… Team Rate CUTS counting on soft ‘flation print and NO tarif’lation …

ZH CPI Preview: Will The Impact Of Tariffs Finally Emerge

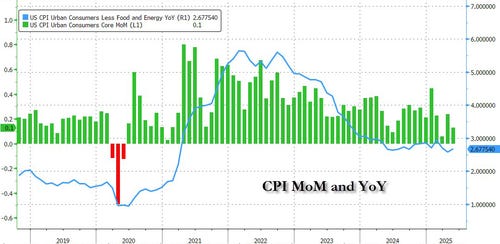

Wednesday's CPI report will be closely watched to see if the tariffs imposed in recent months are finally pushing prices higher, something they have failed to do so far.

Here is what Wall Street expects:

Consensus is looking for CPI to rise by +0.3% M/M in June, picking up in pace vs the +0.1% in May

Core CPI is also expected to rise by +0.3% M/M in June after the +0.1% in May.

In a rather narrow range, expectations for the annual increase in core CPI range from 2.8% to 3.1%

… AND I’ll quit while I’m behind and wish you good luck as you digest earnings and CPI … here is a snapshot OF USTs as of 556a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

…In the absence of any meaningful economic data, the Treasury market was left to drift sideways ahead of Tuesday’s inflation release. The President once again made headlines with tariffs – on this occasion using the threat toward Russia of “very severe tariffs if we don’t have a deal in 50 days… at about 100%.” The fresh levies would come in the form of “secondary tariffs” – presumably on anyone doing trade with Russia. The execution of such tariffs isn’t immediately obvious, although the prospect of using secondary tariffs in an already-strained global trading environment was nonetheless topical. As has been the case with many of the new levies, however, there remains a meaningful amount of uncertainty regarding the extent to which they will eventually flow through to realized inflation in the US. It’s with this context that investors will be closely tracking the June core-inflation figures with an emphasis on the fallout from tariffs…

…We’d be remiss not to at least acknowledge the renewed rumblings for Powell to resign. It goes without saying that the President wants Powell to step aside, allowing Trump to more quickly replace him with a friendlier (i.e. more dovish) Fed Chair. The argument that cost overruns in the Fed’s refurbishment of two historic buildings constitutes legal cause for Powell’s dismissal is a difficult one to make in a typical political environment, but Washington these days is nothing if not atypical. Nonetheless, Powell’s dismissal remains a low probability event, although the broadening of support among the GOP is somewhat troubling and sure to intensify in the coming weeks as the FOMC once again keeps rates on hold later this month…

Unexpectedly hawkish recent US tariff announcements imply a much more heterogenous trade environment.

The risk of an escalatory tit-for-tat scenario has risen, although our base case still assumes that deals will be struck by 1 August to limit the further increase in tariffs.

This bolsters our long-held view on US inflation persistence and our call for no Fed cuts in 2025.

At the same time, with around two-thirds of the potential increase in US tariffs already in place, the incremental information is arguably more important for the rest of the world.

FX may become less correlated, implying more selective (vs broad) USD weakness in H2. We continue to like being received front-end rates in particularly exposed regions (South East Asia and the CE3).

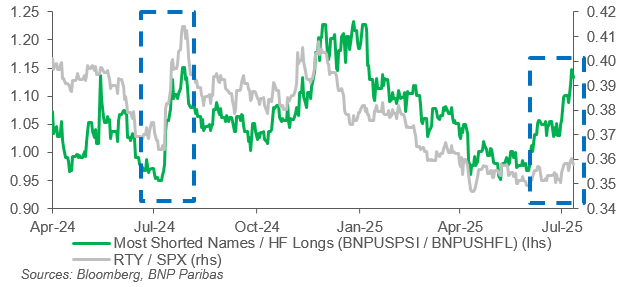

A confluence of flow factors will be driving US equities this week: CPI and initial Q2 earnings are the key catalysts. But they need to be considered in the context of the momentum unwind that has been taking place. The massive underperformance of Hedge Fund longs versus crowded shorts is very similar to the move this time last year. In July 2024, it was a cool CPI print that triggered the rotation trade. This year’s momentum unwind ahead of the CPI release creates more symmetric risks. A hotter print this time could be a catalyst for a reversal of the recent underperformance of some HF longs.

RTY as a CPI and momo-proxy: In the index space, IWM/SPY tends to be a similar trade to HF Longs versus Most Shorted. It is interesting that IWM hasn’t seen the same outperformance as the most-shorted names. One reason might be the massive FX tailwind we have been flagging for mega-cap equities. Heavyweights in SPY should see much more of an earnings tailwind from the FX depreciation than IWM. Investors looking to hedge over CPI should consider RTY. While the vol isn’t obviously cheap, the index has been more sensitive to CPI surprises. July last year the soft CPI saw IWM post a one-day gain of +3.6% versus NDX that was down 2.2% and a more muted reaction from SPX, -0.9%.

The RTY/SPX vol spread has widened, leaving the calls looking a little rich. We would be hesitant still to short the RTY call wing ahead of CPI. One-week IWM Put Spreads line up well as a hedge: IWM US Jul25 218/213 Put Spread, 0.79 Offer, -16.5% Delta, 5.3 x Max Payout. Further out, we would suggest looking at Sep25 and skipping Aug25. September expiry is two days after the FOMC and also captures Jackson Hole (Aug 21-23). IWM US Sep25 210/190 Put Spread, 2.68 Offer, -17.3% Delta, 6.5 x Max Payout.

The massive unwind between the HF longs and most-shorted names is very similar to the move we saw this time last year. IWM hasn’t posted the same outperformance, though …

Feel like we’ve seen this one before … guess we’re hearing lots about it so why not send again, ask for a vote …

… It is hard to quantify the impact on FX and rates, but on the first 24 hours of an announcement of a Powell removal we would expect a drop in the trade-weighted dollar of at least 3%-4% accompanied by a 30-40bps sell-off in US fixed income ed by the back-end. Similar to the experience in April, we would expect the correlation between the bond market and the dollar to turn sharply positive (both down), while we would also expect a widening in cross-currency basis as the market may worry about the politicization of the Fed swap lines …

… Back to the here and now, and same shop with another fan favored stratEgerist …

…They expect monthly headline CPI to come in at a 5-month high of +0.34%, with core also at a 5-month high of +0.32%. We seem to be the highest on the street with consensus at +0.27% and +0.25% respectively.

If DB is correct, that would push up the year-on-year numbers, with headline CPI up three-tenths to +2.7%, and core CPI up two-tenths to +3.0%. Consensus is a tenth lower on both. We’ll mostly be focusing on signs of tariff-related inflation in the core good categories. President Trump continued to beat the low inflation drum yesterday though, saying "we have no inflation", and that "we should be less than 1%" when referring to interest rat es.

Ahead of today's big print, markets have been a bit mixed to start the week as the weekend tariff headlines reverberate, and global long-end bonds continued to edge higher. H owever US futures are edging up this morning (Nasdaq futures +0.3%) after Nvidia have seemingly been given the green light to resume exporting their H20 chips to China that were suspended in April…

A question on ALL of our minds …

14 July 2025 ING Rates Spark: Will tariffs show up in US CPI?

Markets are not fazed by Trump's trade escalation, so far, it seems. Japanese yields keep rising on fiscal and inflation concerns, whilst European government bonds are now looking more attractive on an FX-hedged basis. The big one coming is the US CPI report for June, and to what extent we see the beginnings of tariff-inspired price rises

Finally, a very not-confident sounding writeup about CPI impacted by tariffs …

US June consumer price inflation is the first number that might show trade tax effects. Only half the expected trade tax rise has hit the economy so far. Inventory stockpiling means pre-tax items are still available. How readily US firms can pass on price increases matters. Post-pandemic inflation made this easier. Tariffs have dominated the (non-Republican) media narrative, making price increases easier. The details, not the headlines, will indicate the potential scale of the inflation surge…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

A couple from The Terminal …

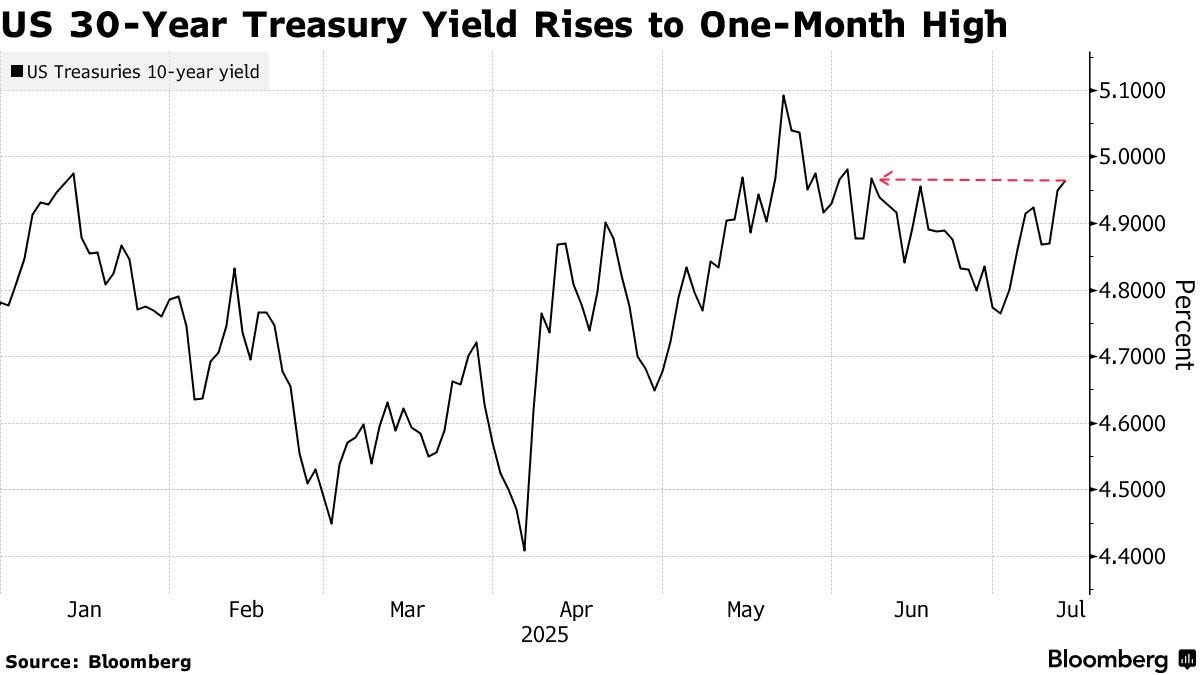

July 14, 2025 at 7:53 PM UTC Bloomberg: US 30-Year Treasuries Extend Decline as Focus Turns to Inflation

… Higher-than-expected inflation “will give the market a bit of pause,” he said on Bloomberg Television. “Can we justify these 15 or so basis points of rates cuts that are priced in September or almost the two full cuts that are priced by the end of the year? And we think the market will realize no.”

The figures may provide fodder for a heavy lineup of Federal Reserve speakers this week. Trump, meanwhile, has been ramping up his attacks on Fed Chair Jerome Powell…

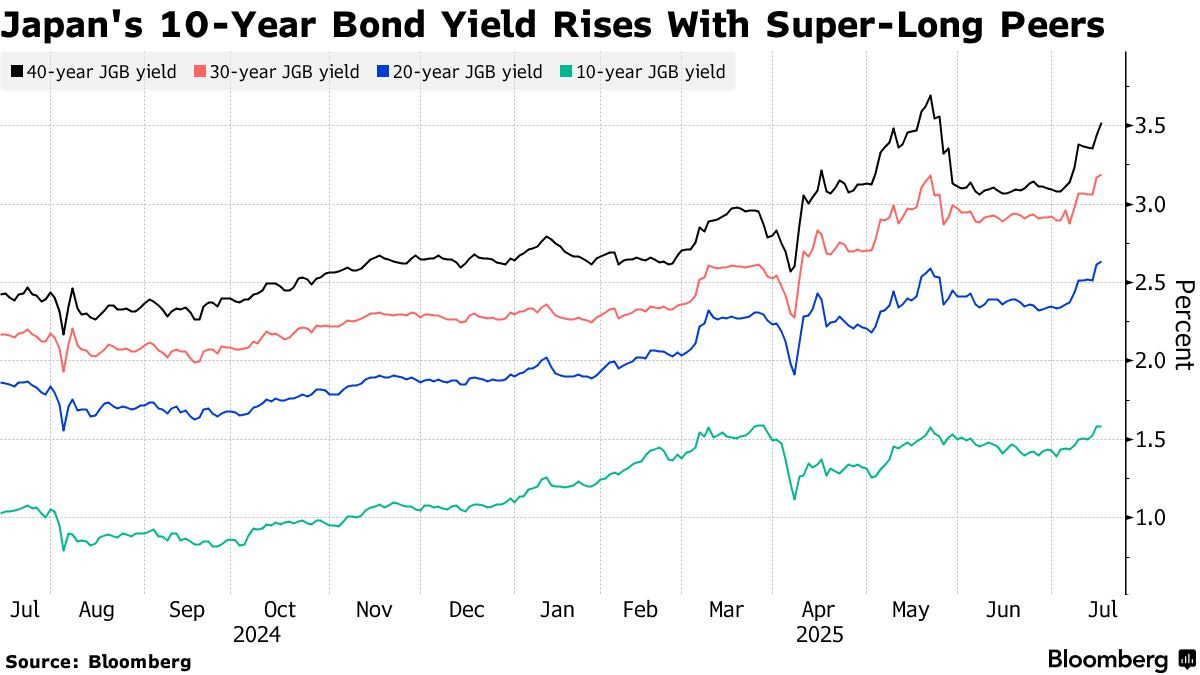

Updated on July 15, 2025 at 1:39 AM UTC Bloomberg: Japan Bond Rout Touches New Pain Point as 10-Year Yield Rises

… The upward shift in yields comes amid concerns that government spending is likely to increase in the wake of an upper house election on July 20. Opinion polls suggest the ruling bloc led by Japan’s Liberal Democratic Party may struggle to win a majority. The LDP itself is looking to cash handouts to win voters and opposition parties are eyeing lower taxes.

Yuichi Kodama, economist at Meiji Yasuda Research Institute, said the 10-year bond yields are important because they drive fixed mortgage rates and would have a significant impact on the real economy.

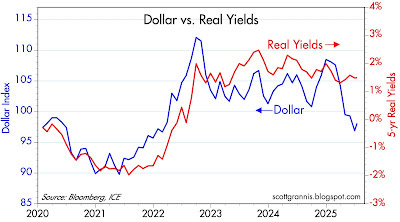

Some charts I find of interest to the general public, and which you're unlikely to find elsewhere:

Chart #1

Chart #1 sheds light on an important input to the dollar's value: real yields. The red line shows the level of real yields on 5-yr TIPS. These are true real yields, since TIPS are bonds whose principal is adjusted by the CPI, and whose coupon is a "real" yield. (Their return to the investor is equal to the rate of consumer price inflation plus a real yield.) Real yields on TIPS are determined by market forces, and are in turn influenced by the market's expectation of future Fed policy. TIPS are not only safe from default, but also safe from the ravages of inflation.

The blue line is an index of the dollar's value vis a vis other major currencies. That the two tend to move together suggests that higher real yields enhance the value of the dollar, while lower real yields detract from the dollar's value. The situation today suggests that the dollar is trading on the weak side of where it would normally be given the current level of real yields. This further suggests that investors aren't entirely comfortable with the outlook for the U.S. economy (e.g., tariffs, deportations)…

Hit inbox yest AFTER hitting send but still worth a look …

July 14, 2025 MacroMonday: Be Wary Of The TACO Trade!

There’s a full slate of key data on deck this week. Hopefully it will bring some clarity to the economic and market outlook. We’ll get the first regional PMI readings for July, with the Empire Fed Index out on Tuesday and the Philly Fed Index following on Thursday. Also on Thursday, the NAHB housing market index is released, and Friday brings the latest read on consumer sentiment via the University of Michigan survey.

We’ll be looking closely for signals regarding employment and inflation, which are still the two most consequential themes driving markets. In that vein, Tuesday’s CPI report and Average Hourly Earnings data will be front and center for us. Historically, CPI and Hourly Earnings have shown a strong correlation, and lately that relationship has been even tighter.

Put simply, a tighter labor market tends to be inflationary through rising wages. Of all this week’s data, Hourly Earnings could end up being the biggest market mover…

… Good luck out there today as you plan your trades and trade your plans …