Good morning … Surely you’ve got something better to do / read / watch / listen to ahead of this mornings all important NFP which will then be chased down by Williams and Waller commentary snuck in AFTER NFP and just ahead of the pre FOMC blackout period.

And certainly, by now you’ve seen / heard plenty ‘bout the un-inverting and been told whether or not to cheer AND what it all ultimately means. There are some more thoughts from Global Wall below and here’s an excerpt

DB: … we're not out of the woods yet, as recessions start when curves are re-steepening and not close to their maximum inversion point. Indeed the last 4 recessions only began once the curve was positive again …

… again more context below as this one continues to play out and there are no right / wrong answers, lets quickly review yesterday’s ADP and ISM…

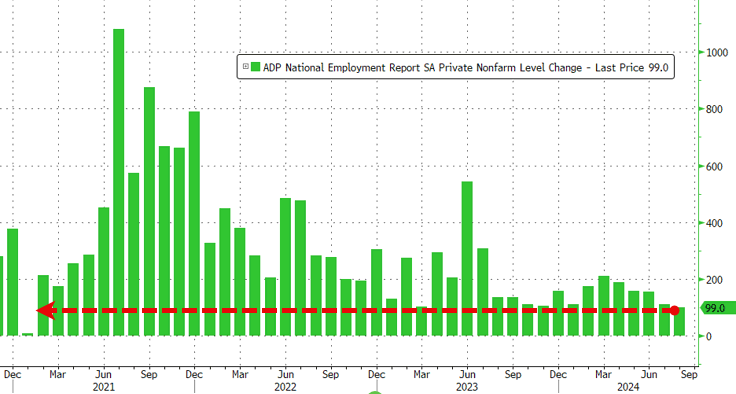

ZH: ADP Employment Report Weakest Since Jan 2021 ZH: Jobless Claims Data Refuses To Accept 'Hard Landing' Scenario... ZH: US Services Surveys Confirm "Baffle 'Em With Bull$hit" Season Is Back...

… and this all added up TO

ZH: Stocks Fade Ahead Of Payrolls As Bonds, Oil Convinced Hard-Landing Is Inevitable

… Yet even though bond-proxies like utilities and staples underperformed today, Treasury yields sank for the 3rd consecutive day, sliding 2bps to 3.73%, and except for the freak Aug 5 plunge (from which they quickly recovered), yields are now back to 2024 lows...

... as the mounting hard-landing panic, which today was boosted by the worst ADP private payrolls report since Jan 2021...

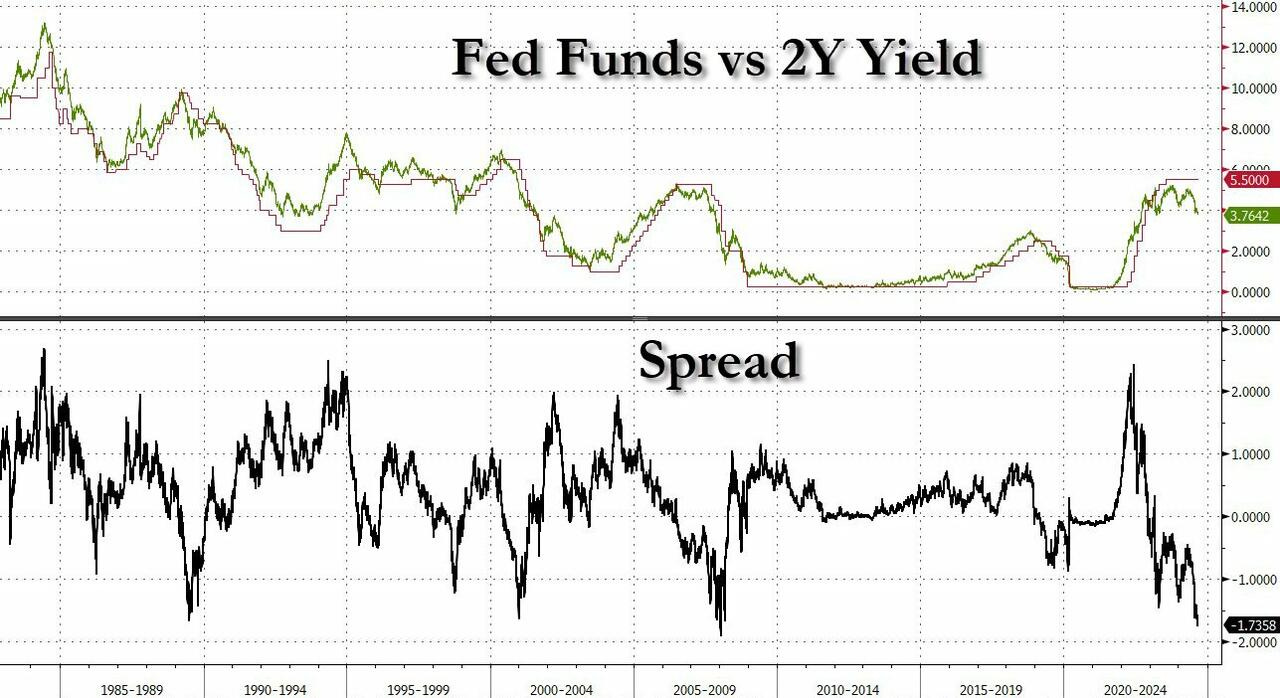

... hints at a bond market that has almost never been more convinced of a very unhappy ending (with just one exception --- spot it in the chart below).

… not ALL is unhappy or lost (think EARL?, gas prices?) but this is classic risk off few days where bond catching F2Q flows ahead of the data and will try to have more recap and victory lap over weekend but for now … here is a snapshot OF USTs as of 655a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities are lower, JPY gains & DXY holds flat ahead of US NFP … Bonds are bid, USTs less-so as attention remains firmly on US unemployment data … USTs are bid but not to quite the same extent as European peers after the pronounced two-way action seen on Thursday’s data points and as participants await today’s NFP report. USTs are holding around 115-00+ which marks the December contract high and is just three ticks shy of the September contract peak from early August.

Opening Bell Daily: Job weakness (Exclusive) … LinkedIn shared proprietary insights that point to an even softer economic outlook than official data suggests.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ in these final few hours / moments before NFP (recaps and victory laps to come over the weekend) …

Argus: Daily Spotlight (05 Sep … stocks vs bonds — a coin flip)

Stocks Back to Fair Value on Model Our stock/bond asset-allocation model, which we call the Stock Bond Barometer, is indicating that stocks are the asset class currently offering the most value. Our model takes into account levels and forecasts of short- and long-term government and corporate fixed-income yields, inflation, stock prices, GDP, and corporate earnings, among other factors. The output is expressed in terms of standard deviations to the mean, or sigma. The mean reading going back to 1960 is a modest premium for stocks, of 0.16 sigma, with a standard deviation of 0.97. In other words, stocks normally sell for a slight premium valuation. But the current valuation level now is a 0.7 sigma discount for stocks, reflecting in large part the sharp move lower in long-term interest rates since the Fed's summit in Wyoming. Other valuation measures also show reasonable multiples for stocks. The current forward P/E ratio for the S&P 500 is approximately 20, within the normal range of 13-24. The current S&P 500 dividend yield of 1.2% is below the historical average of 2.9%, but is also 32% of the 10-year Treasury bond yield, compared to the long-run average of 39% and the all-time low of 18%. Further, the gap between the S&P 500 earnings yield and the benchmark 10-year government bond yield is about 360 basis points, compared to the historical average of 400. Lastly, the ratio of the S&P 500 price to an ounce of gold is now 2.2, within the historical range of 1-3. We expect the results from our stock-bond valuation model to tilt more toward stocks, as interest rates head lower and EPS growth picks up. Based in part on the output from our barometer, our current recommended asset allocation model for growth accounts is 70% growth assets and 30% fixed income.

BAML US Rates Viewpoint (04 Sep and kindly note a robust SEASONAL discussion of rates in the bullish technicals section as well as the section on ‘bonds vs commods — bottomed and turnin’ up’ and so, favoring being LONG BONDS relative to commods) Back to school cheat sheet: buy dips

After the summer holiday, we refresh our rate views. Our core rate views remain in-line with our mid-year update: keep buying dips, stay short spreads, vol surface steepener, & higher funding in 2H24 but stabilization / partial reversal in 1H25. We have also made several adjustments since our mid-year: we revised our rate forecasts lower, embraced our long held 5s30s nominal steeper, & now initiate a forward inflation steepener.

Macro: strong but slowing Keep buying rate dips. Investors should consider exposure to duration at around 4% & 4.25%. We believe investors should be aiming to lighten up on duration exposure close to 3.5% unless big data softening…

…Technicals: bullish UST trends remain underway US 10y yield in a short-term consolidation phase. Consider buying the dip at around 4% and 4.25%. Ideally yield does not exceed 4.15%. US 10y yield in a soft-landing targets 3.50-3.22%, in a hard-landing targets below 3% such as 2.73% and could extend lower. Bonds / Commodities bottomed = buy UST dips & sell commodity rips. Risks: US election year and ten-year seasonal trends support yield which may lead to daily chart bottoms.

The ISM services PMI was roughly unchanged at 51.5 in August, consistent with a solid, but slowed, pace of expansion. The reading reflected mixed changes across major components. Although the employment component softened from July, it remains in the expansionary range following a series of sub-50 prints earlier this year…

…The slight improvement in the ISM services PMI reflected mixed changes across major components, which generally remained in expansionary territory….

…Although the ISM services component softened from July, it indicates firming compared to earlier this year. The employment component fell slightly to 50.2 (-0.9pts) in August, remaining above 50 for a second straight month after registering a string of sub-50 prints since February. Given these, patterns we find it difficult to infer much signal about tomorrow's nonfarm payroll employment number. The business activity component printed at 53.3, down 1.2pts but remaining in expansionary territory, and the new orders component again showed expansion at 53.0 (+0.6pts)…

BARCAP US Labor Market: Upward QCEW revisions likely foreshadow a smaller benchmark revision

The BLS this week revised up its prior estimates of payroll jobs from the Quarterly Census of Employment and Wages through Q4 2023. Working from systematic revision patterns, we think the upcoming benchmark revision will likely be a downward revision of about 568k, a fair bit less than the preliminary estimate of -818k.

… Today's revisions, which were not available at the time of the preliminary benchmark estimate, marked up the prior vintage of QCEW employment estimates throughout 2023. To date, initial QCEW employment estimates have been boosted by 287k in September 2023, and by 166k in December 2023, continuing a systematic pattern of upward revisions since the pandemic (Figure 1). On average, initial quarterly employment estimates have been boosted by about 215k since Q3 2020, with initial March estimates through 2023 having been boosted by about 140k…

…Based on today's revisions, we think the initial QCEW estimate of the level of employment in March 2024 will be marked up by about 250k. This would correspond to a downward benchmark revision of about 568k, or nearly 50k/m. Risks likely skew to an even smaller benchmark revision, given the unusually low initial QCEW response rate for Q1 2024 (Figure 2).

BARCAP: US CPI Inflation Preview (August 2024 CPI): Core CPI to round to 0.2%, again

We expect core CPI inflation edged up by 2bp to 0.19% m/m (3.2% y/y) in August amid slightly less deflation on the core goods side, while core services inflation is anticipated to have held steady. We expect headline CPI increased 0.14% m/m SA (2.5% y/y) and the NSA index to print at 314.803.

BMO: ADP just 99k, Jobless Claims 227k, ULC revised to 0.4%

August's ADP print disappointed at 99k vs. 145k anticipated, for the lowest since January 2021. July was revised lower to 111k vs. 122k initial…Overall, it was a mix of data that has reinforced the recent bull steepening price action…

BMO: ISM Services Inches Higher, Prices Paid/Orders Improve

We expect idiosyncratic factors to drive an above-consensus 0.3% m/m gain in US core CPI in August.

The underlying trend still looks favorable to us, with rent of primary residence likely falling below 5% y/y for the first time since April 2022.

Our CPI forecast translates to a preliminary August core PCE estimate of 0.22% m/m, which should keep the Fed on track to conclude that inflation is headed back to its 2% target sustainably at the September FOMC meeting.

Regular readers will know that I’m a big fan of the predictive power of the yield curve in terms of forecasting the US cycle. However it’s fair to say that its predictive power in this cycle looks to have malfunctioned. 2s10s has been inverted for 26 months continuously, which is the longest ever, and there still hasn't been a recession.

So with the 2s10s poking its head into positive territory over the last 24 hours, it’s tempting to suggest we can sound the all-clear.

But today's CoTD shows we're not out of the woods yet, as recessions start when curves are re-steepening and not close to their maximum inversion point. Indeed the last 4 recessions only began once the curve was positive again. Henry's piece from last year (link here) looks at those examples of how the curve steepened into positive territory before the recession…

Of course, a perfect soft landing would also bring a steeper curve, as the Fed will be able to cut and lower yields at the front-end. So whichever way you lean, a positive sloping curve (if we continue to move in that direction) likely brings forward the moment of truth as to whether the yield curve has completely failed as a leading indicator in this cycle, or whether its powers were just felt later than in other cycles through history.

ING Rates Spark: If payrolls come in line with consensus, then forget the 50bp cut narrative

It's Friday payrolls day, arguably the biggest number of the month. Strangely there is a reasonable 165k consensus forecast. Hit the consensus and we think rates pop. We suspect the market is actually positioned for a sub-100k number. If we don't get that type of validation for material slowdown, yields will be under pressure to rise for a bit

We expect core CPI inflation at 0.20%M in August (0.2%M cons, 3.2%Y). Our forecast is aligned with a core PCE print of 0.17%M. Housing inflation comes softer, goods prices fall but not as fast as in July. We expect headline CPI at 0.17%M (2.6%Y, NSA Index: 314.851).

Just one month ago, markets were panicked by the release of an unreliable labor market signal, distorted by seasonal peculiarities. Now, once again, it is time for the US employment report. The unreliability adds unpredictability to the numbers, but the expectation is for a lower unemployment rate as temporarily unemployed auto-sector workers return to work.

Two things matter about the US labor market, and neither appears in today’s data. Middle-income consumers’ fear of unemployment dictates their consumption patterns. Fear of unemployment should be low (firms may slow hiring, but they are not accelerating firing). The data will be spun by both parties, but most US voters do not know what the last payrolls figure was—labor market perceptions, not reported data, were what matter politically.

In a well-run central bank a, single employment statistic would not change policy. Under Federal Reserve Chair Powell’s “data dependency” mantra, the tone of this report could influence the size of the September rate cut. New York Fed President Williams speaks after the data…

Wells Fargo: Despite Broader Growth Concerns, Service Sector Improves

The services ISM notched a modest gain in August, quelling for now concerns about stalling growth. While the prices paid measure rose, the employment measure indicates a jobs market that is in a decidedly lower gear than it was as recently as earlier this year.

Wells Fargo: August CPI Preview: The Possible Tiebreaker Between a 25 or 50 Bps Cut?

Summary Consumer price inflation likely picked up in August in a reminder that the road to restoring price stability will still have some bumps along the way. We estimate the core index rose 0.25%, which would still be less than the average increase in Q1 that set back the clock on expectations for Fed easing and would keep the year-over-year rate of the core unchanged at 3.2%. Headline inflation for August will likely offer further evidence that through the month-to-month moves, inflation's progress is not going into reverse. We look for a 0.2% increase in headline CPI that would bring the year-over-year rate to 2.6%—the smallest increase since the pandemic's one-year anniversary in March 2021.

A rate reduction at the FOMC's upcoming meeting on September 18 looks all but certain, but the upcoming CPI report could serve as a tiebreaker between a 25 or 50 bps cut if the August jobs report lands in the gray zone between clearly weak and clearly strong. A 0.3% (or larger) increase in the core CPI could make some of the more hawkish members hesitant to begin cutting at all, making a 25 bps rate reduction the compromise outcome. In contrast, another unexpectedly-low print (below 0.2%) could make enough officials comfortable with a 50 bps cut—not because the labor market is falling apart, but because the significant progress on the price-stability side of its mandate no longer requires such a restrictive stance of policy.

… And from Global Wall Street inbox TO the WWW,

AAA: A Sixth Sense About Six Cents? I See Dea… I Mean Falling Gas Prices

… “There are now ten states with gasoline averages below $3 a gallon, which means thousands of retail outlets east of the Rockies are selling gas at similarly low prices,” said Andrew Gross, AAA spokesperson. “With hurricane season remaining weak and disorganized, this trend of falling pump prices will likely continue.” …

… According to new data from the Energy Information Administration (EIA), gas demand fell last week from 9.30 million b/d to 8.93. Meanwhile, total domestic gasoline stocks rose slightly from 218.4 to 219.2 million barrels, and gasoline production increased last week, averaging 9.7 million daily. Falling gasoline demand and oil costs will likely keep pump prices sliding.

Today’s national average for a gallon of gas is $3.30, 17 cents less than a month ago and 51 cents less than a year ago.

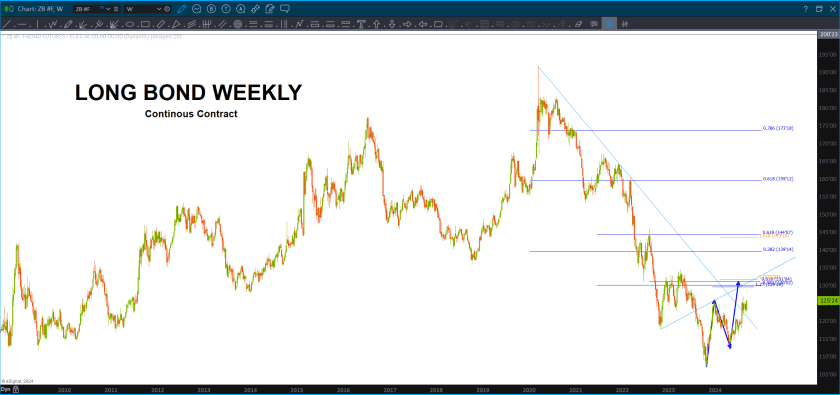

Barts Charts: Bond Complex – September 5, 2024 (from one who was SHORT…)

at EvanMedeiros

it took all year to come together but the long bond trade $TLT is shaping up nicely as it prepares to challenge those December 2023 highs.

Today’s Chart of the Day was shared by Evan Medeiros (@evanmediros).

Bonds continue to shape up for a potential breakout. The +20-year Treasury Bond ETF ($TLT) closed at its highest level of the year and is within striking distance of a 52-week high.

$TLT is trying to recover from its longest and deepest drawdown on record. After building a nine-month base, it's testing resistance from the December highs at $100.

Bonds are also exhibiting relative strength versus stocks. $TLT is up +9.5% in the second half of the year, while $SPY is up less than +1%. In addition, $TLT is closer to a new 52-week high than $SPY.

Takeaway: Bonds are outperforming stocks and shaping up for a potential breakout. $TLT is still dealing with its longest and deepest drawdown on record, but it's trying to emerge from a nine-month base.

… The FRED graph above shows the employment-to-population ratios for native-born (blue lines) and foreign-born (red lines) men and women (solid and dashed lines, respectively). The employment-to-population ratio is reported by the US Bureau of Labor Statistics (BLS); as the name suggests, it represents the fraction of each population group that’s employed…

Kimble: Copper Facing Historic Price Decline If Support Fails! (Dr Copper speaking…?)

Nautilus Research: Yet Another Threshold Breached in U.S. 2-year Yields New 2-year (504 trading day) Low in U.S. 2-year Yields

U.S. 2-year Treasury yields reached a new 2-year low yesterday, potentially confirming a shift in the broader interest rate landscape. Historically, when 2-year yields have fallen to similar multi-year lows, it has often preceded sustained downward pressure across the entire Treasury yield curve. The table below highlights several past occurrences of this signal, revealing a consistent pattern of subsequent yield declines in both short- and long-duration Treasuries.

… #GotBONDS? Will NFP change yer mind and / or support whatever is your position? More over the weekend but for now … THAT is all for now. I’m off to the day job…

Feel traitorous feeling or saying this, but lower gas prices only add wind to the sails of the JOYous candidate. Who's JOY, the CIA, FBI, BIS, IMF, WHO, CBDCs, I wonders....highly doubt it'll be yours or mines :(

Feel traitorous feeling or saying this, but lower gas prices only add wind to the sails of the JOYous candidate. Who's JOY, the CIA, FBI, BIS, IMF, WHO, CBDCs, I wonders....highly doubt it'll be yours or mines :(