Good morning … ‘tech difficulties’ on this side — heck of a way to kick off the ‘golden age’ and just catching up on all the goings on past couple days since hitting SEND over weekend and we’ve now gotten 47, couple new memecoins, and more than several executive orders, for the more economically and geopolitically minded scientists out there, to digest … I only listen to ONE and you may have heard of him (don’t actually know its pronouns) … Mr. Market(s) …

… all is well, stocks AND bonds are bid and EARLs down …

… here is a snapshot OF USTs as of 829a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries opened firmly in Tokyo with real$ demand seen in the belly as 5s squeezed to 4.33%. The bid proved short-lived on tariff headlines (Mexico and Canada on Feb 1st), with futures heavy throughout Lond despite some cash buying seen in the franchise. USTs are still outperforming Gilts & Bunds into a light-data session, though 2s5s10s has given back much of the overnight richening, now -1bps from -2.25bps richer after the Asia open. 2s10s is -3bps and 5s30s -1bp flatter. Overall volumes started elevated but have gradually come down heading into the NY session. Crude Oil is -2.5%, Gasoline -1.1%, with copper -1.5% as well. S&P futures are +0.4%, the DAX flat, after muted APAC risk-asset performance (NKY +0.3%, SCHOMP -0.1%). USDJPY is flat after opening -0.5% lower, CAD -0.9% and MXN -1%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: US Market Open: US futures edge higher, DXY bid whilst CAD & MXN take a hit as President Trump signals tariffs … USTs have been gradually fading from best throughout the morning as we prepare for Trump’s first full day back in office. As it stands, USTs are holding around Monday’s 108-24+ best. Monday price action was fairly contained up until the WSJ piece (re. tariffs) drove USTs to a 108-24+ peak.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

This note speaks TO inauguration day but the content mostly in / around an FX theme … for any / all who might be funTERtained…

First up is a note on day one and another on when the easing cycle will end …

ABANAMRO: US Watch – Trump Day 1: Executive order galore | Insights newsletter

Donald Trump wastes no time in enacting his policy, signing a series of executive orders. There were actions on immigration, (energy) inflation and government hiring policy. There were no explicit orders enacting tariffs, but the threats continued....

ABAmro: Fed Watch – Easing cycle will end in restrictive territory | Insights newsletter

We expect one or two more Fed cuts in the first half of 2025, after which the easing cycle is put on hold indefinitely, leaving the policy rate in restrictive territory. We expect inflation to ease in the first half of the year, allowing for further cuts, while some weakness in the labor market will provide the necessary call for action.

… interesting, to be sure … next up is something written / sent BEFORE the inauguration … and on THAT — inauguration — note, following note is another dedicated entirely …

President-elect Trump has said he is planning to sign 100 executive orders today; an unprecedented number. What do investors need to know?

…In our view, we are likely to see executive orders from President Trump in three categories:

Rescinding certain executive orders that President Biden had signed

Reinstating certain executive orders from his first term that President Biden had revoked (No recent president has reversed a predecessor's executive orders as often as Biden reversed Trump - 67 in his first 100 days.)

Issuing new executive orders focused primarily on six policy areas: immigration, energy and the environment, trade, deregulation, technology, and government reform

We have included a list of all the executive orders (with links to the orders) signed by President Trump during his first term and President Biden at the end of this note. A major portion of what we expect on day one likely will be in the first two categories…

Into Trump’s inauguration, we remain long inflation via 5y breakevens and 10y TIPS, long VIX and long USDCAD. The repricing higher of nominal yields and the USD since November suggests quite a lot is already priced in by way of tariffs. However, moves in real yields and the performance of tariff sensitive vs. insensitive currencies imply more room for the impact from tariffs to be priced in.

Tariffs aside, any weakening in US economic data could squeeze consensus positions given stretched levels.

We think the PBoC will only start moving its FX fixing once tariffs are officially announced, which means a cap on USDCNY around 7.33–7.34. The FX options strike map suggests investors expect USDCNY to reach 7.50 sooner rather than later.

Same French shop, different note — mostly FX but a bigger, MONTHLY look with a page on US rates which, of course, catches my interest …

…USD rates: No more Fed cuts in 2025 Fed to pause its rate-cutting cycle: We believe the Fed is done with its easing cycle and will keep rates steady throughout 2025.

Firstly, US economic growth looks resilient with a strong December payrolls print and PMIs ticking higher. The Atlanta Fed GDPNow projects a 2.7% GDP print for Q4, well above trend. The Fed also expects the long-run unemployment rate to remain steady at 4.2%. In addition, TCJA extensions with a few sweeteners should boost corporate profits, increase equity prices and boost household net worths further.

Secondly, core CPI has printed four times in a row at 0.3% m/m and the Cleveland Fed Nowcast suggests two more such results in December and January. That would be a definitive stall in inflation progress before tariffs have even been implemented. Long-term inflation expectations from the University of Michigan also jumped to their highest since 2008, even while gas prices fell. We expect tariffs and tighter immigration policy will bring y/y headline inflation back above 3% and risk de-anchoring long-term inflation expectations. That is why the Fed raised its end-2025 PCE inflation estimate by 40bp at the December FOMC meeting.

Lastly, the Fed has switched tone in recent months, with the FOMC minutes citing "almost all saw increased upside risks to inflation" and "most saw policy as now significantly less restrictive.“

Overall, we expect the Fed to pause rate cuts at the January meeting.

Yields are close to their peak, with downside risks in H2 2025: US yields sold off following the December FOMC meeting and the curve steepened, as the Fed is incorporating implications of Trump's policies into its long-term inflation and growth forecasts while also raising the long-run neutral dot to 3%. We believe the US rates market has likely priced in peak Fed hawkishness and soft-landing expectations, as evidenced by Fed pricing implying just 1-2 cuts this year, 10y yields back above 4.70% and term premium at its highest level since 2015. As a result, we expect yields to remain at or near their current levels for H1 2025.

However, we believe the anticipated stagflationary impact of Trump's policy mix has yet to be fully reflected in the market. CPI fixings are pricing the end-2025 level about 100bp below our forecast. Meanwhile, our economists believe tariffs and immigration policy will weigh heavily on productivity into 2026 with potential reductions to healthcare spending to offset the benefit of tax cuts. In this environment, we believe the Fed would prioritize growth over inflation, leading to lower nominal and real yields, as well as higher inflation breakevens in H2 2025.

In this next note, a rather large German institution and fan fav offers an economic chartbook on DISINFLATION …

DB: US Inflation Outlook: Fed's disinflation story holds (for now)

…Details within the CPI and PPI point to 0.20% core PCE print for December

…Progress on core PCE showing signs of stalling out

What NEXT? Global Wall never short on answers to questions (both those asked as well as those you have not yet thought up …) and this next note (on rates / USD) written by … the stock jockey in chief …

MS: Sunday Start | What's Next in Global Macro: Rates and the Dollar Remain Front and Center Michael J Wilson

Since December, stocks have traded with more two-way risk than in the prior three months. Furthermore, the breadth of the market has deteriorated, with higher-quality leadership emerging and earnings revisions for this cohort strengthening.

This all makes sense in the context of rising back-end rates and US dollar strength. Going into the election last year, I thought that a Trump win/Republican sweep would be good for stocks but bad for bonds on the view that it could spark a surge in animal spirits as in 2016 on hopes for a more pro-growth/business-friendly agenda. However, the US fiscal situation is much different today, as are the markets’ reaction functions to prospects of stickier inflation. As a result of these changes, the recent move higher in rates has been driven mostly by a rise in the term premium rather than higher growth expectations. I attribute this to a newfound (and justified) concern about how the ongoing fiscal deficits will be financed, given the exhaustion of the reverse repo facility and the need to extend maturities after the elevated T-bill funding over the past several years.

In early December, we suggested that the 4.00-4.50% range on the 10-year Treasury yield was the “sweet spot” for equity multiples. We thought that a break above 4.50% on the 10-year could increase stocks’ rate sensitivity, as this was an important threshold in spring 2024 when the “no landing” narrative came back into market pricing. As rates pushed above this level in December, multiples compressed and the correlation between equity returns and bond yields settled decisively in negative territory, where it remains today.

Importantly, rate sensitivity works both ways. In fact, the correlation between equity returns and yields fell again following last week’s light CPI report as stocks rallied materially on the back of lower rates. All this supports our latest thinking for US equities – i.e., index direction (beta) will be primarily determined by the level and direction of back-end rates and the term premium. And until the 10-year yield falls back below 4.50% and/or the term premium declines on a sustainable basis, this negative correlation between stocks and yields is likely to persist. We continue to prefer higher-quality stocks across industries showing relative earnings revisions momentum – Financials, Media & Entertainment, and Consumer Services over Consumer Goods…

The presidential inauguration on 20 January should set the stage for what’s to come. Global bond yields rise and fall with US data leading the way. With the Fed on pause, markets await clarity on policies from the incoming Trump administration. This may or may not come immediately, suggesting that there is still a chance for yields to continue to test new highs with macro uncertainty as the culprit.

…United States Off to a good start Following a strong December jobs report, a softer CPI print and strong retail sales, justifies the Fed pause at the January FOMC meeting. While the data shows a strong economy and moderating inflation, the Committee’s bias remains towards easing, but later. Waller suggested the possibility of a June rate cut but did not rule out March. Treasuries flip-flopped with the incoming data, reversing the post-NFP sell-off with the below-consensus CPI print. Bonds are likely to chop around within a range over the coming weeks as we await more clarity on the policies of the incoming Trump administration and an extended pause on monetary policy. We remain neutral on duration and view a move toward 5% 10yT yield as a buying opportunity. We recommend tactical trades ahead of the auctions next week.

Recommendations Enter UST 3s7s steepener one business day before the 2y note auction and exit the day after the auction.

…We especially favour the Treasury 3s7s steepener trade, which involves getting into the position one business day before the 2y note auction and exiting the day after (Graph 6). This tactic has consistently yielded positive returns, with an average profit of 2.6 basis points (Graph 7) and has resulted in gains throughout all 12 of the recent 2y auction cycles (Graph 8).

The bond and stock markets were closed today for MLK Day. When they reopen tomorrow, we will all be able to assess their initial reactions to Trump 2.0 following today's Inauguration ceremony. The major stock market futures indexes were up all day. Bitcoin soared in the morning, but turned down in the afternoon. Gold and copper prices fell slightly.

The dollar sold off after The Wall Street Journalreported that Trump isn't rushing to implement new tariffs. Instead, he plans to send a memo to federal agencies directing them to evaluate trade policies and economic relationships with China, Mexico, and Canada.

In other words, there might not be much of a shock-and-awe effect on the markets from Trump 2.0 initially since most of it has been discussed by Trump during his campaign speeches. Instead, the markets might continue to focus on Fedspeak and the latest earnings reporting season. Both were bullish last week. Last Thursday, in a CNBC interview, Fed Governor Christopher Waller was dovish. Waller's comments pushed bond yields down, as did the recent batch of lower-than-expected inflation reports (chart).

Also last Thursday, the big banks reported better-than-expected earnings for Q4-2024. Collectively, analysts now expect S&P 500 earnings to rise 9.1% y/y for the quarter, up from their previous estimate of 8.2% (chart). We are raising our Q4 earnings growth estimate from 10.0% to 12.0% y/y. We had thought it would be a strong earnings reporting season. Now we think it will be even stronger.

… And from the Global Wall Street inbox TO the WWW … a few curated links from the web … and what better place to start than with a few words of positivity from Torsten Slok …

The incoming data continues to show a strong US economy with tailwinds from data center spending, AI spending, defense spending, and government spending via the CHIPS Act, the IRA, and the Infrastructure Act.

Combined with additional tailwinds to growth from high stock prices, high home prices, high crypto prices, Fed cuts, higher animal spirits, and potential Trump policies, the bottom line is that the US economy is entering 2025 on a firm footing.

With GDP currently at 3.1% and core inflation at 3.2%, we continue to worry more about upside risks to growth and inflation.

Our latest chart book with daily and weekly indicators for the US economy is available here.

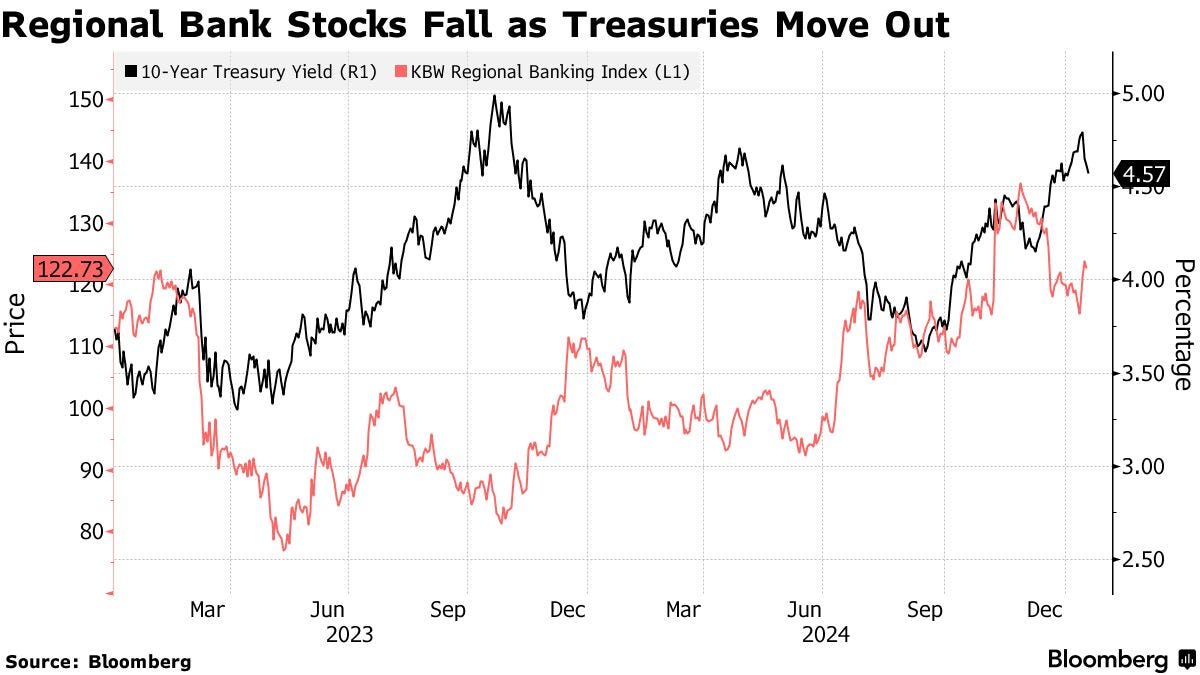

Bloomberg story on (negative)impact of rising yields on regional banks …

Bloomberg: Regional Banks Face Headache From Rising Treasury Yields

Rising 10-year yield could exacerbate CRE, securities losses

About 44% of office loans are underwater in the US: researcher

… A surge in 10-year yields last year likely reversed most of the decline in unrealized losses on banks’ available-for-sale and held-to-maturity securities in the third quarter, Federal Deposit Insurance Corp. Chairman Martin Gruenberg said in a Dec. 12 speech. Even after this past week’s rally after better-than-expected inflation data, the benchmark has since risen about 0.3 percentage points to around 4.58%, adding to the pain for lenders.

If borrowing benchmarks remain high, regional banks risk higher losses on commercial real estate because borrowers will struggle to refinance, said Tomasz Piskorski, a finance and real estate professor at Columbia Business School. He and fellow researchers estimate about 14% of the $3 trillion of US CRE loans are underwater, rising to 44% for offices…

…Smaller lenders are more vulnerable to CRE defaults after demanding lower down payments from borrowers than their larger counterparts in the run up to the interest-rate hikes that began in 2022. Now that office and multifamily values have crashed, the lenders have less of a buffer before taking losses.

The office market has yet to stabilize “which is why we remain concerned and remain well-reserved,” PNC Financial Service Group Chief Executive Officer Bill Demchak said on an earnings call this week. The bank increased the reserves it set aside to cover soured office loans to 13.3%, up from 8.7% at the end of 2023, although it’s a small proportion of their overall book….

This next link / visual is from LinkedIN and cites a St Louis FED study … something to watch / investigate in all ones ‘free time’ …

It will be VERY interesting to see how the Fed (and other central banks perhaps) react to the new administration's policies. The Fed is not exactly known for being proactive. This chart is from a study of the St. Louis Fed that seems to corroborate this. They tracked "sentiment" in the beige book, which they proxied using the "net" of positive words minus negative words. Interesting to see that it is more or less coincident with real GDP growth. I can't say that this is a bit surprise, but it is pretty cool to see it quantified this way. Also, this does seem to be one point of consistency across time irrespective of who was Chair ... that part somewhat surprised me. I was hoping the central bank would look a little less reactive after it transitioned to monetarist principles under Volcker, but that does not seem to be the case. Anyway, just interesting stuff. Happy Sunday…

…Trea$urie$ Apparently the Treasury Department will need to use “extraordinary measures” on January 21st to avoid hitting the debt ceiling. That seems like big news, and anything but a gift to the new administration. I don’t remember hearing that we were that close (the day after President-elect Trump is sworn in) and it was certainly not mentioned during Yellen’s presentation in NYC on Wednesday that I had the pleasure of attending (with a front row seat). I wouldn’t play poker with her after that though. Lots of talk about how they did everything right, and basically the deficit is where it needed to be, but has to be fixed going forward. However, no mention of the imminent need to take “extraordinary measures.”

I listened to a lot of Scott Bessent’s hearings (I was driving on my way to the homeland, which as of now, is not yet the 51st state), and didn’t hear anything about how he would need to use extraordinary measures once he takes office. I honestly don’t know when he gets confirmed, but that was also because I didn’t think day one of the administration would coincide with the start of a dumpster fire.

One of my favorite “measures” is that the Treasury has the ability to give certain funds (the Civil Service Retirement and Disability Fund, for example) IOUs for Treasuries rather than Treasuries. Since a Treasury bond is already to some extent an IOU, it seems both circular and bizarre, but it is part of the law of the land.

With this ability to issue “IOUs for Treasuries” rather than Treasuries, I presume there are many more loopholes that wouldn’t make sense to any market participant, but made sense to the lawmakers, so I’m not worried about the potential for a breach. Having said that, some within the new administration might see breaching the ceiling and being forced to stop a variety of payments and activities as a step towards cutting the deficit. Seems like a crazy idea and would be well “outside the box,” but since we now have what is effectively a presidential meme coin, I’d be hesitant to say that anything is too far-fetched!

AND finally, ZH on BAMLs FLOW SHOW (noted over the weekend HERE) …

ZH: Hartnett: Historic Rout In Treasuries Ending As "Trump Can't Allow Bigger Debt And Deficits"

“20-year corporate bonds now yielding 6.3%...you would think with stocks up 20% past 2 years pension funds would be looking to park some of those gains in bonds” - Michael Hartnett, zeitgeist quote, Jan 17

… Hartnett blames the Fed for the latest leg of this historic rout, and why not: we did just that a month ago, when we showed the mirror image in 10Y TSY yields and the Fed Funds rate ever since Powell's "jumbo" rate cut in September, which triggered the latest bond rout…

… And with that in mind, we turn to Hartnett's latest take on bonds and stocks, where he makes the following observations:

Bond selloff is ending: 5% on 30-year Treasury yield not breached, means "twin peaks"...

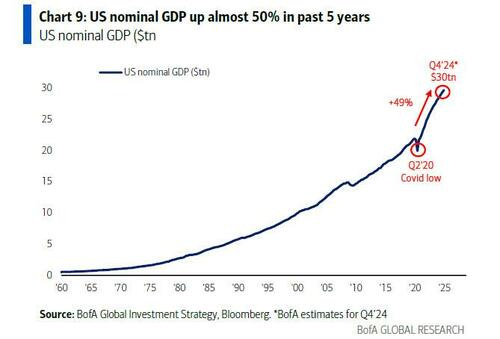

... 2.5% on 10-year real rates also not breached; meanwhile, the Fed's 2025 rate cuts have been priced out and Trump can’t allow bigger deficits & debt since the US has a $7.3tn government, making it the 3rd largest economy in world = biggest driver of 50% jump in US nominal GDP past 5 years...

... and this number won’t be growing in ’25; to this add that the Fed is now more serious on inflation, and Trump is serious on deficits, and Hartnett believes that "investors likely need to be less UW bonds."

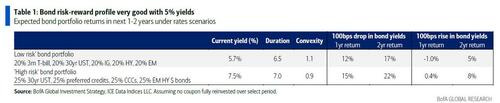

Bond potential returns: the current 5-6% yield plus high convexity means a "low risk" bond portfolio (20% T-bills, 20% 30-year US Treasury, 20% IG, 20% HY, 20% EM) generates11-12% if yields fall back toward 4%; returns potentially 14-15% on 'higher risk' bond portfolio (25% 30-year US Treasury, 25% preferred credits, 25% CCCs, 25% EM $ HY) given same move in yields. Said otherise, Hartnett is certainly turning bullish on bonds.

… more hopefully once tech issues worked out but … THAT is all for now. Off to the day job…