while WE slept: USTs cheaper/steeper; as the RANGE trade ranges, #Got5s?; CPI, NFP precaps; Global Wall asking AI about AI impact on r*; TIME Mag person of the year curse ...

AND … gosh, yesterday’s note was long … while I don’t get paid by the word, well, the hawkish / dovish <choose one> rate cut required bit more time / space, generally speaking.

I’m sorry.

Do want to mention … HOPEFULLY Ms. DiMartino Booth’s OPEN LETTER was not lost in the shuffle and I’d urge one and all to read IF you missed it.

Ok SO as the day begins and the week mercifully comes to an end, I’m drawn to the fact 10s continue to romance 4.15% … I’ll have a look at something over the weekend but today, for whatever reason unknown to me, I’m drawn to this chart of the belly — 5s — on a DAILY basis. It would appear to ME and my untrained eyes that yields have been driven largely this year by a downtrend (GREEN TLINE) and there have been several ripORtunities (nearer 3.50%) for one to sell / get short … Now, though, it would appear gentle, steady UPtrend (RED TLINE) that has helped shape the year that is almost the one that was, well … the UPtrend is relevant today. Both psychologically (3.75%) and as we romance the TLINE …

… and worth noting in / around the FOMC middle of the week, momentum had rolled over, crossed bullishly (on this, the DAILY chart) suggesting path of least resistance LOWER … lets not forget this overSOLD condition could very well work itself off with ‘time at a price’, too …

#Got5s? …. and there you go.

Mom always said, if you don’t have anything NICE (bullish?) to say, then don’t say nuthin’ at all?

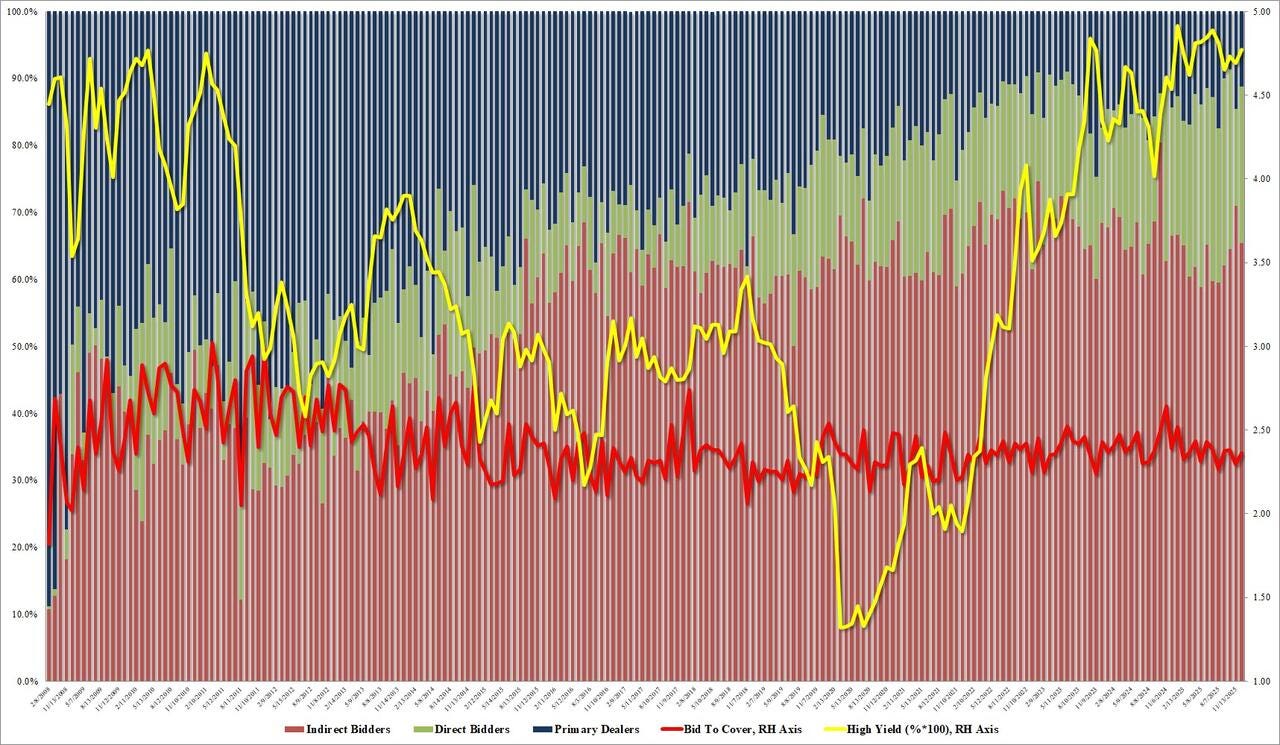

Now then … on heels of yesterdays supply, a quick recap …

…The internals showed continued solid buyside demand: Indirects were awarded 65.4%, down from 71.0% in November. but stripping away that one outlier auction, the foreign demand was the highest since January. And with Directs taking 23.5%, in line with the recent average of 23.9%, Dealers were left with 11.2%, down from 14.5% last month and below the six auction average of 12.5%.

Overall, this was another solid auction with impressive demand and refuting creeping concerns about rapidly rising long-end yields amid a global bond selloff, one which for now at least has avoided the US.

… that said, as good as it may have been, STOCKS lapped the field and with stocks UP, yields did wind up a touch cheaper on the day … doing what it is bonds do …

ZH: Continuing Jobless Claims Plummet To 8 Month Lows

…But while initial claims rebounded back to ‘normal’, continuing jobless claims plummeted

Source: Bloomberg

We assume whatever screw-up that seasonal adjustments caused in initial claims the week before have rippled through to the continuing claims data this week, but still - taken at face value, it’s great news!

However, there could be an even more silver lining as we noted last week, before Trump sent out his ICE troops, California’s Continuing Claims were running ~400K per week. Beginning in the summer, however, these claims steadily dropped... and perhaps this week’s crash in continuing claims is the chopping block coming down on illegals claiming benefits in California?

… devils ALWAYS in details and plummeting claims may NOT be what one thinks … Finally, with stocks recovering (yes, I believe tech did lag) always have to pause and read any time a market related to LEHMAN CRISIS …

ZH: Oracle Plunges Most Since Dot Com Bubble, CDS Blow Out To Lehman Crisis Levels

… AND I’m done here. For now. Hope to have somewhat more over weekend but for now … here is a snapshot OF USTs as of 706a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures point to a mixed open with NQ lagging following AVGO earnings; Markets await Fed dissenters … Global bonds are mildly pressured, scaling back recent upside … USTs have held a negative bias this morning, attempting to scale back from some of the strength seen post-FOMC, which also sparked a steepening of the curve. Today, US paper is trading at the lower end of a 112-09+ to 112-14 range; there is now a clear path towards the 112-00 mark, should the pressure continue, and then 111-29 thereafter. The data docket ahead is void of any pertinent data, but focus will be on scheduled Fed speak via Paulson, Hammack and Goolsbee – the latter, alongside Miran and Schmid, should release an explanation for their recent dissent also.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

CPI up next week (glad someone’s keeping tabs on all this) and here’s a precap for us to make whatever we will … the translation TO PCE doesn’t look particularly rate cut friendly, though …

The BLS will report November CPI next week, but will NOT publish October headline and core CPI, leaving us to track y/y or 2m price changes. We estimate headline CPI rose 3.1% y/y (+0.1pp from September) and core CPI rose 3.1% y/y (+0.1pp). Our forecast for the November NSA index is 325.210.

…Translating CPI to PCE prices is likely to be challenging, given missing October values and m/m changes for November. In our view, the BEA is likely to apply the 2-month price changes reported by the CPI to the published September PCE price index, to arrive at a November PCE price index. Similar to the CPI, we will be unable to calculate the % m/m changes, though we will have an annual (% y/y) rate. Applying our November CPI forecasts, we estimate core PCE to have increased 2.9% y/y in November (from 2.8% y/y in September).

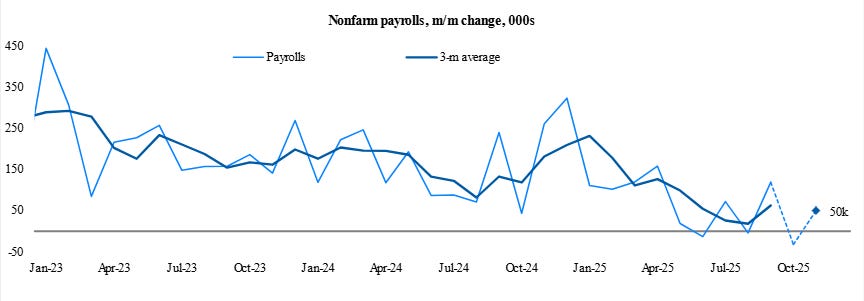

Speaking of precaps, there’s jobs data coming …

11 December 2025 Barclays US Economics: October/November employment preview: Government distortions

We estimate nonfarm payrolls held steady in October and rose by 50k in November. Private payrolls likely grew 75k both months, with government jobs declining due to a fork-in-the-road option. We expect the unemployment rate to edge up to 4.5% and hourly earnings to rise 0.3% m/m…

…We continue to think that the direction of travel for unemployment will be sideways over the medium term. Although we expect job gains to level out at around 50k for the rest of 2025, we think declines in immigration and aging of the domestic labor force will slow monthly labor market entries.

At days end, it’s worthy of note that the RANGE remains the biggest theme at moment and that’s not only MY view (ahem, 4.15% … 10s) but also others, far more well respected (who ALSO bought very front-end…)

…The tone in the US rates market was consistent with the range-trading dynamic that has been in place throughout the last several weeks. This held despite the increase in initial jobless claims to 236k – albeit from a seasonally-impacted prior read of just 192k. The timing of the Thanksgiving holiday continues to distort the series, giving context to the muted market response. The trade deficit unexpectedly narrowed in September, which is a net positive for Q3 growth estimates even as we’re skeptical that net exports will drive the real growth agenda beyond near-term recalibration. We have been impressed, if not surprised, by how well the 10-year sector has managed to remain within the zone of 4.00-4.20%. To put a finer point on it, the 10-year hasn’t been outside the range of 3.934% and 4.207% since earlySeptember, and there doesn’t appear to be much incentive for a breakout anytime soon…

…As for an update on our trading book, we bought FFK6 on Thursday at 96.545. The market is only pricing 20 bp of cumulative rate cuts for the remainder of Powell’s term as Fed Chair. Our read is that the ever-devolving employment picture suggests that there is more downside risk for policy rates than the SEP’s baseline outlook. Next Tuesday could readily challenge expectations for a pause in rate cuts in early 2026, and we’re approaching the BLS payrolls numbers with a healthy dose of caution given the recent weakness in ADP and Revelio Labs. As for our other active trade, the remaining portion of our 5s/30s steepener position (entered 10/24 at 96.1 bp) has become increasingly profitable in the wake of the FOMC. The curve reached as high as 108.2 on Thursday. We’ll continue to target 117.3 bp for the remaining portion of the clip. Our stop level remains at 98.5 bp to protect against losses in the event of a flattening reversal…

Bearish rates? Use AI to assess the AI risks to the risks … makes sense, lets see … what could possibly go wrong … (and yes, I tried it not with 5.1 but still, and got different results … HERE) …

We made the case for higher US equilibrium interest rates driven by a shift in the supply/demand for savings relative to the post-GFC period. We identified two (opposite) tail risks from AI (a bubble or a significant increase in inequalities) as creating a potential challenge to our view.

But what does AI have to say about the impact of AI on equilibrium real rates? Here are prompts to, and answers from, “ChatGPT5.1 Thinking”. Its assessment: “The sign of tech’s effect on r* (upward) is convincing; the magnitude is hugely uncertain.“

Prompt: What does academic research say about the impact of technological progress on equilibrium real rates. Summarise the findings and the conclusion in terms of the net impact of upward vs. downward pressures on equilibrium real rates. Provide the answer in less than 250 words.

ChatGPT5.1 Thinking:

In standard growth and New Keynesian models, the equilibrium real interest rate r* rises with trend productivity (TFP) growth: faster technological progress raises the marginal product of capital and desired investment, so r* increases roughly in line with long-run growth.

Central-bank and academic estimates generally find a positive association between TFP growth and r*, alongside roles for demographics and risk premia.

But recent decades highlight technology-linked downward pressures. First, a broad slowdown in productivity growth is a key driver of the 1–2 percentage-point fall in r* across advanced economies since the 1980s.

Second, ICT-driven declines in the relative price of capital goods mean a given capital stock can be achieved with less spending, weakening investment demand relative to saving and lowering real rates.

Third, some “secular stagnation” models stress that digital technologies can raise desired saving (via higher inequality and income risk) more than investment, again pushing r* down.

Forward-looking work on AI and digitalisation suggests that large, complementary ICT/AI investment could lift r* modestly—typically by 0.2–0.7 percentage points—by boosting productivity and capital deepening.

Overall: theory says technological acceleration exerts upward pressure on r*, but the observed decline in r* mainly reflects a shortfall in broad-based productivity growth plus other secular forces; expected AI-related gains are likely to raise r* only moderately and with high uncertainty.

Prompt: What is your assessment of the conclusion? … …

…My assessment: the sign of tech’s effect on r* (upward) is convincing; the magnitude is hugely uncertain.

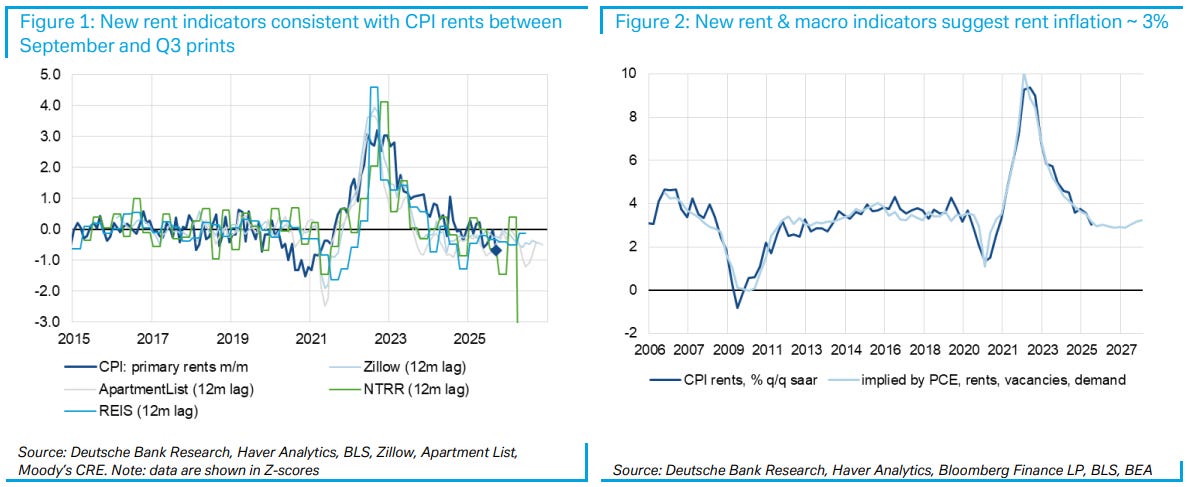

US rent inflation has been on a gradual downtrend since its peak of 8.8% y/y in March-23. Given its large weight (rent and OER together account for over 40% of core CPI), the gradual nature of the post-pandemic slowdown has been a key factor behind the observed stickiness in core inflation. Rental inflation has now normalized, with the 3m rate (3.0% annualized) back around historical averages in September, and the ongoing easing this year has offset upward pressures from other CPI categories such as core goods…

…Looking at a number of alternative new rent indicators shows recent trends indeed somewhat below pre-pandemic averages (Figure 1). With the notable exception of the NTRR - which is known to be prone to large revisions of the most recent observations for methodological reasons - they would seem consistent with monthly primary rent inflation somewhere between the September and Q3 prints (2.4%-3.0% annualised) going forward (Figure 1).

The transmission of falling new leases into CPI may however still be softened by a relatively high level of new rents relative to that of existing rents. As a result, a model based on both, a new rent indicator (the NTRR2 ) and a catch-up term (the ratio of new to existing rents), would imply CPI rents at ~2.8/2.9% y/y at the end of 2026, assuming new rents stay at their recent m/m trend going forward. Assuming new rents to begin reverting to their 2015-2019 average from the middle of next year and incorporating macro factors such as PCE and rental vacancy rates would point to rent inflation falling to 3% at the end of 2026 (assuming m/m rates between 0.24%-0.25% next year), before stabilising in 2027 (Figure 2). For overall core inflation, this slowdown may be enough to offset most of the upward pressure still in the pipeline from tariffs through the first half of 2026.

… AND this large German bank with it’s daily dose of stratEgery, commenting on 10s and the range …

…US Treasuries also had a mixed day yesterday. Yields initially moved lower as markets digested the Fed’s latest rate cut and reacted to messy set of weekly claims data. However that move reversed as the session went on, and 10yr yields (+0.9bps to 4.16%) inched higher late in the session after the Fed Board unanimously reappointed eleven Fed regional presidents to new five-year terms (Atlanta Fed President Bostic, who is retiring, was the lone exception). The regional presidents’ current terms expire in February so the advance announcement suggests that the Board was united in wanting to avoid the risk that the reappointment process raises questions over Fed independence.

At the front end, 2yr Treasury yields (+0.2bps) were little changed, with their rise limited by a decline in breakevens as the 2yr inflation swap fell -2.0bps to 2.43%, its lowest level since November 2024. That was in part due to oil prices declining to their lowest since October, with Brent crude down -1.49% to $61.28/bbl. The amount of Fed cuts priced by December 2026 stayed at 55bps (-0.4bps on the day), so still consistent with at least two cuts next year. Meanwhile, the recent dollar weakness continued, with the dollar index (-0.45%) hitting an eight-week low…

A(nothers)CPI and NFP precap for our dining and dancing pleasure …

We expect firmer core CPI inflation in October and November, 0.28% m/m on average (vs. 0.23% in Sep, 3.0% y/y Nov). Goods accelerate on higher cars inflation. Core services looks slightly firmer as shelter rebounds. Headline at 0.26% m/m (Oct/Nov avg), 3.0% y/y in Nov, Nov NSA Index: 325.102.

Exhibit 1: Core CPI inflation and contributions

December 12, 2025 MS US Economics: Employment Report Preview: A rising unemployment rate

Payrolls probably fell 30k in Oct and rose 50k in Nov. Private payrolls growth stabilizes, but federal gov’t jobs fall 100k in Oct. The UE rate rises to 4.6% in Nov from 4.4% in Sept, with flat LFPR. (Oct is not reported). AHE +0.3% in both months.

…We project payrolls fell in October because of the deferred resignations of federal employees and rose 50k in November.

The Federal Reserve Board of Governors unanimously reappointed the regional Fed presidents. This is normally an uneventful vote, and was scheduled for February. Early reappointment is not unprecedented. Markets have been concerned that regional presidents who disagreed with US President Trump’s monetary policy ideas might be pruned away in February. Whether a deliberately defensive maneuver or not, this action reduces concerns about central bank independence, and should lessen some risks around longer-dated bonds and mortgage interest rates.

Yesterday’s September US trade data demonstrates why the economist’s life is so hard. The export numbers were distorted by exceptional exports of non-monetary gold. Higher gold prices boost the value of exports, and gold trade has been complicated by US buyers’ concerns that it may be subject to tariff. Non-monetary gold is normally excluded from GDP calculations, so the trade position does not necessarily mean better US growth…

Trade deficit narrowing. GOOD NEWS! Not so fast …

December 11, 2025 Wells Fargo: Narrowing in Trade Deficit May Not Mean Big Boost for Q3 GDP

Summary The trade deficit narrowed sharply to -$52.8B in September. Most of the increase in exports was driven by non-monetary gold, which is largely excluded from GDP calculations. The upshot: trade is apt to be far less consequential to top-line growth than it was in the first half.

Finally, we’ve been warned …

Dec 11, 2025 Yardeni AI CALL: The TIME Curse & The Game of Thrones

“The Architects of AI” are this year’s TIME Person of the Year. We asked Google’s Gemini, “Can you list when the front cover of TIME featuring Person of the Year has turned out to be a curse?” Gemini responded as follows: “While TIME Magazine maintains that “Person of the Year” is a measure of influence (for better or worse) rather than an endorsement, the distinction is often lost on the public. Consequently, there is a recurring pattern known as the “TIME Cover Curse”—where recipients of the title suffer assassinated reputations, political downfalls, or literal death shortly after the issue hits newsstands.”

For example, Jeff Bezos was named Person of the Year at the end of 1999, at the peak of the dot-com bubble. Within 18 months, the bubble burst, and Amazon’s stock lost over 90% of its value (though he obviously recovered in the long run).

Here’s another example: Elon Musk capped a massive year for Tesla and SpaceX by winning the title at the end of 2021. The following year was disastrous for him: he bought Twitter (now X), his personal reputation took a severe hit, and he became the first person in history to lose $200 billion in net worth.

We have been warned.

For somewhat MOAR on THE CURSE, I’d highly recommend a quick point / click over to LinkedIN for Jim Bianco’s take HERE

… By the time they are recognized for their actions, some form of mean reversion usually occurs the following year….

… and if leaders lead. Lower. I’d imagine economy follows. Rate cuts. Yields. We’ve seen this movie before …

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

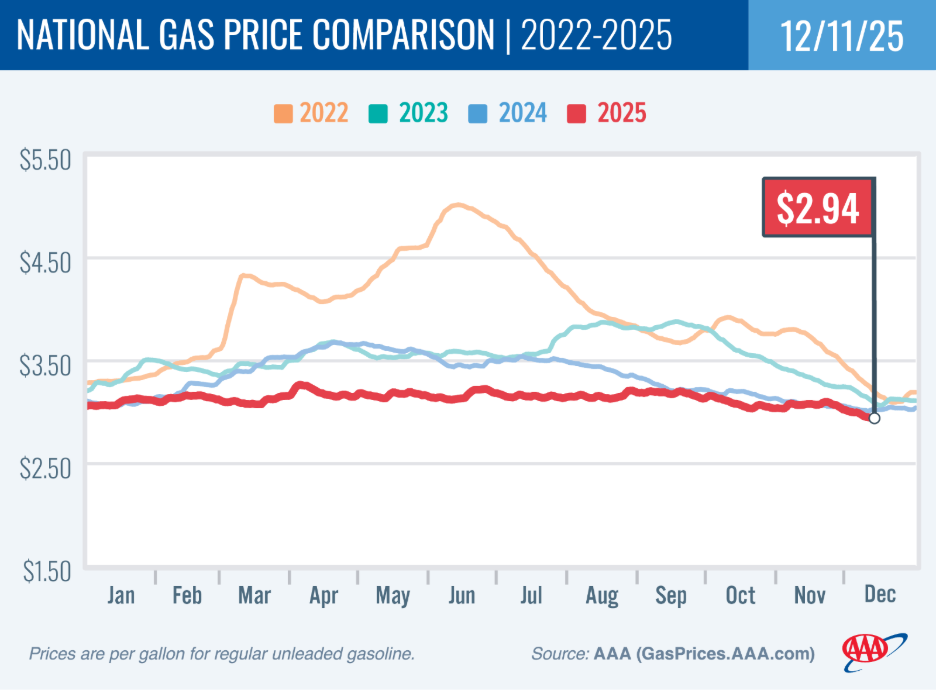

Good news (except for the drop in temps) …

December 11,2025 AAA: Outside the Snow is Falling ... and so are Gas Prices

WASHINGTON, DC (December 11, 2025) – The holiday season is delivering a gift for drivers as the national average dropped 5 cents since last week to $2.94. Gas prices are the lowest they’ve been in four years. The national average has stayed below the $3 mark since hitting $2.99 on December 2. As a record number of travelers prepare to hit the road later this month, they’ll be paying less than they were last holiday season when the national average was $3.04 to close out 2024.

Charts. I like them. Here’s one for us on the outside lookin’ in … the poor man’s long bond (ie TYX — whatever it is)…

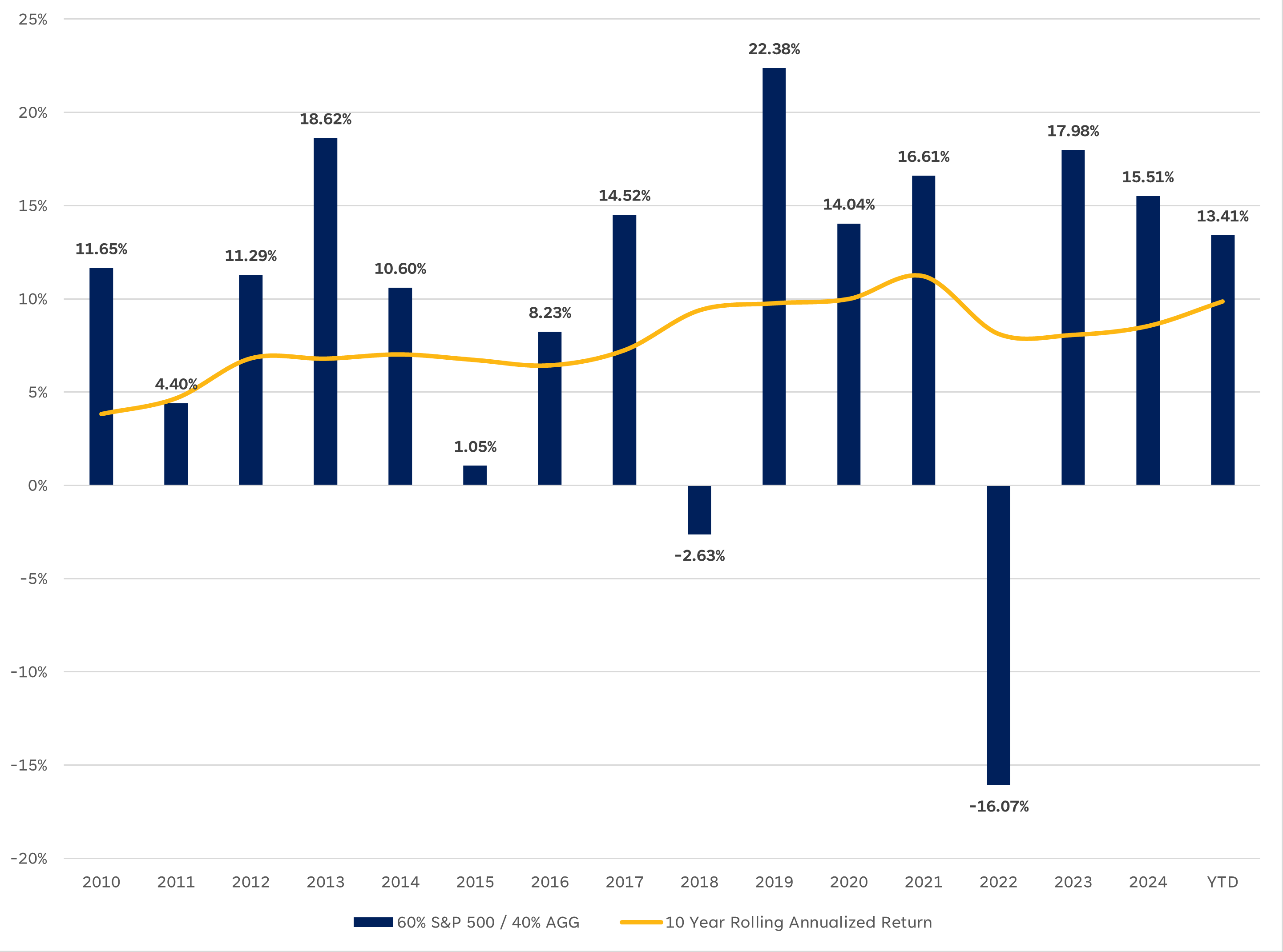

December 11, 2025 LPL: Is the 60/40 Portfolio Still Relevant? Exploring Alternatives

Origin With 12 trading days remaining in 2025, we wanted to revisit one of the most popular investment strategies that has broadly served investors well over the last few decades — the 60/40 portfolio. Pioneered by Harry Markowitz and his modern portfolio theory (MPT) framework in the 1950s, the 60/40 portfolio — comprised of 60% stocks and 40% bonds — argued that diversification among uncorrelated asset classes provided the investor with the most optimal portfolio allocation. Equities served as the growth engine, while bonds provided drawdown mitigation and predictable income; when combined, they should produce higher returns than stand-alone bonds and better risk-adjusted returns than stocks. The key to this strategy is the relationship between stocks and bonds — the two asset classes need to have less than perfect correlation, or better yet, be negatively correlated. In the latter scenario, this meant that if stocks were to fall, bonds would rise, limiting the overall drawdown and volatility experienced in a portfolio…

…60/40 Portfolio Still Delivering, Though Diversification Benefits Have Weakened Annual return of a hypothetical 60% S&P 500/40% AGG portfolio since 2010 with 3-year, 5-year, and 10-year annualized rolling returns

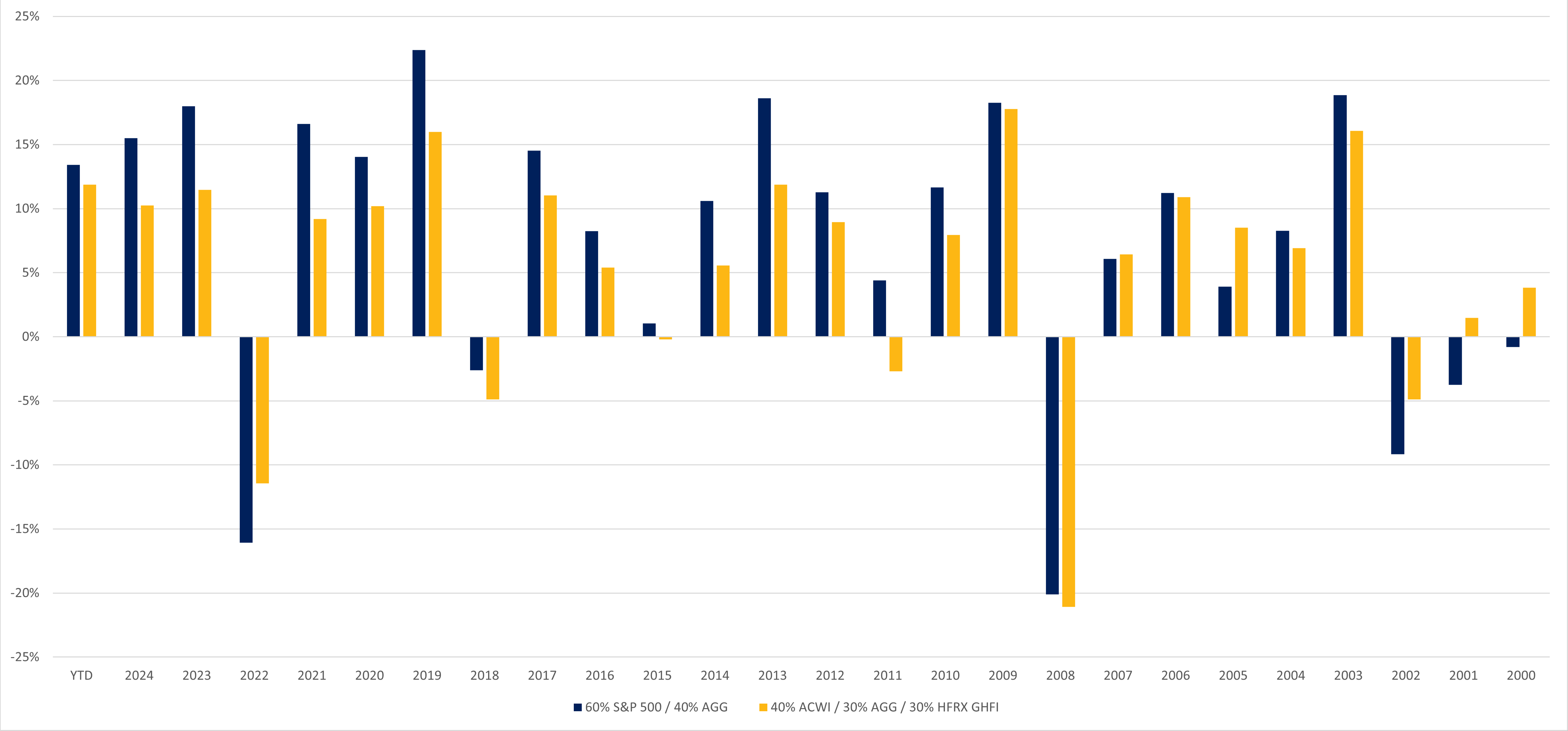

…From Tradition to Innovation: The Evolved 60/40 Portfolio Annual returns since 2000 of hypothetical 60% S&P 500/40% AGG and 40% ACWI/30% AGG/30% HFRX Global Hedge Fund Index (GHFI) portfolios

Conclusion While the two components of the traditional 60/40 portfolio — stocks and bonds — have become more correlated in recent years, dampening their once-historical diversification benefit, this investment strategy still has merit today, especially once including international equities, as it emphasizes the need to spread investment risk and returns across less than perfectly correlated asset classes. As more diversifying asset classes come to market and proliferate, investors should consider the lesson Markowitz introduced nearly 70 years ago — that true portfolio resilience comes from broad diversification across multiple sources of return.

AND against narrative of falterning labor mkt (something alluded to by JPOW at presser and we’ll learn more next week) …

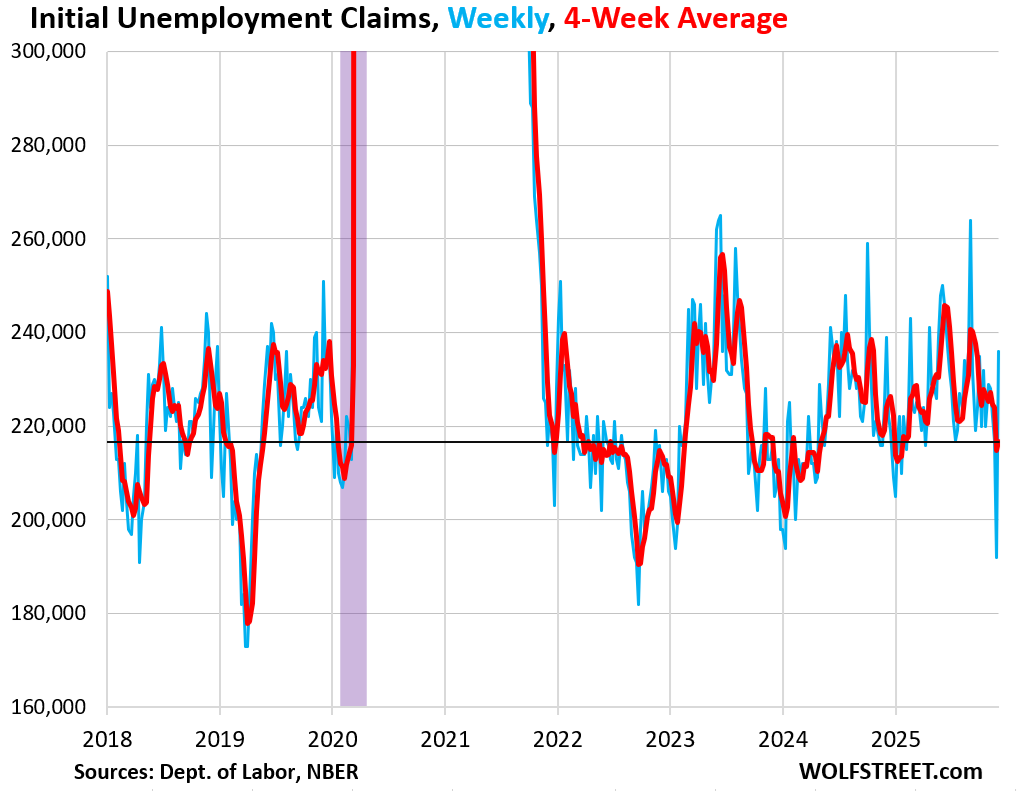

Dec 11, 2025 WolfST: Layoffs Show No Signs of a Weakening Labor Market If the labor market is weakening, it’s on the job-creation side of the equation, maybe in part due to AI.

…Which is why we look at the four-week average, which largely irons out the week-to-week squiggles, and which ticked up to 216,750, seasonally adjusted, which is historically low, and in the same low range that it has been in for the past four years.

…This is administrative data, not survey-based data. Freshly laid-off people filed these applications for unemployment insurance at state unemployment agencies, which then reported them to the US Department of Labor by the weekly deadline, which then combined the data and published it today.

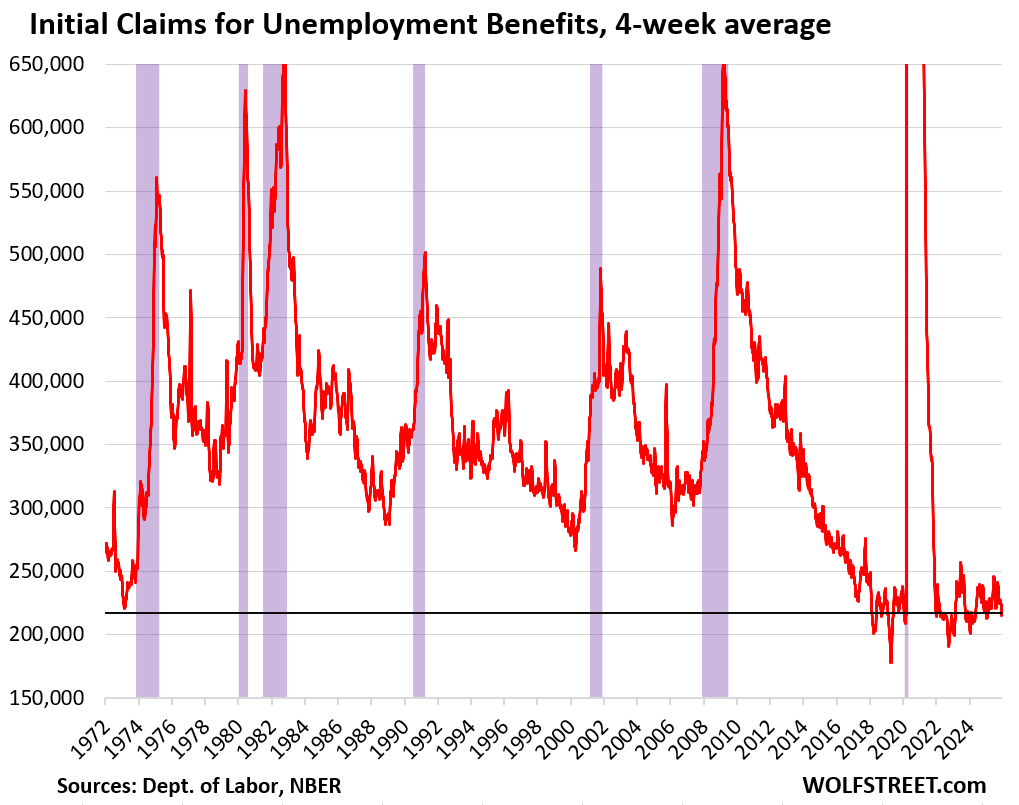

In a longer timespan going back to the 1970s, initial claims are very low, despite the growth of nonfarm payrolls over the decades. They were lower only during the tight labor market of 2018 and 2019 and during the labor shortages coming out of the pandemic.

Layoffs show no signs of a weakening labor market. If the labor market is weakening, it’s on the job-creation side of the equation.

We have also consistently seen that churn in the labor market has calmed down dramatically from the pandemic spike, with relatively few people quitting, with retirements being down, with layoffs & discharges being relatively low. As fewer people are leaving their jobs, they leave fewer job openings behind, and fewer people need to be hired to fill those newly opened jobs. While job openings remain relatively high – they’re at the level of the peak before the pandemic – there is a lot less turnover in the labor market, so it’s harder for people who are out of job to find a job, all discussed here.

This greater difficulty for laid-off people to find a job, and to spend more time looking for a job, shows up in the continued claims for unemployment insurance – but even those have improved recently…

AND given Time Person of the year, figured I’d use ChatGPT to help …

AND… THAT is all for now. Off to the day job…HOPEFULLY back over weekend!

Not an original idea, but getting the suspisious feeling AI is nothing but 'man behind the curtain' pulling the levers it believes we desire, thanks for experimenting. I have an AI phobia afraid I'll be more Dumbed Down; yes same was said for the Calculator, and Aristotle feared written language would cause man to lose our storytelling abilities.

Not an original idea, but getting the suspisious feeling AI is nothing but 'man behind the curtain' pulling the levers it believes we desire, thanks for experimenting. I have an AI phobia afraid I'll be more Dumbed Down; yes same was said for the Calculator, and Aristotle feared written language would cause man to lose our storytelling abilities.

This note is Never too long many thanks👌