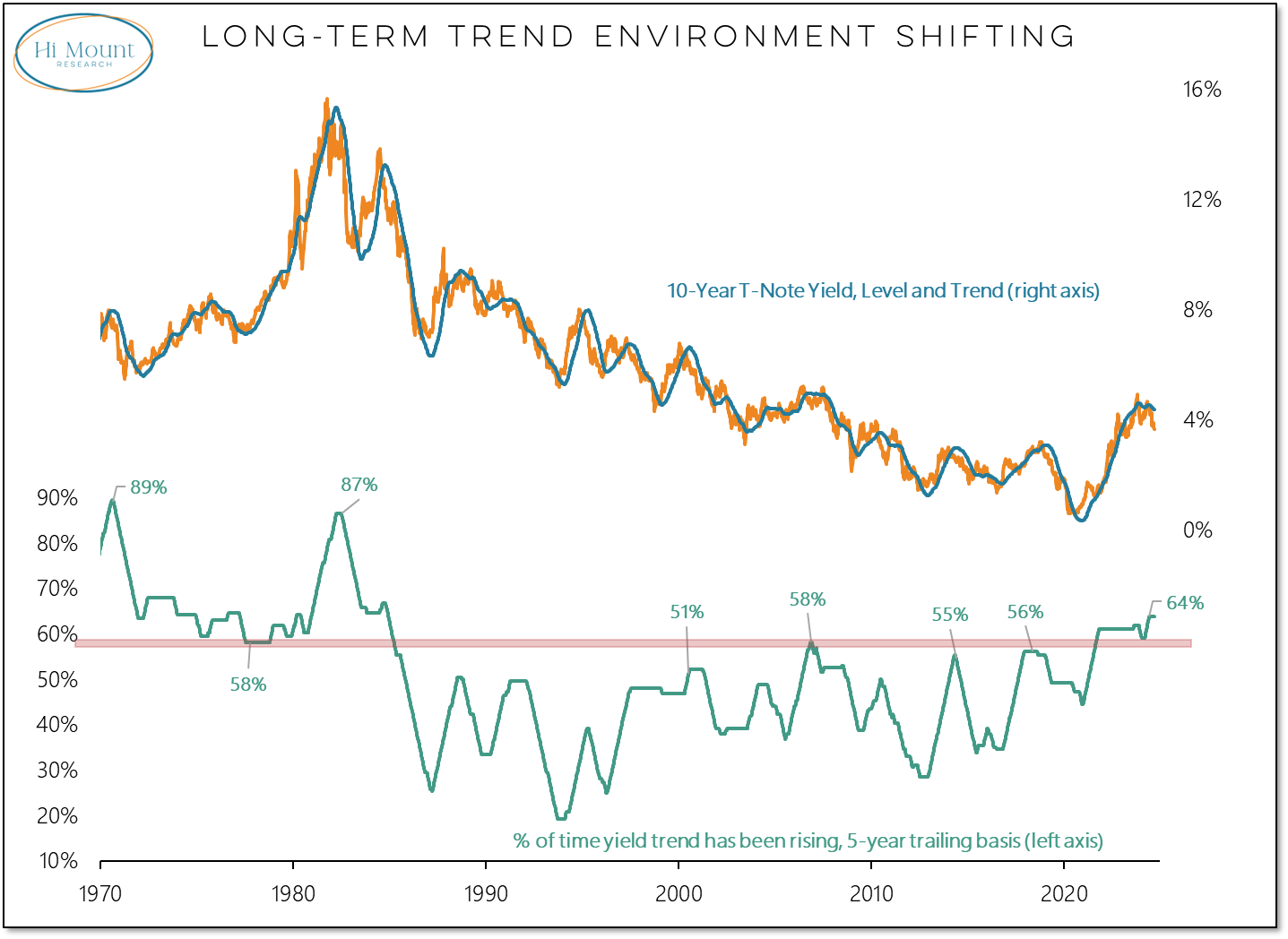

Rate cuts are coming as the trend environment gets more challenging for stocks

The Fed is in focus this week. The headlines focus on the question of 25 vs 50 basis points for the initial cut. The bond market is pricing in nearly 175 basis points of total easing as 2-year yields drop to their lowest level in over two years.

The long-term trend environment for bonds has shifted. Looking through the easing cycle that will begin this week, yields are likely to remain higher for longer than the experience of recent decades would suggest is likely.

Breadth has been bullish as new highs exceed new lows. But while net new highs have been positive, they have struggled to expand. That leaves stocks vulnerable to rising volatility. But as long as more stocks are making new highs than new lows, odds favor above average returns and below average risk…

They're not tryin to kill Kamala just sayin 😉,

1 drawback living near Reno, I'm subjected to Commiela's constant commercials during NCAAF/NFL,

'A new way forward', 'This is the Time', the ultimate Recycled candidate,

I'm sure it was another 'Lone Nut', Rothbard has interesting thoughts on THAT matter,

I guess she's Less Scary than Big Mike? 😜