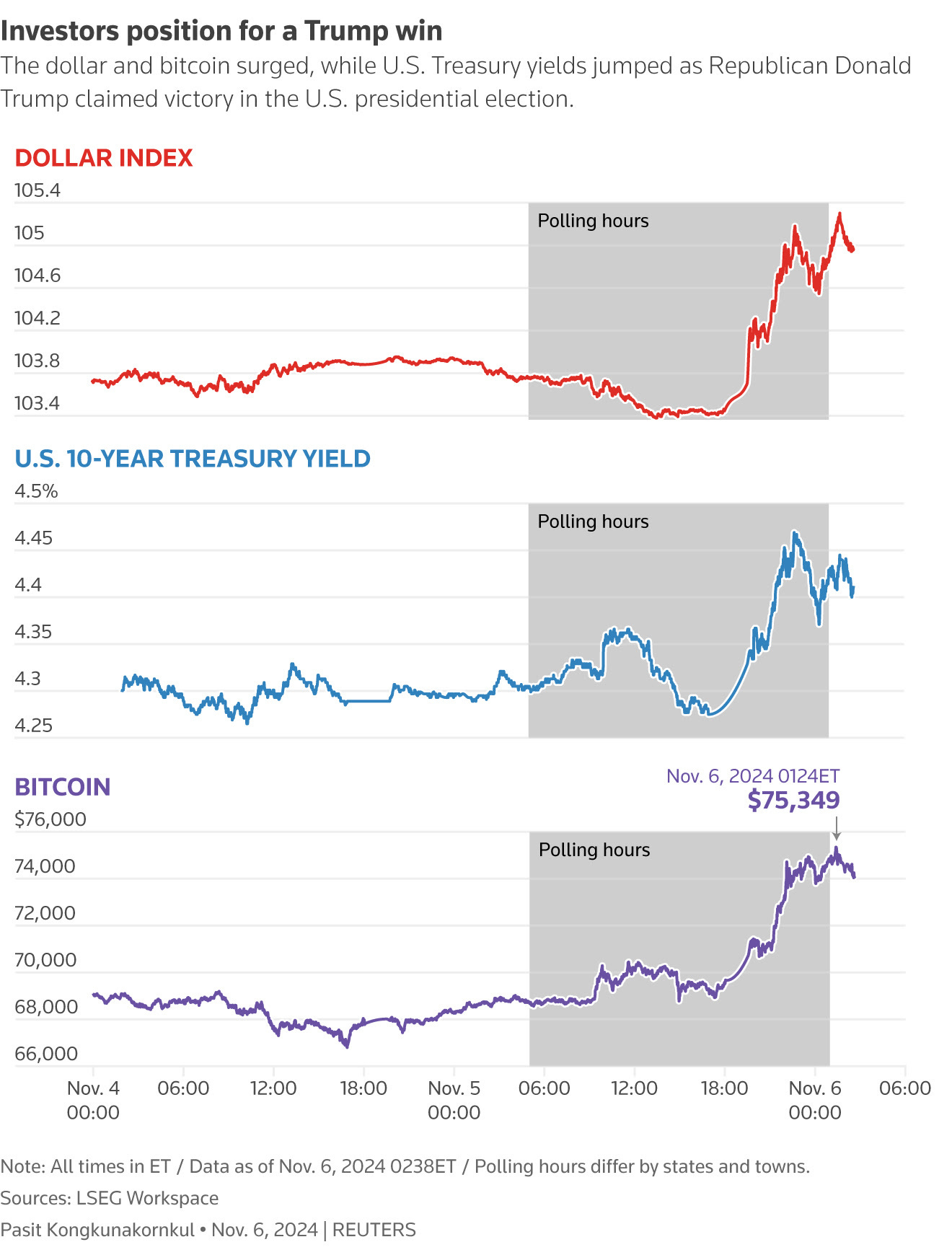

It would appear to be nearly a clean sweep or a very large red wave, at least from the bond markets perspective as the term structure pricing in substantially cheaper and steeper is said to be classic red wave Trump Trade … strong dollar, BITC and higher yields as a result OF consequences from meeting the new boss, same as the old boss and so, higher ‘flation resulting from increasing tariffs …

30yy DAILY: breaking badly (above down TLINE) with support near

… and as yields grind UPWARDS of 20bps ahead of supply — concession (?) — we’ll move right along …

… and so, now we know (?)

… now I’m NOT sure it’s 100% confirmed but this is the sort of thing we’re going to see over the coming hours, days and weeks and while this is of yuuuuge signficance, thinking about TRUMP TRADES (re)GRIPPING markets, well, lets just jump right in.

… and so, now we know …

WSJ: Trump Trades Take Hold - Drives Stock Futures Higher Investors are piling into trades linked to a potential Trump victory, sending bitcoin prices to a record, while Asia saw some currency falls and sharp stock declines.

WSJ: Stock Market Today: Futures Surge, Bonds Tumble as Trump Nears Victory Investors are piling into trades linked to a potential Trump victory

… AND so it (re)begins … separately, we ALSO learned more ‘bout ISM Services …

ZH: Rate-Cuts? ISM Services Soars To 27-Month-Highs

… we ALSO know what folks thought of 10yr USTs ahead of the elections …

ZH: Yields Slide After Solid, Stopping Through 10Y Auction

… whether or not this is any indication of what’s to come later on today with $25bb new issue 30s … and for somewhat MORE from someone with a Bloomberg license …

NEWSQUAWK: US Market Open: Election results indicative of Trump Presidential & Senate victory; House too close to call … USTs pressured and Bunds bolstered by the Trump Trade; US curve markedly steeper, attention on the House result to see if this continues … USTs are pressured, with Trump set to return as President with control of the Senate and a projected ~60% chance of having House control as well; though, the House remains far too close to call and as it stands, we may not have an answer for several days or even weeks. The Trump Trade is in full swing for bonds with USTs at a contract low of 109-07, vs a 110-21+ initial high print for the session. However, if this narrative moves to a Trump ex-Congress (i.e. Rep. Senate but a Dem. House) government, then we may see a fading of the steepening in favour of flattening.

Opening Bell Daily: Trump win fuels everthing rally. Trump wins and the Trump Trade is now an everything rally. Investors poured into stocks, crypto, and memetokens overnight to position for a second Trump White House.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ both before and now AFTER the election results appear to be IN and final ‘ish …

ABNAmro: Republican sweep raises risks to the outlook | Insights newsletter

Republican clean sweep makes it significantly easier to implement full policy agenda. Risks very firmly tilted to the downside for US and global economic growth and to the upside for US inflation. While Fed policy could be tighter than our current base line, the ECB could cut rates faster. Republican sweep sets the stage for US-European rates divergence. Parity for EUR/USD could be on the cards. We will publish an updated macro and market base scenario later this month.

Investors Generally Like November The long-term upward trajectory in the U.S. stock market has its foundation in the country's democratic political system (remember to vote today!) and its market-based, capitalist economic system. In theory, the stock market efficiently allocates the nation's capital to generate solid investment returns. Theory typically turns into reality in November, which since 1980 has been the best month for equity performance, with an average 2.1% gain, ahead of April (+1.60%), July (+1.4%) December (+1.3%), and October (+1.3%). November's batting average is high as well: stocks advance during the month 72% of the time. The best Novembers have been 1980 (+10.2%), 2001 (+7.5%), 1996 (+7.3%), 1985 (+6.5%), 1998 (+5.9%), and 2002 (+5.1%). But there have been some clunkers: 2000 (-8%), 2008 (-7.5%) and 1987 (-5.9%). Last year, the S&P 500 rose an impressive 8.9% for the month. What about during presidential-election years? Good question. The track record is even more impressive here. For the 11 election-year Novembers since 1980, stocks have, on average, climbed 2.6%. November usually starts off at a fast pace, as nonfarm payrolls are reported and many companies are still reporting 3Q earnings. This year, the Fed meets this week and will likely lower rates again. The presidential election will undoubtedly be close, and may take a few days to produce an eventual winner -- but that doesn't have dent November's long-time track record.

BARCAP: Services ISM hints at November jobs rebound

The ISM services PMI registered another solid month in October, rising to its highest level (56.0) since the summer of 2022. Today's readings, which were likely submitted in the weeks following October's payroll survey reference week, hint that the sharp slowing in services employment was hurricane-related and short-lived.

BNP: BNPP US Election Tracker: Back to the (Trump) future? 06 Nov 2024 07:13 GMT

KEY MESSAGES As at the time of writing, US election results point to Republican control of the Senate as well as a high likelihood of a second Donald Trump presidency. Some time may be needed to determine whether Republicans will have a majority in the House of Representatives.

The US president has significant leeway to act on tariffs alone, whereas more expansive changes to fiscal policy and immigration will depend on final margins in Congress.

Overall, we think likely policy measures will be net inflationary, with a more mixed impact on growth.

For the rest of the world, tariffs and uncertainty about trade and foreign policy mean downside risks to economic growth, with a more ambiguous inflation impact…

…In rates, before the outcome of the House is known, we prefer to be long 5y breakevens. Should a Red Wave be confirmed, there is scope for yields to rise further in the back end of the curve….

…US rates: Long 5y breakevens With the information on hand, the US rates market continued its recent trend of higher yields, higher real yields, wider breakevens, steeper curve and tighter spreads.

These market moves very closely mimic the moves right after the 2016 election, which ended with a Trump victory and Republican sweep. While 2016 serves as a good template, there are two key differences versus 2016.

Higher inflation sensitivity: Given the inflation surge in 2021-2022, rates investors currently have a heightened focus on inflation risks compared with 2016. This focus is furthered by President Trump’s campaign that floated significant tariffs, and tighter immigration. This inflation focus – especially with high odds of President Trump winning – could help breakevens to continue to widen. Breakeven widening could be supercharged if a Red sweep scenario materializes – and investors have to contend with inflationary impacts of fiscal stimulus in addition to tariffs and immigration.

More bond vigilantism: Another contrast to 2016 is that markets have been more sensitive to the US’s fiscal deficit picture. Any future plans of fiscal expansion – via tax cuts or otherwise – will see a meaningful reaction in wider term premiums and higher yields. However, this term premium expansion will ultimately depend on whether the US House has a Republican majority or not.

For now, we favor going long 5y breakevens, and hold back on being short duration until the odds of a Republican sweep rise.

It's been a big night with Mr Trump looking set to become just the second President to serve non-consecutive terms in history, and the first for well over a hundred years, after Grover Cleveland in the late-19th century. So a likely remarkable political comeback after an approval rating in the low 30 percent range when he left office in January 2021…

In celebration of election day, today’s chart highlights the movements of long-end yields around previous presidential elections. The chart shows the trajectory of 30y yields in the workdays around presidential elections dating back to 1984, with Democrat victories shown in blue and Republican victories shown in red. For each data series, the change in 30y yields is relative to the level at the close of each election day.

There are two notable outliers in the data set. The first is the election cycle that saw significantly higher yields following a Republican victory, which represents the market reaction after Donald Trump’s surprise victory in the 2016 election. The second is a Democrat victory (the series that drops off the y-axis on the 12th workday after the election), which represents the market reaction after the 2008 election. Since that election occurred at the time of the global financial crisis, the decline in yields likely had less to do with the election and more to do with economic conditions and the policy response to the crisis.

As seen in the chart, the long-end has tended to cheapen in the aftermath of Republican victories, with 4 of the 5 such examples in the sample resulting in higher yields in the 10 workdays following the election. The lone exception to this rule was George W. Bush’s victory over Al Gore in the 2000 election. This election being the outlier makes sense given the unique circumstances around recounting ballots in Florida, which created some initial uncertainty regarding the winner of the election. For Democrat victories on the other hand, 30y yields tend to fall after an initial period of fluctuations, with all 5 examples in the sample seeing lower yields by the 10th workday following the election. When comparing these two patterns, the chart suggests that the decline in 30y yields after a Democrat victory tends to persist for longer compared to higher yields after a Republican victory.

DB (Saravelos): More thoughts - the Trump policy mix is not priced

…The policy mix is NOT priced. We should stop debating if "Trump is priced" given that the election is now behind us. The key question now is what policy mix is priced. In our view, the market is currently reflecting a very moderate policy mix in terms of the size of fiscal easing and tariffs. This is true across the board in FIC markets: terminal Fed Funds are still below 4% (they could easily be at or above); ECB pricing is closer to 2% than 1% (should be at 1.5% at a minimum); inflation swaps in the US are barely pricing a tariff-driven inflation hump; there is still little term premium in fixed income; the dollar is pricing no tariff risk premium on our models and European sector credit performance is not reflecting tariff risk.

To sum up, if the Trump policy platform goes ahead, there is still much more to go in the dollar and broader FIC market pricing, in our view.

As Donald Trump performs better than many polls had predicted, the market is bracing for a clean sweep for the Republican candidate, with 10Y UST yields rising beyond 4.4%. The eurozone has reacted with a bull steepening as more ECB rate cuts are priced in again. But the wider risk sentiment seem to hold

Donald Trump’s victory will ensure a lower tax environment that should boost sentiment and spending in the near term. However, promised tariffs, immigration controls and higher borrowing costs will increasingly become headwinds through his presidential term

MS: US Public Policy Brief: US Election: A Red Reminder November 6, 2024 07:19 AM GMT

While the presidential election has not yet been officially called, we see a clear path to a Republican White House & lingering potential for Democrats to control the House of Representatives yielding 'divided' government, warranting key reminders for investors about policy paths and market impacts.

At the time of recording, the US Senate has been called for the Republican party, and the House and presidency remain open. Financial markets have moved to price a victory by former US President Trump. However, markets appear to assume that the campaign rhetoric (specifically around deportations and tariffs) will not fully translate into policy.

The second most pressing concern of voters, according to exit polls, was the economy. This does not refer to abstract concepts like GDP, but to perceptions of economic wellbeing. Evidence before the election suggested that inflation perceptions were a significant economic concern. Inflation perception is a complex topic—entire books have been written on it—and investors may need to focus on the heightened political sensitivity of the subject…

Wells Fargo: ISM Riddle for the Fed: Service Activity Soars as Factories Slump

Summary The service sector is expanding at as fast a pace as it has since early 2022 as the gap between service sector activity and manufacturing activity widens to a degree only seen once before in records dating back to the 1990s.

We may not know tonight who will be the next president, but we should know which party will win a majority in the Senate and the House. It appears that Republicans are likely to do so. In this case, a Harris administration would be gridlocked, while a Trump administration would have more power to implement his policies, including higher tariffs (raising inflation risks) and lower taxes (ballooning the federal deficits). That could push the 10-year yield up to 4.75%-5.00%, which should attract lots of buyers.

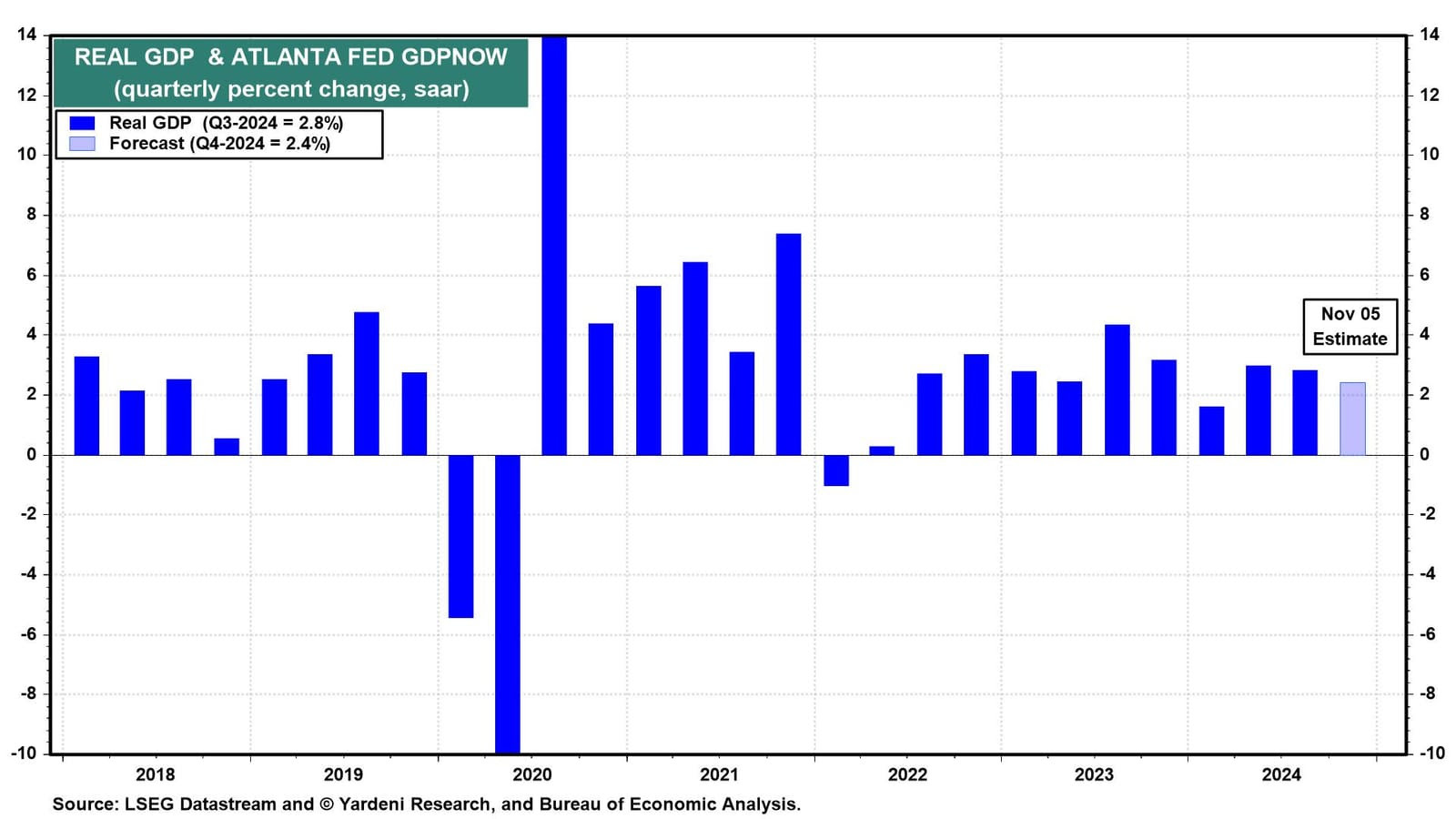

Meanwhile, the Fed is widely expected to cut the federal funds rate (FFR) by 25bps on Thursday. If we were on the Federal Open Market Committee (FOMC), we would strongly dissent in favor of a pause. By most measures, including today's nonmanufacturing PMI report, the economy has been roaring even before the Fed's September 18 meeting when the FFR was cut by 50bps (chart).

When the Fed cut by 50bps rather than 25bps on September 18, we immediately concluded that was too much, too soon. The Bond Vigilantes have agreed with our assessment, raising their expectations for long-term inflation and taking the 10-year US Treasury yield from 3.65% on September 16 to 4.44% this evening (chart).

Only one FOMC member dissented from the September 18 decision, favoring a 25bps cut. There are likely to be more dissenters at this week's FOMC meeting. They may prefer not to fight the Bond Vigilantes for now given the strength of the economy and vote in favor of no cut on Thursday. Without commenting on political matters, they might fear that the US elections will result in persistent and large federal budget deficits despite strong economic growth…

Since the Fed began to raise interest rates in March 2022, the FOMC has constantly expected the economy to slow down, see chart below. But it still hasn’t happened. In this Daily Spark, we discuss why.

Bloomberg: Traders Load Up on Last-Minute Rate Bets on Treasury Rally

Options, futures, cash positions are all turning bullish

Wagers seen as hedging a potential Harris presidential win

OH....WHAT A NIGHT !!!!!!!!!

UNBELIEVABLE !!!!!!!!

https://youtu.be/bzZufxcPwZE?si=dw9UuhrbyQIiS6xd

The Impossible Dream (The Quest)

By Andy Williams