while WE slept: USTs cheaper / steeper (DJT Truth fear, JPOW, yer fired?); extend 10yy (long)tgt, move trailing stops (BNP)! "After the tantrum" (HSBC) and more ...

Good morning … I interrupt normal workflow for latest Truth Social post making waves on Global Wall …

… I’ll move along as this one gets more widely disseminated and consumed / priced IN.

The wait for Dr Hunt’s latest quarterly continues and with markets holiday tomorrow, ‘posting’ will be light but rest assured, if / when I see something, I’ll try to say something and with that in mind, on heels of yesterday’s JPOW ultimately sayin’, ‘NO PUT FOR YOU’ (not ONLY my view — see BMO below), so lets jump in…

10yy DAILY: 4.33 - 4.03, a triangulating range and some ‘soft’ targets …

… TLINEs etched in which bring MY attention on current levels as KEY … momentum (slow stochastics, bottom panel) remain overSOLD and one of 2 things can / will happen to alleviate such a condition — either we spend TIME AT A PRICE or we move lower …

Where to begin? What a day. Stonks down bigly YEST (JPOW put dismissed, gone for good?) and futures are indicated higher this morning (Japan trade deal near?) — 2 steps back, 1.5 steps forward?

NOT quite the progress one wants to see and I’ll ask how much of the activity being driven by fewer and fewer eyeballs into the holiday long weekend just ahead.

My former bond mkt colleagues will be closin’ up shop early today while stock jockeys stick around all day (always funTERtaining to watch as things like TLT and HYG trade when underlying market closed and the ‘adults in the room’ have left the building).

The belly of the curve has become increasingly popular (BlackRock’s Rick Rieder on BBG likes ‘em) and yesterday, Dept of Tsy offered up some longer duration … did YOU #Got20s?

… great if you did, as JPOW took stage shortly after the auction process and quickly sank stonks, providing some quick RISK OFF F2Q profits in newly minted 20s (and the rest of the rates space) …

ZH: Stocks Puke As Fed Chair Powell Raises Specter Of Stagflation, Awaiting "Greater Clarity"

…Powell said: "tariffs are highly likely to generate at least a temporary rise in inflation."

"The inflationary effects could also be more persistent. Avoiding that outcome will depend on the size of the effects, on how long it takes for them to pass through fully to prices, and, ultimately, on keeping longer-term inflation expectations well anchored.

Powell again stressed the central bank's focus on preventing potential tariff-driven price hikes from triggering a more persistent rise in inflation…

…Powell raised the spectre of stagflation:

"We may find ourselves in the challenging scenario in which our dual-mandate goals are in tension. If that were to occur, we would consider how far the economy is from each goal, and the potentially different time horizons over which those respective gaps would be anticipated to close."

This differs from Waller earlier this week:

Should the Fed face both a rapidly slowing economy and still elevated inflation, “the risk of recession would outweigh the risk of escalating inflation.” …

… Dunno ‘bout you but seems to becoming increasingly clear to ME that WallEEEEeeeee may be what we see as the ‘shadow’ chair appointed in the Fall, getting the markets comfy with him before he’s appointed chair in 2026?

Anyways, before 20yr auction, followed by the Fed put being summarily dismissed (ZH recap HERE), some informative data which can / will be used to defend whatever your narrative (and PnL) may be …

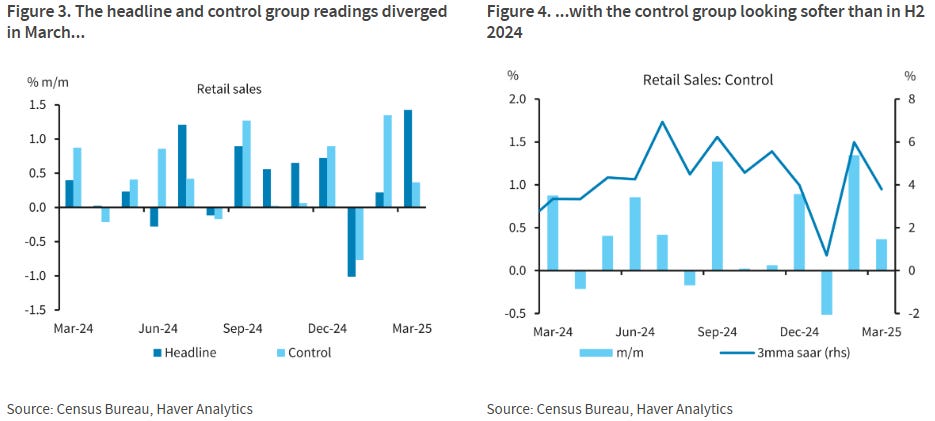

ZH: US Retail Sales Soared Most In 2 Years In March As Auto-Spending Spiked Ahead Of Tariffs

WolfST: Drunken Sailors Back in Splurge Mode, Retail Sales Surge. Even at Restaurants & Bars not Part of Frontrunning Tariffs … The recession is going to have to get back in line and wait.

… and then some mfg related data…

ZH: US Industrial Production Dipped From Record High In March

… Seriously, though, who am I kiddin’?

Zero point ZERO chance I’ve got a real view and know what it is JPOW said that actually mattered. I’d BET it was just a culmination of position SQUARING on not much NEW information while at the same time, a bit of SHOCK and awe the Fed chair offered some truth bombs about POTENTIAL for inflation AND slowing growth.

You’ll see some more on this below (best in show, for example).

Markets were then left to their own to TRY and interpret whatever it is they think they think and see as next move.

I suppose IF things get bad enough, the presidential working group on markets (Plunge Protection Team) might be forced into action … lets all HOPE not but if the PPT does arrive, am quite sure things like this ‘stack, aren’t gonna be top of anyone’s mind.

On THAT note I’ll move along … here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: NQ benefits after strong TSMC results, USD firmer whilst EUR slips ahead of ECB … Bonds are softer following the robust macro tone, EGBs await the ECB … USTs are softer, with benchmarks coming under pressure early doors as the general risk tone improved after strong TSMC numbers. Prior to this, a bearish bias was already in-play as APAC shrugged off the Wall St. lead and climbed, with focus on Trump’s positive commentary on trade with Japan. The US-Japan progress weighed on JGBs, resulting in them briefly underperforming overnight alongside a long-dated JGB liquidity auction. Currently at a 111-02+ low and around 15 ticks from the overnight high. Ahead, Weekly Claims, Philly Fed, Building Permits/Housing Starts & Baker Hughes.

Retail sales accelerated 1.4% m/m, boosted by a surge in auto sales ahead of tariffs. Control group sales rose a modest 0.4% m/m, on the heels of an upwardly revised February print (1.3% m/m). The data imply solid PCE momentum in Q1 and positive carryover effects for Q2.

I know much has already been made of this next note but I’m offering as I just stumbled across it AND always find some morsel of detail when I read through it straight from the horses mouth as opposed to only seeing the graphic / highlight from others … which I’ve also excerpted some below BUT … have a point and click through if you so choose…

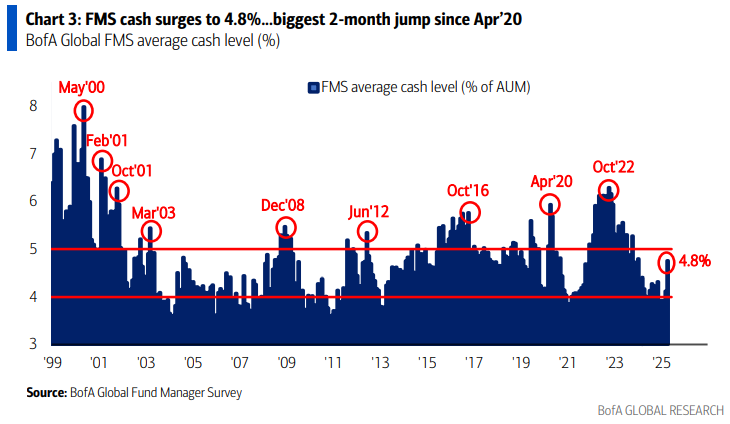

15 April 2025 BAML: Global Fund Manager Survey The Bear Necessities

Bottom line: 5th most bearish FMS in past 25 years, 4th highest recession expectations of past 20 years, record no. of global investors intending to cut US stocks (Chart 1); FMS max bearish on macro, not quite max bearish on market (“peak fear” norm is ≈6% cash level vs 4.8% today); but our FMS says a. April asset price lows to hold near-term, b. big upside needs big tariff easing, big Fed rate cuts, and/or economic data resilience…

…On Allocation: record increase in bond allocation, global equity allocation lowest since Jul'23, US stock allocation sees largest 2-month drop ever; investors most UW cyclicals vs defensives since May’20, cut industrials (most UW since Aug'11), tech (most UW since Nov’22), banks, discretionary, add utilities (most OW since Dec'08), pharma & staples…

…BofA FMS cash level rose to 4.8%, up 125bps since Feb’25…the largest 2-month increase since Apr’20…

… Note FMS cash levels averaged 6.2% in the 9 prior highs since 1999 (May’00, Feb’01, Oct’01, Mar’03, Dec’08, Jun’12, Oct’16, Apr’20, and Oct’22) …

Best in show on the JPOW PUT …

April 16, 2025 BMO Close: Pocketing the Powell Put

…Yields spent most of Wednesday’s session range-bound with 10-year rates flipping between higher and lower several times throughout the session until a more durable rally emerged in the wake of Powell’s comments in the afternoon. The net-bullish skew has once again reinforced the constructive momentum that’s returned to the US rates market this week after the violent selloff of early-April. The Fed Chief triggered a broader risk-off tone that pushed 10-year yields as low as 4.26%. When asked if the Fed would intervene if stocks fall sharply, Powell said, “I'm going to say no, with an explanation… markets are processing what's going on, markets are struggling with a lot of uncertainty and that means volatility… markets are functioning conditional on being in such a challenging situation, markets are doing what they're supposed to do, they're orderly and they're functioning just about as you would expect them to function.” To sum things up, Powell chose to downplay official intervention risks rather than lead the market to assume a Fed put is on standby. This by no means suggests that Powell wouldn’t intervene if conditions were to reach a level of true disorder, rather that current circumstances are still far from the strike price for the Fed put.

The major takeaways from Powell’s prepared remarks were almost identical to those from his prior speech on April 4th. The Chair reiterated a familiar message that, “tariffs are highly likely to generate at least a temporary rise in inflation. The inflationary effects could also be more persistent.” Powell also reiterated that the announced tariffs are “significantly larger than anticipated.” This is somewhat notable as it implies that the 90-day pause on reciprocal tariffs for non-retaliating countries did not yield any change in the anticipated size of the average effective tariff rate. That said, it wasn’t much of a surprise given that most estimates are still around 25%, according to Fed Governor Waller. Powell also made headlines through his emphasis on the dueling economic threats posed by the global trade war. Specifically, “The [Trump] administration is implementing significant policy changes and particularly trade is now the focus. The effects of that are likely to move us away from our goals.”…

…February’s TIC data showed the largest jump in overseas holdings of Treasuries in over four years. Within the details, China’s holdings jumped by $23.5 bn to $784.3 bn, and Japan surged by $46.6 bn to $1.13 trn. For Japan, this was the biggest monthly gain since before the pandemic. While somewhat encouraging datapoints, it goes without saying that it is stale information in the context of recent concerns around overseas sponsorship for Treasuries and speculation of retaliatory selling in response to Trump’s tariff actions. While the foreign appetite for Treasuries in February was ‘good news’ with respect to the global willingness to underwrite the US deficit, the data doesn’t resolve any of the big questions around overseas demand at the moment – the next two months of data promise to be much more telling in this regard.

France on being / STAYING long 10s and on self fulfilling prophecies …

16 Apr 2025 BNP: QTOW: Extend US 10y yield target and move trailing stop loss

Our long US 10y Treasury trade idea (see QTOW, dated 14 April) has performed well since inception. We initiated the trade, as signals from both our MarFA™ Macro and our faster MarFA™ Trading (3m lookback) suggested that the US rates selloff was overdone. Further, we see US 10y nominals as having decoupled from the current softness of data and data surprises. Tightening in US financial conditions in late February and March is also set to weigh on our US data projections. MarFA™ Macro currently shows US 10y yield 16.4bp too high (2.3 z-scores), while its fair value keeps grinding lower. Based on a view from our FCI-Data Tracker projection model, we now extend the target to the new fair value level of MarFA™ Macro of 4.14%, from 4.29% previously, and move the trailing stop loss to 4.45%.

16 Apr 2025 BNP: US: With business expectations, perception becomes reality

KEY MESSAGES

The latest business surveys highlight the remaining chance for the US economy to avoid a recession, as well as the risks of a serious downturn emerging in the absence of continued and immediate moderation in tariff policy from the administration.

Consumer and business expectations tend to be noisy but can ultimately be self-fulfilling.

Surveys suggest the economic expansion remains ongoing but anemic, with much of the optimism of the post-election environment having evaporated but no clear evidence that the economy has passed the point of no return.

…Consumer sentiment alone often gives false signals about a recession: consumers can report a dour outlook but keep on spending. However, if weakness here is joined by lower equities and higher initial jobless claims, there is a higher likelihood that an economic downturn could happen or is already happening (Fig. 5). Historically, declines of 10% or more in sentiment and in the S&P 500 along with a sustained 20% or more increase in initial jobless claims have indicated a recession. Right now, this mix of indicators suggests an elevated risk of recession.

TICS out yesterday and some factoids from WolfST below but in meanwhile …

17 April 2025 DB: About China possibly selling Treasuries last week

We share our perspective on a popular client question from the past week: Did foreign central banks, in particular China, sell their Treasury holdings?

Hard data on China’s activity is limited and released with considerable delay, while its holdings are further obscured through the use of offshore custodial accounts. This leaves us to hypothesize possible narratives for China’s selling – if it indeed sold Treasuries.

One plausible scenario is that China preemptively sold Treasuries to bolster dollar liquidity in preparation for potential currency intervention to counter depreciation pressures on the yuan.

We think unloading of Treasuries as direct retaliation for the tariffs is unlikely, though it’s possible China was comfortable with some degree of the signaling effect as long as it maintained plausible deniability.

In this next note, another steadfast bond bull offers a MAJOR bond letter …

16 April 2025 HSBC: The Major bond letter #60. After the tantrum

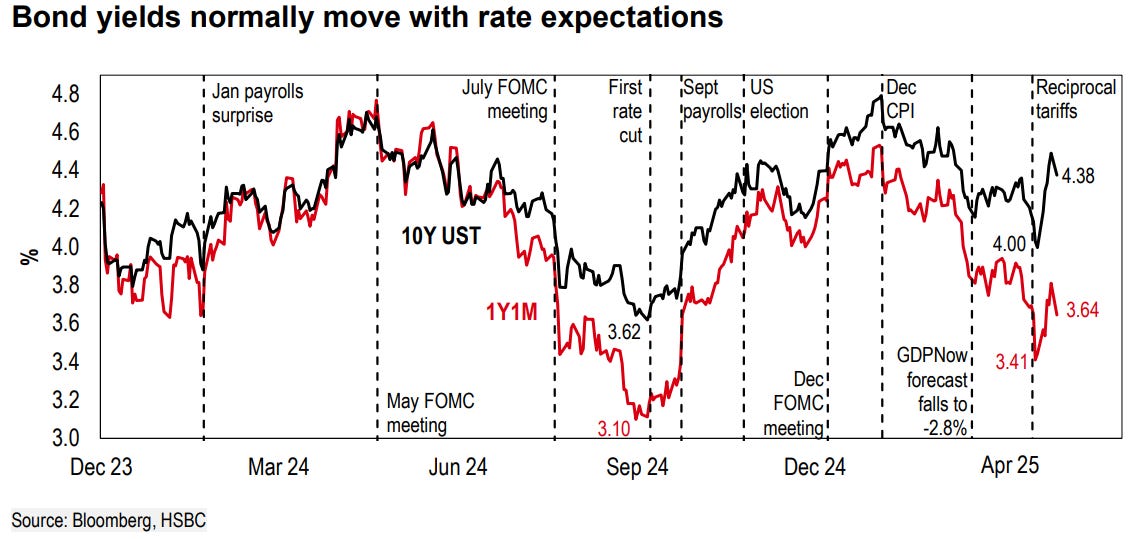

All was well in the USD29trn Treasury bond market, or at least seemed to be. Yields were moving along a downward path through the first three months of the year, in sympathy with the US Treasury Secretary Scott Bessent’s early objective (Bloomberg, 6 February 2025). And then along came the reciprocal tariffs in the second week of April and the bond market had a bit of a tantrum.

In “normal” times, bond yields move with rate expectations, and this is because most of a bond’s yield is explained by the policy rate and the market’s view of where this rate is going. But something strange is afoot. The gap between rate expectations and bond yields has increased quite sharply (see chart), indicating that investors are requiring additional compensation for holding bonds compared with money market rates. Before we discuss why this happened and what’s necessary for bonds to reconnect, let’s explain our chart.

Market expectations of where policy rates will be in a year’s time are approximated by the one-year forward (1Y1M). As the chart shows, this red line can move a long way from the policy rate. Ahead of the first rate cut for this cycle (18 September 2024) markets anticipated a total of 250bp easing over the following year. There have since been 100bp of Fed funds cuts and, at 3.64%, today’s 1Y1M implies the equivalent of three more 25bp cuts below the current Fed funds upper bound.

The gap between the two series in the chart captures the additional yield required in compensation for taking duration risk. It is a type of term premium. We once described the theory behind term premium as a “dark art” because it always seemed to be shrouded in mystery and conspiracy (see Dark Art, 21 April 2017) – something that you know lies out there in the shadows, but often can’t quite be seen. Yet, inevitably, when everyone’s talking about term premium (with some even trying to forecast it), you know it is probably on the way to being priced in – and at the point where it starts to fade from view…

…As a final thought, let’s return to the chart. The 10-year Treasury has spent most of the last year in a 100bp range, which is not far off the average for a typical calendar year. The gap between the one-year forward and 10-year Treasury (red and black lines) is 74bp today, modestly wider than the 52bp gap that existed last September.

Only two weeks ago, both rate expectations and Treasury yields were threatening a return to the lows of last September. The Treasury market has thrown a bit of a tantrum since then with term premium coming out of the shadows and higher yields provoking a response. We’ll see in the coming weeks if the bond market can get the upper hand on policymakers.

16 April 2025 ING: US retail sales bounce as savvy consumers buy ahead of tariffs

Retail sales jumped as consumers brought forward purchases of 'big ticket' items to get ahead of feared tariffs. But with confidence plummeting on price, job and wealth concerns, the consumer will be less of a growth engine later in the year

Stay neutral on TIPS-breakevens as markets remain volatile and any sell-off in equities or decline in oil prices could lead to further tightening; maintain long 2-year TIPS but with a tight stop.

Key takeaways

1 year CPI swap gains have been pared back since April 2, with a 21bp contribution from the decline in oil prices.

Our five-factor fair value model suggests a neutral stance on breakevens as they are more sensitive to a sharp sell-off in equities compared to Treasuries.

TIPS ETFs have started showing outflows after the recent peak, following the announcement of a pause in reciprocal tariffs.

We maintain long 2-year TIPS but with a tight stop, as we see the trade benefitting from slower growth amid heightened uncertainty around tariffs.

Forcing a recession is never a good idea (see Apollo below for more) and …

17 Apr 2025 UBS: Self-inflicted slowdowns and the Fed

Federal Reserve Chair Powell noted US President Trump’s trade taxes would raise inflation and lower economic growth. Markets have already worked this out, but Powell saying it has policy implications. On the evidence of (unreliable) sentiment surveys, over a third of US consumers think inflation will exceed 10% this year. Powell emphasized longer-term inflation expectations, which should still allow for rate cuts. The self-inflicted nature of the economic slowdown may limit the number of cuts.

Trump attended trade talks with Japan—this matters as deals require Trump’s assent. Trump talked about a “big deal” which markets are interpreting as a big retreat. Japan’s trade data today emphasized that imbalances in an ageing society are unlikely to be concerning—Trump’s focus on Japan seems more reminiscent of 1980s economics.

The ECB is expected to cut rates (62 economists agree, and how could so many economists be wrong?). Comparing ECB President Lagarde’s comments with those of Powell might be instructive, as the European economy will suffer less damage from Trump’s taxes than will the US.

The US Philly Fed business sentiment survey is due. All sentiment data is extremely suspect nowadays, but markets are focused on the corporate inactivity amidst policy uncertainty. Even unreliable evidence therefore has influence.

Covered Wagon on ReSale Tales and mfg production …

April 16, 2025 Wells Fargo: More than Just a Pre-Tariff Shopping Spree Despite Wilting Sentiment, Q1 Consumer Spend Now Looks Less Dreary

Summary The March retail sales report met expectations on the headline and exceeded expectations after accounting for upward revisions to prior data and a composition of spending that reflects more than just a pre-tariff splurge. The upshot is that Q1 PCE is shaping up to be halfway decent.

April 16, 2025 Wells Fargo: Manufacturing Production Holds Up for Now

Summary Manufacturing output increased 0.3% in March, a bit more than expected. We know that industrial supply imports surged in recent months, giving factories the inputs they need. If tariffs get in the way of that pipeline, output could slow. A sharp drop in utility output could be an early signal of that.

Finally, for some further reading and ‘wisdom’ from the stocks for the longrun shop …

+ The April tariff announcements (Liberation Day and the 90-day pause) underscore the volatile and uncertain forces that have raised both downside risks to the economy and upside risks to inflation.

+ While the Federal Reserve appears to be still skewed toward rate cuts later this year, Chair Powell acknowledged the economy and labor markets remain solid, providing the policy makers some cushion to “take a step back and let things clarify.”

+ The Treasury 10-Year yield is expected to remain at an elevated, ”normal” level with heightened headline and data dependency producing continued volatility.

+ We believe the bond portfolio decision-making process could benefit from taking an active-passive barbell approach from a solution standpoint.

+ On the equity side, the market is gripped with fear, but we take the longer view and see this as a buying opportunity.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

First up, I’d have a hard time finding a truer statement than this…

April 16, 2025 Apollo: Creating a Recession to Lower Long Rates Is Not a Good Idea

If the US enters a recession, long-term interest rates are likely to go down, and it would be cheaper for the US government to refinance existing government debt.

However, the chart below shows that the interest payments saved if interest rates decline by two percentage points would be more than offset by the deterioration in government finances associated with a recession.

Specifically, if interest rates decline by two percentage points, the US government would save around $500 billion in annual interest payments. But if the US enters a recession, the government will have lower tax collections and pay more in unemployment benefits, and the historical deepening of the budget deficit during recessions of around 4% of GDP would correspond to an additional $1.3 trillion erosion of US government finances measured in 2025 dollars.

The bottom line is that it is not possible to improve the budget deficit by creating a recession because during a recession government finances would deteriorate by double the amount saved in interest payments, see chart below.

That was then and today’s note another statement of the obvious — rates are rising AND Japanese investors are … selling?

The term premium in US Treasuries is rising, see first chart below. The market does not know if this is because of the fiscal situation, inflation expectations becoming unanchored, or discussions about who the next Fed Chair will be.

Some of the move higher in rates has been technical, driven by unwinds of levered basis trades and swap trades.

In addition, the move lower in the dollar is telling us that the move higher in rates is also because of foreigners selling Treasuries.

For example, Japanese investors have in recent weeks been significant sellers of foreign bonds, and this has been associated with a significant appreciation of the yen relative to the dollar. This does not necessarily mean that Japanese investors are questioning American exceptionalism. In fact, in 2022, when the Fed started raising interest rates, Japanese investors were also significant sellers of foreign bonds, see second chart below.

We are hosting a conference call today at 9 am EDT to discuss what is going on in markets and the outlook for the economy, you can register here.

Times like these I wish I had a Terminal and could craft my OWN visual with TICS data and more currently weekly MoF inputs … oh well.

Here’s a VIEW from The Terminal.com …

April 17, 2025 at 4:06 AM UTC Bloomberg: Is this the brink of the recession we had to have? US trade policy may create an epic buying opportunity, but much later if there is a downturn.

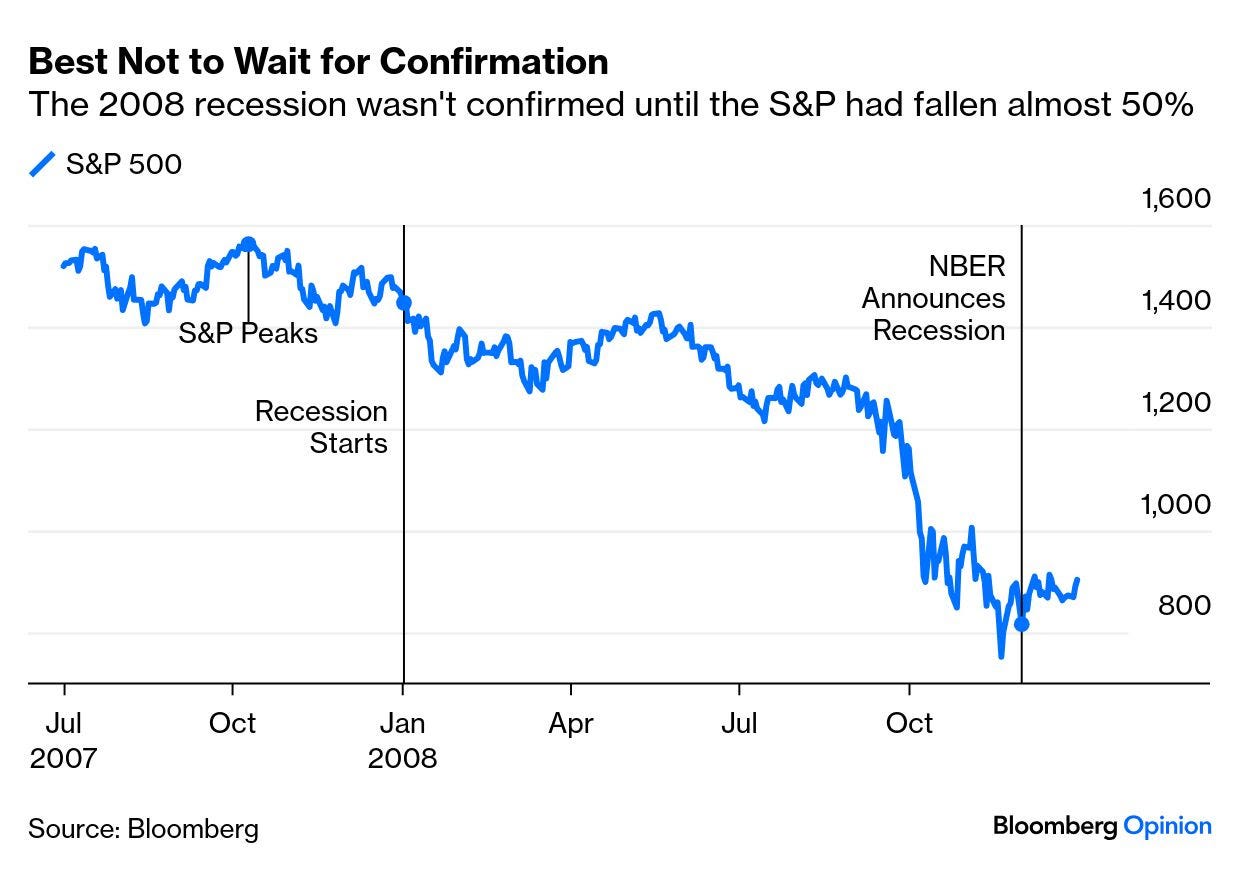

…Recession When you think a recession is coming, it generally pays to sell first and ask questions later. Waiting for confirmation that the economy is declining is just too costly. For a spectacular demonstration, look to the events of 2008, when the National Bureau of Economic Research announced that a recession had started in January of that year — but didn’t announce this until December:

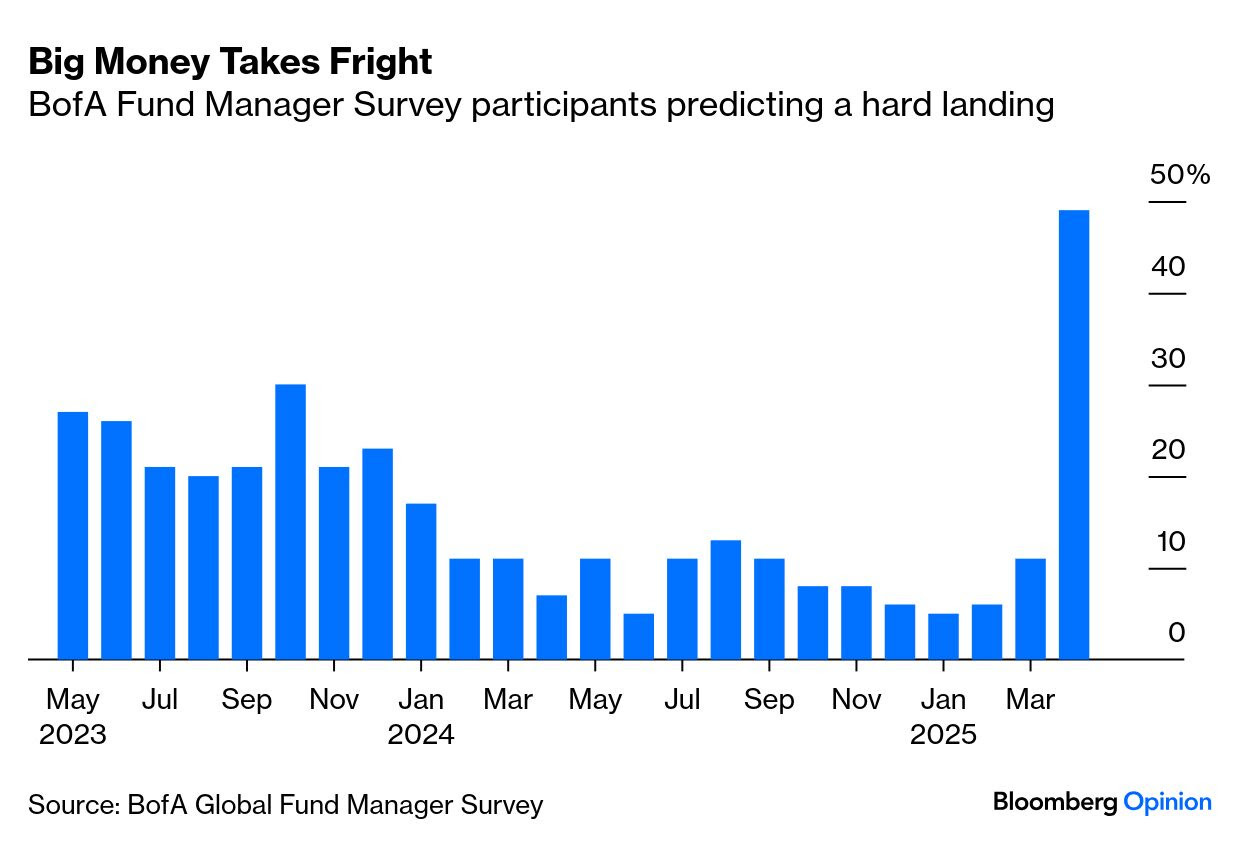

From the start of the recession to the NBER’s acknowledgement, the S&P 500 almost halved. It was better to take a judgment first. That’s why there’s particular interest in the latest survey of global fund managers by Bank of America Corp., the first since the “Liberation Day” tariffs announcement, which showed a dramatic increase in fears of an economic hard landing:

If big fund managers take fright, then their actions can guarantee a market selloff as they move their money to safety…

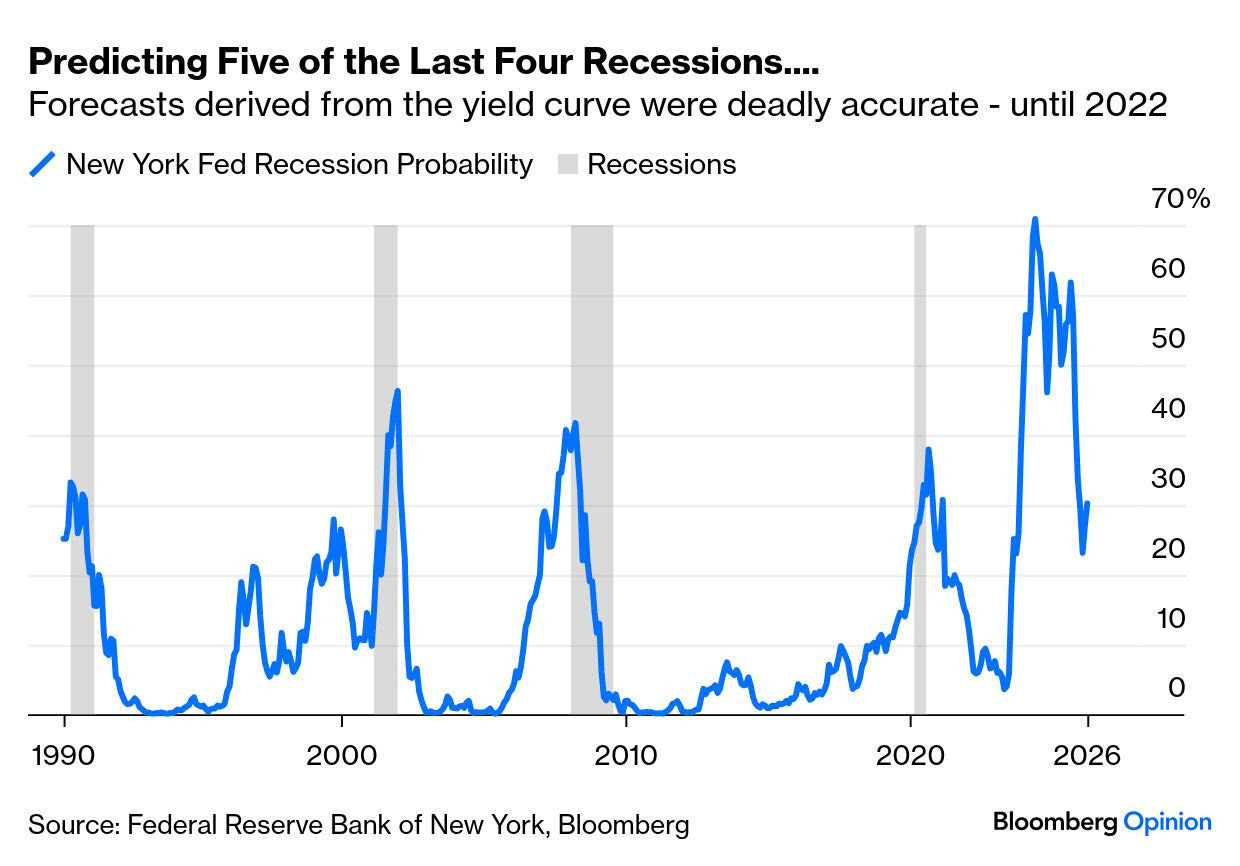

… There’s another problem with making a confident recession prediction. Formerly reliable market indicators have been foretellingone for so long without success that it’s getting harder to take them seriously. The New York Fed recession probability indicator is based on the bond yield curve. Over time, an inverted curve, in which long bonds yield less than shorter-term instruments, has been a surefire sign of trouble ahead. But it’s never been more confident of an oncoming recession than it was in 2022, and so far it hasn’t come to pass:

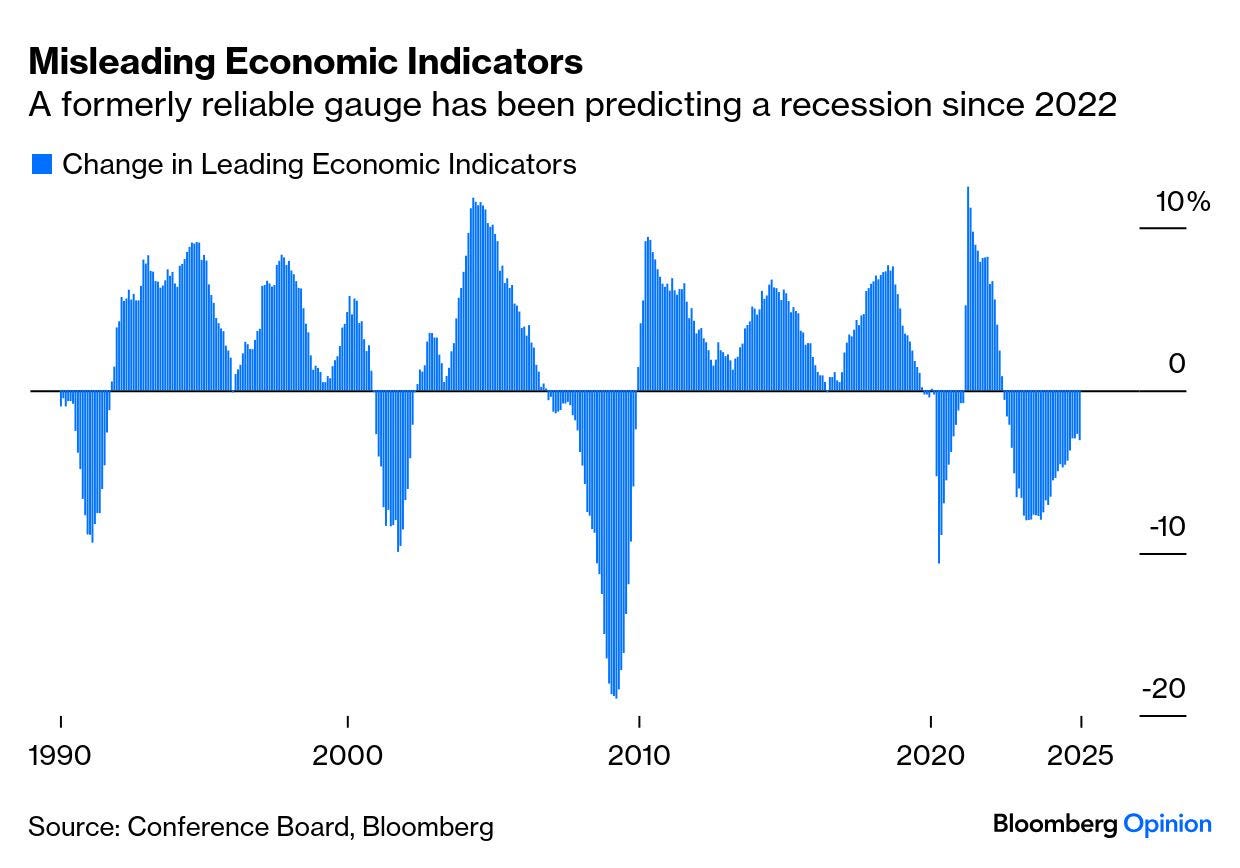

Another virtually foolproof signal comes from the Conference Board’s Leading Economic Indicators, which smooshes together various measures of the economy and market. Just like the yield curve, it successfully predicted the last four recessions, but also a fifth that still hasn’t happened:

One problem with getting out of the market when everyone is scared of a recession is that this is often a great contrarian time to buy…

As discussed last week, Trump blinked when it became crystal clear that we were seeing material problems in areas such as funding and safe assets, as well as the liquidity and functioning of the Treasury market and rising Treasury yields.

With marketable Treasury debt exceeding $26 trillion, the bond market is still in charge! As political strategist James Carville said years ago, the bond market can intimidate anyone – even President Trump!

Imagine the conversation Secretary Bessent had in the oval with the President telling him that 10-year yields were rocketing higher, not collapsing, and that the Treasury market was no longer functioning smoothly. This suggests a second Trump “put” was also exercised last week.

State Street on bond ETFs …

April 16, 2025 STATE STREET Global Advisors Q2 ETF Bond Outlook: How to position for more volatility With tariff uncertainty fueling market volatility, our Bond Market Outlook looks at how investors can build resilient bond portfolios.

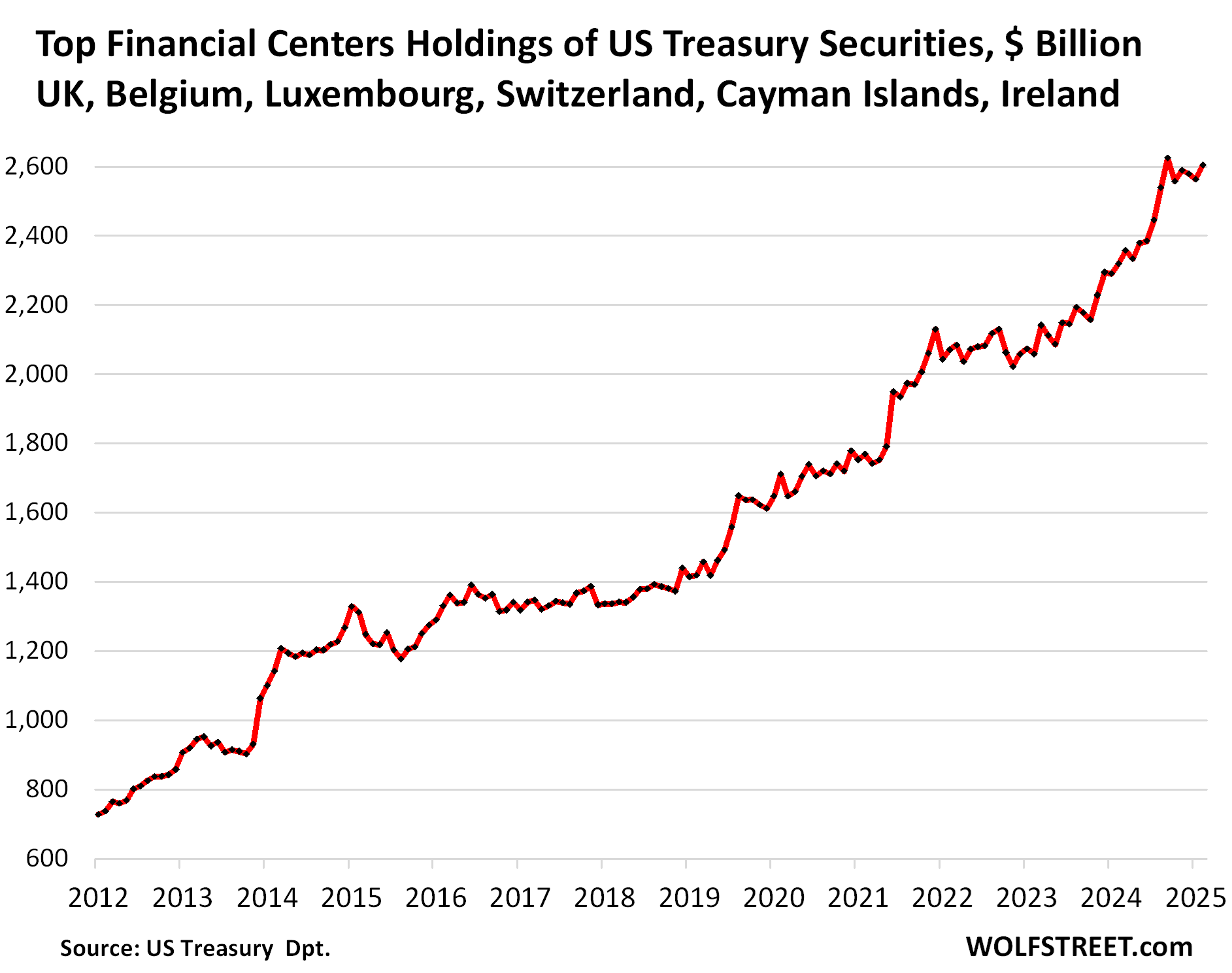

Wolf on TICS (Feb data so a bit stale but still) …

WolfST: Foreign Investors Massively Bought US Treasury Securities in February: China, Japan, Canada, Euro Area, UK, Financial Centers, Taiwan, India, even Brazil

Biggest increase since June 2021. And they mostly bought long-term Treasury debt. No major holder dumped.

…Higher yields create demand. Yields of US Treasury securities have remained relatively high compared to the securities of other countries. The 10-year Treasury yield is currently at 4.28%, compared to the German 10-year yield of 2.51%, the Japanese 10-year yield of 1.20%, or the Canadian 10-year yield of 3.08%. One of the exceptions is the UK 10-year yield, at 4.61%.

These higher yields for Treasury securities make them very attractive to foreign buyers. We saw that this buying continued at the 10-year and 30-year Treasury auctions last week, and at the 20-year Treasury auction today: There was blistering demand from “indirect bidders,” a category that includes foreign bidders…

…Japan’s holdings jumped by $47 billion in February. It thereby recaptured nearly all the declines since April 2024 that resulted from its efforts to prop up the yen, which had plunged.

Since 2012, Japan’s Treasury holdings rose and fell, and currently are where they were in 2012:

…The six largest financial centers added $42 billion in Treasury securities in February (+1.6%) and $285 billion over the past 12 months, to $2.60 trillion, just a hair below the record of September 2024. Since 2012, their holdings have more than tripled!

Finally …

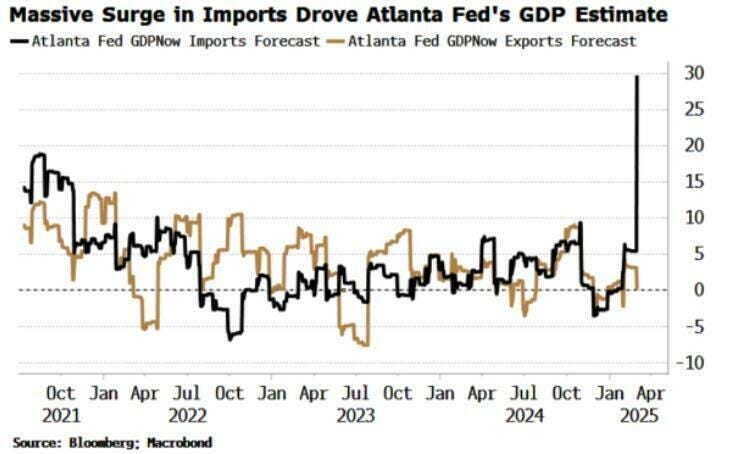

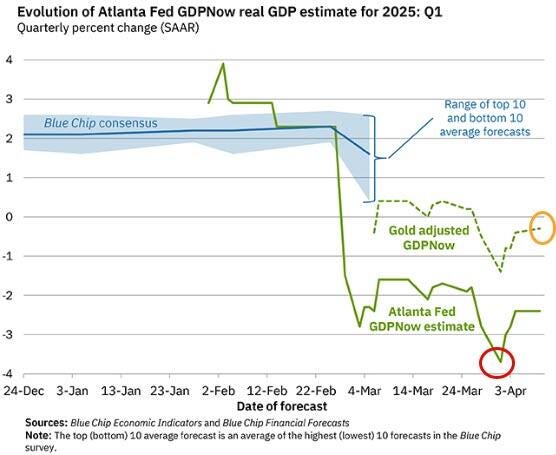

ZH: 'Depression' Narrative Bust: Atlanta Fed 'Adjusts' Away GDP Plunge Forecast

... we subsequently learned that the plunge in GDP was the direct result of a spike in imports, which subtract from GDP.

As it turns out, and as Goldman economist Manuel Abecasis explained this morning, most of the widening in the trade deficit since November was driven by higher gold imports.

That's right: the same spike in gold that indicates something is (perhaps terminally) broken with the financial system as we have now seen a record scramble for physical gold, also just happens to be slamming the US economy!