Good morning … Today, the 23rd anniversary of the horrible evils of this day in 2001 is tougher for some than others and at the very same time, today’s a day to be grateful for each day we’ve got and for all the opportunity around.

Today’s note is not something more special than anything else you’ll stumble on and there are true stories of heroism and fortune.

I’m grateful for the chance to be here and this chance was NOT afforded to many who perished … on this day, 23yrs ago

The 23rd anniversary will be marked by many at precisely 846a, 903a, 937a and finally, 1003a … if you know you know. You remember exactly where you were and what you were doing / thinking and feeling at each of those moments, 23yrs ago.

These moments will likely be drowned out by the machinations of our geopolitical machine and repercussions of ones SPIN of how the dust settled after last nights debate.

I’m not going to weigh in on either and simply do as I do every year. I’ll leave work tonight, grateful for whatever commutes i’ve suffered through in the past and will in the future. They may be terrible but I’ll make it home. To my family. My oldest is 23yrs old and was about 6mo on this day, 23yrs ago.

This evening, I’ll head to my local municipality ceremony which honors the local FDNY, NYPD and first responders, and their families, who made the ultimate sacrifices that day.

Many of these men and women of our community are coaches and teachers that had — and continue to have — a huge impact on my family.

May their memory forever be a blessing.

We must never forget, despite whatever the clown show of the moments may be in political, as well as markets, theater…

About last night … well, it was about MORE than a debate between a couple of living politicians. About last night … it was, in fact, more than just words … here are a few more words … About LAST night …

246 people went to sleep in preparation for their morning flights. 2,606 people went to sleep in preparation for work in the morning. 343 firefighters went to sleep in preparation for their next shift. 60 police officers went to sleep in preparation for morning patrol. 8 paramedics went to sleep in preparation for their morning shift of saving lives and 1 K9 went to bed a good boy …

None of them saw past 10:00 am the next morning Sept 11, 2001. In the blink of an eye, their lives were cut short.

Tonight, as you prepare for bed in preparation for your life tomorrow, kiss the ones you love, snuggle a little tighter, and never take one second of your life for granted.

… About Last night … source unknown.

… …

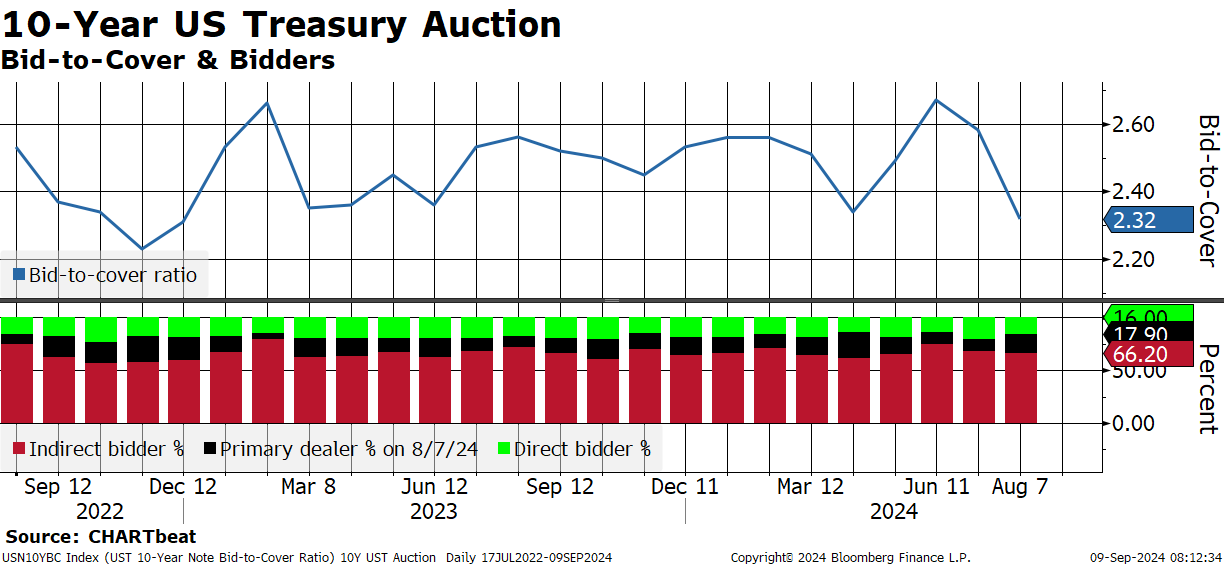

Now moving on to the matters at hand and ahead of this mornings ($39bb 10yy) #UpcomingAuctions …

10yy: 3.60 appears to be next resistance level to watch …

… and as bonds become overbought — can remain so until facts change — i ask if it’s flight to quality (ie FEAR of Harris and economy), Oil down, rate CUTS, all of the above and / or something I have neglected to mention??

… with that in mind, a few visuals from someone (CHARTbeat) with a terminal …

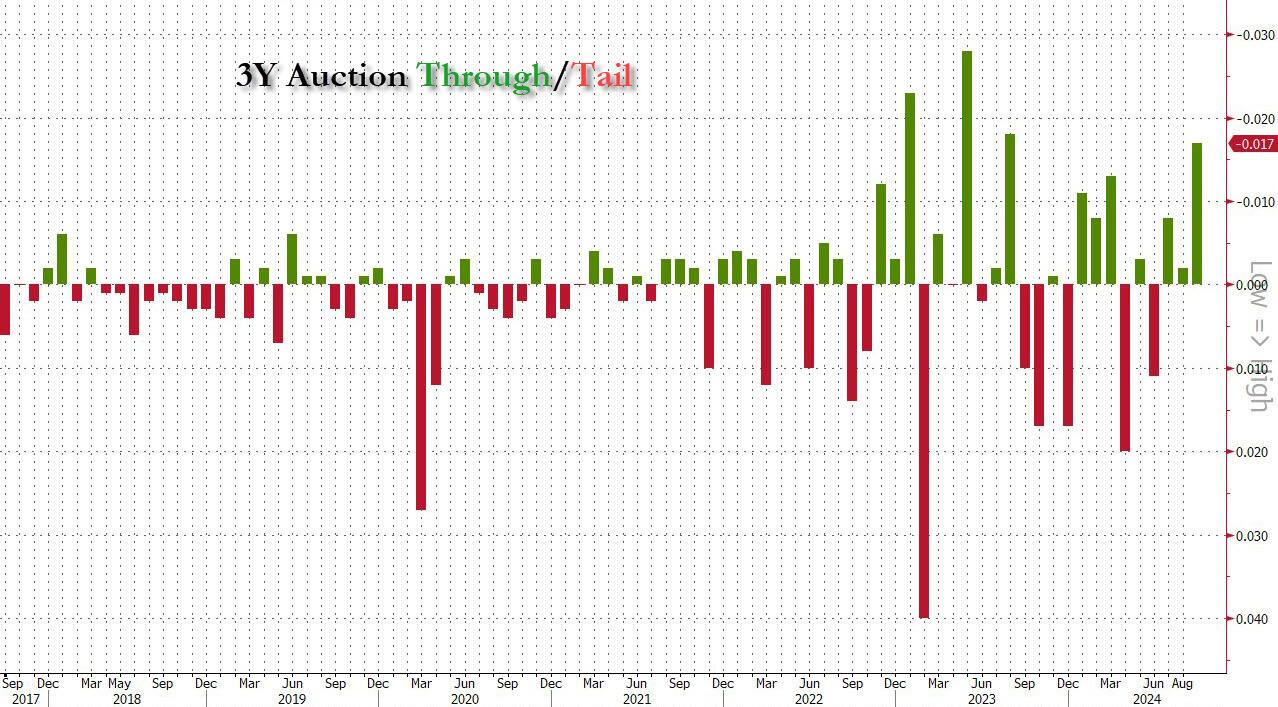

… and a quick review / recap of how yesterday’s 3yr auction came and went just ahead of the widely anticipated rate CUT …

ZH: Stellar 3Y Auction Stops Through, With Highest Bid-to-Cover On Record

…Pricing at a high yield of 3.440%, the 3Y auction was not only 37bps below last month's 3.81% and the lowest since August 2022, but also stopped through the 3.457% When Issued by 1.7bps, the biggest Through since August 2023 and the 4th biggest on record.

As one would expect for a auction with big demand, the bid to cover jumped to 2.662 from 2.551, above the recent average of 2.564.

… and so, let us HOPE this afternoons 10yr auction goes as well.

Living in hope and trying not to die in fear, we’ll move right along and … here is a snapshot OF USTs as of 651a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures lower & DXY subdued following the US Presidential Debate ahead of US CPI … Bonds are entirely in the green continuing the price action seen in the prior session; Gilts outperform after softer-than-expected UK GDP metrics … USTs have extended on their recent upside amid a slew of factors, including yesterday's strong 3yr auction, anticipation of Fed easing ahead of CPI, recent downside in oil prices and Harris' performance in the debate last night. The 2yr yield is at its lowest level since September 2022.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

First up some longer-form (monthly) thoughts / charts straight from largest, most well known (and sponsor of an overseas tennis tournament) FRENCH bank in the land

USD rates: Yields to fall gradually with Fed rate cuts Near-term risks point to higher rates, flatter curve: In the near-term, we forecast higher yields and a flatter curve versus the forwards as healthy labor market rebalancing eases concerns of a hard landing for the US economy. This allows the Fed to cut rates at a gradual 25bp/meeting pace starting at the September FOMC decision. We forecast a series of 25bp cuts to next March, then shifting to every other meeting until the fed funds rate approaches 3.00%.

Medium-term baseline is for lower yields, steeper curves: However, our medium-term baseline is for the US to avoid a recession but still moderate to around potential growth in H2 2024 as consumers become more selective and election uncertainty delays some investment projects. With a disinflation trend in place, the Fed has shifted its focus to the labor market. For US yields, this means the upside is more limited and the downside will be determined by growth and activity data. Risks are therefore skewed to lower yields and a steeper curve, in our view, with yields outperforming the forward curve.

The long-end may be prone to more stickiness versus the front-end as UST supply should remain heavy with risks to further coupon supply increases in H2 2025 if the deficit deteriorates further (we forecast USD1.975trn for FY2025). Additionally, ongoing QT and dealer balance sheet constraints should see higher financing costs to buy USTs as well.

Historically, the UST yield curve tends to begin steepening more sustainably within three months of the first rate cut, with the ultimate level determined by the depth of the cycle. We continue to favor 5s30s UST steepening, but if the labor market were to weaken more than we forecast in Q4, we would expect more downside to US yields and would favor shifting to 2s5s or 2s10s UST steepeners.

… AND since OIL is top of everyone’s mind, some techAmentals from one of if not THE best’us in the biz …

…WTI futures (CL1) Price posted a bearish outside day, smashing below support at 67.71 (Dec 2023 low). Techs here also look bearish, with weekly slow stochastics not showing signs of a cross higher as well. We think prices could move another 3+% lower towards 62.43-63.64 (Dec 2021 low, 2023 low). A weekly close below 67.71 would add to bearish signs.

To the other side, resistance is likely at 71.67-72.48 (August low & June low).

Here are some thoughts from one of Global Walls favorite stratEgerists who happens to work with one of if not THE largest German banks in the world … from thinkin’ bout 25bps and the DOTS TO somewhat longer-term thinking (ie MONTHLY chartbook) …

… While September Fed pricing was little changed, the total amount of rate cuts priced over the next 12 months rose to a new high of 240bps (+8.2bps on the day). From the Fed’s perspective, one trend that’s helping to remove inflationary pressures has been the sharp decline in oil prices over recent weeks. In fact, yesterday saw Brent crude oil (-3.69%) close beneath $70/bbl for the first time since December 2021. That continues a declining trend for oil recently as it was only on July 5 that Brent crude peaked at almost $88/bbl intraday, so we’ve seen a significant move in the last couple of months. The losses have been driven by a range of factors, but fears of a sharper downturn for the global economy have been significant, given the correlation between oil and broader economic demand …

…That dovish SEP shift would signal more cuts this year but there is also ample scope for the projections further out to move. As an illustration of that, today’s chart reproduces the individual June SEP projections for the fed funds rate in 2026 and the longer run. As indicated by the red box, in June, 15 FOMC participants thought it would be appropriate for the fed funds rate to be strictly above 3% at the end of 2026, but only 5 projected a longer-run rate that high. Taken together that means at least 10 participants – over half the Committee – judged it would be appropriate for the nominal policy rate to be above its longer run level more than two years from now. (Even accounting for the fact that the longer-run dots tend to fall on quarterpoint marks while the year-end dots are midpoints of the 25bp target range, leaves that proportion around 1/3.) This gap should be gone in next week’s updated projections and arguably the 2025 dots should be quite close to the longer-run ones.

We’re in the seasonally weak part of the year… Using data since 1928, we are now in a seasonally soggy patch for the S&P 500…

September has been the worst month for the S&P 500 since 1928, the only month where it’s been lower more than higher over 95 years… It’s also been lower in all of the last four years...

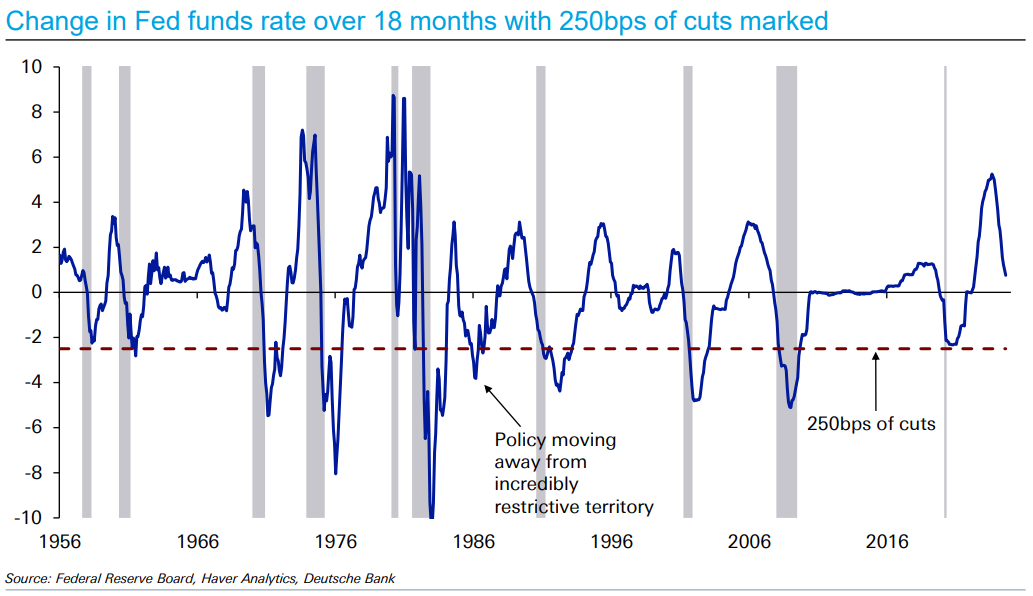

…Futures are pricing in over 250bps of cuts in the next 18 months… That would be historically rare outside a recession… Only exception was in mid1980s when policy was in super-restrictive territory under Volcker… Seems hard to imagine this happening without a recession…

The real fed funds rate is now at a post-GFC high but not at extreme levels if no recession. Clearly a recession would likely see enough cuts to approach or go below zero. Current market Fed pricing seems more recession than soft landing skewed.

And remember our long-term view that markets are a very poor predictor of rates…

…We can’t call the economic all-clear yet though, as US recessions only happen when the yield curve has steepened back up, and often only when back in positive territory. So, while moving away from an inversion is typically seen as a positive, it actually means we’re closer to reaching the moment of truth...

… and from Germany we turn TO large bank from The Netherlands …

Rates remain under downward pressure. Today's US CPI should give the Fed free rein with next week's likely rate cut. Kamala Harris, seen as the winner of last night's presidential debate, also favours rates downside, although the presidential race is still very much open

…USTs to lose from Trump presidency, impact on Bunds more ambiguous Of the two candidates, a Trump win would be most inflationary, and thus worse for USTs in our view. Tax cuts and import tariffs would add to price pressures and contribute to a higher terminal Fed rate. A clean sweep scenario, one in which Trump wins both the presidency and Congress, would allow the most drastic tax cuts. If he only manages to win the presidency, then the focus would be more on foreign policy, which would likely incite trade tensions with Europe and China, and undoubtedly lead to increased tariffs.

… from The Netherlands to Switzerland we go for a debate recap AND CPI prep …

The market consequences of the US presidential debate rested on whether it changed probabilities around the election, and whether more substantial policy insights were offered. On the former, betting markets and the media suggest US Vice President Harris “won”—although debate victory does not always translate into electoral victory. On the latter, this was a debate of social media memes more than in-depth policy analysis.

August US consumer price inflation is due. The first focus for investors is whether a moderation of consumer price inflation will change the Federal Reserve’s policy decision. The Fed is chasing inflation lower, and it is unnecessarily late to start the rate cut cycle, but there is probably not enough inflation weakness to prompt a larger rate cut.

The second focus is whether US consumer spending power is enhanced by lower inflation (as wage growth remains OK). If inflation is falling because the fictitious owners’ equivalent rent is falling, there is no boost to consumer spending power. If other prices are falling (and some goods prices are well into deflation territory), that will help spending power…

Missed NFIB yesterday but never fear …

Wells Fargo: Small Business Optimism Takes a Step Back in August A Weakening Labor Market and Economic Uncertainty Dim Outlooks

Summary Small Business Inflation Is Receding, But So Is Labor Market Health Small business owners appear to be more preoccupied with worsening labor market conditions and dimming sales outlooks than they are looking forward to incoming rate cuts. The NFIB Small Business Optimism Index dropped to 91.2 in August, completely erasing July’s gain and taking some shine out of the prior four-month upswing. As nonfarm payrolls continue to show a moderation in hiring, hiring plans trended lower and the net share of small businesses actually adding headcounts reached its lowest reading in two years. The uncertainty index also continued to climb as firms face an uncertain public policy landscape post-November. On the bright side, inflation’s descent appears intact. The share of small businesses raising selling prices in August reached its lowest level since January 2021.

Finally from Dr. BOND VIGILANTE Yardeni … apparently China is the sole reason we’re celebrating lower prices at the pump (?) …

Yardeni: China Is The Source Of The Deflation Trade

Forget about a recession in the US. Currently, it is China's recession/depression that is weighing on oil prices, global bond yields, and the dollar. Weak Chinese demand for oil caused OPEC today to trim the outlook for global oil demand, further depressing oil prices. Brent crude oil prices fell below $70 a barrel on Tuesday to their cheapest since December 2021 (chart).

Declining oil prices dragged the 10-year Treasury yield down to 3.65%, lows not seen since early 2023 when markets fretted that the mini-regional banking crisis would spark a recession (chart).

… And from Global Wall Street inbox TO the WWW,

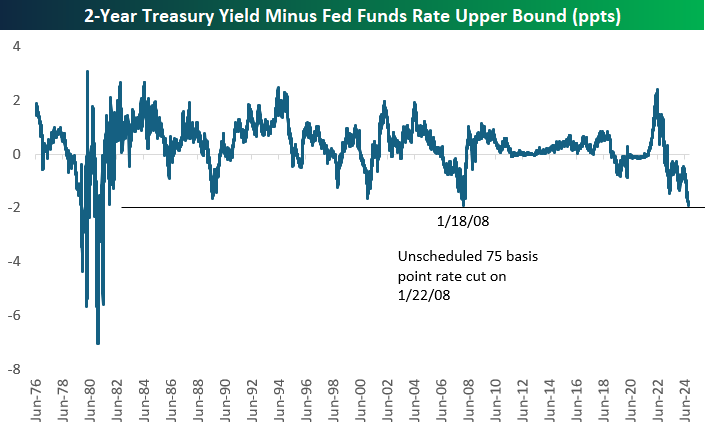

Bespoke group with a keeper of a chart — one that continues to pop up time to time — FF and 2s …

BESPOKE: Utes on Top; $10k in USO; Paul on CNBC; Fed Funds Yield Curve

…The 2-year Treasury yield is currently trading below 3.6%. At the same time, the Fed Funds Rate still sits at 5.25%-5.50%. As shown in the chart below, 1/18/08 was the last time the spread between the 2-year Treasury yield and the upper bound of the Fed Funds Rate got this inverted. Four days later on 1/22/08, the Fed held an emergency meeting to cut rates by 75 basis points, and eight days after that on 1/30/08, the Fed cut another 50 basis points.

Given how lopsided this spread is, how likely do you think it is that the Fed cuts by 50 basis points rather than 25 basis points at its next scheduled meeting later this month?

Bolingbroke from Bloomberg SPEAKS and we should listen / read as we know positions matter …

Bloomberg: Traders Still See at Least Two Jumbo Fed Cuts Coming Soon

(Bloomberg) -- Traders in the US interest-rate options market are still betting on at least one super-sized Federal Reserve interest-rate cut this year — just probably not before the Nov. 5 US election.

Ahead of next week’s central bank policy gathering, Fed swaps reflect expectations for a quarter-point cut, with only a scant possibility for something bigger. Looking out further, it’s a different story.

Recent activity in options linked to the Secured Overnight Financing rate shows that traders are increasingly positioning themselves for roughly 150 basis points of cuts by the central bank’s Jan. 29 policy decision. That’s the same as is currently priced in in by the swaps market.

To implement that amount of easing, officials would, in the absence of an intermeeting move, have to implement cuts of at least half a point at two of the four scheduled gatherings through January — moves that are bigger than the standard quarter point…

… and never heard the 60/40 question phrased quite like this but okie dokie …

LPL: Is the Stock-Bond Diversification “Free Lunch” Back on the Table?

Conclusion While it’s still early in this trend, LPL Research welcomes a shift to a regime of negative stock-bond correlation as it allows multi-asset investors to take more advantage of the “free lunch” of diversification. We continue to consider core fixed income as an attractive asset class, and an integral part of most multi-asset portfolios. Within core fixed income, we maintain a preference for up-in-quality credit exposure and a neutral interest rate sensitivity (duration) relative to benchmark indexes, while monitoring signs of a potential stock market correction. We continue to hold a strong overweight to preferred securities as valuations remain attractive. LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) anticipates heightened levels of volatility as multiple signals come to bear on the economy, elections, and the seasonality backdrop.

AND from Twitter …

at HostileCharts

$TLT - Such a clean risk/reward long against $100.

A rolling 6-month % change between the long duration Treasury index and S&P 500 is a helpful tell on how serious underlying economic issues are. Surges from this ratio into the top decile are typically accompanied by 1) equity corrections and often 2) recessions. No evidence yet.

I heard it retold today, the story of JPM ordering ALL of their staff out of WTC after the 1st plane struck, despite the NY port authority saying Remain Calm, all is Well. Reminds me of people in Hawaii a yr ago, those who didn't do as they were told and Stay Put....well they ended up living! TRUSTING the Government, especially in a crisis, is about the last thing we should do, IMHO.

In Memorial: NEVER FORGET !!!!!!!

I heard it retold today, the story of JPM ordering ALL of their staff out of WTC after the 1st plane struck, despite the NY port authority saying Remain Calm, all is Well. Reminds me of people in Hawaii a yr ago, those who didn't do as they were told and Stay Put....well they ended up living! TRUSTING the Government, especially in a crisis, is about the last thing we should do, IMHO.