ZH: Tariff Tantrum 2.0 Sends Stocks & Bonds Lower; Oil & The Dollar Surge

… oh, ok so … nothing NEW, then.

Biz as usual.

I know one thing I didn’t miss — latest from Dr. Hunt (still being drafted?) … And so, without further adieu, an updated look to 3yy after yesterdays selloff and ahead of this afternoons $58bb of fresh supply …

3yy: RANGE 4.05 - 3.65 makes middle to be about 3.85% which is ‘bout where we are here / now …

… NOW here’s where it gets interesting … in the move somewhat higher, momentum (stochastics) have become overSOLD on daily … dare we think dipORtunity …

… if only tariffs weren’t inflationary … no, wait, deflationary … no, wait, if only they weren’t impacting the equity markets AND bond markets negatively … hey, at least we’ve got the OBBBA which, depending on what / who you believe, will make the economy so strong it then … doesn’t need rate cuts … no, wait, we want and NEED rate cuts …

If yer NOT a touch confused, yer NOT payin’ attention … Clearly an extra day off wasn’t enough…

In OTHER news this morning from Bill Dunkleberg’s operation …

July 8, 2025 NFIB SURVEY: Small Business Optimism Remains Steady in June Taxes remain small business owners’ single most important problem

The NFIB Small Business Optimism Index remained steady in June, edging down 0.2 of a point to 98.6, slightly above the 51-year average of 98. A substantial increase in respondents reporting excess inventories contributed the most to the decline in the index. The Uncertainty Index decreased by five points from May to 89. Nineteen percent of small business owners reported taxes as their single most important problem, up one point from May and ranking as the top problem again. The last time taxes reached 19 percent was in July 2021.

“Small business optimism remained steady in June while uncertainty fell,” said NFIB Chief Economist Bill Dunkelberg. “Taxes remain the top issue on Main Street, but many others are still concerned about labor quality and high labor costs.”

Key findings include:

A net negative 5% (seasonally adjusted) of owners viewed current inventory stocks as “too low” in June, down six points from May. This signals a net increase in inventories, with 7% reporting inventories “too low” in June compared to 8% in May. Twelve percent reported current inventories “too high” in June compared to 7% in May. This component contributed the most to the Optimism Index’s decline.

The net percent of owners expecting better business conditions fell three points from May to a net 22% (seasonally adjusted). Historically, this is still a positive reading with the 51-year average at a net 3%.

The net percent of owners expecting higher real sales volumes fell three points from May to a net 7% (seasonally adjusted).

Twenty-one percent (seasonally adjusted) plan capital outlays in the next six months, down one point from May.

The percent of small business owners reporting labor quality as the single most important problem for business remained at 16%, unchanged from May. The last time complaints about labor quality fell below 16% was in April 2020. Fewer small business owners reporting labor as their top problem aligns with other data suggesting a more tempered labor market economy-wide.

Eleven percent of owners reported that inflation was their single most important problem in operating their business (higher input costs), down three points from May and the lowest reading since September 2021. Inflation pressures continue to ease on Main Street.

The data on overall health of respondents’ business showed substantial deterioration, with declines in the percentages reporting their business was in excellent or good health. When asked to rate the overall health of their business, 8% reported excellent (down six points), and 49% reported good (down six points). Thirty-five percent reported the health of their business was fair (up seven points), and 7% reported poor (up three points).

Full surve HEREfor more but for now, I’ll hustle out the way allow YOU to prepare P&L / balance sheets for this weeks onslaught of duration supply

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT USTs edged modestly lower overnight before the RBA's surprise ‘hold’ decision injected a late stir into the market, pushing core duration lower just as the Asia session wound down. In LDN, a more active environment was cited, our desk seeing flattening reverse in favor of bear-steepening. 5s30s trading briefly above 98 amid better buying from RM in intermediates and some mixed flows in the back end of the curve. Liquidity was seen as a touch thinner heading into the NY open, with some light dip-buying seen fading the extremes of the LDN session. SPX futures are showing +0.1% here at 7am, DAX +0.6%, Crude -0.2%, Gold -0.4%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Constructive risk environment focusing on tariff extension to August 1st; AUD outperforms on unexpected hold … USTs saw a slightly softer start to the day, given the constructive risk tone. Similar story for EGBs and Gilts, though the magnitude of downside has increased throughout the morning, USTs to a 110-25+ trough, taking out Monday’s 110-29 base and now teetering just above 110-25, the WTD low from the last week of June.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ as they come hat-in-hand for your vote in the Extel survey … All here time / date stamped to best of my abilities given I was outta pocket yest (Monday) …

… If the letters to Japan and South Korea are any indication of what’s to come, it appears that Trump has given the US’s key trading partners another three weeks before returning to the ‘Liberation Day’ tariff levels.

It's unclear how the market will react to such an eventuality. On one level, the sharp selloff in equities and subsequent rise in recessionary angst that followed Liberation Day ‘should’ serve as an archetype for the market’s response. However, Trump has already demonstrated a willingness to pause (and pause again), which begs the question whether we’re entering the season of the pause, or if August 1 is truly the deadline.

We’re cautious against over-interpreting the bear steepener – primarily because of this week’s 10- and 30-year auctions and the implied need for a meaningful concession. The solid employment report has the Fed on-hold at least until the September meeting and with the debt ceiling resolved for the time being, there is upside potential for forward supply – at least in the bills market. The next few weeks will be an important litmus test of the demand for bills given the prevailing macro narrative and the Fed’s extended period on hold. We’re not anticipating any dislocations resulting from the ramp up in front-end borrowing, even if the market will be watching this week’s auctions, yet again, for any indication of a buyers’ strike. The fresh tariff delays will likely support ongoing participation by overseas participants…

We reduce our year-end Brent price target by USD5/bbl to USD55/bbl on more resilient supply from US shale and Iran versus our previous forecast

US shale producers have taken the high crude prices (WTI topped USD75/bbl) as an opportunity to hedge more of their supply, making them less sensitive to lower prices.

Further, with some sort of equilibrium between Iran and the US/Israel, we expect the US sanctions on Iranian crude to remain but for implementation to be weaker than previously assumed.

We expect crude to recover after Q126 as supply growth (both from OPEC+ and non-OPEC) moderates, mitigating the risk of excessive length. We target USD70/bbl by end-2026.

An early morning read / catchup on what I missed as well as day ahead …

… A reminder that yesterday we released 2025's version of "Charts to make you go “WOW!” (link here). Perhaps not every chart will leave you speechless, but we tried to include plenty that offer a fresh perspective—either by taking a longer-term view or by framing current themes in a slightly different light. I'll be hosting a webinar on the pack on Thursday at 2pm London time (9am NY time). To register please click here…

…A quiet day where we were all waiting for tariff news sprung into life just after Europe closed yesterday as the first major tariff news of the week broke. In a series of posts on social media, President Trump announced new tariff rates on several trading partners. He started off by announcing 25% tariff rates against Japan and South Korea, effective August 1st. This was followed by “trade letters” to a further twelve countries including South Africa (30% rate), Malaysia (25%), and Indonesia (32%). President Trump also said that “any goods transshipped to evade a higher tariff will be subject to that higher tariff,” while noting that these would be separate from the sectoral tariffs. The headline rates for most countries announced yesterday were around the same levels as the Liberation Day tariffs, but President Trump also said that if countries were to raise their tariffs in response, then “whatever number” they choose will be added onto the 25% charged by the US.

White House Press Secretary Leavitt announced that more letters will be arriving throughout the week. After sending the posts, the President signed an executive order that effectively delays the new tariff rates until August 1, prolonging the current 10% tariff rate and giving nations more time to meet the trade demands from the White House. The President continued to signal he was open to deals, saying the August 1st deadline was “not 100% firm” and that they could “maybe adjust a little bit, depending.” Overnight, Politico reported that while a US-EU trade deal had not been finalised, the US had offered the EU a 10% tariff rate with caveats. Given the higher rates seen earlier in the day for other trading partners, the EUR has rallied (+0.32%) overnight and is back to levels before the letters started rolling out yesterday.

Stocks fell in response to the tariff news, although the S&P 500, which closed -0.79%, was already -0.6% just before the announcement in anticipation of the noon Washington timeline that had been given over the weekend with regards to letters being sent out. The index was down -1.25% at the lows of the day, before rebounding as investors priced in the possibility of trade deals getting over the line for larger trading partners before putative tariffs kick in…

… As a visual learner, am always a fan of charts and so, here are some from one of Global Wall’s favs …

… Not every chart may leave you speechless, but we’ve aimed to include plenty that offer a fresh perspective—either by taking a longer-term view or by framing current themes in a slightly different light.

One standout section shows why this has been the worst decade on record for government bonds across many metrics, and why concerns over US debt sustainability are rising. On the other side of the Atlantic, we’ve now hit the 100-year anniversary of the last time Italy recorded a budget surplus. An astonishing stat, but at the moment, France (which last posted a surplus in 1974) is the bigger risk.

In the US, inequality remains extremely high—though it’s more evident in equities than housing. Still, it’s striking that more Americans aged 70 and above are buying homes than those under 35. Surely this can’t be sustainable?…

…Oil is one of the many commodities that struggle to out-pace inflation over the very long-run even if there are long periods of deviation from the trend… Oil is now pretty much at its long-term average in real terms…

…The worst decade ever for Government bonds? On a 5 or 10yr basis this has been the worst period on record for nominal 10yr UST returns…. In real terms it hasn’t been quite as bad as the 1970s or post the inflation seen after WWI….

…After the terrible decade,10yr US Treasury yields are now slightly beneath their long-term average yield since 1800… at least some value has returned...

…30yr US yields look high in the 20 years of the TIPS market but are only just above average when we create a proxy over the last 70 years… Are investors putting a lot of faith in long-term inflation trends that as we see on the following page aren’t justified?

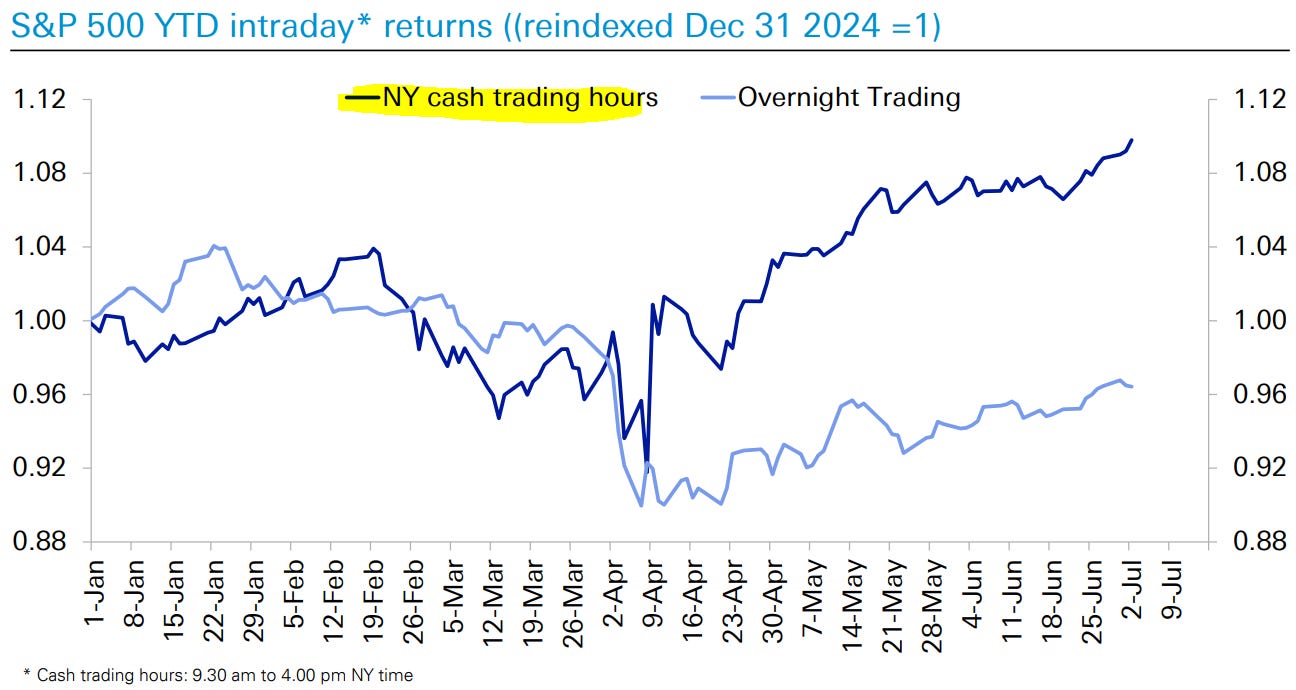

…Most of the post Liberation Day gains in the S&P 500 have occurred in US trading hours suggesting a predominantly domestic buy-in to the US story while the RoW sits more on the sidelines… for more see Parag Thatte’s piece here Investor Positioning and Flows: Waiting For Substantive Trade R

… with these WOWZA charts in mind, a few others more economically driven …

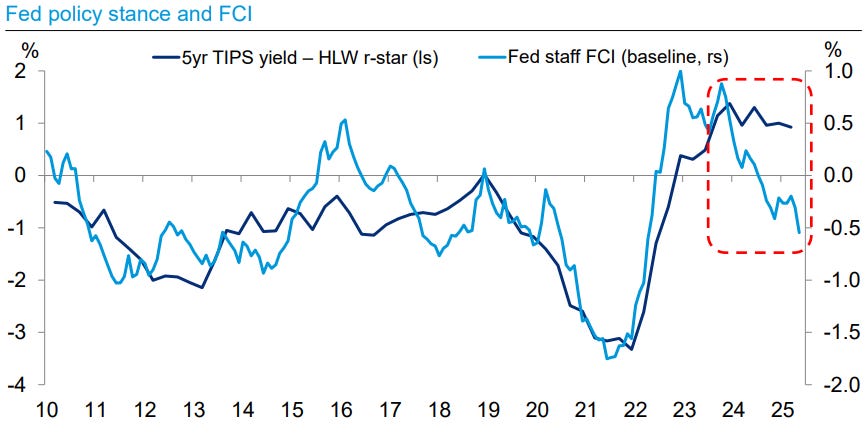

…Fed: Are cuts still coming? …How restrictive is policy? Depends on the measure of r-star

Loose financial conditions indicate that R-star is likely higher

…DB Fed forecast versus alternatives – we are modestly more hawkish

DB identification of the 2025 dots in the June SEP

German stratEgersisms working overtime these past few days (completely coincidental the Extel survey open, amIright?) and another from the this shop on IF we could get some sorta summer dipORtunity …

08 July 2025 DB Mapping Markets: Could we get a summer crisis again in 2025?

… With the height of summer approaching, market speculation is rising about a fresh bout of turmoil. After all, Q3 historically sees the biggest spike in the VIX, liquidity is thin, and many historic crises have begun in the late-summer period.

Could 2025 bring another upset? Several contenders spring to mind. There’s the threat of reciprocal tariffs on August 1. We could start to see the inflationary impact of tariffs, which could see markets price out the rate cuts they’re expecting. There’s ongoing concern about fiscal policy. And of course, there’s the unknown factors (like the yen carry trade unwind in 2024) that we haven’t even considered.

But markets have been remarkably resilient this year. The macro fundamentals remain strong, and policymakers have consistently adjusted policy in response to market turmoil. So market dynamics are acting as a constraint on policy and, as long as that remains the case, it would take a bigger shock that policy can’t fix to cause long-lasting market turmoil.

Q3 has historically seen the biggest upward move in the VIX index on average (pts change by quarter)

So what are some of the summer crises of recent years?

2024 – A weak US jobs report sparks turmoil as the yen carry trade unwinds

2022 – Markets slump as central banks dial up the hawkish rhetoric, and European gas prices spike

2015 – The Euro crisis resurfaces in Greece alongside an equity sell-off in China

2011 – US embroiled in debt ceiling crisis, whilst Euro Crisis deteriorates

2008: The GFC moves into its most critical phase

2007: The first signs of the GFC become evident

So what could trigger a fresh bout of turmoil in 2025?

1. US tariffs snap back higher on August 1.1. US tariffs snap back higher on August 1.

2. The inflationary impact of the existing tariffs becomes obvious, causing markets to price out rate cuts.

3. The resilience of growth starts to falter, raising fresh speculation about a recession like last summer

4. Fiscal fears flare up again.

With public debt levels historically high, this is a perennial fear currently. Several countries have already faced a spike in bond yields this year, including the US in May after the credit rating downgrade by Moody’s, and the UK last week after there was speculation about Chancellor Reeves’ position and whether the fiscal rules would be eased. That followed on from previous jitters in early January.

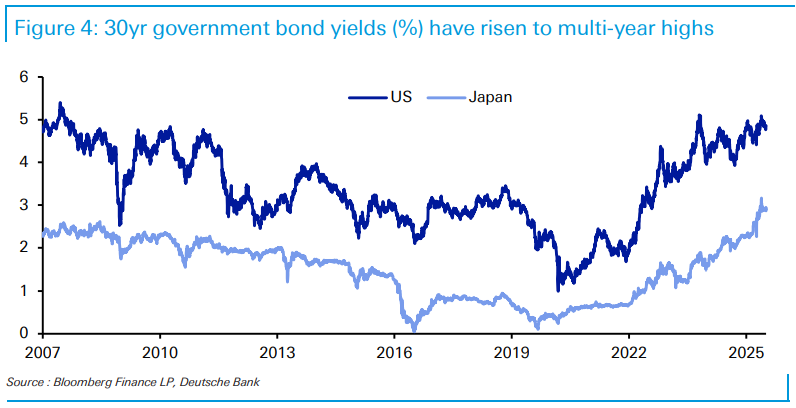

In both cases, an unexpected trigger caused issues, but it played into preexisting concerns about high deficit levels. This is occurring at a time when we’ve already seen concerns over France’s deficit following their elections last year, when Germany is pursuing a large fiscal stimulus, and Japan’s 30yr yield is trading above 3%

The problem with fiscal concerns is market dynamics can become selffulfilling. If bond yields start to rise, that raises doubts about debt sustainability, which can trigger a further rise in bond yields. Indeed, this is very much what happened in the summer of 2011, and Q3 that year saw the spread of Italian 10yr yields over bunds rise from 186bps to 365bps.

5. A geopolitical shock causes a significant oil price spike.

…But markets have been incredibly resilient this year, so can anything knock them off course? There’s a couple of important reasons behind the market resilience this year:

1. None of the shocks so far have created a durable change in the macro fundamentals.

2. Policymakers have shown a consistent willingness to adjust policy in response to market turmoil…

Same German institution offering an update on earnings in an asset allocation package …

07 July 2025 DB: Asset Allocation - Q2 Earnings: Looking For A Slight Deceleration Amidst Tariff Fog

With macro growth forecasts up slightly (+), the dollar drag diminishing sharply (+) but oil prices also down steeply (-), on net the top-down drivers suggest solid earnings growth, picking up modestly (from 8.7% yoy in Q1 to 9.6% in Q2).

But we expect a drag (-2%) from the idiosyncratic effects of tariffs, not picked up entirely by macro models. We look at several ways to identify the industries most impacted. Those seeing: the biggest downgrades; the sharpest declines in earnings growth; large disconnects between macro-implied and Q2 bottom-up analyst consensus; and large dispersion or uncertainty in analyst estimates.

Combining the growth implied by top-down drivers (+9.6%) with idiosyncratic tariff impacts (-2%) points to Q2 earnings growth of 7.6%, a slight deceleration from Q1 at 8.7%. Q2 consensus has stabilized in recent weeks but calls for a sharper slowing in earnings growth than what we foresee, setting up for beats near historical average rates (5%).

Will we get the typical earnings season rally? There is a long-standing pattern of equities rallying through the earnings season, about three-fourths of the time, with a median gain of 2%. The magnitude of gains was tied inversely to positioning going in, which at slightly below neutral this time, is supportive of another rally.

Upon further review, the data was …

July 7, 2025 First Trust: Monday Morning Outlook - Not So Hot

In the immediate aftermath of Friday’s much anticipated Employment Report it seemed like the judgement from analysts, talking heads, and even markets was unanimous (or nearly so) that there was good news to celebrate.

Superficially, it’s not hard to see why that view of the report quickly became the conventional wisdom. Payrolls rose a respectable 147,000 in June and were revised up 16,000 in prior months, outstripping the consensus expected 106,000. At the same time, the unemployment rate, which the consensus expected to tick up slightly to 4.3% (from a prior 4.2%) instead ticked down to 4.1%…

…Why aren’t we in the cheerleading chorus? Because private payrolls were up only 74,000 in June and were revised down 16,000 for prior months, bringing the net gain to a tepid 58,000. In other words, the overall payroll gain in June itself was roughly half due to government and all of the upward revisions in prior months were due to the government, as well. Long term, more government jobs are not a sign of a healthy economy nor are they going to make it healthier in the future…

… We think Powell may be letting politics cloud his judgement, which is why we like Trump’s apparent plan to name Powell’s successor well in advance of the end of Powell’s tenure as chairman next spring. That way Powell will remain on the job, but the public and investors can also listen to how the next chairman (as well as some current Fed members who disagree with Powell) will handle the same economic situations.

The economy is not in recession yet, but markets are not pricing in enough of a risk of a recession in the year ahead.

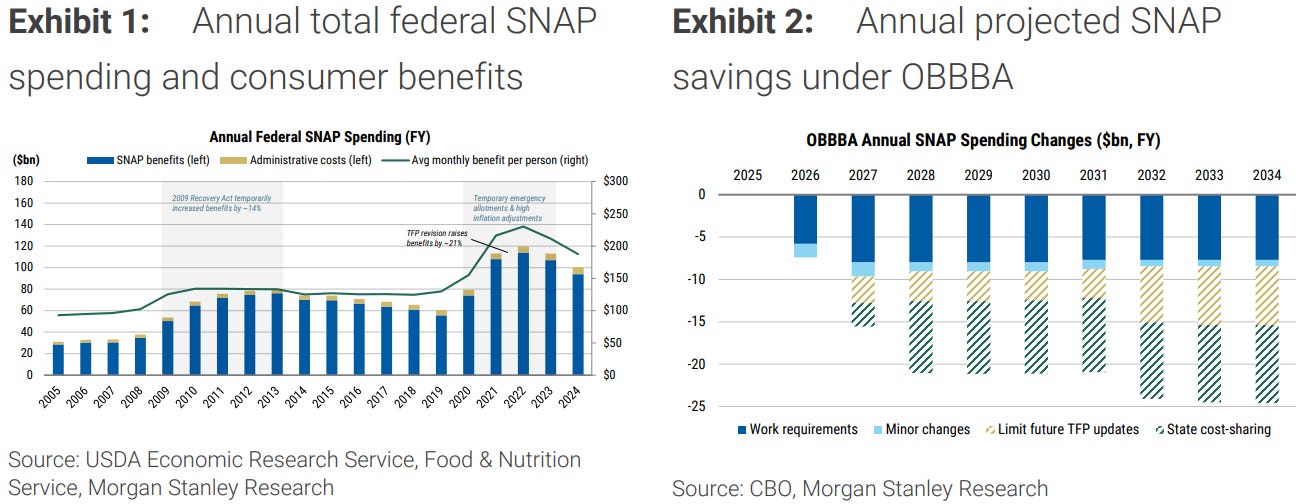

OBBBA impact on consumption from the bottom UP perspective …

July 7, 2025 MS: US Consumer: Implications of SNAP Cuts in the Final OBBBA

Key takeaways

The US has enacted the One Big Beautiful Bill Act (OBBBA) containing smaller SNAP cuts ($185bn over 10Y) than initially proposed by the House ($300bn).

We expect $9bn of incremental cuts in 2026, mostly from work requirements, which represents ~60 bps of annual food-at-home spend.

We estimate a ~20-bp headwind to food-at-home spend in 2026 (and ~400 bps in aggregate through 2035) given historical inelasticity of food demand.

We estimate a 25-42 bp headwind to US CSD spend in 2026 and 32-62 bps on average per year through 2035.

Same shop with a review of tariff impacts on Asian economies …

July 7, 2025 MS: Trade Tensions As We Approach Deal Deadlines

The rhetoric around tariffs has risen. While we may get more details as the week progresses, our core view remains: uncertainty will likely persist, weighing on corporate confidence, capex and the trade cycle.

Key takeaways

Only Vietnam has secured an agreement so far; the outcomes of other negotiations remain unclear.

Deals may be completed before August 1; tariffs could rise tactically before a deal is done; tariff rates may be set unilaterally by the US.

We still see challenges in reaching a comprehensive deal for US-China. An added challenge will be the issue around transshipments.

Moreover, sectoral tariffs for pharma and semis may be forthcoming.

Bottom line: Trade uncertainty to likely persist for longer. We expect high-frequency data points to reflect damage to the growth cycle in the next 2-3 months.

Tariffs postponed then unpostponed but tariffed … AND new TAXES arrive as other tax breaks set to sunset are extended (and whats this — econ data that is REPUBLICAN biased?) …

One more time: tariff discussions continue This afternoon, President Trump signed an executive order delaying the implementation of the reciprocal tariffs, originally postponed to July 9, to August 1 (link to the order here). Previously, the 90-day pause on the country-specific reciprocal tariffs announced in early April was due to expire on Wednesday.

Separately, the White House released letters today to the leaders of a dozen countries assigning reciprocal tariff rates now due to take effect August 1. The language was nearly identical from letter to letter (see below for the letter sent to President Cyril Ramaphosa of South Africa). Most of the new rates announced today were close to those announced in early April. It is unclear why those nations were selected from the 57 facing higher tariffs snapping into place this week. Secretary Leavitt said in the press conference (link here), "That's the President's prerogative and those are the countries he chose." Reuters reported today that the EU would not receive a letter setting out a reciprocal tariff rate (link here), which is noteworthy because of the size of the trading relationship.

Among other large trading partners, the President announced that Japan and South Korea would each be charged tariffs of 25%. Japan faces a reciprocal rate 1 pp higher than the 24% announced April 2, and South Korea faces the same rate as originally announced April 2. For the larger trading partners we show the April 2, so-called Annex 1 rates (link here), in the table below compared to the new rates announced in the letters released today…

US President Trump announced the start of a new wave of taxes on US consumers, with a 25% tax on US citizens who want to buy products from South Korea and Japan. Other countries’ exports also received higher tax rates, but it seems a wasted effort to analyze every Trump social media post when investors understandably anticipate future retreats. Japan and South Korea accounted for around 8.5% of US imports last year, so this tax increase adds 0.1 to 0.2 percentage points to consumer price inflation.

The June US NFIB survey of small businesses is due. Traditionally, this is Republican biased. Republican consumer confidence improved in June. The comparison might be interesting. The New York Fed one-year inflation expectations will be distorted by political polarization.

US consumer credit is not especially noteworthy at the moment, but may become more important. As real incomes start to decline, consumers are likely to use savings and credit to temporarily support spending.

This time NEXT week we’ll be preparing for CPI and so, here’s a pre-cap …

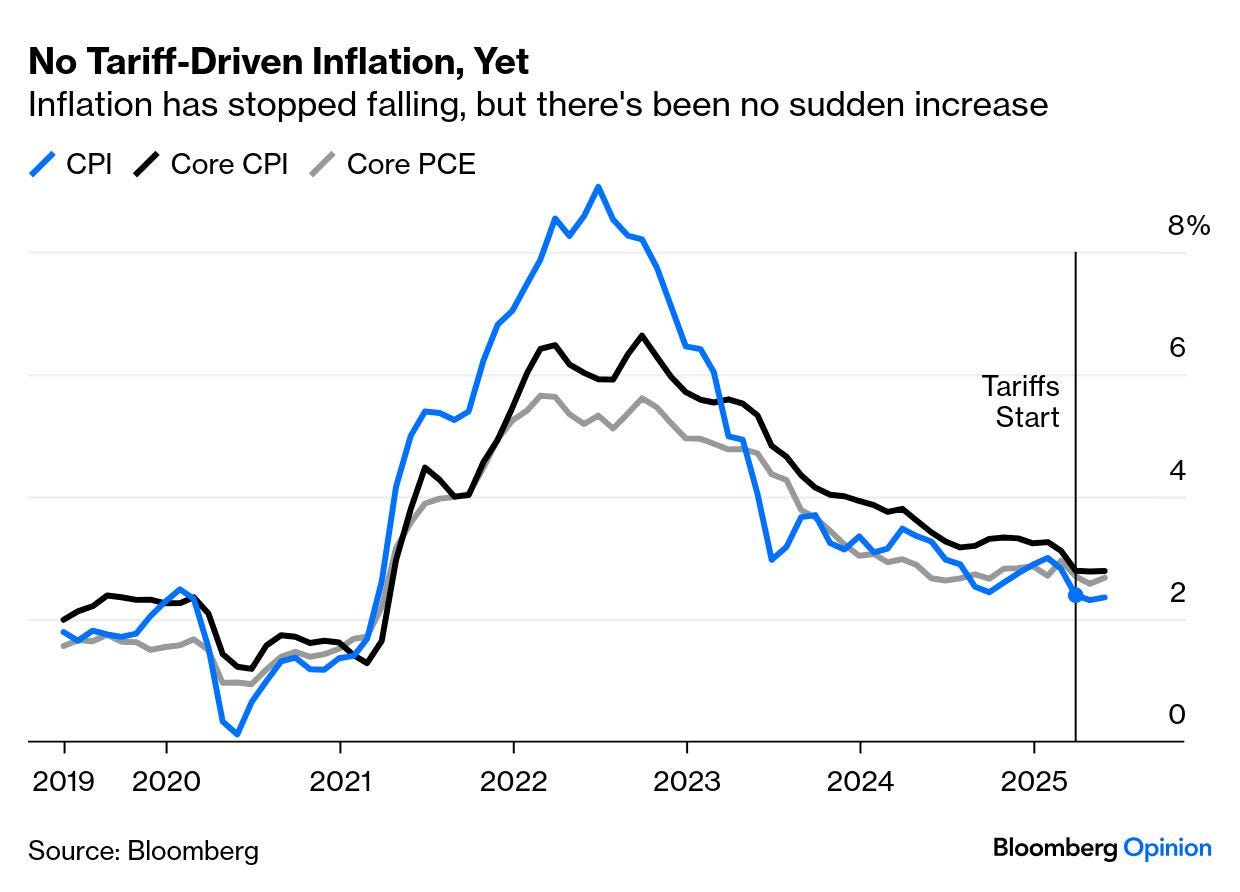

Summary The June CPI report is likely to show inflation beginning to strengthen again, albeit not enough to alarm Fed officials at this juncture. We expect the headline CPI to rise 0.25% in June, which would nudge the year-ago rate up to 2.6%. Excluding food and energy, we anticipate the core CPI to increase 0.24% and view the risks skewed more to an upside surprise of 0.3% versus another downside surprise of 0.1%. If our forecast is realized, the 3-month and 12-month annualized rates of core CPI would strengthen to 2.4% and 2.9%, respectively.

The next three months will mark a key stretch of inflation data. While inventory frontrunning has mitigated the need to raise goods prices, it will become increasingly difficult for businesses to absorb higher import duties as pre-tariff stockpiles dwindle. We expect core goods prices to pick up further in the second half of the year as a result, but look for the pass-through to be limited by growing consumer fatigue. Amid a softer labor market and services inflation dissipating a bit more, the pickup in core inflation stemming from tariffs is likely to look more like a bump than a spike.

Finally, Dr BOND vigilante with an annotated chart of … stocks …

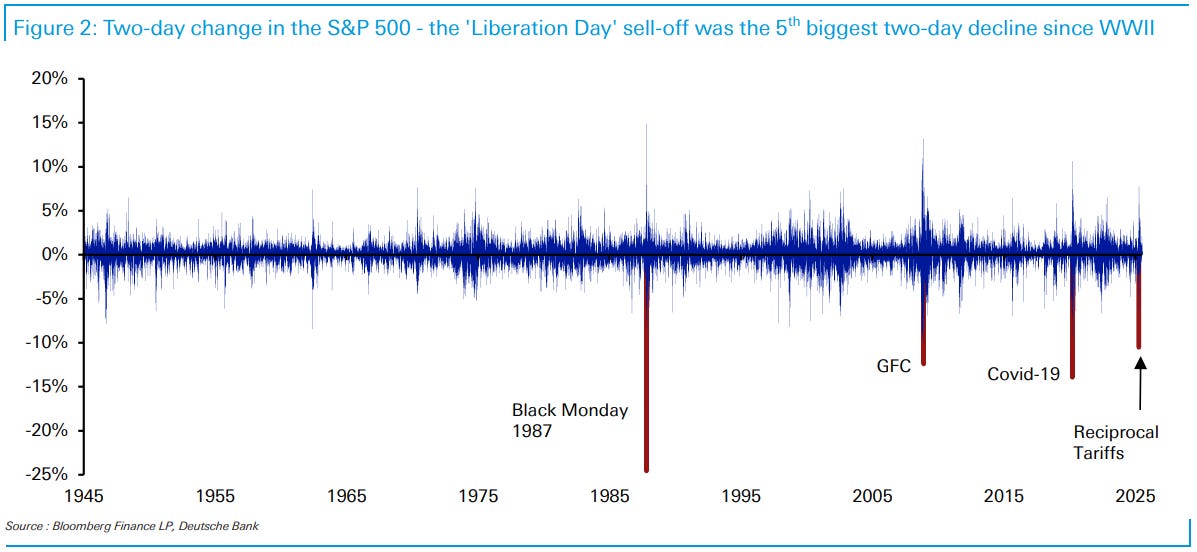

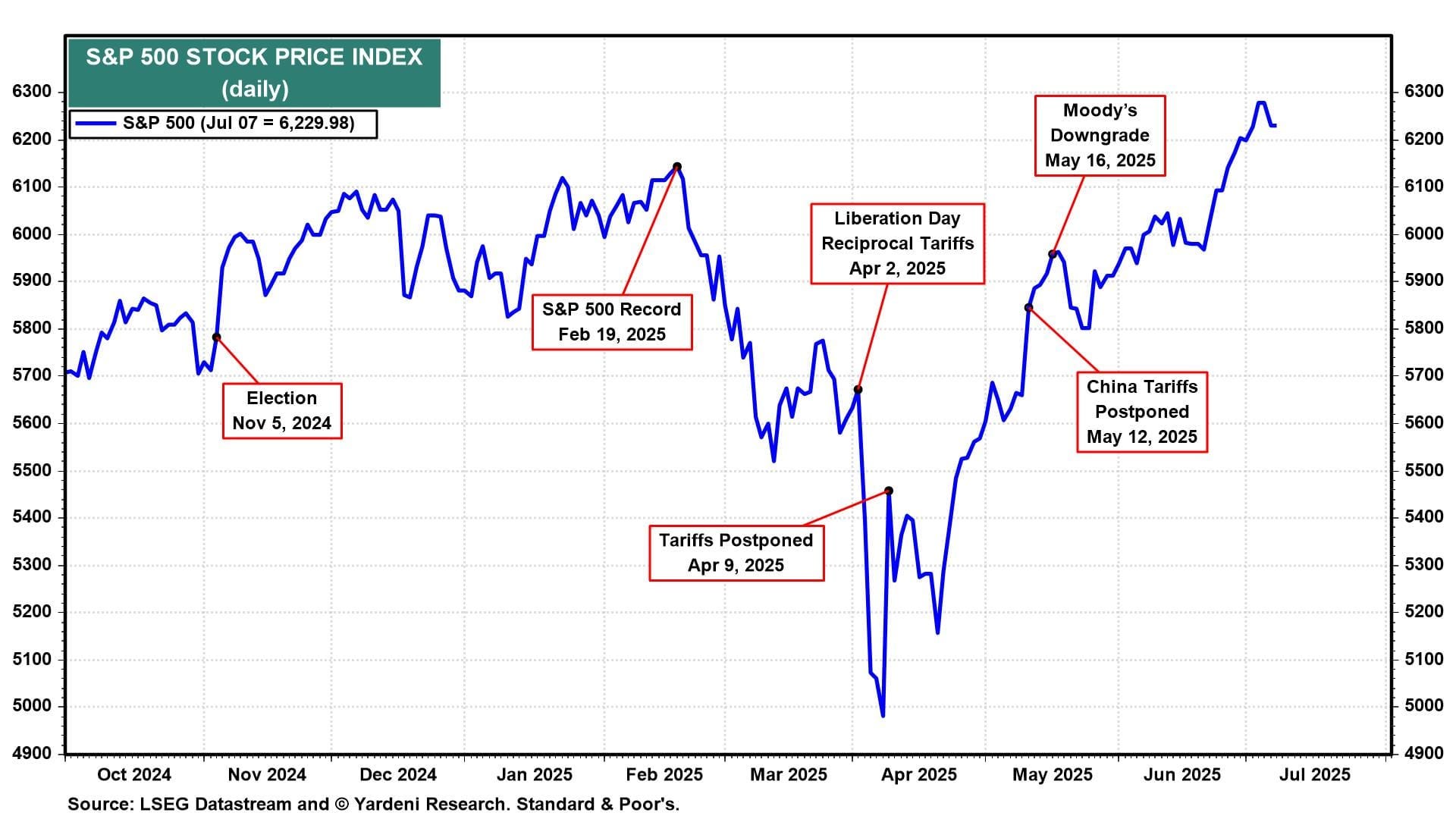

Liberation Day I occurred on Wednesday, April 2 after the stock market closed, when President Donald Trump imposed reciprocal tariffs on America's trading partners. The immediate reaction was what we called "Annihilation Days" in the stock and bond markets until April 9, when Liberation Day I was postponed until July 9 (chart). Today, Trump announced reciprocal tariffs again on 14 countries. Their governments have until August 1 to respond before the tariffs are imposed. This time, the initial reactions of the stock and bond markets to Liberation Day II have been relatively muted, so far.

In an April 11 NBC interview, Peter Navarro, a White House trade adviser, claimed that "90 deals in 90 days" was possible. So far, there have been only two trade deals announced, with the United Kingdom and Vietnam. There is also a framework agreement with China…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

All star charting says we’ve got a bearish break 10s … or, ‘scuse me .. TNX — which, frankly, am not sure even what it is but … lots on the web cite it so …

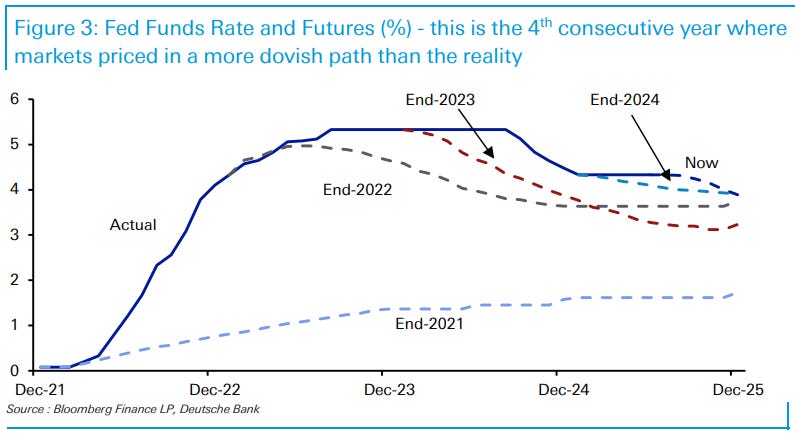

The bond market continues to price the next Fed move to be a cut, with the expectation that growth is slowing down.

But the stock market is trading cyclicals higher relative to defensives, with the expectation that growth is about to accelerate, see chart below.

This is not consistent. Either the bond market is wrong, and rates must move higher due to accelerating growth. Or, equity markets are wrong, and stocks have to move lower because growth is slowing down.

… who you bettin’ on — stonks or bonds …? AND on THAT note, one more funTERtaining chart from the intertubes OF stocks vs bonds …

An article showing preference of EGBs over USTs as well as an OpED with a handful of funTERtaining visuals from The Terminal dot com …

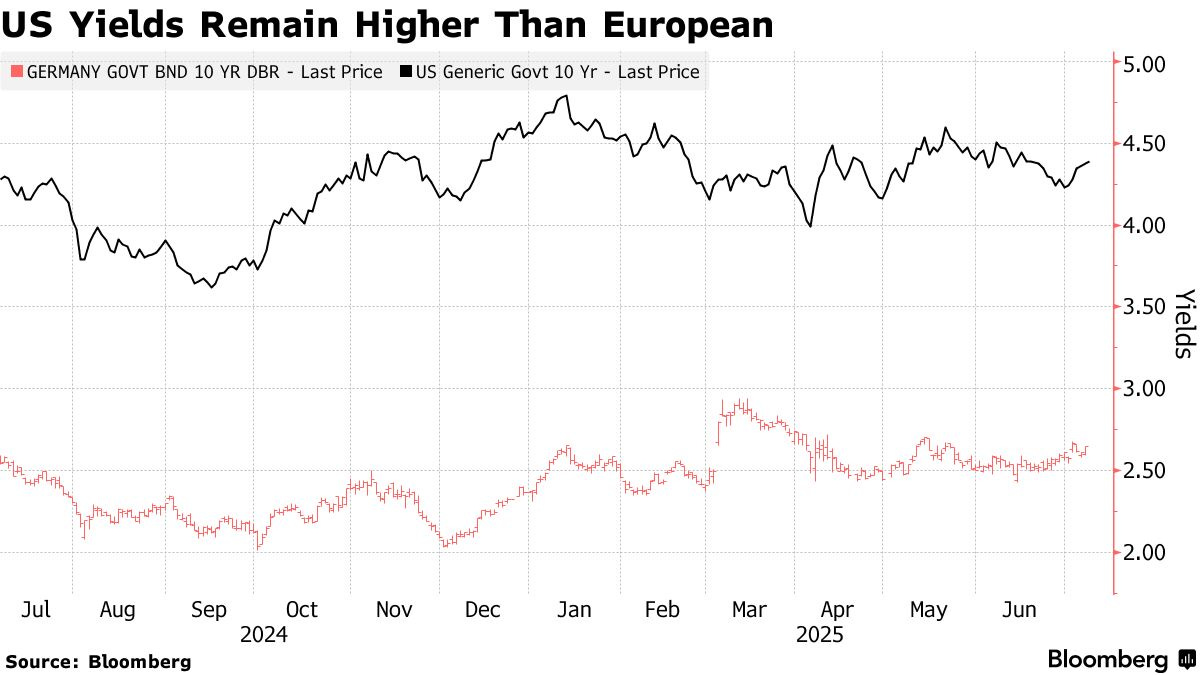

July 8, 2025 at 7:35 AM UTC Bloomberg: BlackRock Prefers European Government Bonds Over US Treasuries

BlackRock Investment Institute shifted its view on European government bonds to neutral from slightly underweight, citing the attractiveness of their yields versus Treasuries.

“We prefer euro area government bonds and credit over the US,” strategists including Jean Boivin and Wei Li wrote in a weekly note. “Yields are attractive, and term premium has risen closer to our expectations relative to US Treasuries.”

The strategists see sticky inflation keeping the Federal Reserve from cutting rates far. They also said high fiscal deficits may prompt investors to seek more compensation to hold long-term Treasuries.

Treasuries sold off over the past week after posting their best monthly performance since February last month as traders priced in the prospect of Fed rate cuts. Some of those bets have been rolled back after the US reported strong employment data for June.

Within the eurozone, BlackRock prefers peripheral bonds such as those from Italy and Spain.

July 8, 2025 at 4:32 AM UTC Bloomberg: Your Tariffs Are in the Mail, Sealed With a Diss There’s still a lot of drama left for trading partners who haven’t received letters yet.

… TACO Tuesday may never come. The conclusion of the three-month pause in the swingeing “reciprocal” tariffs announced on April 2 may not see the expected fireworks after a (not-so) Manic Monday, in which the US kicked the can down the road until Aug. 1. Tariffs are unchanged until then. A Freaky Friday, in the middle of the summer doldrums, awaits.

Letters to different countries revealing the proposed tariff rates on their goods that would apply fromthe end of this month seeped out throughout the day. Most were unchanged from the steep rates announced on Liberation Day, while some were reduced a little. They can still raise eyebrows. Levies of 25% on Japan, South Korea, and Malaysia would,if sustained, surely depress global trade and growth. In all cases the letters, apparently written by the president himself, included a threat to match any retaliatory tariffs, and a hope of reaching a deal this month …

…Tariffs Haven’t (Yet) Made a Big Impact on Inflation or Jobs

June inflation won’t be available until next week. For the first two months since the Liberation Day 10% baseline took effect,however, signs of tariffs driving price increases were minimal.

Unemployment for June, published last week, similarly showed no significant impact from tariffs. It was possible when the 90-day pause started that the data would have enough time to demonstrate that the drive toward protectionism must end. That hasn’t happened. As a result, these tariffs may be more durable.

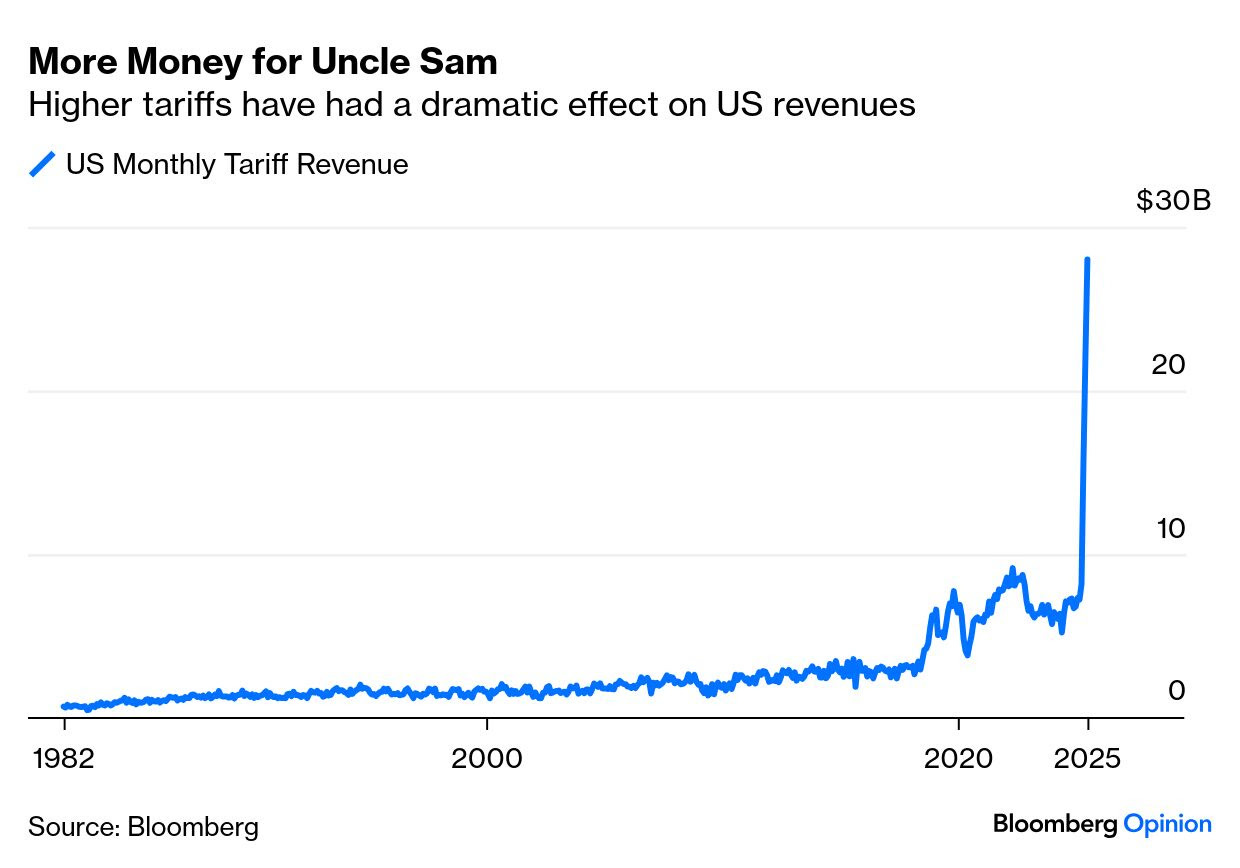

Companies Have Paid a Lot of Money in Tariffs to Uncle Sam

The tax cuts in the One Big Beautiful Bill Act make revenue from tariffs all the more important. There is always a risk with any tax that a high rate disincentivizes activity and reduces the tax take. That hasn’t happened so far:

The current baseline 10% rate might eventually prompt a fall in imports — which is, after all, the point of the exercise. For now, the revenue is some kind of a proof of concept. The 10% tariffs are, almost certainly, here to stay…

A question for a (macro)Monday brought to you a day late — sorry / not sorry — better late than never?

This is one of the lightest data weeks we’ve seen in a while. Aside from Tuesday’s NFIB Small Business Survey and Wednesday’s FOMC Minutes, it’s quiet on the macro front.

Last week the story was laser focused on employment.

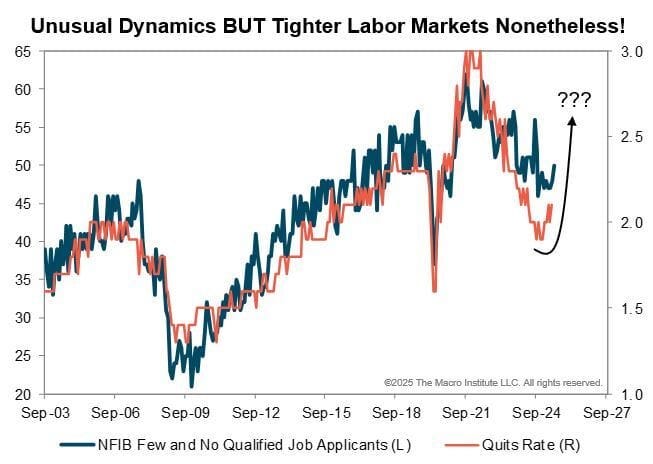

June payrolls beat expectations, but the real story lies in the details:

The "foreign born" labor force shrank for the third month in a row. It’s tough to draw hard conclusions from this, but it suggests that stepped-up deportations are having an impact.

The unemployment rate ticked lower pointing to a tighter labor market.

That matches the signal from the Quits Rate in the JOLTS report and the “few or no qualified applicants” reading from NFIB.

Bottom line? If these trends hold, wage inflation could be set to reaccelerate…