while WE slept: USTs bull steepen on strong volumes (RBA unch and BoJ ends NIRP, maintains JGB purchasing pace); #Got20s?; 5 reasons narrative 'bout to shift (again)

ZH: Bank Of Japan (Finally) Kills The World's Last Negative Interest Rate, Yen Weakens

… Finally, even with the decision to pull the trigger, we note that the debate over whether the BOJ has met the supposedly main condition for raising rates - stable 2% inflation - is hardly over.

As Bloomberg reports, inflation may slow as the impact of imports-driven price gains wears off, meaning that if officials go ahead and change policy, they could end up facing criticism in the future that they’ve passed a premature judgement on prices, former BOJ board member Takahide Kiuchi recently wrote. “And that in turn could become an obstacle to smooth policy normalization,” he said.

… With that now behind us — for now — or, more than likely, it’s just the end of the beginning. I still think the global carry trade coming to an official end will have consequences far and wide but we’ll discuss another time. Ahead of today’s 20yr auction I thought that would be as good a place as any to ‘begin’ …

20yy DAILY: above 4.66% would be less than optimal … so position long with stops up against it? go with a sell if we take it out? up to you to decide but here’s why I’m watchin’ and askin’ …

… As always, more questions than answers and watching but for now … here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are bull-steepening on the margin after a relief-rally reaction to the RBA removing its hiking bias and the BoJ ending NIRP but maintaining its JGB purchasing pace (amid limited forward guidance). UST volumes are decent at ~150% prior to the 20-year auction, FX activity also picking up with JPYUSD -1% and AUDUSD -0.7%. S&P futures are -7pts here at 6:45am, the NKY 225 the lone gainer in APAC overnight (+0.7%), with SHCOMP -0.7% and the KOSPI -1.1%. Crude Oil is UNCH’d and HG is giving back gains -1.1%. US 2s10s curve is +0.9bps steeper, with eh 2s5s10s fly +0.4bps cheaper.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities mixed, Dollar bid & JPY lower post-BoJ hike; US 20yr supply due … Bonds incrementally firmer as attention turns to US 20yr supply

Financial markets have been on an incredible run since November, with a multi-asset rally driven by hopes of a soft landing. That led the S&P 500 to one of its longest ever rallies, as the index advanced for 16 out of 18 weeks for the first time since 1971. Alongside that, US and European HY spreads are around their tightest in two years, Brent crude oil prices are back above $85/bbl, and even a traditional haven asset like gold has reached a new record.

Looking forward, it’s going to be a pivotal few days for markets, with decisions from the Bank of Japan and the Fed, along with the global flash PMIs. In particular, there's growing anticipation that the Bank of Japan could finally end their negative interest rate policy.

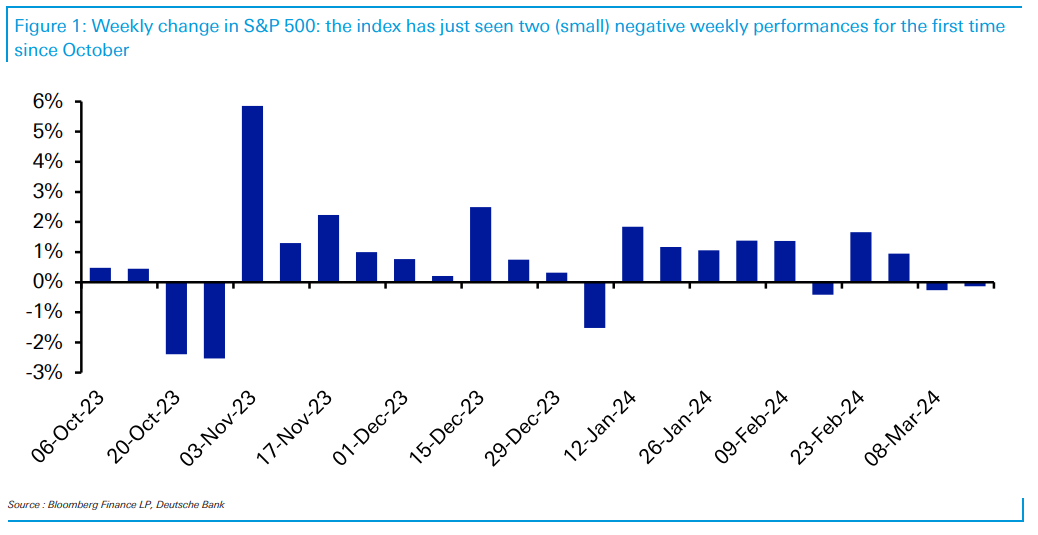

But ahead of those events, there are several signs that doubt is beginning to creep into market optimism, with the S&P 500 posting two consecutive weekly declines for the first time since October…

1. For the first time since October, the S&P 500 has now posted 2 consecutive weekly declines

2. There are clear signs that inflation is proving more persistent than expected a couple of months back.

3. More inflation has led investors to dial back their expectations for rate cuts this year.

4. The speed of the current equity rally has been very rapid, and history suggests it was always going to be hard to maintain that speed.

5. When inflation is already above target, then easier financial conditions risk leading to a hawkish reaction from central banks…

The recent uptick in US inflation—we expect 0.29% mom for February core PCE, up from a 0.13% average in Q4—has prompted us to soften our baseline Fed call to three 25bp cuts this year (vs. four previously) in June, September, and December. Still, our conviction in a soft landing remains high. First, recent activity and employment data have sent softer signals, punctuated by the rise in the unemployment rate to 3.9%. Second, elevated immigration has boosted labor supply and raised the "breakeven" pace of payroll gains needed to keep the labor market in balance. Third, wage growth has continued to decelerate steadily. And fourth, alternative data suggest that the recent increases in OER and used car inflation are likely to reverse. The ECB, BoE, and BoC are also likely to initiate cuts in June but are likely to move faster than the Fed given more economic weakness. In contrast, the BoJ looks set to terminate its negative interest rate policy at its March meeting following a strong spring shunto. Industrial activity has turned up in China, consistent with its big manufacturing bet, but housing and credit markets remain sluggish. Under our economic forecasts, the resilience of global risk asset markets appears justified, although upside from here is likely to be more limited.

Goldilocks Japan: BOJ Ends NIRP, YCC, and ETF Purchases at March MPM

The Bank of Japan (BOJ) decided at its March 19 Monetary Policy Meeting (MPM) to end its negative interest rate policy (NIRP). At the same time, it decided to cease yield curve control (YCC) and its overshooting commitment, and to end purchases of exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs). The policy changes were in largely in line with prior media reports (including the Nikkei, March 16).

The BOJ said it "...judged it came into sight that the price stability target of 2 percent would be achieved in a sustainable and stable manner..." and that it "considers that the policy framework of Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control and the negative interest rate policy to date have fulfilled their roles." The BOJ stated that going forward it would use the short-term interest rate as a primary policy tool, marking a return to a more standard monetary policy from unconventional monetary policy for more than 10 years…

US interest rate expectations jumped about yesterday. There was a lack of either meaningful data or Federal Reserve commentary. However, there is also a lack of a medium-term policy framework, articulating the Fed’s views on the interaction between policy and economics. At a time of structural change, that lack of a framework encourages volatility.

The Bank of Japan’s policy decision lies ahead. The Nikkei newspaper has reported an imminent end to negative interest rates and yield curve control, and years of experience suggest that carefully timed stories in the Nikkei are normally uncannily correct. The question is whether there will be further tightening (beyond the natural real rate increase as inflation rates slow)…

The BoJ delivered the policy change as expected, but the forward guidance was simpler than we thought. Let's see how Governor Ueda explains the guidance

Well, throughout 2024 we've seen a deterioration in stocks going up in price. That has certainly been well-documented.

But it wasn't until this month that we've started to see an expansion in stocks actually going down in price.

Apollo: Inflation Is Sticky at 3% (from Team Rate CUT to … NO cut … something, as always, for everyone …)

The Fed’s inflation target is 2%, and the bottom line of the inflation discussion is that inflation has started to move sideways at 3%, and this is a problem for the Fed, see chart below.

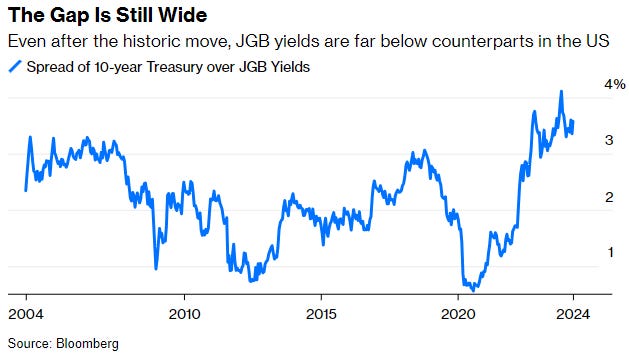

Bloomberg: The BOJ's end of history is much more than less than zero (Authers’ OpED — worth a look on this historical morning after …)

The Bank of Japan finally made its move out of negative interest rates, ending an abomination. Everyone should be grateful

… There is also a sense of cold reality. The BOJ still has the world’s lowest policy rates and says that “accommodative financial conditions will be maintained for the time being.” Even before the press conference by Governor Kazuo Ueda, the phrase “one and done” was in the air. The gap between Japanese yields and US Treasuries remains wider than for most of the last two decades:

If you were already betting on Japanese rates to stay low (through the carry trade), it’s safe to carry on. The policy of advertising monetary moves in advance even makes it less likely to be taken for surprise…

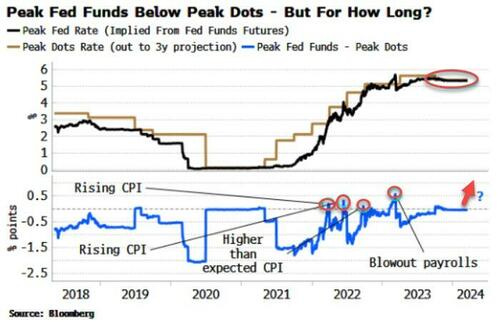

Bloomberg (via ZH): Rates Markets Are At A Hawkish Tipping-Point

… We could be knocking on the door of another of these episodes. The peak expected rate as inferred from fed funds futures has been moored almost identically at the peak rate expected by the Fed itself, based on the FOMC’s dots. The chart below shows the previous times pricing exceeded the Fed’s projections.

There are four distinct episodes, all of them driven by a sell-off in rates markets rather than a move lower in the dots. As shown in the chart, the first two were when CPI was rising and had not yet peaked. The third was a higher-than-expected CPI print, while the fourth was January 2023’s monster payrolls number…

… All else equal, that would take the market back below the dots.

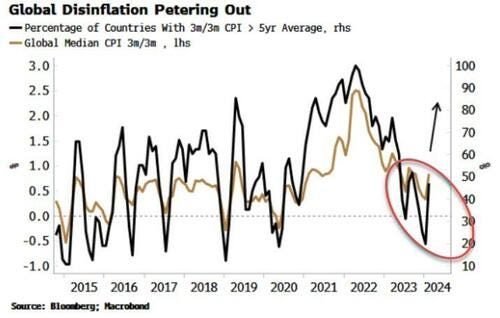

But traders are beginning to get uneasy about “sticky” inflation. Sticky might not be the problem - there are multiple signs that inflation will start rising again, as discussed here and here. Moreover, it’s not just a US phenomenon: globally there are signs that the disinflation trend is ending.

The market may well get impatient and move rate expectations higher if the Fed does not move the dots higher next week, sensing a policy mistake is in the offing. And if inflation keeps rising, then this latest episode where the market out-hawks the Fed may not be so brief.

FirstTrust: Monday Morning Outlook - Focused on the Fed

The Fed meets this week, which means investors and analysts will be sifting through Wednesday’s FOMC statement, updated economic projections, the “dot plots,” and Powell’s press conference searching for any signal – real or imagined – about what our central bank will do next. In particular, the market is on tenterhooks about when rate cuts will start, how fast those rate cuts will come, or if the Fed will simply hit the “pause” button on the prospect of rate cuts until deep into 2024…

… As always, we will be watching the press conference following Wednesday’s meeting for any mention of the Fed looking more closely at the money supply, but we won’t get our hopes up. The M2 measure of money is down 2.0% in the past year, which would not be good for the economy if these figures are accurate and if they continue.

Another key issue is whether the Fed will publicly abandon it’s 2.0% target to make it easier on themselves to achieve their goal. We think that will happen eventually, but that’s several years from now, not soon. The Fed likely thinks it would lose credibility if it announced a higher target for inflation, and could send long-term interest rates spiraling upward; that’s not a risk the Fed would take, particularly in an election year.

Our advice to investors: listen to and watch the Fed but don’t obsess about it. The changes in monetary policy from meeting to meeting don’t matter nearly as much as the productive capacity of the American people.

Inflows to bond funds, ex-money market mutual funds, have been rising since bottoming in January 2023.1

Attractive yields drove strong inflows to bond funds over the past year.2

Return on cash is likely to decline as the Fed looks to rate cuts later this year.3

After a historic rate-hiking cycle, estimates and futures suggest three rate cuts in 2024.4 That means reinvestment risk in cash-like instruments in the coming months that investors will need to manage…

… The most interesting aspect for the upcoming FOMC meeting will be the Dot Plot. I believe the Dot Plot will be considerably more hawkish than it was last December. The December forecast for the median federal funds rate might be revised down to two cuts from three cuts, and I wouldn't be surprised if the dots predicting less than two rate cuts are greater than those that exceed two rate cuts.

Headlines will say that this is more hawkish than what is priced into the Fed funds future market. I will remind our readers that the futures market prices are a biased predictor of what market participants expect to happen. Because Fed funds futures have a hedge feature (what finance theory refers to as a negative beta asset) the Fed funds futures rate is lower than what the market ‘expects’ will happen. I think there is an additional one cut priced in from this hedge feature—so a Dot Plot of two cuts is actually consistent with three cuts in the current market, which matches what we see now…

… AND almost done but as I continue to watch / listen to machinations outta DC cannot help but think all a bunch of clowns. This morning’s ‘toon helps nail the insane process of thought …

Memecoin bubble, what an interesting concept. Stonks went parabolic in Weimar German. The Ven & Turkish Stonk markets performed among the best during hyperinflation-currency devaluations too. I told many to sell their Doge prior to the Musks appearance on SNL. It's lonely being the Storm Crow :)

Your comic amusingly-yet-sadly reminds me of a 3-part ZH story about the fall of HP yesterday. Strangely all our CA-state computers are HP, must be some payola scheme imo

Memecoin bubble, what an interesting concept. Stonks went parabolic in Weimar German. The Ven & Turkish Stonk markets performed among the best during hyperinflation-currency devaluations too. I told many to sell their Doge prior to the Musks appearance on SNL. It's lonely being the Storm Crow :)

Your comic amusingly-yet-sadly reminds me of a 3-part ZH story about the fall of HP yesterday. Strangely all our CA-state computers are HP, must be some payola scheme imo