June 25, 2025 7:00 pm ET WSJ: Trump Considers Naming Next Fed Chair Early in Bid to Undermine Powell Warsh, Hassett and Bessent are among those under consideration as Trump evaluates their commitment to cutting rates Nick Timiraos

… At a private audience of finance professionals in Boston this month, Warsh said he thought Powell would serve out his term. But he added, “I wouldn’t be shocked if the president made a nomination sooner than would be customary, just to…try to make a lame duck lamer or something like that,” according to remarks reviewed by The Wall Street Journal.

Some close to Trump harbor reservations that Warsh would be a maverick once he takes the job, particularly given his past views that identify him as a so-called policy “hawk,” meaning someone who has worried more over the years about inflation than employment.

“My fatal flaw is I say what I believe,” Warsh told the Boston audience when someone asked about his hawkish reputation. “If the president wants someone who is weak, I don’t think I’m going to get the job.” …

… not new news but news, nonetheless new more DOVISH chair — consequences — an easy readthru and with this ‘friction’ in mind, 2 down 1 ($44bb 7s today) to go …

ZH: Mediocre 5Y Auction Tails As Foreign Demand Tumbles

…Overall, this was a medicore and disappointing, if quickly forgettable, 5Y auction, yet one which barely caused a blip in the second market upon the break. Attention now turns to tomorrow's 7Y sale while the big question is just how will the US fund the trillions in looming deficits that make up the Big Beautiful Bill, and when will that finally hit demand for long-term debt.

… so a less than optimal auction (as technical setup wasn’t all that good) leaves then plenty of month, 1/2yr (fiscal years end - Japan) room and appetite for 7s, then, am I right?

7yy: TLINE resistance (4.02) on verge of breaking and support up north of 4.20…

… and as one contemplates bidding strategy today, ahead of month/qtr end, worth noting DAILY momentum (etched in) is stretched (ie overBOUGHT) and so, not necessarily a good ‘concession’ or setup but then again … if you believe in WSJ story and the idea of rate cut(S) coming soon, then, well, yer fine … nothing to see here …

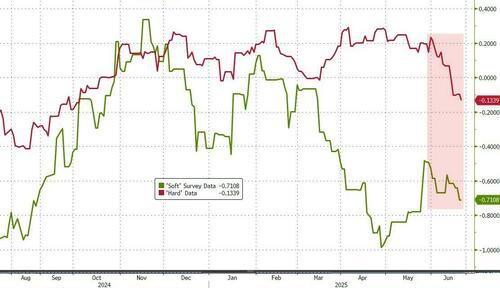

… Fact of the matter is that hard-data has started to catch down to the soft and as is noted out there by those far smarter than I, the coming NFP and CPI reports will either confirm or negate the ever higher rate CUTS pricing of this moment …

ZH: Crypto & MegaCaps Rise As Dismal Data Drags Rate-Cut Odds Higher

A dismal plunge in new home sales prompted further (dovish) increases in rate-cut expectations today, with July at 27% and September at 84%...

…But, US Macro data continues to disappoint with 'hard' data now starting to catch down to 'soft' data...

…And in other news, perhaps most important development for UST complex in quite some time (besides, you know, the clownshow of auditions to become dove-in-chief) … Forgive me if this is old news to y’all … a couple links …

June 25, 2025 at 5:40 PM UTC Bloomberg: Federal Reserve Releases Plan to Relax Key Bank Capital Rule

The Federal Reserve unveiled plans to roll back an important capital rule that big banks have said limits their ability to hold more Treasuries and act as intermediaries in the $29 trillion market.

The Fed will vote Wednesday to propose changes to what’s known as the enhanced supplementary leverage ratio, which applies to the largest US banks like Bank of America Corp., JPMorgan Chase & Co. and Goldman Sachs Group Inc. The revisions would reduce holding companies’ capital requirement under the ratio to a range of 3.5% to 4.5%, from the current 5%. Their banking subsidiaries would see that requirement lowered to the same range from 6%.

“The proposal will help to build resilience in U.S. Treasury markets, reducing the likelihood of market dysfunction and the need for the Federal Reserve to intervene in a future stress event,” Michelle Bowman, the central bank’s new vice chair for supervision, said in a statement accompanying the draft rule. “We should be proactive in addressing the unintended consequences of bank regulation.”…

…Some of the sharpest criticism of the Fed’s proposal to reduce the enhanced version of the SLR has come from Senator Elizabeth Warren, a Massachusetts Democrat who recently wrote a letter to bank regulators. She called the leverage rule a “critical safeguard” that promotes financial stability and warned that the economy already faces risks from President Donald Trump’s tariff policies.

CNBC: Divided Fed proposes rule to ease capital requirements for big Wall Street banks

…On the whole, the plan seeks to loosen up banks to take on more lower-risk inventory such as Treasurys, which are now treated essentially the same as high-yield bonds for capital purposes. Fed regulators essentially are looking for the capital requirements to serve as a safety net rather than a bind on activity…

ZH: Fed Moves To Relax Key Capital Rule For Big Banks To Support Treasury Markets

The Federal Reserve has adopted a draft proposal to ease a key capital requirement for the nation’s largest banks, aiming to reduce regulatory pressure that discourages them from holding low-risk assets such as U.S. Treasurys and to make it easier for these institutions to act as intermediaries in the Treasury market during times of stress, when liquidity is most needed…

…At a public board meeting in Washington on June 25, Fed governors voted 5-2 to advance a long-awaited plan to modify the enhanced supplementary leverage ratio (eSLR)—a post–2008 financial crisis safeguard that requires global systemically important banks (GSIBs) to hold capital against all assets, regardless of risk. The proposal will now be published in the Federal Register and will be open for public comment for 60 days.

…“In the case of the leverage ratio, over-calibration may lead to diminished liquidity in the Treasury markets and other unintended consequences,” Powell said. “A leverage requirement functions best when it is generally a backstop to risk-based capital requirements,” Powell continued, adding that when leverage requirements are binding, they can discourage banks from participating in lower-risk lower-return activities that support the U.S. financial system and economy, such as Treasury market intermediation.

The proposed rule would replace the current flat leverage buffer of 2 percent at the parent bank level and 6 percent at the subsidiary level with a variable buffer based on each bank’s systemic risk score.

That change would reduce total capital requirements for America’s biggest banks by about 1.4 percent, according to Fed staff estimates. While capital requirements for bank subsidiaries would fall by a much larger 27 percent, most of that capital would remain locked within the banking group due to holding company rules and would not be available for shareholder payouts.

The reductions apply to Tier 1 capital—the core capital that includes common stock and retained earnings—used as a primary buffer to absorb losses during times of financial stress.

Supporters of the proposal say that the current version of the leverage rule has become too rigid—penalizing banks for holding safe assets and discouraging them from helping stabilize financial markets during periods of stress. Vice Chair for Supervision Michelle Bowman, who spearheaded the effort, called the recalibration a “sensible and timely” fix that restores the eSLR’s original purpose.

… I’m sure all this is not new news and completely as everyone might have thought BUT the timing of the SLR update / change and efforts to enhance functioning and liquidity in the UST market, well … I’m sure coincidentally coincides with the OBBB and potential onslaught of UST issuance …

Said another way, nothing to see here (no quid no pro quo) … back to our cars, folks. Shows over … onwards and upwards but first … here is a snapshot OF USTs as of 700a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: DXY hit on reports that Trump may name Powell successor early, US equity futures gain slightly into data … USTs are firmer, benefitting from the WSJ reports that President Trump could announce the next Fed Chair much earlier than is traditionally the case. Trump himself has intimated he has the list down to a handful of individuals; unsurprisingly, all those on the WSJ list are or are expected to err on the dovish side of things. USTs to a 111-28 peak thus far, notching another best for the month and now to within a point of the 112-23 peak from May, but of course still a significant distance from the mark. Ahead, 7yr supply rounds off the week’s taps, which have gone well thus far. US data and Fed speak is also due.

Fed futures pricing now sees rates falling 137 basis points to 3% by early 2027 - 30 bps more than it priced a month ago. There is now a one-in-four chance of a cut as soon as July and some 63 bps of Fed cuts by year-end.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Housing … it’s worth watching for obvious reasons (aDURable goods, for example, and moving for a better job, etc) and so, some of the data backing Team Rate CUT(s) …

25 June 2025 Barclays: May new home sales retreat sharply

New home sales fell 13.7% m/m in May, to 623k, alongside a cumulative downward revision of 43k to sales estimates from February-April. The surprise weakness in May could reflect higher mortgage rates during the month, as well as increased median and average new home prices.

Best in show on the day that was with just a mention of SLR (and swap spreads)…

…Wednesday’s choppy price action was contained to a narrow range as Treasury yields remain at the local lows. Despite climbing as high as 4.33% intraday, 10-year yields managed to close below the 200-day moving-average of 4.30% for the second consecutive session in a move that reinforced the constructive momentum for Treasuries in the near-term. Powell’s second day of testimony underpinned the market’s baseline assumption that September 17th will see the resumption of rate cuts, although the implied odds of a move on July 30th climbed up to 25%. The 5-year auction tailed by a modest 0.5 bp, yet end-users took an above-average share of the issue despite the lack of a builtin concession – both on an outright and relative basis. Swaps spreads widened modestly after the release of the Fed’s framework for SLR reform, although there remains an overhang of uncertainty as it relates to the potential for a full exemption of Treasuries from the SLR ratio calculation …

… Treasuries have put in a solid performance in recent sessions with 10-year yields back below 4.30% from above 4.50% as recently as two weeks ago. The fundamental inputs on offer during the final two trading sessions of the week will help define the bottom of the yield range that typically defines the price action in the run up to NFP-Friday. We’re closely watching 4.25% for initial resistance before the starting point of the NFP-driven selloff on May 2nd at 4.21%. Only the daily momentum chart, today’s session saw the fast stochastics slip into overbought territory, although the slow one remains comfortably above 20. For support, the 200-day moving-average remains a focal point at 4.30%, and through there we see the 100-day moving-average of 4.36%.

DBs early morning catchup with a few words on the what next …

… With markets holding steady, we’re now at a point where the focus is turning to several important catalysts over the next two to three weeks. The first is the US tax bill, which is currently working its way through the Senate, and the administration is trying to get it passed by Independence Day on July 4. To achieve that, things could move quickly from here, and Senate Majority leader Thune has previously said to Axios that they could start voting on the bill tomorrow. Moreover, Politico also reported earlier this week that House Speaker Johnson told House Republicans to stay in town, given that the House needs to pass the same version as the Senate before President Trump can sign the bill. So it’s a fluid situation on timing, but given the upcoming July 4 deadline, it will need to move swiftly in the days ahead in order to pass by then. Remember that alongside the tax cuts, the bill also contains an increase to the debt ceiling, so if passed, it would remove that risk from the summer as well.

As well as the tax bill, the focus is set to swiftly turn back to tariffs, as the 90-day extension to the reciprocal tariffs ends in less than two weeks’ time on July 9. As it stands, it’s still unclear what will happen at that point, although several countries remain in negotiations with the US. The administration has signalled that trade deals are likely to follow the passage of the tax bill, and NEC director Kevin Hassett said earlier in the week that “We know that we’re very close to a few countries and are waiting to announce after we get the Big Beautiful Bill closed”.

After that, the June CPI report on July 15 is likely to assume outsize importance, as that’ll be crucial for whether the tariff pass-through is being felt in consumer prices. Only yesterday, Fed Chair Powell mentioned the uncertainty around this, saying that in terms of who’ll pay for the tariffs, “it’s very hard to predict that in advance”. But it’s crucial for the path of rate cuts, as those officials calling for caution have in part based that around the tariff impact showing up in the summer inflation numbers. We’ve already seen an impact in categories like major appliances, and even with the 90-day reciprocal tariff delay, there’s still the baseline 10% in place, as well as others in place like the steel/aluminium tariffs, the Canada/Mexico tariffs, and the China tariffs…

Haven’t seen an updated MIDYEAR in a while and this one hales from Jamie Dimon’s operation … here’s an excerpt pertaining to USTs (where they would buy 2s on DIPS and maintain 2s 10s end year forecast (3.50% and 4.35%) …

…Treasuries Treasuries have put in a mixed performance: front-end and intermediate yields have declined 15-35bp, while the long end has lagged and yields have risen modestly. However, this masks more significant volatility, as most of the Treasury complex has traded in a wide 70-90bp range YTD. Amid this steepening trend, the Treasury market has had four different thematic trades YTD. First, the term premium story took hold in early January, with US and UK yields rising quickly just before President Trump’s inauguration. Second, sentiment data weakened through the winter, driving yields lower as recession risks increased. Third, the narrative switched quickly to stagflation, as the so-called “Liberation Day” tariff announcement not only increased downside risks to growth, but also sharply increased inflation risks, driving yields higher for a period in mid-April. Fourth, fiscal policy took center stage in mid-spring, and long-end yields increased sharply in the US and across DM government bond markets, as investors began to grapple with rising government debt amid shortening duration demand globally.

Looking ahead to 2H25, we think the front end of the Treasury curve offers strategic value: recession risks have declined from their peak, but remain elevated as growth is expected to slow over the balance of the year. The front end appears somewhat cheap after adjusting for the Fed’s reaction function and changes in growth expectations (see Treasuries, US Fixed Income Markets Weekly, 6/6/25). However, money markets are pricing in an earlier and more aggressive path of Fed easing than our own forecast, as OIS forwards are pricing in a full 25bp ease by early-fall and close to 50bp of easing this year. Moreover, risk-adjusted carry is punitive front end. Thus, we do not recommend adding duration at current levels. That said, we would look to add exposure if 2-year yields retraced to the top end of the recent range near 4.05-4.10%.

Moving out on the curve, long-end yields remain at levels that persisted prior to the GFC. We’ve argued for the last two years that the rapid growth of the Treasury market has outstripped demand from the Fed, foreign investors, and banks, which had comprised a 60-70% share of ownership of the Treasury market in the post-GFC era, and their share is set to decline further (see In the eye of the beholder, 9/12/23). Long-end yields retracing to their cycle highs last month, against the backdrop of easier monetary policy than the last time they reached these levels, is consistent with rising term premium. Indeed, the widely-followed ACM model published by the New York Fed has risen by 175bp since mid-2023, to levels seen at the tail end of the taper tantrum (Figure 17Term piuhasren ply,thoug iremans owhtbel vshatperisd otheGFC). While this is a big move, it is not unexpected: term premium has retraced closer to average levels observed in the decade prior to the GFC, and does not seem to be unduly high in our opinion right now. Moreover, the demand for longer duration assets seems to be receding globally now as well (see US Treasury Market Daily, 5/22/25). Given this backdrop, we maintain our forecast that 2- and 10-year yields will end the year at 3.50% and 4.35%, respectively.

The question we’ve received recently is whether there is a risk of another large repricing to higher yields. There is scope for a further 40-50bp increase in term premium over time, but we do not see the ingredients for another explosive move in markets now, like what we observed over the fall of 2023, the fall of 2024, and earlier this year. Importantly, positioning is much cleaner: ahead of the large selloffs in the fall of 2023 and earlier this year, active investors had been overweight duration, as our Treasury Client Survey and core bond fund index were more than 3 standard deviations above their trailing 1-year averages (Figure 18). Ultimately, as fundamentals shifted, these longs were liquidated, exaggerating the moves to higher yields. Currently, both of these position indicators are close to averages observed over the last year, and do not indicate that there is a large duration overweight that is at risk of being unwound.

Similarly, market participants remain on edge and see parallels with the UK gilt market prior to the disruptive mini-budget sell-off in September 2022. We agree that a high debt-to-GDP ratio coupled with a fragile environment for intermediation has lowered the bar for a disruptive rise in long-term yields. However, the average maturity of the Treasury market is substantially shorter than that of the gilt market, and without the same concentrated ownership and leverage risks. Therefore, we think the risk of a “Truss moment” in the US is relatively low right now (see Treasuries US Fixed Income Markets Weekly, 5/30/25)…

Sizeable miss in Australia CPI; Fed announces SLR reform; USTs bull-steepen; European currencies gain amid NATO defense spending agreement; French OATs outperform; BoJ's Tamura reiterates he sees rate hikes even if uncertainty persis; DXY at 97.70 (-0.2%); US 10y at 4.291% (-0.4bp)

…The Fed proposes to change the enhanced supplementary ratio (eSLR) for GSIBs from a flat 2% rate to 50% of Method 1 GSIB surcharge; SOFR swap spreads marginally widen (30y: +0.5bp), bank stocks outperform (KBW Banking Index: +0.7%), though reaction is muted.

USTs marginally bull-steepen in a relatively quiet session as housing data disappoints, rallying even as Chair Powell reiterates the Fed's cautious stance and the 5y auction tails by 0.5bp…

…In the NY afternoon, the UST rally had started to stall, and the 5y auction seemed to corroborate a slight softening in demand. The auction tailed by 0.5bp with a cut-off yield of 3.879%. The bid-to-cover-ratio edged down to 2.36x (P: 2.39x; 1y Average: 2.39x). The pullback came from indirect participants whose allotment fell to 65% (P: 78%; 1y Average: 70%), but was partially offset by direct participants whose allotment rose to 24% (P: 12%; 1y Average: 18%). This left primary dealers with an allotment of 11% (P: 9%; 1y Average: 12%).

The UST rally eventually regained momentum heading into NY close as the Fed OIS curve continued to reprice lower. Ultimately, the curve bull-steepened with the front end 1-2bp lower and the long end largely unchanged.

The Fed held an open Board Meeting to discuss proposed revisions to the Board’s supplementary leverage ratio (SLR) standards. The enhanced supplementary ratio (eSLR) would reduce the buffer for GSIBs from a flat 2% rate to 50% of the Method 1 GSIB surcharge e as determined by the Board’s GSIB risk-based capital surcharge framework (for more, read here). Following the announcement, bank stocks outperformed (KBW Banking Index: +0.7%) and SOFR swap spreads marginally widened (30y: +0.3bp). However, the reaction was fairly muted as media reports previously speculated on the proposed framework…

… somewhat more on SLR from a closing commentary from a shop domiciled across the pond …

…reasuries traded mixed to weaker for much of today’s session before finding footing in the afternoon and finishing slightly stronger, and bull steeper, across the curve. The apparent catalysts were a solid 5-year auction and the Fed’s draft notice of proposal to change the bank supplementary leverage ratio (SLR) applicable to global systemically important bank holding companies (GSIBs). Leverage ratios establish minimum capital requirements a banking organization must hold against its assets, unadjusted for risk of those assets. The proposal, although still in draft form and now subject to a 60-day comment period, suggested capital relief for banks via a lower SLR that would allow banks to hold less total capital, which the proposal says will allow for greater capital allocation into lower risk activities, such as Treasury market intermediation. This reform will be welcome for banks, but it notably did not include more drastic measures such a “carve out” of Treasuries or Treasury repo from the calculation of these capital ratios. Because of that, we see this proposal as on the light side of what markets could have expected from today’s announcement. We think that banks will be pushing over the next 60 days for more aggressive measures to be included, like carve outs for Treasury assets and Treasury repo, although some Fed members (Barr and Kugler specifically today) have already pushed back and said that these more modest changes would increase systemic risk and not lead to banks allocating capital to lower risk activities. Nonetheless, Treasuries gained today in part on the confirmation that changes are officially underway, even if such a proposal was already well telegraphed.

From a higher-level view, markets and certain officials have been looking towards bank capital regulation for quite some time as a way to increase broker-dealer activity and to avoid the leverage ratios becoming a binding constraint during stress events. This would include, for example, the massive volatility seen in Treasury and swaps markets post Liberation Day, when broker-dealers pulled back and liquidity worsened to exacerbate the sharp move. This type of reform, and Treasury carve outs specifically, would also allow banks to buy and hold more Treasuries to help offset and intermediate in the massive increase in Treasury supply seen over the last few years with more expected in the coming years. But one could also note that without these changes, which would in theory help alleviate the weight of increased Treasury supply in markets (via greater market liquidity and banks as a larger marginal buyer), the onus would remain on the fiscal authority to spend less. For that we must continue to watch progress on the budget bill that is inching its way through the Senate, with Republicans still hoping to vote on the OBBBA by this weekend.

Swiss (British) stratEgerist seems annoyed … maybe it’s just me …

The Wall Street Journal reports US President Trump may announce the next Federal Reserve Chair in September or October. The Senate needs to confirm the Chair, and in Trump’s first term was prepared to oppose several of Trump’s Fed nominees. Only convention prevents the Fed from overruling the Chair—an obvious political appointee may be ignored by the FOMC. The greatest threat to policy independence would be someone who was not an obvious political puppet but was swayed by Trump’s instructions.

US first quarter GDP is due for revision (no changes are expected). This records economic activity before much of the impact of trade taxes, government disruption, and immigration roundups. It is a reminder of US economic strength at the start of this year, which is important as it provides a firm foundation for activity in the face of subsequent damage to growth.

US May trade and inventory data will give some hints as to the effects of trade taxes, and maybe a suggestion as to how long it will be before those taxes show up in consumer prices…

… more on housing from a large provider of mortgages to the USofA …

June 25, 2025 Wells Fargo: New Home Sales Retrench in May High Mortgage Rates and Growing Resale Supply Discourage Buyers

Summary New Home Sales Fall Back as Buying Conditions Worsen Following a jump in April, a move up in financing costs slowed new home sales in May. New home sales tumbled 13.7% over the month to the weakest pace in seven months (623K). The South experienced a particularly notable drop-off. The trend so far this year amounts to a 3.2% year-to-date decline in transactions, reflecting mounting headwinds to new home demand. According to Mortgage News Daily, mortgage rates breached 7.0% in May, reaching the highest level since February. Mortgage rates have retreated somewhat since but remain a substantial barrier to home buying. Rising resale inventory and less-intense price appreciation for existing homes are also notable headwinds, especially as new home inventories remain at their highest point since October 2007. That said, a recent downtrend in single-family housing starts may ease the supply overhang somewhat.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

…“The markets are very overbought on a short-term basis and leadership is concentrated heavily toward S&P 500 and Nasdaq 100 (NQ=F),” said Dan Wantrobski, technical strategist and associate director of research at Janney Montgomery Scott. “If breadth does not follow the breakouts in S&P and Nasdaq, then we will be on the watch for a correction.”

…Breaking Out Among the 11 S&P sectors, information technology, industrials and communication services are the only three that have touched all-time highs. Meanwhile, the small-cap Russell 2000 Index still has a long way to go to reach the high of late November, just after Trump won the US election and sparked a wide risk-on rally in stocks.

But some technicians are seeing encouraging signs.

Mark Newton, head of technical strategy at Fundstrat, says this week’s show of strength in industrials, transports, consumer discretionary and financials — even though some of these groups are yet to make fresh records — is a compelling reason to stick with equities.

…Momentum Signal Some chartists also say the relative strength index, which is a momentum indicator that shows whether an asset’s prices have veered too quickly in one direction, is projected to move into a bearish zone later this summer. That typically indicates a reversal may be around the corner. At the moment that index shows that the S&P 500 is hovering close to overbought territory on a 14-day basis.

Finally, with all the goings-ons in NYC with regards to Mayoral race AND at risk of getting TOO political …

ZH: Wall Street Panics As Socialist Set To Take Over New York, REITs Tumble At The Idiocy Of It All

… In a midday note from Goldman's trading desk, the bank noted that its NYC Office REITs basket tumbled 430bps amid the "big focus on the back of Mayoral Candidate Zohran Mamdani winning last night. Lot of inbounds on what this potential administration means for NYC exposed REITs, particularly across Office and Apartment REITs with exposure to NYC."

Some developers and landlords said they are already making plans to exit New York and focus on more business-friendly markets like Miami, Dallas or Nashville…