Good morning … how’s bout that there 20yr auction … higher yields, concession, all seemed great, right? Turns out was a more mixed (tail but solid internals) liquidity event …

… these results came just about an hour before the BEIGE book …

ZH: Ugly, Dovish Beige Book Warns Of Manufacturing Decline In "Most Districts", Greenlights Further Rate Cuts

… AND pressed for time this morning, i’ll move right along and so, here is a snapshot OF USTs as of 734a:

(and since I’m late) … HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are richer/flatter with the US point stabilizing overnight, the shift in momentum driven by regional and offshore interest, though there was not a clear fundamental catalyst for the rally back towards 4.00% 5s. Our desk in London noted a lack of selling pressure generally, with dip-buying demand re-surfacing at stretched technical readings (TY 14d RSI at 28 yday). That said, early flows were relatively light but once prices began to drift higher, volumes picked up in the belly, aided by a FV-WN block steepener (~$300k 01). Crude oil is +1.1%, XAU +0.8%, DAX futures +0.8%, S&P futures +0.4%, with 2s10s -2.25bps.

… The rout in the municipal bond market (BBG link), suggesting some retail ‘statement shock’ at play, which forced an Ohio agency to shutter plans for issuance this week, with AAA yields ~18bps higher yesterday (largest selloff in 2-years).

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: TSLA +10%, Autos gain on China reports, PMIs mixed, USD & US yields soft into data … USTs/Bunds are on a firmer footing, with EZ PMIs continuing to paint a dire picture in Europe; Gilts are the clear underperformer amid reports that Chancellor Reeves will announce major changes to fiscal rules releasing GBP 50bln for spending … USTs are firmer and pulled around alongside the above Flash PMIs ahead of its own release and weekly jobs data. Holding towards the 111-12 session high with the curve modestly flatter though with action across it a touch mixed at points as the belly finds itself the marginal laggard from a yield perspective.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

… from France on US reFUNding (and issuance on into 2025) …

BNP US refunding preview: TIPS and tricks for Treasury debt into 2025

We expect Treasury to maintain current nominal coupon and FRN auction sizes at the November refunding but look for any indications on the timing of future increases in the medium term.

A further reliance on T-bills is expected to fund deficits, QT and buybacks into next year, with TIPS auction size increases also expected in 5y and 10y tenors in the medium term.

Depending on the US election outcome, political risks skew our near-term issuance estimates lower once the debt ceiling is reinstated at the start of 2025 and Treasury is forced to rely on cash balances and accounting measures to avoid a potential default.

We slightly lower our Q4 crude price forecasts to reflect worse-than-expected sentiment overriding relatively tight light crude fundamentals.

Our outlook for 2025 and 2026 is largely unchanged. We see limited room for OPEC supplies while low outright crude stocks and downside supply risks may give the market a floor.

We expect Brent crude to price in the mid-to-high USD70s/bbl range throughout 2025 and 2026.

Our base case assumes the Middle East crisis de-escalates even though we have raised our high case significantly to reflect limited options to circumvent the Strait of Hormuz.

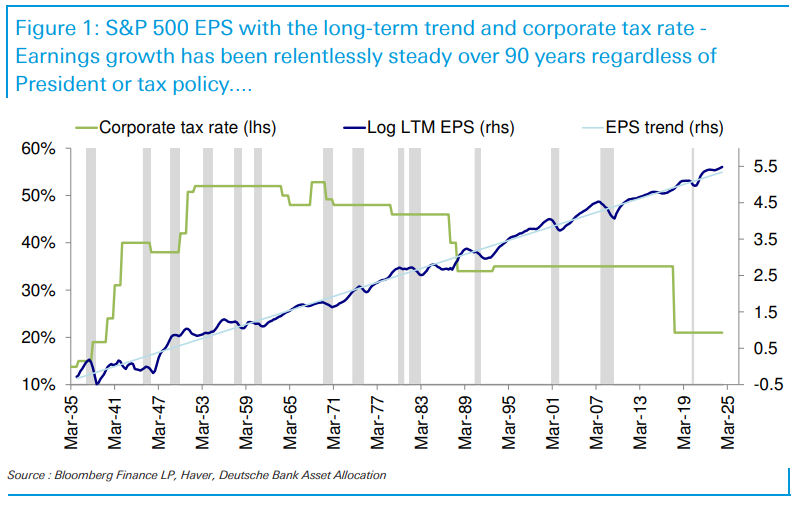

… an excellent chart of the day (yest) showing stocks (EPS) and corp tax rates over the longrun — trends without any visible political impact …

DB CoTD: Steady EPS growth has survived all Presidents

… Over the last 90 years, the corporate tax rate has been changed by many administrations, but the long-run EPS trend has hugged an annualised growth rate of c.6.5% quite tightly. Although there was a long period of stable corporate tax rates between the mid-1980s and the TCJA of 2017 (under Trump), the reality is that the effective tax rate had been falling consistently over that period after accounting for deductions, credits, loopholes and other tax-saving strategies.

As an aside, the 50 year-plus period where US tax rates have fallen from around 50% to around 20% has coincided with the structural US fiscal deficit going from close to flat to nearer 7% today. A simple CoTD is too short to discuss whether there’s some causality between the two, but there does feel like there is an element to today’s chart where inadvertently we are solving for a steady EPS growth rate. When economic and productivity growth was rapid (pre-1970s), corporate taxes were higher and rising, and maybe prevented companies from fully exploiting this. However, as growth and productivity have fallen, EPS growth has remained steady but perhaps helped by an ever decreasing tax take.

One interesting implication of this going forward is that if AI does create a productivity miracle, will the corporate tax rate go back up over time, regardless of politics? That way you keep a steady EPS growth rate but return some money to a phenomenally stretched fiscal balance sheet. Before you cross-examine this statement, consider that I’ve only just thought of the idea as I type this, so it may be far off the mark. But I do wonder whether the relatively steady EPS climb over nearly 100 years is partly due to some inverse correlation between productivity growth and the tax rate.

As pointed out by our US economists, estimating the impact of proposed tariffs on consumer price inflation involves significant complexities, including currency adjustments and pricing reactions of both foreign and domestic firms. Therefore, we employ a range of estimates to gauge the potential magnitude of the impact on CPI and benchmark this against market expectations. Utilizing a methodology based on import shares relative to consumption expenditures, and considering various tariff scenarios (including a 10% universal tariff and a 60% tariff on Chinese imports), the analysis projects a potential impact on headline CPI ranging from 0.8 to 2.5pp.

In terms of market pricing, while the CPI curve indicates some upside from April 2025, market-implied estimates for CPI ex gasoline suggest this acceleration is primarily attributable to oil price dynamics. Furthermore, market pricing is currently below DBecon forecasts for both 25H2 and 26H1, despite the fact that our economists' forecasts do not currently incorporate any tariff policy. We therefore see USD breakevens as significantly underpricing the inflationary risks of the proposed tariffs. Conservatively taking the lower bound 80bps CPI impact with a 50% implementation probability suggests a ~40bps upside. This analysis only considers the direct inflationary impact of tariffs, excluding potential further upside from fiscal policy.

Given uncertainty surrounding the implementation timing (which could depend on control of congress) and phasing, we recommend being long 1y2y ZC CPI (current level: 2.50%; indicative target: 2.75%; indicative stop: 2.35%).

… always good to take a moment and perform a bit of a reality check and so …

What on earth is happening in the markets? The yield on 10-year US treasuries has jumped by 60bp since mid-September. For investors, that is the biggest monthly loss since the meltdown of autumn 2023. And this time, even more than last year, the slump in bond prices has gone global, setting international bond markets up for an unprecedented third consecutive year of negative total returns. Yet equity prices are hitting new highs almost daily, not just in the US but also in many other markets, at least in local currency terms.

Many investors and analysts seem to be baffled by this divergence, especially considering the extreme levels of geopolitical, fiscal and global trade uncertainties which were highlighted Tuesday at the International Monetary Fund’s annual meeting with the publication of the World Economic Outlook.

But in my view, explaining the recent performance of financial markets is pretty simple. The chart below holds the key.

The rise in US bond yields over the last two years has been a return to normality

… History suggests that the next inflation shock, whether it comes from energy or war or trade protectionism or labor militance or fiscal profligacy or monetary expansion or some entirely new problem, may be much harder to reverse than the transitory inflation that resulted from Covid and the Ukraine war. Of course, history need not repeat itself, nor even rhyme. But the chart below suggests that prudent risk management today must involve substantial ownership of inflation hedges like gold, energy, commodities and CPI swaps, and much more limited exposure to government bonds.

In late 1971, the Fed declared victory over inflation…

The authors of the latest Federal Reserve Beige Book are clearly followers of TikTok memes. The economy was described as being modest and demure (actually as growing at a “slight or modest pace” but it amounts to the same thing). The benign growth story fits with most economists’ central projections. On inflation, anecdotes suggested a more concerted resistance to profit-led inflation from consumers…

… finally whenever Dr. Bond VIGILANTE himself talks ‘bout them vigilantes …

The US presidential and congressional elections aren't until November 5, but the Bond Vigilantes are voting early. The 10-year US Treasury bond yield has risen a whopping 63 basis points to 4.25% since the Fed's September 17-18 meeting (chart). In exit polls, the Bond Vigilantes are saying they are voting against Fed Chair Jerome Powell's dovish monetary policy because the economy is running hot, and the Fed's premature 50bps rate cut 0n September 18 raises the risk that it will overheat.

We anticipated this might happen. On September 2, we wrote that better-than-expected economic indicators were likely to rattle the bond market. On September 22, we wrote: "So now investors must consider the possibility that the Fed's easing will continue to drive the 2-year yield lower, but the 10-year yield might move higher on concerns that the Fed might heat up a warm economy." We are sticking with our 4.00%-4.50% range for the bond yield. We resisted raising our S&P 500 yearend target of 5800 when it rose above this level recently. We aren't lowering it now that it is back at that level.

The Bond Vigilantes may also be voting against Washington, figuring that no matter which party wins the White House and the Congress, fiscal policies will bloat the already bloated federal government budget deficit and heat up inflation. The next administration will face net interest outlays of over $1 trillion on the ballooning federal debt (chart).

NVIDIA is now bigger than the total market cap of five of the G7 countries, see chart below. And foreigners own 18% of the US stock market.

The bottom line is that global equity markets, including retirement allocations to equities, are basically leveraged to NVIDIA.

Let’s hope the value of NVIDIA doesn’t decline significantly.

The idea that public markets are safe and retirement savings in public markets are safe is misguided.

Some investments in public markets are safe, and some are risky.

Same for private assets. Some private investments are safe, and some private investments are risky.

… and from NVIDIA to a Bloomberg OpED …

Bloomberg: Bond markets fear the 'known unknown' of a GOP sweep

They deeply dislike the prospect of unchecked Trump tax cuts driving up deficits, even if stocks are likely to benefit.

Beware Bond Math!

Treasury yields are rising again. In part, that’s down to the extremely exciting factor of combustible US politics and the shifting odds on the elections. But it’s also in part driven by the extremely unexciting issue of bond market liquidity and a rising term premium.

The term premium is an infuriatingly technical subject, made worse by the fact that it’s unknowable in real time and can only be calculated with any precision in hindsight. Points of Return covered it in 2022, while colleagues Michael Mackenzie and Liz Capo McCormick wrote an analysis last year that you can find here. The New York Fed defines it as “the compensation that investors require for bearing the risk that interest rates may change over the life of the bond.” Most of the time, it will be positive; investors generally will want some compensation for such risks.

Shifting short-term expectations of the Fed will tend to move bond yields, as has visibly happened over the last year. The point of the term premium is to explain any rises or falls in yields that can’t be put down directly to the Fed:

…

…more on vigilantes from NOT THE guy …

Discipline Funds: We Need to Have a Talk About “Bond Vigilantes”

…We should debunk one myth right off the bat. When Musk says the US government is going bankrupt like a household he’s quite simply misunderstanding how the monetary system works. Individuals go bankrupt. Large aggregated sectors do not. For example, the aggregated private sector cannot go bankrupt. The US government is a huge aggregated sector in the US economy. It does not go bankrupt. In the aggregate it can print money to fund all spending and it cannot run out of this money unless it borrows in a foreign currency, which it doesn’t do. Of course, it can cause wildly huge inflation. We know that after Covid, but comparing the Federal Government to an individual is just wrong.1

Of course, you might say this is all semantics. High inflation is a form of default. I don’t necessarily disagree! But when we assess the burden of the national debt we are really assessing the risk of inflation that comes from that debt. So, is the interest on the national debt causing an inflation problem? I think the evidence is very clear on this – no. Just look at the impact of raising interest rates when compared to inflation. If anything, it looks like raising interest rates causes inflation to move down, not up.2

… Back to Druckenmiller and friends. This seems to be a pretty persistent thing with Druckenmiller. For example, I wrote nearly this exact same article 11 years ago in response to a WSJ op-ed in which Druckenmiller said the exact same thing. He said the USA was bankrupt and that the Fed was too loose. The 10 year yield was 2% at the time, the Fed was on 0% and rates would slowly drift lower until we got the Covid shock 8 years later. It was a dreadful prediction. I think the same exact thing is happening now. Don’t get me wrong. Druckenmiller is one of the all-time great investors, but betting on US government default has been a bad bet for a very long time. In my humble opinion, the error in this analysis is two-fold:

Assuming that interest payments are problematic – they are not because the Fed can control them with a dial and also because high rates put DOWNWARD pressure on inflation.

Assuming high inflation must result from government deficits. I think it’s absolutely true that large deficits put upward pressure on inflation. I’ve said this a billion times during Covid. But government spending is 23% of GDP. That’s the same level it was at in 1982! And while it’s a large portion of aggregate spending we should remember that 77% of spending is coming from OTHER sources. In most cases, it’s much more efficient sources such as the most efficient corporate machine the human race has ever seen (corporate America).

Again, don’t get me wrong. When government spending explodes to 45% of GDP like it did in 2021 then big inflation can come from this because the government becomes the primary (reckless) spender in the economy. But that’s not the case today. Government spending as a percentage of GDP is about the same as it’s been for most of the last 40 years. So it begs the question – in an economy like the USA does the government drive inflation or is the government driving a small amount of inflation that is not as important as other factors in the economy? In my opinion, other factors are driving the secular inflation trend and that includes:

Huge innovative efficiencies being driven by corporate America that exert downward pressure on inflation.

Demographic changes that are turning America into an older and slower growing population.

Inequality which is exerting pressure on those with the highest marginal propensity to spend.

If anything, it takes huge deficits to offset these three huge trends. It takes something like a Covid stimulus to result in big-time inflation. Otherwise, the government, even with its currently large deficits, cannot create high inflation without exploding the deficit again. Will that happen? It’s certainly a risk. But it wouldn’t be my baseline estimate. If anything, the deficit is likely to shrink in large part because the Fed is going to cut rates in the coming years.

So, long story short – the bond vigilante narrative is overblown. Does it mean we don’t need to worry about government spending and inflation? No, I think investors should continue to protect themselves from inflation, even if it remains low. But we also shouldn’t blow this out of proportion and feed into hyperbolic narratives about how the USA is on the verge of bankruptcy…

… for those of us who believe everything on the intertubes (ok ok some of the time, there’s good stuff) …

at tdgraff

Can I interest you in an asset class with terrible fundamentals but the valuation is also expensive?

Not often you post Gavekal. Interesting though

You're doing god's work as usual

Very interesting articles.....