Good morning … In to the weekend and without cause for any concern, I’m going to watch 10yy vs 4.08% and some context…

… again NO reason to suspect it’s coming or out there (although momentum / stochastics bottom panel are reflexing higher) and the WEEKLY downtrend is defined. Perhaps it is a DIPortunity or something that’s more wishful thinking (but then, we know how THAT goes … when up nearer there, we’ll be running around thinking it — bullish move — is OVER !

In any case, watching this afternoon’s close in relationship to 4.08 and in as far as yesterday’s economic inkblot test …

ZH: US Retail Sales "Beat" Thanks To Yet Another Massive Downward Revision ZH: Can The Fed Defend Cutting Rates With NSA Jobless Claims Near Record Lows? ZH: They Can't Keep The Lies Straight... (industrial production)

For the 13th month in the last 16, US Industrial Production data was revised lower (significantly lower)...

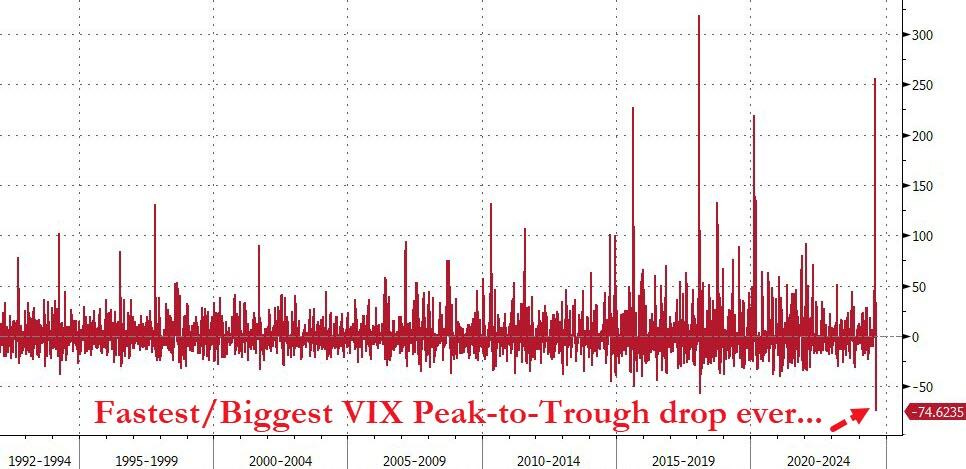

… This all combined to produce very stable markets by days end with the VIX plunging ‘at a record pace’ …

ZH: Stocks Soar, Bonds & Bitcoin Battered On 'Fake' Data As VIX Plunges At Record Pace

...at its fastest/largest pace of decline ever...

…. which leads me to ask … IF stocks SOAR and we’ve totally put last weeks equity — gotta CUT NOW — move in rear view mirror and THEN some, is a rate CUT still needed??

OR said / asked another way, has the markets already priced one / several IN and so, nothing further really required?

… here is a snapshot OF USTs as of 650a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities on the front foot, USD lower & Crude slips on Libya's Waha updates … USTs are contained, but off worst levels, Gilts fairly unreactive to its own Retail Sales, holding just shy of 100.00 … USTs have climbed slightly above 113-00, as the complex received a modest bid in recent trade. Docket features Building Permits/Housing Starts, Uni. of Michigan prelim. and remarks from Fed's Goolsbee.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: July retail sales: Well above consensus (as expected)

Retail sales jumped 1.0% m/m, reflecting a rebound in auto sales following June's disruptions and another month of resilience in the control group. Although motor vehicle sales disruptions exaggerate the headline, today's data continue to downplay concerns about demand deterioration, sustaining the resilience narrative…

BMO: Jobless Claims Drop, Retail Sales Improve, Chances of 50 bp Cut Decline

We expect Fed Chair Powell to signal that incoming data supports the FOMC beginning to normalize policy imminently, all but cementing expectations for a September rate cut.

While we do not think Powell will rule out a 50bp cut in September, he is likely to downplay fears that the Fed is behind the curve or that the US economy is rapidly deteriorating. Our base case remains for a 25bp move.

We look for a cumulative 50bp of cuts by year end. Risks to this view are becoming more one-sided, however, and a more pronounced weakening of the labor market that might challenge the employment leg of the Fed’s mandate would warrant greater easing.

DBDaily: US retail beat weighs against 50bp cut (inkblot … see whatcha wanna see)

DB: Early Morning Reid (on ReSale Tales and the ‘control group’ which, if my memory serves me correctly is …’all sales, excluding receipts from auto dealers, building-materials retailers, gas stations, office supply stores, mobile homes and tobacco stores. This filtered number is a more precise method of gauging consumer spending, and consumer spending is a large component of U.S. GDP.’ -CME Group HERE)

… Yesterday's moves were driven by the upside surprise to the US July retail sales, Walmart’s earnings for Q2 and initial jobless claims that were decent. In terms of the details, headline retail sales strongly exceeded economists’ expectations, accelerating to +1.0% month-on-month (vs +0.4% expected), up from -0.2% in June (revised down from 0.0%). This is the fastest increase in retail sales since January 2023. And retail control rose by a strong +0.3% (vs +0.1% expected), with a third consecutive monthly increase bringing the 3m annualized growth of retail control to +6.8%, its highest since June 2023…

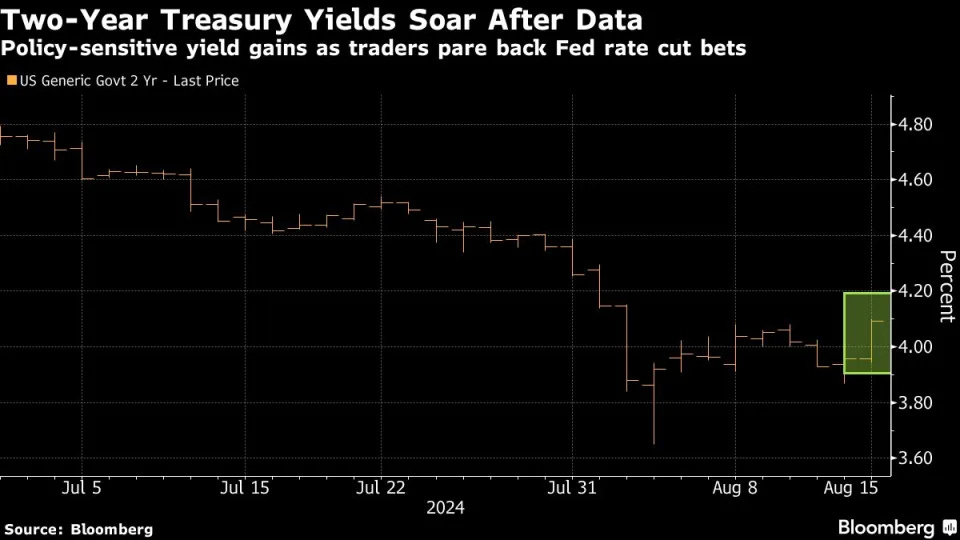

… Despite these remarks, markets still trimmed expectations of a 50bps cut in September with the amount of cuts expected falling from 35bps to 32bps, bringing the odds of a full 50bps cut to 30% from 40% the day before and down from being fully priced at the peak last Monday. The number of cuts expected by year-end fell -9.7bps to 94bps. This is below 100 for the first time since the July payrolls print on August 2 and down from an intra-day peak of 138bps last Monday.

Off the back of this, fixed income sold off, and the US 2yr yield rose +13.5bps, its largest daily increase since the first week of June…

DB: July inflation recap: Rent surprise doesn't dent disinflation trend

Both headline (+0.15% vs. -0.06% in June) and core (+0.17% vs. +0.06%) CPI were slightly softer than we expected. Taken together, the year-over-year rate for both headline and core fell a tenth, the former to 2.9% and the latter to 3.2%. Shorter-term trends showed noticeable improvement, with the three- and six-month annualized rates both falling by 0.5 percentage points respectively (to 1.6% and 2.8%).

The major story within the July CPI data was large price declines in some volatile categories like used cars and airfares offsetting a surprise re-acceleration in both primary (+0.49% vs. +0.26%) and owners' equivalent (+0.36% vs. +0.28%) rents. Though several regions saw rent accelerate, the increase was most striking in the West, particularly in the larger cities. With leading indicators still pointing to a downtrend, we think the fundamental story of rental disinflation still holds. That being said, near-term rent gains may be higher than we previously expected.

Tuesday's PPI data was also important, which when viewed alongside the CPI data point to a core PCE print slightly weaker than its CPI counterpart. Taken together, we are looking for core PCE to post a +0.15% gain in July (rounding down to 0.1%), which would have the year-over-year rate rise by about 3bps to 2.66%.

Our forecasts have ticked up slightly, mainly reflecting a bit slower pace of rental disinflation in the near term. Our initial read on the August core CPI data is that it will grow by 0.26%. In turn, our 2024 core CPI forecast has come up by a tenth to 3.1%, along with our 2025 forecast to 2.5%. Our 2026 forecast is unchanged at 2.4%. The analogous numbers for core PCE forecasts are 2.7% (unch.), 2.2% (up a tenth), and 2.0% (unch).

Our expectations remain for three 25bp rate cuts this year. However, the debate over rate cuts has likely shifted to between 25bp and 50bp moves upfront. With inflation seeming to be on a sustainable trajectory to target, the upcoming data on the labor market will likely dictate the pace at which the Fed ultimately cuts.

UBS: The politicization of inflation (hate when he weighs in on OUR politics … really I do … dunno why, just do…and didn’t ask, hey Paul … what do YOU think bout us and our elections … we’re not weighing in on protests in UK — and neither is he …)

The US middle-income consumer is doing just fine, with yesterday’s retail sales data showing little fear of unemployment and a willingness to indulge in the national pastime of spending money. Today’s Michigan consumer sentiment data will tell us about the extraordinary degree of US political partisanship, not about what consumers are feeling.

Inflation has become a politicalized issue in the US—hence, Vice President Harris’s focus on food prices. The US presidential election may be won or lost in the aisles of WalMart. Consumers’ inflation perception is strongly influenced by food pricing, and food pricing is susceptible to profit-led inflation (because consumers have less information about costs than retailers do)…

Wells Fargo: Retail Sales Is Counterprogramming the Job Report

Summary In the month of July retailers saw a sales increase of $6.8 billion, or 25% of the total gain from the prior two years in a single month. While most of that was an autos bounce after an ugly June, gains were broadly based and thus at odds with reports of a more cautious consumer.

Yardeni: Consumers Are Still Shopping, Not Dropping

… We continue to expect the Fed will cut the federal funds rate (FFR) by 25bps in September. That may be its only cut this year, too. Market expectations for 100+ bps of rate cuts over the next six months are overdone, as they were at the start of the year (chart). We remain in the one-and-done camp for the remainder of 2024.

Here's more on today's data …

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Traders Shred Bets on Big Fed Rate Cuts on Resilient Economy

(Bloomberg) -- Treasury yields surged after signs of a resilient US economy in the latest data releases prompted traders to lower their expectations of aggressive Federal Reserve interest-rate cuts this year.

The move in Treasuries was led by the policy-sensitive two-year yield, which rose 16 basis points to nearly 4.12% on Thursday after readings of US retail sales and weekly jobless claims came in better than anticipated. Treasury yields were trading near their session peaks after 3pm in New York.

Traders pared back bets for a super-sized September rate reduction, pricing in less than 30 basis points of easing next month. They now see a total of 92 basis points of cuts for the remainder of 2024, down from more than 100 prior to the data…

Bloomberg: Carry Trade That Blew Up Markets Is Attracting Hedge Funds Again

Yen shorts have risen around 30 to 40% in past week, ATFX says

Any hint of BOJ keeping rates on hold may embolden yen sellers

Bloomberg: The rout — What a short, strange trip it’s been (Authers’ OpED)

… To start, this is how stocks have performed compared to bonds this year so far (proxied by the main ETFs tracking the S&P 500 and Bloomberg’s index of bonds with maturities of 20 years or more). The switch from stocks to bonds was the sharpest since 2020, after years in which stocks and bonds had moved together. Subsequently, the rebound has been only slightly less dramatic. Stocks have beaten bonds by about 18% in the last 12 months. That’sa lot:

… Troy Ludtka of SMBC Nikko points out that over the last 12 months, the 10-year Treasury yield has moved almost perfectly in line with the oil price, with a two-week lag — a rise in Brent Crude will be followed two weeks later by aclimb in the bond yield, and vice versa. It’s hard to dismiss as coincidence. Maybe we’re being fooled by randomness, but it seems unlikely:

Tight synchronization like this brings back some bad memories of the years before the financial implosion of 2008.

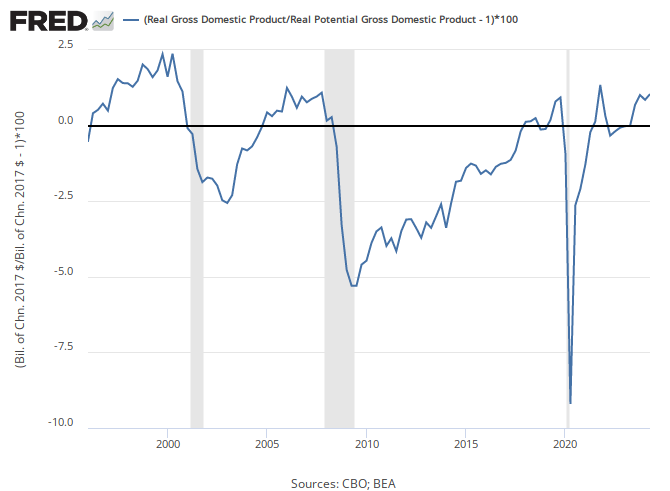

Real GDP growth picked up significantly in the second quarter of 2024, according to the BEA’s advanced estimate, at an annualized rate of 2.8%. While this output growth is an important measure of activity on its own, many policymakers also pay attention to actual output growth with respect to potential output growth, the economy’s estimated maximum sustainable output.

The FRED graph above shows the output gap, which is the difference between actual and potential real GDP. Output has been above potential for the past year; most recently, it appears to have exceeded potential output by about 1% in the second quarter, up from approximately 0.9% in the first quarter. This is an improvement over 2022 and early 2023, when the output gap was slightly negative, and is roughly in line with the second half of 2019, when economic growth was relatively high compared with its 2010-2018 average.

The graph also shows the output gap tends to be negative after recessions, but then eventually returns to a positive gap after a recession. For example, the 2008-2009 financial crisis was deep and long enough to keep actual output below potential all the way through 2017. It wasn’t until late 2019 that the gap became firmly positive around levels not seen since 2007.

One signal of the economy’s resilience is that output returned to potential within two years of the initial COVID shock in 2020 despite a precipitous decline. Another signal is that the output gap has continued to become positive even as potential output has continued to grow at a stable pace: Annualized quarterly growth rates of potential output have hovered around 2% since 2018. By comparison, growth rates of GDP have averaged 2.8% over the past eight quarters. This also has implications for monetary policy, referred to in this FRED Blog post about the Taylor Rule.

An important caveat: Potential output cannot be observed, so policymakers contend with considerable uncertainty here, including frequent and unpredictable revisions to the estimate of potential output. A good illustration of these revisions over time was delivered by Larry Summers in the 2016 Homer Jones Memorial Lecture.

ING: US data resilience sees market favour a 25bp September cut

Stronger retail sales and jobless claims numbers have provided evidence to suggest a 25bp cut at the September FOMC looks more likely than a 50bp cut right now. Nonetheless, with Fed officials emphasising a growing focus on the labour market, the 6 September jobs report is what will determine what happens

Signs of cooling inflation and a slowing but still growing economy have helped drive Treasury yields lower across the curve (today’s move notwithstanding). However, the recent shift on the yield curve has not been parallel across maturities, as the more monetary-policy-sensitive 2-year Treasury yield fell more than 10-year yields. The bull steepener — when short-term rates fall more than longer-term rates — has left the closely watched 10-year minus 2-year Treasury curve spread only about 0.16% away from ending its record-long inversion of 529 trading days.

Curve Spreads are Close to Normalizing

… Summary The shape of the yield curve receives a lot of attention in the financial media, especially when it crosses above and below zero. However, its use as a recession indicator needs some additional context. First, both an inversion and dis-inversion often precede a recession, but the timing of when the actual recession occurs can vary significantly after each signal. Second, the ominous headlines over the curve normalizing do not necessarily align with historical market performance, as the S&P 500 tends to trade higher after curve spreads cross back above zero.

Overall, LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities, while actively monitoring for signs of an inflection point during this pullback. The Committee maintains its modest overweight to fixed income, funded from cash, which can help buffer against equity market volatility should economic conditions worsen.

WolfST: These Retail Sales, in Face of Dropping Prices of Goods Retailers Sell, Support Solid Growth in “Real” GDP & Inflation-Adjusted Consumer Spending

Our Drunken Sailors are in No Mood to slow down. Massive waves of migrants also boost retail sales.

Our Drunken Sailors, as we lovingly and facetiously have been calling them for over a year, the pillars of the US economy, are still at it, splurging at retailers. Retail sales jumped by 1.0% in July from June, seasonally adjusted, the biggest month-to-month increase since January 2023. Year-over-year, not seasonally adjusted, retail sales rose 4.0%, to $724 billion…

More over the weekend but for now, good luck as you plan your week ENDING trades and trade you week ENDING plans … THAT is all for now. Off to the day job…