while WE slept: USTs bull steepen, light volume, w/RM buyin' 20s; 10yr streak; bond vigilantes engaged; a few 'fav charts' and more. happy holidays and new year!

Good morning … this will be final installment until after XMAS and may very well be until 2025 and so, thank you to all for stopping by. HOPE markets have treated you fairly in 2024 and wishing you all very best as page in the calendar turns and 2025 is your best ever.

I hope you find whatever it is you are looking for … while visuals offered HERE (yest) clearly far better than my current limited capability, if you are searching for a general look at 10s, for example, this may be the reason you came in today …

10yy: 4.60% has no noticeable, obvious importance but …

… in that we generally like ‘round numbers AND momentum seems stretched into overSOLD territory, well … a press above 4.60% — time for Fed to CUT rates again, yet??

AND we’ll see how this plays out over coming days / week and in the meanwhile, a quick recap of the day and news which ultimately made UP the price action …

ZH: Jobless Claims Improve, Q3 GDP Revised Higher, But Another Manufacturing Survey Collapses

ZH: US Existing Home Sales Surged In November, But...

ZH: Trump Effect? US Leading Economic Indicators Positive For First Time Since Feb 2022

ZH: Bonds & Bitcoin Battered Despite Soft Data Slump; Gold & The Dollar Jump

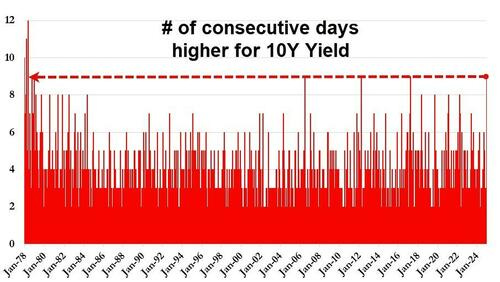

… 10Y yields have made higher highs for 9 straight days - the last time it rose for 10 straight days was in 1978...

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are bull-steepening in quieter conditions, franchise flows again skewed towards better buying from real$ in 20s, the sector’s out-performance on the curve easing slightly. The gradually richening in London has been driven by 5s, reversed some of yesterday’s acute cheapening on the fly (2s5s10s -2.5bps). Ahead of PCE, overall convictions remain light with our desk reporting better interest to add duration on the balance heading into year-end. Risk-off conditions are prevailing in equities with S&P futures showing -47pts here at 6:45am, Crude -1.2%, Copper flat, and the DAX -1.5%. Bunds and gilts are bull-steepening in-line with USTs, mild peripheral underperformance seen, while the DXY has backed off -0.2%, USDJPY backing off the 157-handle overnight.

… We’ve included the weekly chart of 2s10s in today’s chart pack as well, showing how the multi-month consolidation pattern from late-SEPT has now been resolved steeper in a familiar ‘falling wedge’ continuation pattern, arguing for a steepening move towards the 42bp level in the medium-term …

… and for some MORE of the news you might be able to use…here are some resources and curated links for your dining and dancing pleasure …

NEWSQUAWK: Stocks continue to slide on Quad Witching, USD edges lower ahead of PCE & Fed speak … USTs and Bunds are incrementally firmer but ultimately contained into PCE and Fed speak … USTs are modestly firmer but yet to significantly deviate from the unchanged mark in 108-19+ to 108-26+ parameters. Docket ahead features monthly PCE data before the docket turns to Central Bank speak with Fed’s Williams, Daly & Hammack scheduled; the latter is set to explain her dissent. The yield curve continues to steepen though action is modest and a function of the short-end continuing to pull back from post-Fed highs.

Opening Bell Daily: Fed guessing game. The Fed's inflation fight looks like a guessing game. Policymakers' actions and forecasts are at odds with one another as Trump 2.0 looms.

Reuters Morning Bid: Government shutdown and tariff fears jar year-end markets

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … First up a note from UK shop on US GDP …

BARCAP: Third Q3 GDP estimate: Strength should carry forward into Q4

The BEA's third estimate marked up GDP growth in Q3 by 0.3pp, to 3.1% q/q saar, reflecting upgrades to consumer service spending and net exports. Strength in final sales to private domestic final purchasers (PDFP) bodes well for another above-trend GDP print in Q4.

… what that says ‘bout rate cuts (or tantrum other day) is, well up to you I suppose … Same shop chiming in on stocks …

A hawkish Fed has brought a much needed reality check to euphoric Trump trades. Overdue consolidation could make it easier for investors to deploy capital in the new year. But policy uncertainty and desynchronisation will likely reshape markets in 2025, potentially benefiting Europe. Happy holidays!

… So the latest Fed-induced pull-back may not come as a big surprise to all, and could ultimately make it easier to deploy capital in the new year, with policy expectations now reset …

… Policy uncertainty returns. Fed's hawkish 'pivot' this week has reminded the market that reflationary policies were likely to have at least a slowing effect on disinflation, which would mean less cuts going forward (so no free lunch). US 10 year yields are now back at the 4.5% level, considered to be the threshold at which higher yields start to impact equities negatively, both in terms of direction and breadth. With the Fed removing its put and signalling higher for longer, we think this issue will be a key risk in 2025 and could slow/cap the market's ascent from here. As we wrote about in our 2025 Outlook - Regime change, 18 Nov, the degree and speed at which Trumponomics materialise may indeed alter the growth, inflation and policy paths, and fuel more volatility. But it is not just the Fed that has re-introduced policy uncertainty. Unexpectedly making the debt ceiling debate live again so early, and before the new administration is in place, tells us that policy volatility and brinkmanship may be the norm for the next four years.

Figure 3. Rising yields have hit the pain threshold for equities...

… this next one is one of MY personal favorites … a chartbook of WHO’s doing what in USTs …

DB: Who is buying Treasuries, mortgages, credit and munis? (December 2024)

This chartbook features nearly 100 slides presenting a comprehensive analysis of demand for U.S. fixed income products. Drawing primarily from the Federal Reserve's quarterly Flow of Funds accounts, these charts provide insights into the cross-sections of fixed income instruments and investor categories.

U.S. Fixed Income Securities Outstanding Reach $59.3 Trillion in Q3 2024

… same shop reflecting on prior activity in the bond market with a notable quotable …

… There was also scar tissue in bond markets, with 10yr (+4.8bps) and 30yr (+6.0bps) Treasury yields reaching their highest levels since May. The one area where there was a sense that the moves may have been overdone was at the front end, where the rate priced in by the December 2025 meeting was down -4.5bps on the day to 3.96%. For all the speculation about the Fed returning to hikes, it’s worth remembering they still cut rates this week and signalled more ahead, so the easing bias remains, even if it’s not as aggressive as it was. Indeed, investors are still pricing in 37bps of cuts next year, which isn’t too far off the Fed’s median dot at 50bps. So for DB to be correct that there are no cuts next year, we will need the Fed and the market to continue to change their minds.

But when it comes to the next 24 hours, the big question now is whether a US government shutdown is about to happen. The situation has moved quickly since Wednesday, when Elon Musk fiercely criticised the stopgap spending bill negotiated in Congress, with Trump and JD Vance then coming out against it later that day. Yesterday saw House Republicans put forward an alternative proposal that would fund the government through March and raise the debt limit for two years. The debt limit issue had been pushed by Trump who even said he’d be open to abolishing the debt limit altogether, saying he “would support that entirely”. However, the latest bill was voted down by 235 votes to 174 in the House last night, with 38 Republicans joining virtually all Democrats in voting against it. This leaves the Republican House leadership searching for a Plan C with less than 24 hours to go before the shutdown deadline. And as it stands, Polymarket are currently pricing in a 64% chance of a shutdown before year-end …

… on heels of the FOMC circus and fiscal clowns past couple days, a good ole FAQ is in order …

MS: FAQ: Debt Ceiling – Abolish vs. Increase | US Interest Rate Strategy & Public Policy Brief

With the suspension period set to expire at year-end, debt limit conversations are set to pick up. President-elect Trump supports abolishing, rather than increasing, the debt ceiling. We discuss what elimination of the debt ceiling means for spending, taxpayers, and markets.

Key takeaways

President-elect Trump voiced support for getting rid of, rather than increasing, the debt ceiling.

Abolishing the debt ceiling would not authorize new spending, nor come at a cost to taxpayers.

But abolishing the debt ceiling would avoid potential significant risks in financial markets, if the x-date were crossed.

A precise x-date is not yet possible be forecast given uncertainties around extraordinary measures, but we outline a plausible path for it to fall in 3Q25.

… well times and a good read for any / all vigilantes out there (more from THE head of the bond vigilantes — at least the fella who named ‘em — in a moment) …

Back to the FOMC for a straggler of a report / recap …

The Fed cut rates by another 25bps, bringing the total to 100bps since September.

The Fed's projections suggest they will cut by only 50bps in 2025, down from 100bps. Given the similarity between our economic views and the Fed's, we have changed our own rate call for 2025 in line with the Fed's.

The Fed’s hawkish guidance triggered a further rally in the USD, but we continue to see limits to the current USD strength.

… Same shop with a note on immigration which caught my eyes …

UBS: US Economic Perspectives Census sees the immigration surge

New Census methodology could impact 2025 household survey In a report we published in March, US population growth, we estimated US population was running twice the official Census Bureau estimates. Today, the Census Bureau published updated estimates, employing a new methodology to better capture the primary source of the discrepancy: net international migration. As a result of the sizeable pickup in net international migration in 2022 through 2024 that we estimated, we marked up our assessments of potential GDP growth, and the pace at which the labor market can run without putting downward pressure on the unemployment rate. In our annual outlook note following the Presidential election, we marked down our forecast for population growth, based on our reduced projections for net international migration in the coming years. That also fed through to our potential GDP growth projections for future years, and the pace of job gains that could keep the unemployment rate stable.

The Census Bureau appears to be attempting to address the likely too low earlier estimates. In our estimates the Census Bureau's previously estimated pace of roughly 1.1 million annualized net international migration in 2023 was likely closer to 2.8 to 3.0 million. In the graph below we show how the originally published Census estimates compare to what the Census Bureau published today. The Census Bureau published the details of the change at this link.

That additional contribution pushed the estimate of overall population growth to 1% in the year ending July 1 2024, after growth of 0.5% in 2019 and now 0.6% in 2022, by comparison. With rising deaths due to population aging and falling fertility, most of the US population growth is due to immigration. For example, for the year ending July 1 2024, the Census Bureau estimates natural population growth of 518K, and net international migration of 2,786K, for total population growth of 3.3 million. In other words, net international migration represented 84% of US population growth according to the Census Bureau, hence it's importance in estimating potential GDP growth and other measures related to economic growth…

…This also implies, from what we see today, the 2025 population assumptions that would underpin the household survey next year would assume faster population growth. For example, the Census Bureau did not publish an age 16 and over breakout, but their assumed 2025 growth in the CNIP is roughly 4 bps higher than the 2023 vintage of estimates assumed for 2024 (0.57% versus 0.53%). However, the net international migration would imply the skew of the age distribution changes, so the actual impact on the population growth assumptions for the age 16 and over population that US labor force statistics are based upon would presumably be even larger. While the impact on the ratios may not be pronounced (sample weights often cancel out from the numerator and denominator) depending on how the distribution of the population shifts, directionally the assumed faster population growth, all else equal, would imply next year we see faster labor force and employment growth in the household survey than would have otherwise been the case.

… curious how many immigrants there are in Switzerland? Same shop with a different, more topical hit piece …

With the wearisome repetitiveness of a tacky Christmas song, a US government shutdown is again threatened. A budget deal backed by president-elect adviser Musk and President-elect Trump failed to pass Congress. Absent a deal, the US government starts to shut down tonight. A short-lived shutdown affects government workers, but has limited economic impact. The longer a shutdown lasts, the more disruptive it is to the US economy. Economic data may not get published in a shutdown (a problem for Federal Reserve Chair Powell with their addiction to data dependency) …

… US personal income and consumption data should continue to signal rising real incomes. The fact that household incomes are so strong, allowing consumption without use of savings or credit card debt, gives a solid foundation for US economic growth in 2025 …

“Classic: A book which people praise and don't read.” ― Mark Twain

If the observation from Mark Twain was true during his lifetime (1835–1910), how much more does that sentiment resonate in the era of the smartphone and social media? We can all relate to the challenge of delivering a clear message in a crowded media landscape and as attention spans get shorter every year.

What follows is our distillation of the most impactful current economic themes into our favorite selection of graphs and charts. It is time-consuming work compressing big ideas into the fewest possible words. This was not lost on Mr. Twain who once began a letter saying, “I apologize for such a long letter, I didn't have time to write a short one.” At the end of this report, you'll find our Wells Fargo Economics Wrapped, which highlights our most-read reports of the year…

… Servicing Debt vs. Armed Services Despite the federal debt-to-GDP ratio jumping roughly 35 percentage points in the five years following the start of the Great Recession, the ultra-low interest rate environment of the 2010s kept interest outlays on the federal debt in check. Now, the potent combination of another jump in debt combined with interest rates near 20-year highs has led to a rocketing up in interest expense for the federal government. The cost of financing the public debt now rivals spending on national defense.

…Effectively Stuck The average rate on a 30-year fixed mortgage slipped below 4% in June 2019 and remained there for nearly two-and-a-half years. In the wake of the pandemic, home sales surged amid a search for more space while other households took advantage of lower rates by refinancing existing mortgages. Not only is a 3-handle on an existing mortgage rate not unique today, it's the norm. The effective rate on all mortgage debt outstanding was just below 4% in the third quarter, while the market prevailing rate is near 7%. It is no wonder households are less inclined to move today. They are locked-in at historically low mortgage rates.

Wells Fargo: G10 Central Banks Don't Deliver Any Big Holiday Surprises

Summary

It was an active day for G10 central banks, with four institutions announcing monetary policy decisions today. The Bank of Japan (BoJ) held its policy rate at 0.25%, as expected, although its accompanying comments were less hawkish than expected. Governor Ueda said more information is needed on wage increases to hike rates, and cited uncertainties around U.S. economic policy. That said, we think the fundamental case for BoJ policy normalization remains intact, and continue to expect 25 bps rate hikes in January and April.

The Bank of England (BoE) held its policy rate at 4.75%, although the 6-3 vote split to hold rates steady was perhaps a bit closer than expected, and the BoE also indicated that economic growth has softened. At the same time, the BoE noted recent higher inflation readings and said a gradual approach to removing monetary policy restraint remains appropriate. Our base case remains for the BoE to lower interest rates at a 25 bps per meeting pace through early 2026, although the risk of a steadier pace of easing has risen to some extent.

The Riksbank cut its policy rate by 25 bps to 2.50% and signaled a more gradual approach going forward given the lagged effects of monetary policy and the magnitude of easing the central bank has delivered so far this year. Officials lifted their inflation forecasts in the near-term slightly and reduced the GDP growth forecasts for 2024 and 2025. We have adjusted our forecast to look for two more 25 bps rate cuts in 2025, once per quarter in the first half of the year, to reach a policy rate of 2.00%.

The Norges Bank held its policy rate steady at 4.50% at today's monetary policy announcement, but also signaled that monetary policy easing should begin in early 2025. The central bank said that economic activity is holding up better than expected and at the same time, said inflation has moved closer to target, and that inflation pressures have been slightly more subdued than previously assumed. We forecast an initial Norges Bank 25 bps rate cut in March.

… importantly, Dr Bond Vigilante weighin in on … well .. vigilantes …

Yardeni: Bond Vigilantes Butting Heads With Washington's Profligate Crowd

Despite yesterday's 25bps cut in the federal funds rate (FFR), we're not raising our subjective odds of a stock-market meltup. While we're cautious in the short run through January, we're sticking with our odds of the Roaring 2020s (55%), a 1990s-style meltup (25%), and everything that could go wrong (20%). The reason we aren't raising our meltup odds is because the FOMC delivered a "hawkish cut" yesterday, signaling fewer cuts next year amidst concern about inflation.

Nevertheless, the Bond Vigilantes are still fighting inflationary monetary and fiscal policies. They've tightened financial conditions to offset the Fed's 100bps cuts in the FFR since September 18. They may also be starting to resist inflationary fiscal policies. President Donald Trump told NBC today that he would like to ditch the debt ceiling, which would remove a speed bump from ever-increasing government deficits.

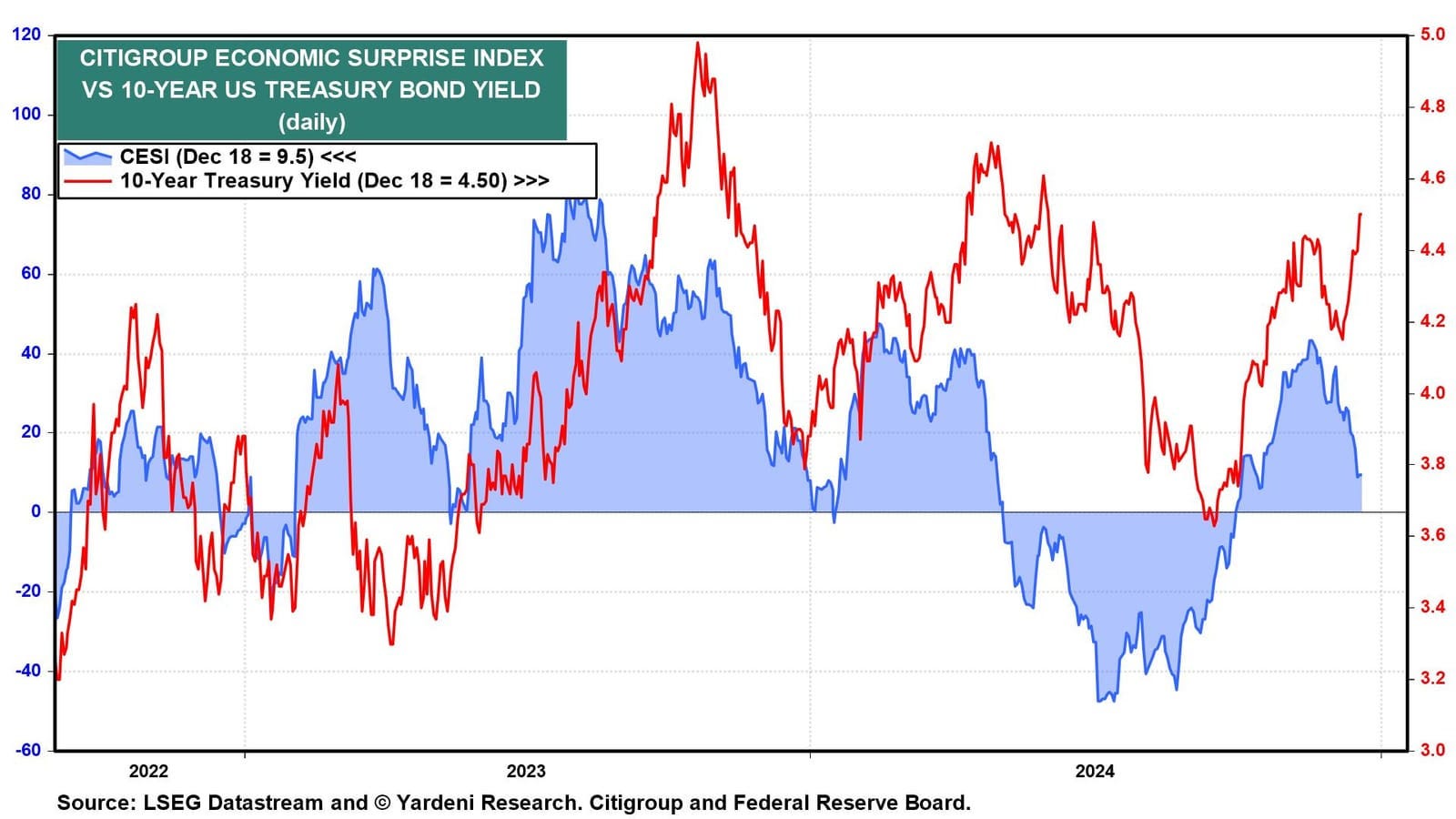

The US Treasury yield curve rose to its steepest level this cycle today, a positive 26bps spread between the 10-year and 2-year yields (chart). The 10- and 30-year yields also climbed to the highest levels since the spring, trading around 4.55% and 4.75%, respectively.

While stronger economic data helped boost bond yields throughout most of Q3 and Q4, there's now more "bad" reasons for the rise in yields. As a result, bond yields have risen since the Fed started to ease in September even though the Citigroup Economic Surprise Index has been falling (chart).

Economic data released today were mixed, but mostly supported our story that the economy's potential growth is much stronger than many expected including Fed officials. Here's more:

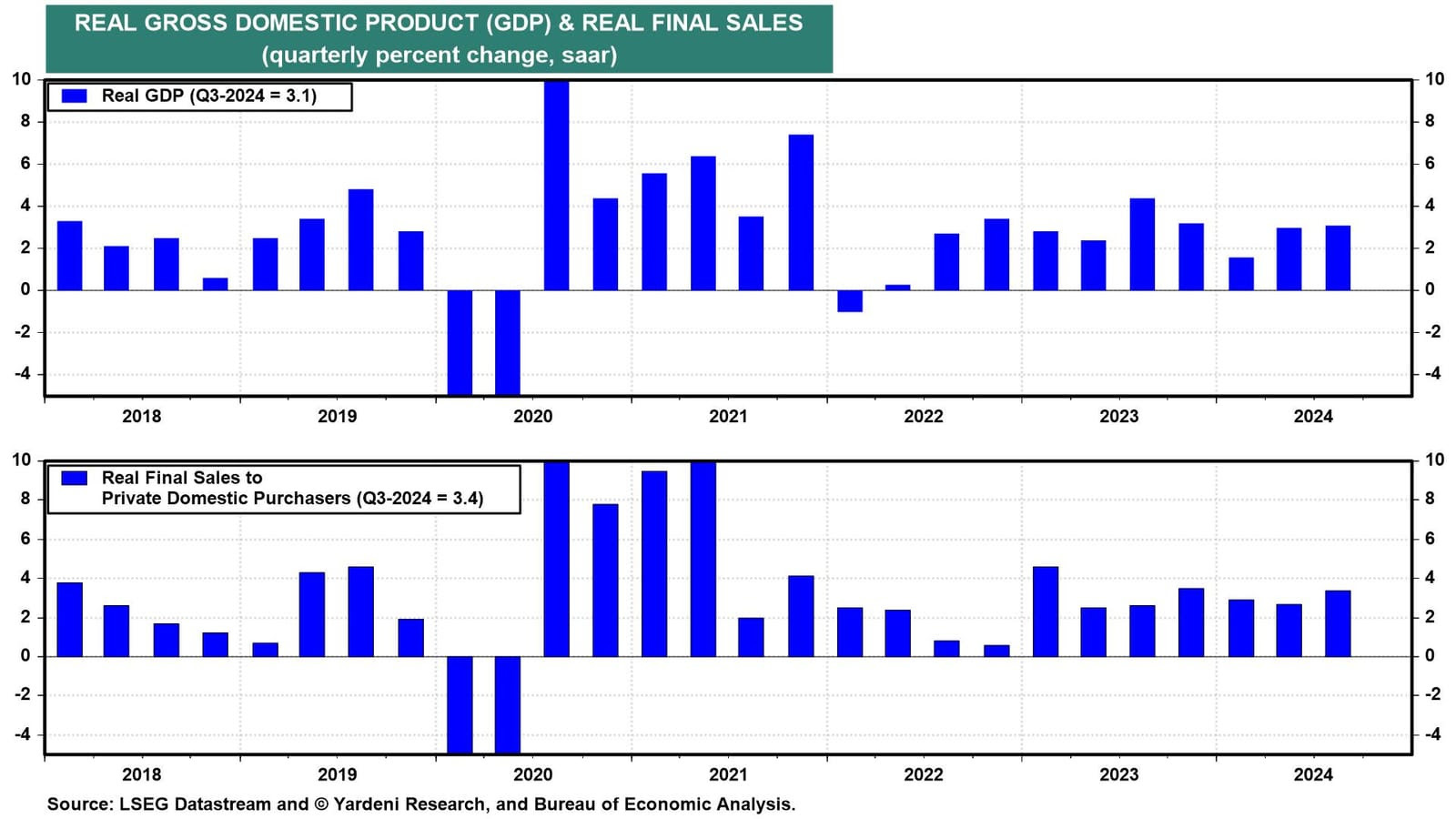

(1) GDP. Q3 real GDP was revised up from 2.8% to 3.1%, led by an increase in personal consumption expenditures from 3.5% to 3.7% (chart). Investment in equipment and intellectual property were both revised higher as well, a good sign for future productivity growth.

Real final sales to domestic purchasers, what Fed Chair Jerome Powell likes to refer to as core GDP, was revised from 3.2% to 3.4% in Q3. Real disposable personal income growth was also revised up from 0.8% to 1.1%.

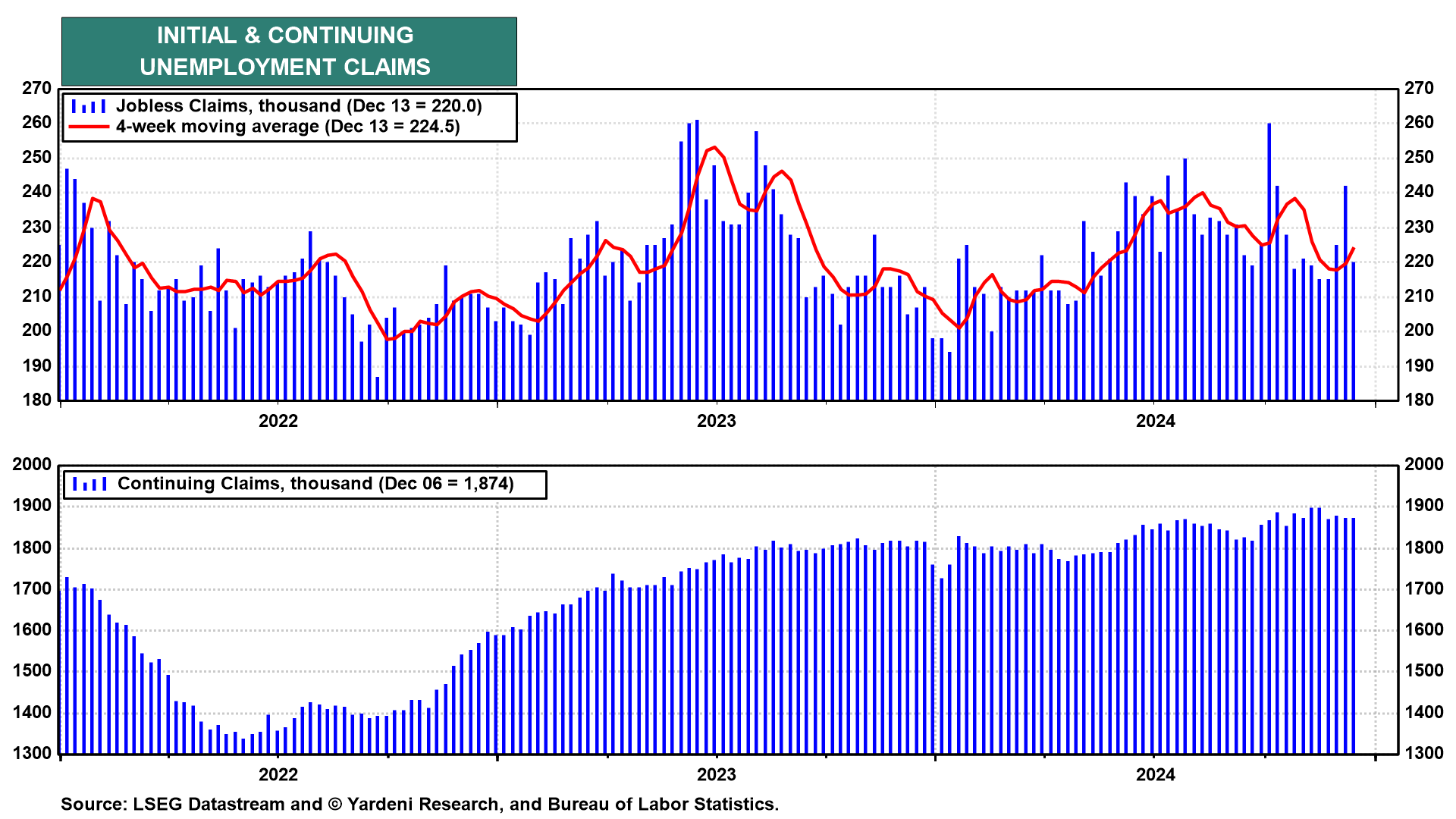

(2) Unemployment claims. Initial jobless claims fell 22,000 back down to 220,000 in the week ended December 14, as the Thanksgiving bump faded (chart). Continuing claims fell 5,000. The labor market remains solid, as we've been predicting.

(3) Regional manufacturing. December's regional manufacturing surveys from the Philly and Kansas City Federal Reserve banks both fell, suggesting the national ISM M-PMI will remain in contraction this month (chart). Future expectations across the New York, Philly, and Kansas City Feds all remain upbeat, suggesting the manufacturing sector may rebound next year. However, a possible tariff war could disrupt US production.

(4) Housing. Existing home sales rose in November and were up 17.7% y/y, the largest annual increase since 2021 (chart). Would-be homebuyers may be growing impatient over waiting for mortgage rates to fall. Considerable wealth gains and real income increases could also help rationalize further purchases.

… And from Global Wall Street inbox TO the WWW … First up, Torsten yesterday …

The Fed has now cut interest rates 100 bps this year. In a strong economy where growth over the past two quarters has been 3.0% and 2.8%, see chart below, the Atlanta Fed expects GDP growth in the fourth quarter to be 3.2%, well above the CBO’s 2% estimate of long-run US growth.

The strong economy, combined with the potential for lower taxes, higher tariffs, and restrictions on immigration, has increased the risk that the Fed will have to hike rates in 2025. We see a 40% probability that the Fed will raise interest rates in 2025.

For investors, it is starting to look similar to 2022—too high inflation, rising interest rates, and falling stock prices.

The bottom line is that there are significant downside risks to the 60/40 portfolio as we enter 2025.

… next, a view … an opinion which we know how it is that they are all created equally and how some are more equal than others …

Bloomberg (OpED): Central banks started a rates descent they can't finish The Fed’s cold feet on cuts shows that the world is down from a peak, but the changing terrain is no less dangerous.

… monetary policy easing has been the norm this year. The number of central banks that cut rates has exceeded those hiking every month in 2024:

The Fed arrived late but in style with September’s jumbo cut, but now faces the prospect of staying at a new plateau for a while. This is a repeating pattern. Central banks in developed markets were noticeably slower in their response to the inflation surge. As a result, the rates when they came inflicted much pain, and they had to wait before starting to cut. This year, nearly 80% of developed world central banks eased policy with the most notable exceptions being Japan — which exited the negative interest rates policy (NIRP) it had had in place since 2016 — and Norway and Australia, which held steady throughout the year …

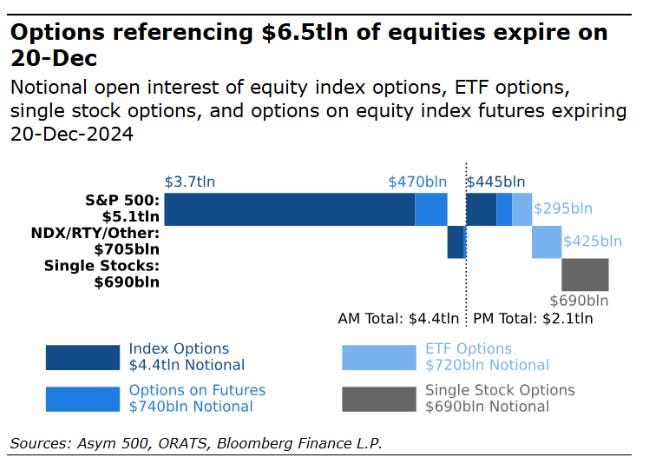

As Wall Street traders come to grips with the Fed’s plans to slow the pace of rate cuts, today’s US options expiration that has historically stoked turbulence offers a final hurdle to end-of-year calm.

The quarterly “triple-witching” will see some $6.5 trillion worth of options tied to individual stocks, indexes and exchange-traded funds fall off the board — this year’s largest and among the biggest on record, though still slightly smaller than a year ago, according to an estimate from derivatives analytical firm Asym 500.

This quarter’s expiration comes at a critical time for market positioning after the Fed on Wednesday signaled it will go more slowly than anticipated on rate cuts.

While the risk is sometimes overblown by Wall Street players, share volumes typically spike during the options expiration, which has a reputation for causing sudden price moves as contracts disappear and traders roll over their existing positions or start new ones…

… here, in this mornings inbox, a note from FRBNY folks as they take a look back (in effort to learn from history, I presume) …

… Concluding Remarks In a recently issued staff report, we use payments data to study the March 2023 bank run. We find that the run was concentrated on only two days and was driven mainly by a relatively small number of large depositors. However, a large set of banks were run on, far in excess of the banks that ultimately failed. Although run-on banks had on average worse fundamentals, there are large overlaps between the balance sheet characteristics of run and non-run banks. Banks react to their run by increasing their borrowing, mainly from FHLBs and only as a last resort from the discount window.

The Fed cut rates still this week but the debate on future decisions is set to become more intense. Consensus expects only limited directional moves in 2025, a view which could easily be proved wrong amidst an uncertain outlook.

… US equities took a big hit in the aftermath of the Fed’s message

Directional moves in financial markets to be only limited in 2025? While this year has produced a lot of ups and downs and surprises in financial markets and the economy, not all expectations have proved incorrect. For example, the German 10-year yield is currently trading almost bang in line with the Bloomberg consensus expectation a year earlier. That said, few analysts probably saw the spread between German 10-year bonds and 10-year EUR swaps visiting negative territory (lower swap rates than government yields) and trading at close to flat currently. No major changes are expected next year either, with the end-25 average forecast quite close to current levels as well. Our own baseline does not look hugely different either.

The US 10-year yield, in turn, looks to end the year around the highest forecast in the Bloomberg panel at the end of last year. The higher levels are not expected to last, though, and the average forecast puts the yield at a slightly lower level compared to current levels at the end of next year. We see risks tilted clearly to the upside compared to this view and the US 10-year yield return to 5% next year…

…US 10-year yield set to end the year higher than expected a year ago

… and a bit more on immigration …

WolfST: Census Bureau Massively Revises Up Population Growth: +8 Million in 3 Years, +3.3 Million Last Year, Largely due to Immigration. Population Surges to

Total Employment to be substantially revised higher early 2025 when the BLS incorporates these up-revisions into its household survey employment data.

… AND before hitting send, once again my sincere thanks for stopping by and all the engagement. Wishing one and all very best of holidays and hoping 2025 is your best ever … And spotted in nearby NJ stripmall (no, not really but…)

AND … THAT is all for now (and likely, the year …) Off to the day job…

Merry Christmas Happy new yrs enjoy the break all!