Good morning … Tariffs continue to be the word of the day and yesterdays news (?) after market close caught SOME off guard (given autos took a hit in after-hours trading) …

Wed, Mar 26 20256:20 PM EDT CNBC: Trump announces 25% tariffs on all cars ‘not made in the United States’

… followed by even MORE sabre rattling …

Mar 27 20253:02 AM EDT CNBC: Trump threatens ‘far larger’ tariffs if EU and Canada unite to do ‘economic harm’ to the U.S.

… and the world begins (?) responding …

Mar 27 20254:44 AM EDT CNBC: Germany slams Trump’s 25% auto tariffs as bad news for U.S., EU and global trade

… and …

March 27, 2025 at 2:26 AM PDT Reuters: Valeo to raise prices as a result of Trump's 25% tariffs on car imports

… and the ping-pong game goes on and am sure, nearly certain, that UNcertainty has not yet left the building …

March 27, 2025 at 1:00 AM PDT Yahoo: The Fed has a new favorite word: 'Uncertainty'

… and so … head HEREto see latest updated “Economic Policy Uncertainty” index (or HEREon FRED if you wish instead) …

For now, though … #Got7s? Want some?? A look at where we’ve been in effort to figure where we’re possibly going …

7yy DAILY: is 4.28% going to be IT … where IT is the ‘dipORtunity’ detailed…

… as momentum nearing an overSOLD ‘sell’ and downtrending line, interest to cover short and consider a rental certainly comes to mind here / now …

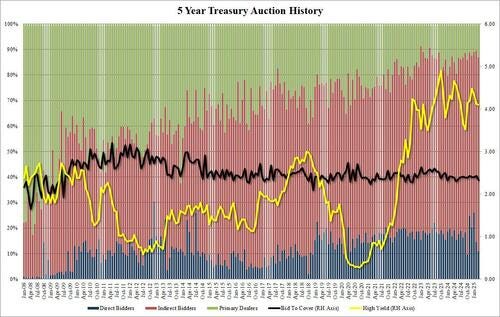

… and this on heels of a very much MIXED 5yr auction …

Hot on the heels of yesterday's stellar 2Y auction, moments ago the Treasury sold $70BN in 5 year paper in an auction which may not have been quite as impressive at first sight, but which was nonetheless just as solid when taking a closer look below the surface…

…The bid to cover was also a bit on the light side, sliding from 2.42 in February to 2.33, the lowest since May 2024.

But this is where the weakness ended, because the internals were probably the strongest since middle 2024: Indirects were awarded 75.84%, the highest since October and well above the six auction average of 69.3%. And with Directs dropping to just 10.97%, which was the lowest since last October, and well below the 18.9% recent average. This left 13.2% to Dealers, up from 10.6% in February and the highest since, you guessed it, October.

… for somewhat more from that site with a Terminal …

… the price action above is on heels of some funDUHmental inputs.

Wednesday, Mar 26, 2025 - 12:42 PM ZH: Recession Canceled... Again: US Durable Goods Orders Back Near Record-Highs In February

…Not exactly recessionary signaling. Of course, the first excuse out of every talking heads' mouth will be "well it's front-running Trump's tariffs... and won't be sustainable" - we shall see (and why didn't the forecasting analysts see that coming?).

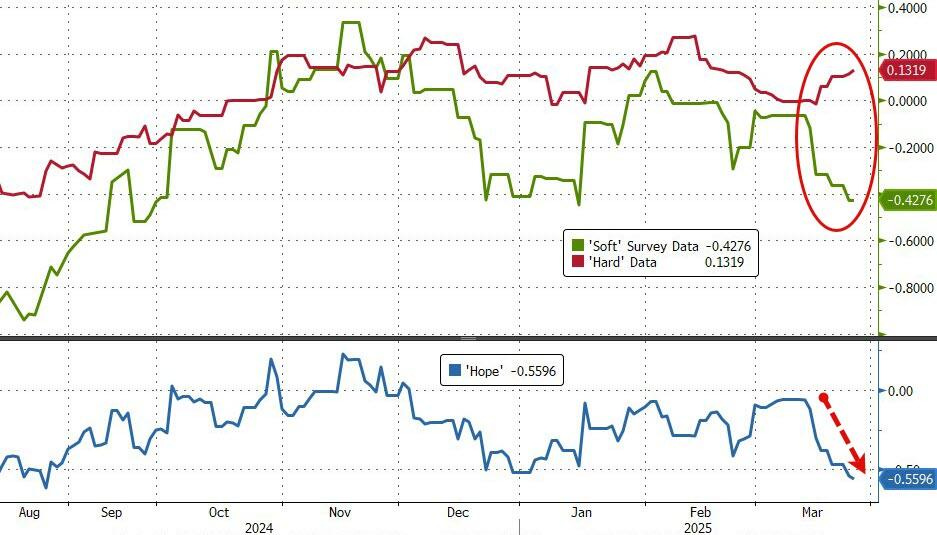

The partisan 'soft' data to non-partisan 'hard' data decoupling continues to grow.

… here is a snapshot OF USTs as of 725a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries have trended lower throughout the overnight session on moderate selling pressure, with Gilt weakness and a supply overhang (>40bn in IG issuance) weighing. The selling subsided momentarily in early London on bund strength, before differential widening resumed with 10y US-Gmy >160bps. Selling was seen from real$ in intermediates and TYs, with the latter contract now below CTA sell levels. Interest to buy dips was noted as moderate, although the desk saw light interest to buy the front end (2-3yr sector) from CBs. From fast money they've also seen interest in flattening expressions, 2/10s and 3/10s, mainly. Overall volumes are elevated as we await the third read on GDP, claims and the 44bn 7-year auction. Crude is -0.3%, Copper flat, DXY -0.1%. S&P futures are showing -2pts here at 7am, with Eurostoxx underperforming.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: European bourses hit on auto tariff rhetoric, DXY mixed vs peers while EGBs & USTs diverge … USTs meanwhile find themselves in the red, with yields picking up on the global and US inflationary implications of such action, as such yields are firmer with the curve steepening ahead of data and 7yr supply; a sale which follows a robust 2yr and more a tepid 5yr outing earlier in the week.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

A global monthly note with an section on the USofA …

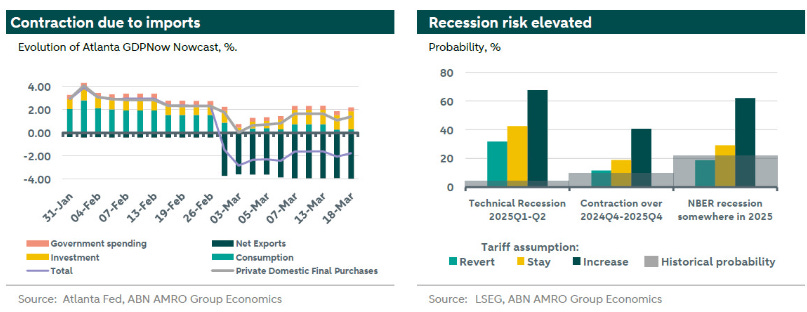

26 March 2025 ABN AMRO: The reports of a contraction are somewhat exaggerated

Import frontloading depresses 2025Q1 GDP nowcasts, while private domestic demand remains solid. This increases the probability of a technical recession, especially if further tariffs arrive later in Q2. Recession probabilities marginally elevated with current policy, with upside risks if tariffs are increased.

AHhhhhdooorables …

26 March 2025 Barclays: Durable goods orders: Stocking for a storm

New durable goods orders posted a surprise 0.9% m/m gain, reflecting a surge in new orders for motor vehicles and parts amid anticipation of tariff-related disruptions. Even so, capital goods orders weakened, hinting that a drag on fixed investment from policy uncertainty could be taking shape.

Same shop on Chinese data overnight …

27 March 2025 Barclays: China inflation: Low for longer

The situation facing Chinese households has worsened amid a deteriorating labour market and significant debt service burdens. A new trade war would be deflationary, as it would exacerbate overcapacity.

… We see a rising risk of persistent and low inflation (or even deflation) in the coming years, in view of severe and widespread excess capacity and structural weakness in consumption and property investment, which collectively account for ~70% of GDP. Moreover, we think a potential new trade war between China and the US would, on balance, have a deflationary effect, given that downward pressure on exports would exacerbate China's problems with overcapacity.

Overall, we expect China's CPI inflation to stay low and PPI deflation to persist, barring a surge in global commodity prices.

France on Liberation Day …

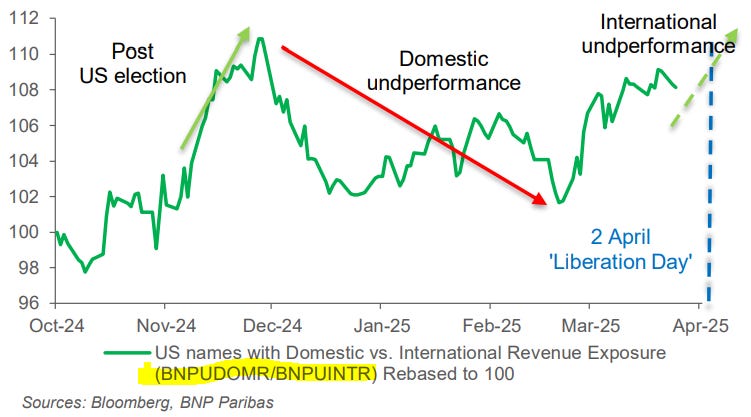

26 Mar 2025 BNP: US equity derivatives: Hedging ‘Liberation Day’

Growth and tariff risks looming: In our Outlook (Late Cycle Exuberance, dated Dec. 20th 2024) we suggested that bullish hopes for 2025 were at risk of being derailed by a more immediate focus on tariffs. And the first year of Trump's second term might resemble 2018 more closely than 2017. April 2nd ‘Liberation day’ tariff deadline is an important catalyst for that view heading into Q2. Post-election, we saw a rotation from International to Domestic stocks (see fig 1. International vs Domestic Revenue baskets - BNPUDOMR/BNPUINTR). That outperformance faded into year end. Recently, Domestic stocks have again begun to outperform those with higher international revenues. We are highlighting hedging ideas in this piece for investors anticipating tariff related turbulence for equities, particularly in Internationally exposed stocks.

Fig. 1: Tariff risks could particularly threaten US names with high exposure to international revenues

Headline Durable Goods Orders unexpectedly rose +0.9% MoM in February's preliminary estimate. This beat the -1.0% MoM BBG consensus and nearly all of the economists' estimates in the survey. Moreover, January's initial read of +3.2% MoM was revised up to +3.3% MoM. Ex-Transportation, the move was +0.7% MoM vs. +0.2% MoM estimated, and 0.0% MoM prior was revised up to +0.1% MoM. Core Orders (non-defense capital-goods ex-aircraft) unexpectedly fell -0.3% MoM vs. +0.2% MoM surveyed and +0.8% MoM prior was revised up to +0.9%. Note that this is the first decline since October 2024. Core Shipments (a proxy for equipment investment within the GDP calculation), came in at +0.9% MoM vs. +0.2% MoM expected, and -0.3% MoM prior was revised up to -0.2%. This is the largest monthly gain in a year, and consistent with solid business equipment spending estimates for Q1 GDP…

… YESTERDAY was an updated S&P call (Barclays) and today an updated RATES call …

We expect rates to stay in a range near term. Treasury yields could decline modestly in Q225 to reflect tariffs’ negative impact on growth and the Fed resuming rate cuts in June and September in our macro forecast.

Rates could rise in H225, if and when President Donald Trump’s progrowth policies, such as tax cuts and deregulation, come into effect.

In our forecast, rates continue to grind higher in 2026, but are capped below 5.00%. Our 10Y 2026 year-end target is now 4.75% vs 4.95% in the prior forecast to reflect a less optimistic growth outlook.

…Market participants have re-calibrated the future rate path since the beginning of 2025. As suggested by Fed Chair Jerome Powell at the March FOMC meeting press conference, the Fed is on hold for the time being, and is in “no hurry” for further action. Still-elevated Trump 2.0 policy unknowns mean that the economic outlook is far from certain, contributing to a cautious stance for the Fed. On macro, tariffs have led to expected weakening growth and sticky inflation. The labour market has cooled, albeit gradually. Our macro forecast expects the Fed to cut the policy rate by 25bp at each of the June and September FOMC meetings, compared to a slightly more dovish market pricing around 62bp easing for the balance of 2025 (see Figure 1)…

Make of this newly minted and LOWERED BUT HIGHER than current f’cast.

German bank note asking an intriguing question which harkens back TO … That ‘70s show … as in 1973 …

26 March 2025 DB: Making the implausible happen again?

Could the implausible happen again: a US recession without a much lower 10-year Treasury yield? We think, yes.

Typical US recessions are triggered by negative demand shocks, usually resulting from tight monetary policy. Weaker demand translates into lower inflation and a higher unemployment rate, allowing the Fed to ease policy substantially, thereby lowering the 10-year Treasury yield.

If tighter fiscal policy generates a negative demand shock, the same logic is likely to apply. However, there is so far scant evidence that current US policies have resulted in any material fiscal tightening. On the other hand, we see early evidence that trade policy could trigger a negative supply shock that would raise both inflation and the unemployment rate. As pointed out a few weeks ago, this outcome is increasingly reflected in consumer expectations.

Unlike a more "traditional" negative demand shock, it is not clear that a negative supply shock should result in a lower 10-year yield. Indeed, the Fed may be unable to ease policy due to rising inflation expectations. If the Fed nonetheless eases monetary policy, term premia should rise substantially because of likely persistently high inflation.

This is exactly what happened in 1973, the one instance in recent US history of a recession triggered by a negative supply shock. At that time, the Fed initially hiked rates despite the US economy being in recession. When the Fed subsequently eased despite still-elevated inflation, the term premia rose substantially. The net result: the 10-year Treasury yield was more than 125bp higher at the end of the recession than just before it started.

… and from the implausible to the, well, plausible …

26 March 2025 DB: A little reciprocity goes a long way

Next week on April 2nd, the Trump administration is set to deliver long-awaited details around its tariff plans. While substantial uncertainty remains around what will be announced, recent news reports and indications from the administration have provided somewhat greater clarity on the potential scope of what will be delivered. In this piece, we trace out a few scenarios for outcomes of next week’s announcement.

Our analysis focuses on the top 15 countries formally identified for investigation by the USTR in public filings and as measured by the value of 2024 goods imports. These 15 trading counterparts account for over 85% of US goods imports and all have persistent goods surpluses with the US.

We also concentrate on the "reciprocal" tariff rate, which we quantify as the weighted average tariff rate of each country and an additional penalty for each country's VAT. Recall that the VAT was specifically cited in Trump's executive order as a discriminatory "non-tariff barrier".

We estimate that "reciprocal" tariffs could add roughly 4 (best case) to 14ppts (worst case) to the overall US tariff rate relative to its 2024 level of 2.5%. The hit to 2025 real GDP growth could be as little as -25bps to as high as 120bps. For core PCE inflation, the impact is nearly the mirror opposite as reciprocal tariffs could add anywhere from a couple of basis points to potentially 1.2ppts. Importantly, these impacts are additional to the risks to growth and inflation from previously announced tariff actions.

Plausibility aside, a few words from none other than Jim Reid himself on 10s yesterday and what MAY have been behind push HIGHER in yield …

… Elsewhere, the tariff news also saw copper futures (+0.64%) rise to a record high, which followed Bloomberg’s report that US copper tariffs could happen within several weeks, which would be much sooner than the 270-day deadline for the investigation launched last month. So that added to fears about inflationary pressures, pushing the 10yr Treasury yield (+3.9bps) up to a one-month closing high of 4.35%. Matters also weren’t helped by a fresh rise in oil prices, with Brent crude (+1.05%) up to its highest level so far this month, at $73.79/bbl. So by the close, the US 1yr inflation swap was up +3.5bps to 3.02%, only just beneath its recent closing peak of 3.05% last month. Higher yields and the risk-off tone helped the dollar index (+0.33%) rise to its highest in three weeks …

More on this BBG story below … finally (at least for the time being) on rules of engagement with regards to policy makers and tariffs …

26 March 2025 DB: When is it ok to break the (policy) rules? The Fed's response to tariffs

We build on our recent note outlining growth and inflation scenarios in response to potential tariff announcements next week (see "A little reciprocity goes a long way") by discussing the implications for the Fed this year. Under milder tariff outcomes (defined in this note) we see scope for the Fed to keep rates on hold this year, in line with our current baseline. These scenarios broadly look similar to the Fed's median projections from March, but with somewhat higher inflation.

However, under more aggressive tariff scenarios, we see material risk of a recession. In this case, we would expect the Fed to "look through" tariff-driven inflation and focus on a weakening labor market, as long as inflation expectations were not unanchoring. We argue that this could be a scenario where the Fed should break the (policy) rules, which in some cases argue for keeping rates steady or even raising rates this year.

A few words (and some my fav visuals / slides) from THE cross-assets ‘playbook’ …

March 26, 2025 MS: Cross-Asset Playbook: In Search of Late-Cycle Defensives

Macro – Diverging Growth Narratives Policy uncertainty pulls forward growth risks in the US, but reacceleration in prices means the Fed only cuts once more this year. Europe sees potential for growth upside from recent fiscal announcements. China’s macro outlook is improving, but reflation remains gradual.

Markets – In Search of Late-Cycle Defensives Risks are rising as the market lurches into late cycle, and we think the skew of outcomes is for equity and credit risk premiums to rise. It’s a good environment for defensives, but rich equity and credit valuations, uncertainty over the type of macro slowdown, and conflation of secular and cyclical trends complicate calculus.

Strategy – Stay Nimble, Stay High Quality We stay OW high-quality fixed income (e.g., USTs, Agency MBS, IG corporate credit, CLO AAA). We are EW global equities on middling risk/reward; we like Japanese stocks and see US tactically outperforming Europe. We continue to like credit vol as a cheap downside hedge even after the recent sell-off.

So confidently put that ALL things ‘47 does is wrong and going to sink the economy…here, this next note suggests tariffs are one way ticket to Doomsville via higher taxes for ALL in every way / shape and form … both realized and even unimaginable ways … FACTS, they say. We’ve all got a right to our own individual OPINION but NOT our own set of FACTS. That said …

US President Trump announced an aggressive tax increase for US consumers, with a 25% tariff on imported cars. Officials later clarified it also covers car parts. The tax will raise US inflation and lower growth, but the full impact will take time.

It is tempting but incorrect to compare the 25% tax with the 24% post-pandemic auto price increase. The tax applies to import prices but not later supply chain costs—consumer prices will rise less than 25%. US consumers will likely hold onto their existing cars for longer, and may switch to buying used cars, so used car prices will rise. Higher new and used car prices eventually increase auto insurance prices—this tax affects people who do not buy a car at all.

Slower US growth will impact car exporters to the US. Whether car exporters lose market share depends on how US companies react. If US car manufacturers raise prices using tariffs as an excuse, there is less of a growth hit to the rest of the world.

Final 4Q GDP data is due from the US, and is expected to be stable at around trend growth. February US wholesale and retail inventory data becomes more important—inventories have the potential to offer short-term relief from the tax increases.

… same shop on … AHhhhhdooorables …

26 March 2025 UBS: Durables report solid amid uncertainty

Core orders a little softer but shipments improve in February

… These are the data where we would expect to see whether uncertainty or trade tensions are weighing on business expansion plans or investment. In the 2000s, these series proved useful for following the deterioration in business sector activity ahead of the downturn. In our prior writings recapping the research literature of the economic impact of policy uncertainty, these were the most timely components of business investment, which paused for several quarters during the tax policy uncertainty in 2011-2012. The level of core orders still remains above its December level by 0.6% despite the softening in February, potentially signalling we aren't yet seeing a major reversal in investment trends at this juncture. But the decline in February was the first in four months, so we will continue to monitor these data closely.

… AHhhhhdooorables …

March 26, 2025 Wells Fargo: Upside Surprise in Durables Looks More Rebound than Recovery

Summary Durable goods orders came in better than expected in February, but strength was due to aircraft specifically, and the underlying orders trend remains weak as businesses are hesitant to invest amid increased economic uncertainty. A rebound in durable shipments, however, suggests equipment investment will be solid in the first quarter.

… Durable goods orders surprised to the upside in February. Despite the Bloomberg consensus of 59 forecasters looking for a 1% drop in orders, total orders rose 0.9% with some modest upward revisions to the previous month of data as well…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Here’s an important note on Dr Copper and tariffs that MAY have something to do with YESTERDAYS rise (DB above) in yields …

March 26, 2025 at 11:02 AM UTC Bloomberg: Trump Weighs Imposing Copper Import Tariffs in Weeks, Not Months

US tariffs on copper imports could be coming within several weeks, months earlier than the deadline for a decision, according to people familiar with the matter. Copper traded in New York rose to a record…

Which followed by …

March 26, 2025 at 8:51 PM UTC Bloomberg: Copper’s Hottest Trade Risks Painful End If US Tariffs Arrive Early

… The global copper market was turned on its head in January when Trump first talked about imposing tariffs on imported copper. Now, there’s fresh angst after Bloomberg reported that the US administration aims to introduce levies within weeks instead of months as had been widely anticipated …

… So goes Dr Copper then so goes … <insert whatever narrative you’d like HERE>

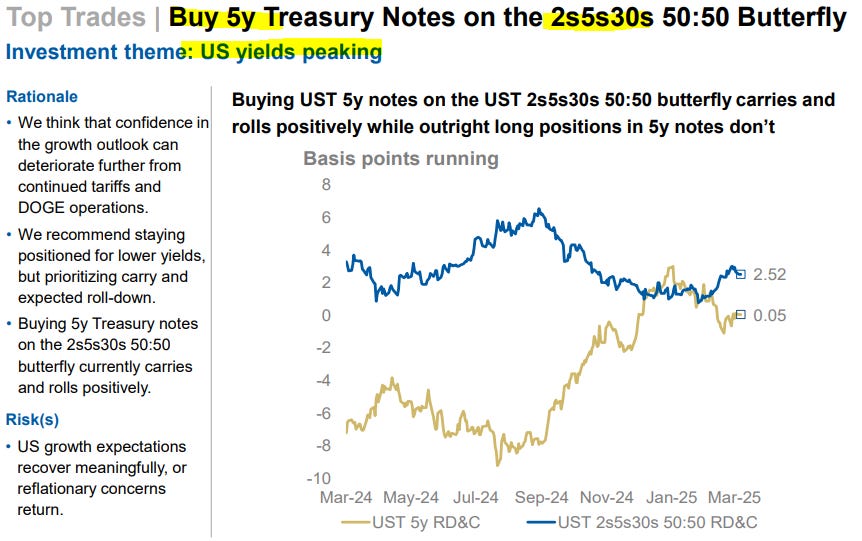

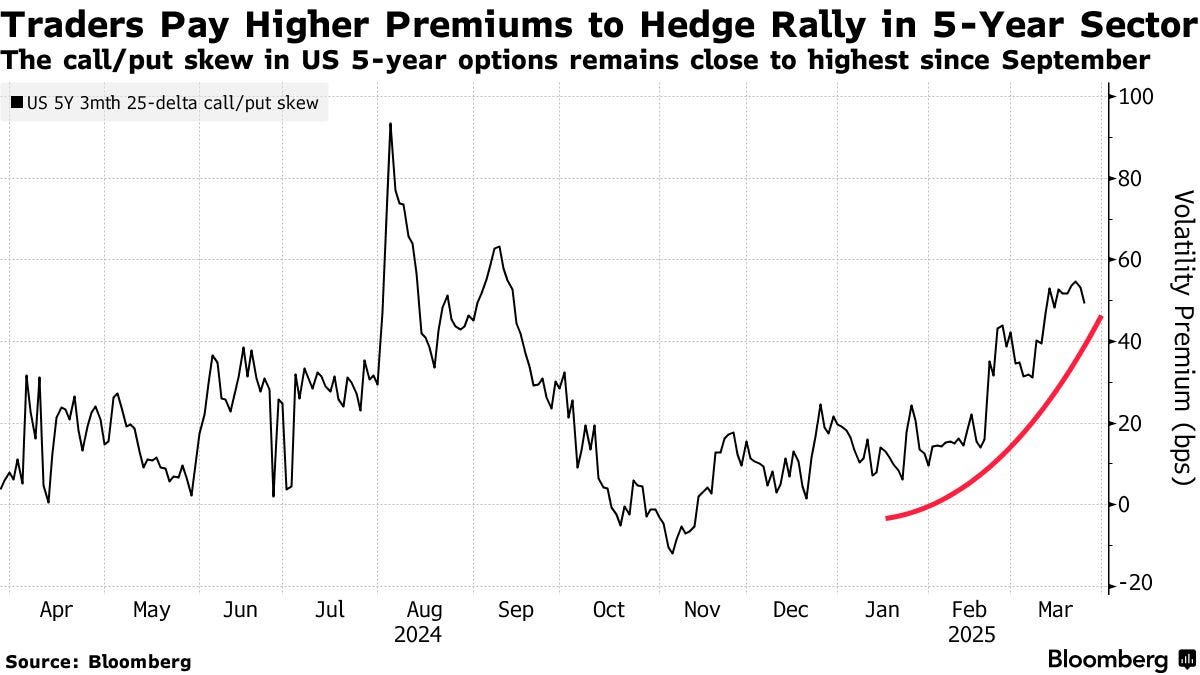

On heels of yesterday’s 5yr auction, this one caught my eye …

Bloomberg: Five-Year Treasuries Are the Go-To for Wall Street’s Risk-Averse

A popular trade is gaining even more steam in the Treasury market as tariffs muddy the Federal Reserve’s interest-rate path and concern builds around US growth: Buy five-year notes.

Leading up to President Donald Trump’s April 2 deadline on levies, the options market shows a preference by traders to own exposure to US government debt due in five years. That high demand has pushed the extra cost of owning options that’ll pay out if those notes rally has risen to the highest since September.

“The five-year sector should benefit the most from a Fed that might be late to start to cut rates due to higher inflation,” said Priya Misra, portfolio manager at JPMorgan Asset Management. “The longer the Fed waits, the more they will need to cut more in totality.”

Five-year notes have been touted across Wall Street in recent months as an attractive offering among Treasuries, in large part because of their relative resilience to dual risks. By contrast, two-year notes are ultra-sensitive to the Fed’s interest-rate policy, while those maturing in 10 and 30 years tend to be more vulnerable to concern about US economic health and ballooning deficits.

Goldman Sachs recently pointed to the balance of safety offered by the five-year sector. Barclays, Morgan Stanley and Wells Fargo have all touted the so-called belly of the curve since the latest Fed meeting.

Finally, from The Terminal.com, a note on potential BASIS TRADE BAILOUT …?

March 27, 2025 at 1:00 AM UTC Bloomberg: Fed Urged to Mull a Hedge Fund Bailout Facility for Basis Trades

The Federal Reserve should consider setting up an emergency program that would close out highly leveraged hedge-fund trades in the event of a crisis in the $29 trillion US Treasuries market, according to a panel of financial experts …

… The key source of risk to address is the so-called basis trade, where hedge funds seek to profit from tiny price gaps between Treasuries and derivatives known as futures. Kashyap told reporters that “it’s a pretty concentrated trade,” involving perhaps 10 hedge funds or fewer.

If hedge funds need to unwind their positions quickly, the danger is that bond dealers may not be able to handle the enormous sudden volume of transactions. When the Fed had to intervene in 2020, the basis trade was roughly $500 billion in total — just half today’s figure.

“To relieve the stress on dealers, it would be sufficient for the Fed to take the other side of this unwind – purchasing Treasury securities, and fully hedging this purchase with an offsetting sale of futures,” the authors wrote…

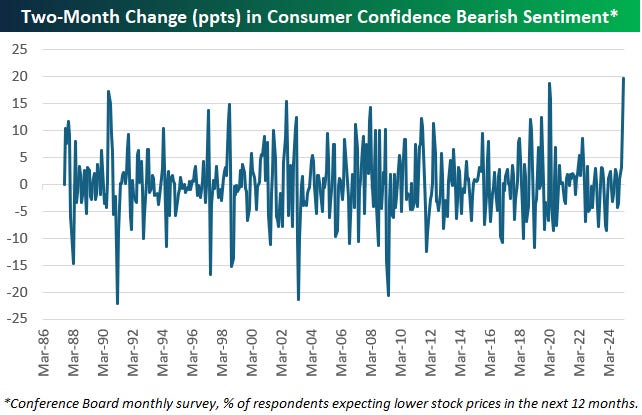

This next visual quite gripping and recession’istas going to be passing this one ‘round like a hot potato …

BESPOKE: Biggest 2-Month Jump in Bearish Sentiment Ever

The results from the Conference Board's monthly Consumer Confidence survey were published yesterday and showed an extreme shift from bulls to bears when it comes to stock market expectations. In the history of the survey dating back to 1987, the two-month jump in consumers expecting lower stock prices in the year ahead was the highest on record! As a reminder, investor sentiment is typically viewed as a contrarian signal. We covered forward stock market returns after big jumps in bearish sentiment in yesterday's Chart of the Day that you can view with a new membership.

… remember, watch what they say and whatever they do …

Confirming (?) there’s not much there there … here … yet …

March 26, 2025 LPL: Weakness, But No Recession Yet

…Conclusion The economy is probably not in recession at this point, but the uncertainty about Fed policy, interest rates, inflation, and trade wars put a damper on how consumers and businesses feel about current conditions. However, tracking the hard data can give us a fuller sense of how society is doing. One stat to monitor is unemployment claims, which we expect to rise if we are getting closer to recession.

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities, with a preference for the U.S. over emerging markets, growth over value, and large caps over small. However, we do not rule out the possibility of additional short-term weakness, as the pace of growth is cooling, and trade policy and geopolitical uncertainty remain high. While the risk-reward trade-off for beaten-down stocks has clearly improved, a swift and sustainable recovery seems unlikely under the cloud of trade uncertainty. We continue to monitor tariff news, economic data, earnings estimates, and various technical indicators to identify a potentially attractive entry point to add equities.

Finally … every single baseball fan / player today waking up BE LIKE THIS …

{kind=link}