$Got5s? IF you happen to be lucky enough to have rented some north of 4.30%, might be time to put some hay in the barn … begin romancing the idea of a short but that’s just me, thinkin’ outloud …

Said another way:

Moving on to some — not all — of what was driving markets (lets be honest, as some will show below, BONDS still being led around by EARL while other assets, notSOmuch) … Data? Sure … see it however you wann see it …

ZH: "Firing On All Cylinders, But..." US Manufacturing Surveys Send Mixed Signals In May

…The headline PMI has hit a four-year high, with strong factory production growth for a second successive month in response to a further marked upturn in order books, but since the outbreak of war in the Middle East we have seen production and demand buoyed by stock building as companies worry over rising prices and supply difficulties.

This stockpiling was again widely evident in May and makes it hard to take an accurate reading on the underlying health of the manufacturing economy, as growth will cool once this stock build has run its course,” Williamson noted.

“The incidence of supply chain delays is the highest since August 2022, with the buying of safety stocks not only adding to the supply squeeze from the closure of the Strait of Hormuz but also pushing prices higher for a wide variety of inputs.

Williamson ends on a more ominous - stagflationary - notes: warning that the resulting steep jump in producer costs sends a worrying signal that broader economy inflation has further to rise in the coming months.

WolfST: As Prices Spike, Manufacturing Expands at Fastest Rate in 4 Years, Orders Surge, Supplier Deliveries Slow — Amid improved automation and efficiencies, production rises, but employment doesn’t, or only a little…

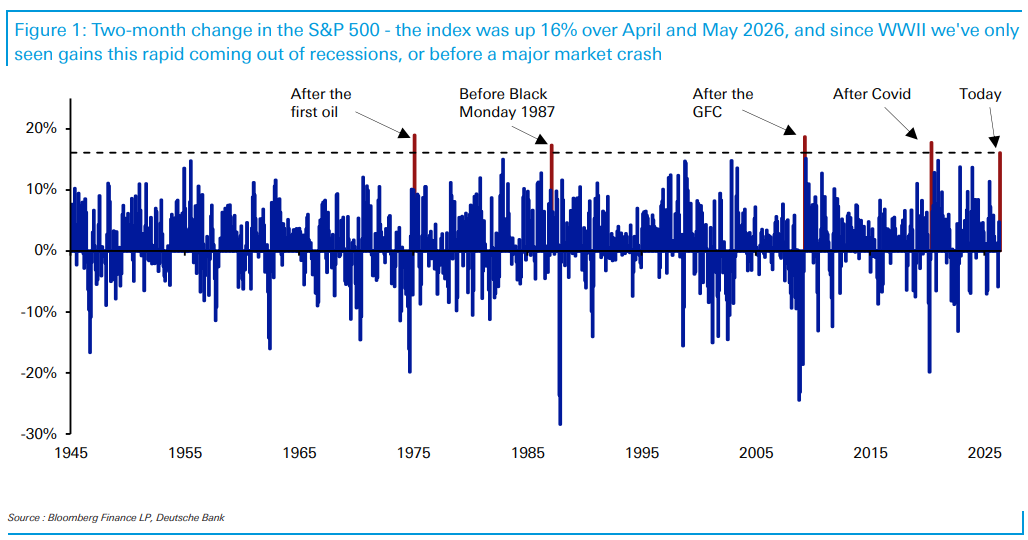

… however you wanna see it, well, go right ahead. Let me know what next. For more funTERtaining questions like this, kindly see note from a large German bank below highlighting a visual of the S&P over past couple months …

…the S&P 500 up +16% in two months. But since WWII, the S&P 500 has only seen a two-month gain that fast coming out of a recession (like the GFC and Covid-19) or before a major crash like Black Monday 1987…

… they continue along noting 10s been WITH EARL while most all else having decoupled … hmmm. The more you know!

Bond Market Theater: The AI Party Upstairs, the Bond Vigilantes in the Basement

Wall Street is once again trying to dance on two floors at the same time. Upstairs, equities are celebrating every AI headline like it's 1999 with better GPUs. Downstairs, the Treasury market is staring at 4.5% 10-years and muttering that maybe inflation didn't actually die—it just changed disguises. Oil remains the loaded gun on the table as Iran headlines whip yields around like a Labrador chasing tennis balls, while traders continue pricing a Fed that's supposedly "almost ready" to ease despite growth refusing to roll over. The curve keeps sending mixed signals, positioning is crowded, and consensus still believes central banks can thread the needle without breaking anything. That's adorable. Stocks are treating higher yields like a mild inconvenience; bonds are treating them like a crime scene. Eventually one market is wrong. My money is on the one trading cash flows, not dreams.

Punchline:The stock market is ordering champagne while the bond market keeps checking the fire exits. 🍾🔥

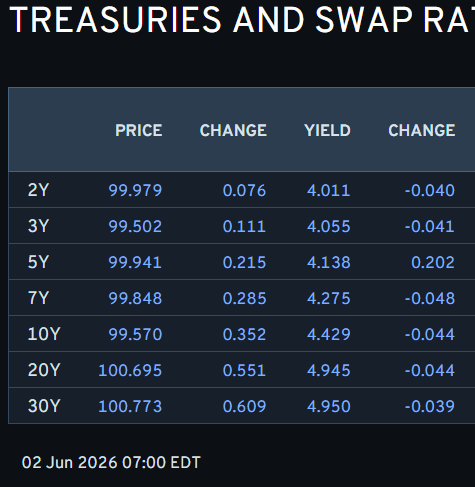

Onwards and upwards TO the reason many / most of you are likely here … whatever it may be on Global Wall’s mind but first … here is a snapshot OF USTs as of 700a:

… for somewhat MORE of the news you might be able to use … a few curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Equities broadly supported following constructive US-Iran comments … Global benchmarks benefit from lower energy prices, JGBs outperform following a solid 10yr auction … As for price action, USTs benefit from the lower energy prices this morning, with gains of c. 8 ticks at pixel time; currently holds at the upper end of a 109-22 to 109-30 range (vs Monday’s trough of 109-09+). From a yield perspective, rates at the belly of the curve are underperforming vs short-dated rates, signalling that traders remain uncertain about near-term geopolitical progress. The 10yr (4.43%) now resides back towards recent troughs, and another leg lower could see a test of the low from 12 May at 4.41%. Focus ahead turns to US JOLTS.

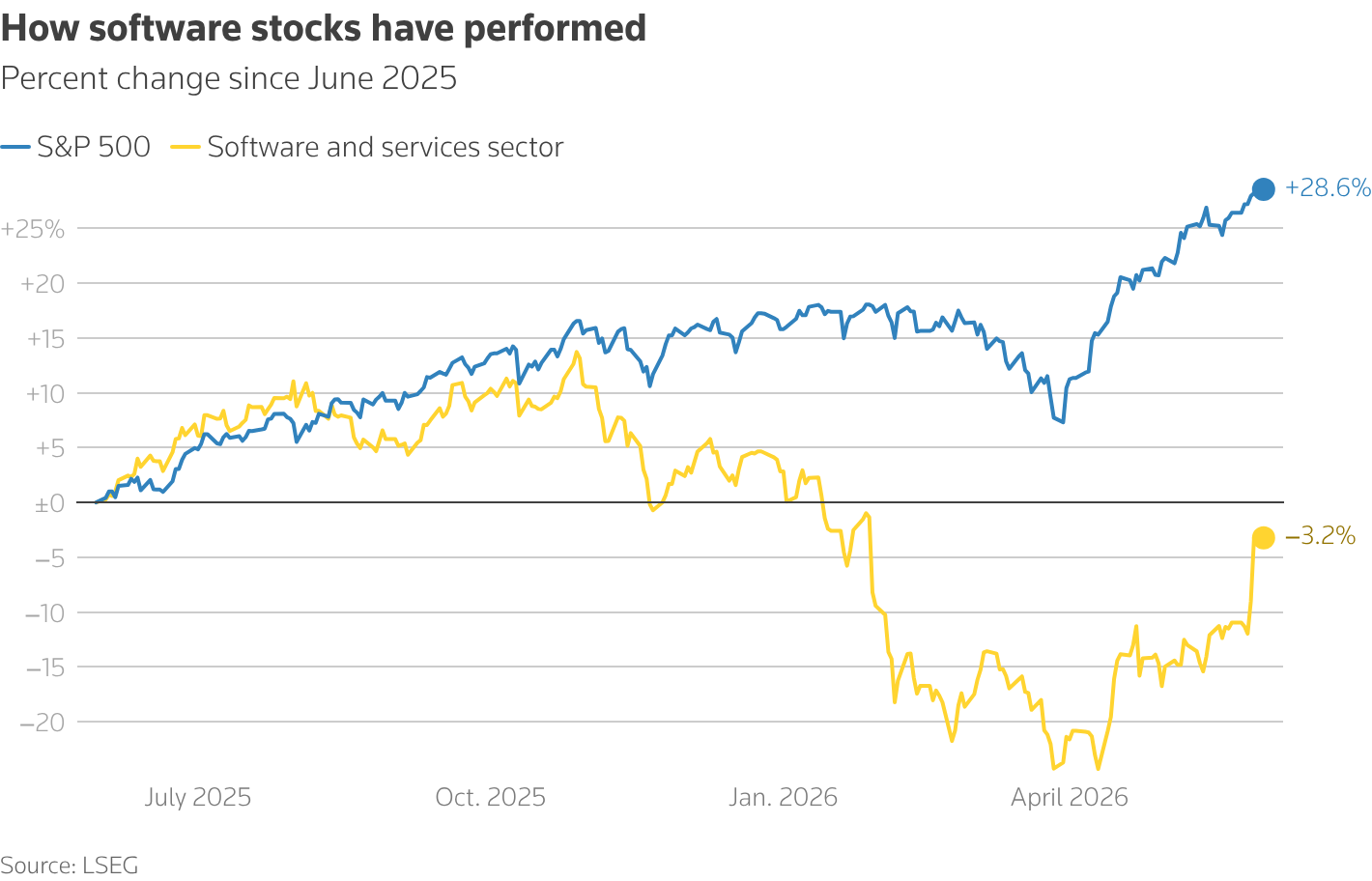

The S&P 500 software sector index logged its strongest monthly gain since October 2002 in May and ended last week at its highest level since late January after strong results from Dell and Snowflake.

After a jarring slide earlier in the year on concerns that AI agents could threaten traditional business models, the sector has almost recouped all 2026 losses to date. Stocks such as ServiceNow, IBM, Adobe, Salesforce and Workday all continued that rally this week, and the index climbed another 4% on Monday.

Yield Hunting Daily Note | Nov 18, 2025 | Selloff Continues, BDCs? , FMY/TSI Buys For Safety, PIMCOs Cheap!

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS of Global Wall you might be able to use …

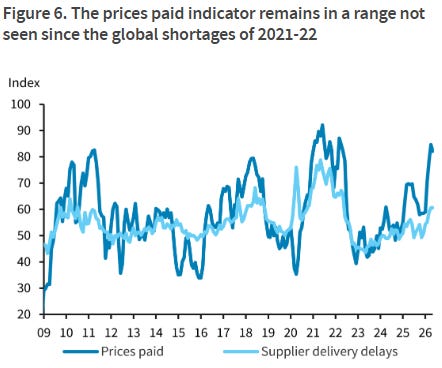

May's headline ISM strengthened again amid elevated domestic goods demand from the AI capex boom. At the same time, cost pressures remain intense, with the prices paid reading remaining at levels resembling those during the widespread shortages of the post-pandemic period.

…10-year yields briefly topped 4.50% on Monday as a function of renewed US-Iran peace deal concerns and strongerthan-expected ISM Manufacturing data. The initial downtrade was triggered by reports that Iran suspended negotiations with the US in protest of Israel’s escalation in Lebanon. Hours after the suspension was announced, the selloff was partially retraced as President Trump expressed optimism about diplomacy in a pair of posts on social media. Despite Trump’s insistence that Israel and Hezbollah have agreed to dial back fighting, WTI crude oil was up nearly $5/bbl on the day and yields were modestly higher. Nonetheless, 10-year rates remain near the bottom of the local range, and we maintain that there is more room for Treasuries to cheapen if the US and Iran fail to reach a peace deal than there is scope for the market to richen if an agreement is reached. We’d look to reset tactical short positions in the event that today’s opening gap from 4.443% to 4.436% is backfilled…

Dislocations are opportunities …

02 June 2026 DB: What are the biggest market dislocations? June 2026

In another of our “dislocations” series, we got thinking about what looks strange in markets, and what might therefore be ripe for a correction.

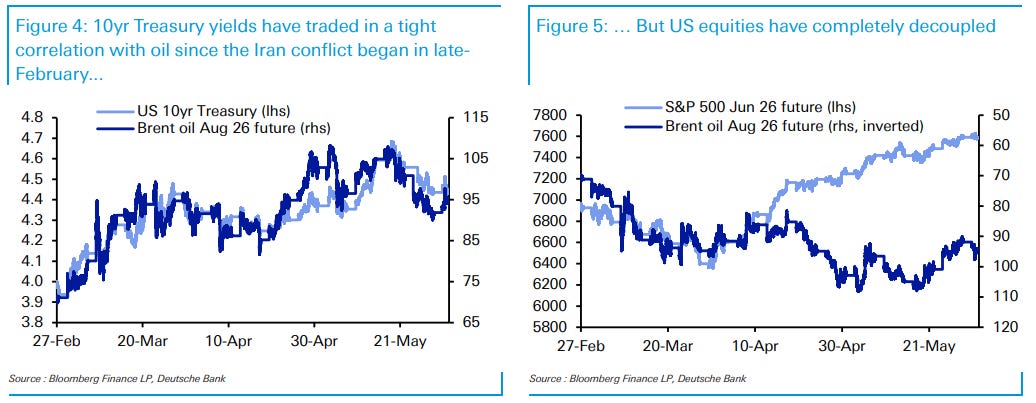

This month, it feels like the tail risks around the distribution are unusually large. Equity and credit markets have been remarkably resilient against geopolitical shocks, yet sovereign bonds like 10yr Treasuries are still trading in a tight correlation with oil prices. Interestingly though, with investors still confident that a US-Iran deal will be reached, the oil futures curve has remained relatively steady over the last couple of months, even as the Strait of Hormuz has stayed closed longer than many expected.

We noted a few points:

Global equities have seen remarkable strength, with the S&P 500 up +16% in two months. But since WWII, the S&P 500 has only seen a two-month gain that fast coming out of a recession (like the GFC and Covid-19) or before a major crash like Black Monday 1987.

Along similar lines, credit spreads also remain historically tight, even as warning signs on the consumer are building.

Nevertheless, this resilience to geopolitical risk in equity and credit markets still isn’t reflected among sovereign bonds. 10yr Treasury yields have continued to trade almost entirely in line with oil prices over the last month, even as other assets have decoupled.

Despite the Strait of Hormuz staying closed longer than initially anticipated, the oil futures curve has been remarkably contained in the last two months.

…Conclusion …Yet strikingly, sovereign bonds aren’t following this pattern of resilience seen in equities and credit. In fact, the 10yr Treasury yield has traded in a tight correlation with oil prices. So markets are still showing some vulnerability against geopolitical risk.

Nevertheless, one factor driving this wider resilience is that oil markets haven’t seen a bigger reaction against the Strait of Hormuz’s closure. So even though it’s remained closed much longer than many expected, longer-dated oil futures have remained broadly stable over the last couple of months. The fact that we haven’t seen a sharper upward move in the futures curve has meant investors aren’t pricing in severe stagflation, preventing a bigger downturn in risk assets. Whether that can hold if the Strait of Hormuz remains closed is questionable, but for the time being, market expectations of lower oil prices in the future are themselves acting as an important pillar of support.

…In the outlook, our baseline expectation is that a US-Iran deal is reached this month that allows shipping through the Strait of Hormuz to resume, with Brent crude falling back to $86/bbl in Q4. However, if the Strait of Hormuz experiences a prolonged closure, that would push Brent towards $150/bbl, hitting global growth and pushing Europe into recession. But net net, our global GDP forecast has only been trimmed slightly to 3.0% this year, before recovering back to 3.2% in 2027.

For markets, our equity strategists remain constructive, still seeing the S&P 500 at 8000 by year-end. However, our fixed-income strategists expect a further selloff, with 10yr Treasury yields reaching 4.7%, and 10yr bund yields up to 3.2%. In credit, we also see some mild spread widening by year-end, particularly in Europe. And on the FX side, we expect a continued (albeit slower) dollar depreciation, with EUR/USD reaching 1.20 by year-end…

…This backdrop of rising oil prices yesterday led investors to price back in the chance of a stagflationary shock. So yields moved higher, with the 10yr Treasury yield (+1.7bps) reversing a run of 7 consecutive declines to close at 4.45%, though it did retreat from an intra-day high of 4.516% …

What IF SoH opens … all fixed?

June 1, 2026 MS Cross-Asset Brief: If the Strait reopens, how quickly can Middle East production return?

1) Will oil and demand-side pressures derail the disinflation path? Tariff wear-off makes it unlikely

2) If the Strait reopens, how quickly can Middle East production return? 75% recovery over 4 months

3) Can the USD still weaken if the energy shock persists? Yes

4) Are higher bond yields a headwind for equity valuations? Not necessarily

5) Why do we expect a broadening in US equities? The fundamental backdrop is improving for cyclicals

Exhibit 1: Even if the oil market remains tight for longer, keeping rates higher, equity valuations may not be impacted as much as investors think

…Exhibit 8: … but elevated bond volatility, particularly over the medium-term, has greater repricing implications

US-Iran talks falter; oil jumps on Hormuz concerns; ISM manufacturing hits four-year high; AI supports equities; bunds and gilts bear-flatten; DXY at 99.17 (+0.2%); US 10y at 4.45 (+1.8bp)…

…US rates sold off in a front-end-led bear-flattening move as oil prices rose and manufacturing data surprised to the upside (2y: +2.9bp; 10y: +1.8bp; 30y: -0.2bp). Treasuries cheapened after reports that Iran halted indirect message exchanges with the US, raising concern around energy supply and inflation. The sell-off extended after ISM manufacturing rose to 54.0, the strongest reading since May 2022, while prices paid remained elevated despite easing from the prior month. Construction spending also beat expectations, reinforcing the view that growth momentum remained resilient. Yields later pared highs after President Trump said talks with Iran were continuing at a “rapid pace” and that Israel and Hezbollah had agreed to stop fighting…

Talk of a regime shift is sweeping through the world’s most powerful central bank. Yet newly appointed Fed Chair Kevin Warsh would be forgiven for thinking his timing is less than perfect. Inflation remains stubbornly elevated: April’s consumer prices (CPI) hit 3.8% year-over-year, while producer prices (PPI) jumped to 6.0%.

This inflationary resurgence is fuelled by conflict in the Middle East, and whilst markets remain optimistic that a peaceful resolution will be found, there is no such consensus on the macroeconomic outlook. Is this spike merely cyclical - a temporary bump to be looked through - or is it something structurally insidious that demands an immediate, hawkish response?

No wonder investors are anxiously awaiting the new Chair’s first comprehensive public speech following the 17 June Federal Open Market Committee (FOMC).

This press conference is Chair Warsh’s official platform to lay out his vision, a moment made critical by the inclusion of the quarterly Summary of Economic Projections (SEP). Above all, markets are hunting for clues on how his chairmanship will evolve, specifically regarding two pillars:

A new philosophy on the balance sheet

A commitment to communication restraint…

…What Does It Mean for Markets?

We enter the Warsh era with record highs for the stock markets, tight credit spreads, more normal interest rates, and heightened geopolitical uncertainty. Central bank balance sheets move at a glacial pace; do not expect a dramatic U-turn, but rather incremental, structural shifts. High-grade spread markets might face pressure if the Fed’s asset composition shifts too rapidly away from MBS in favour of Treasuries, particularly against a backdrop where US government bonds are already yielding more than swaps.

Similarly, transitioning from an ample-reserves framework back to a scarce-reserves system will be a high-wire act. Any missteps will quickly show up as volatility in funding market spreads. Strapped with massive fiscal deficits and elevated inflation, bond markets are in no mood for erratic policy experiments.

The most compelling drama will be how Chair Warsh delivers the rate cuts President Trump expects while simultaneously tightening the screws on liquidity. His desire for less market communication may have to wait. Given that this inflation shock originated externally, predicting its expiration date is anyone’s guess.

Balancing quantitative tightening via the balance sheet with easing through the policy rate is the ultimate monetary tightrope. Good luck, Mr. Warsh!

Another day, another round of Gulf war stories—the latest originated from semi-official Iranian sources, so markets took them more seriously. Iran’s apparent suspension of negotiations with the US prompted US President Trump to attempt a ceasefire between Israel and Hezbollah. Market opinions differ as to the terms and effectiveness of this.

Rising oil prices hurt US farmers, directly (tractors use a lot of fuel) and indirectly (via things like fertilizer costs). Trump countered the rising costs from war policy by lowering costs from trade war policy, cutting agricultural equipment tariffs. Farmers planning near-term investment spending benefit by paying lower tariffs—farmers who are just growing crops face higher input costs without relief…

…US job openings “data” is due. If this were accurate it would be really helpful, but the survey response rate is very low. Policy uncertainty seems to have paralyzed decision making by US chief executives, leading to a “no hire, no fire” approach. That gives enough job security to allow consumers to reduce savings to meet higher prices.

GREAT question asked / answered …

Jun 1, 2026 Yardeni: Is There Enough IPO Money On Planet Earth To Fund SpaceX?

The mega IPOs are coming. SpaceX is set to go public on June 12, raising $75 billion to $80 billion at a market valuation of up to $1.8 trillion. It will be the largest equity offering in history. Then, Anthropic and OpenAI are expected to go public with market capitalizations of $1 trillion to $1.75 trillion each. Fears are mounting that the “AI-3” IPOs will suck the oxygen out of the rest of the stock market. We aren’t as concerned.

The combined market value of these three companies is widely expected to total $4 trillion to $5 trillion once they go public. The capital being raised is around $200 billion. To raise so much money, Wall Street’s investment bankers are planning to give retail investors the opportunity to participate in these IPOs. We expect that they will respond enthusiastically.

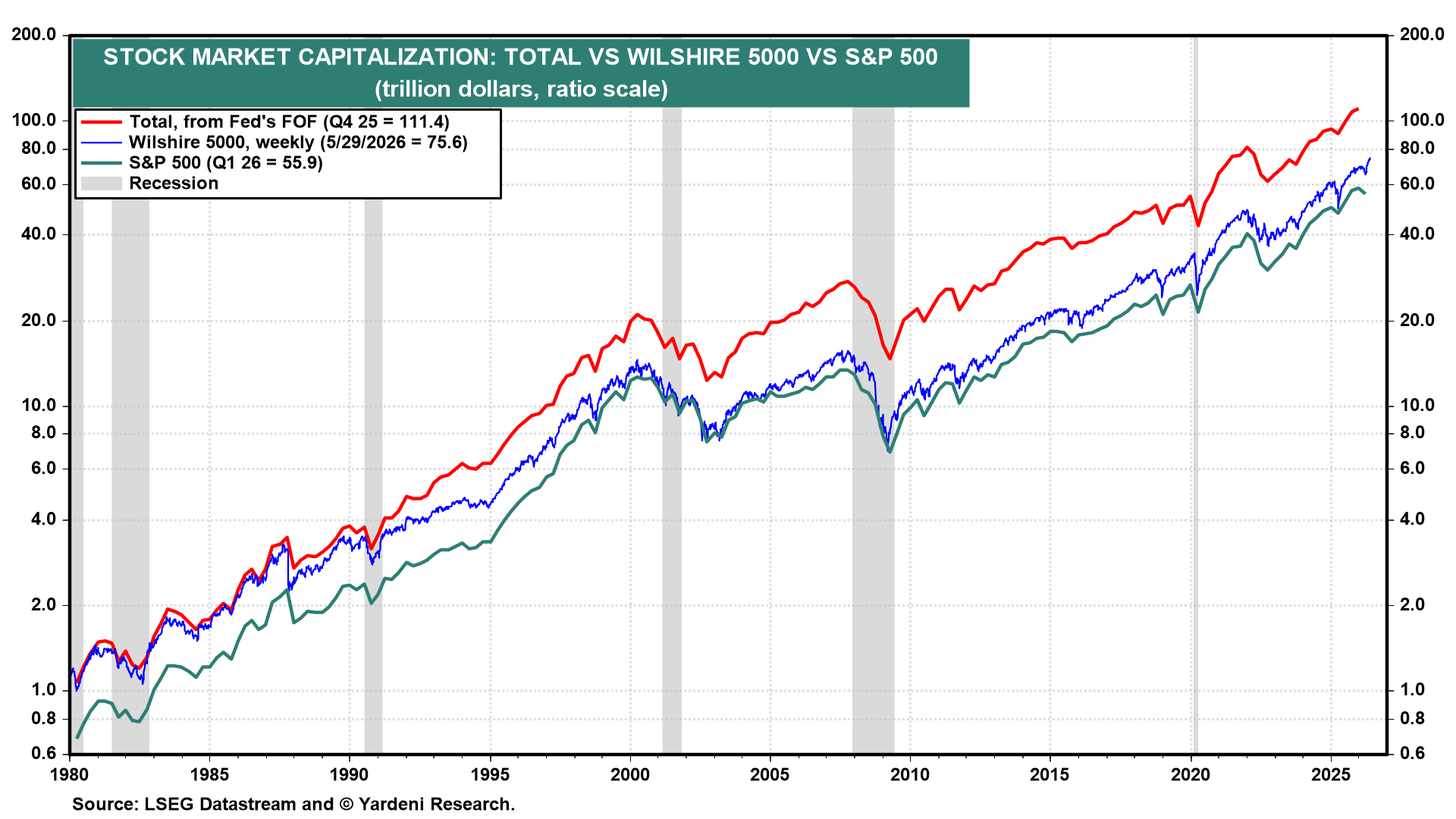

The market capitalization of the Wilshire 5000 is $75.6 trillion (chart). It is close to $60.0 trillion for the S&P 500. Will these measures increase by $4 trillion to $5 trillion when the AI-3 go public? Not based on free float, i.e., the shares that are available for the pubic to trade (excluding closely held shares, insider holdings, and government stakes). SpaceX is only floating roughly 4.3% of its shares to the public. The other two AI-3 are also likely to provide relatively puny free float.

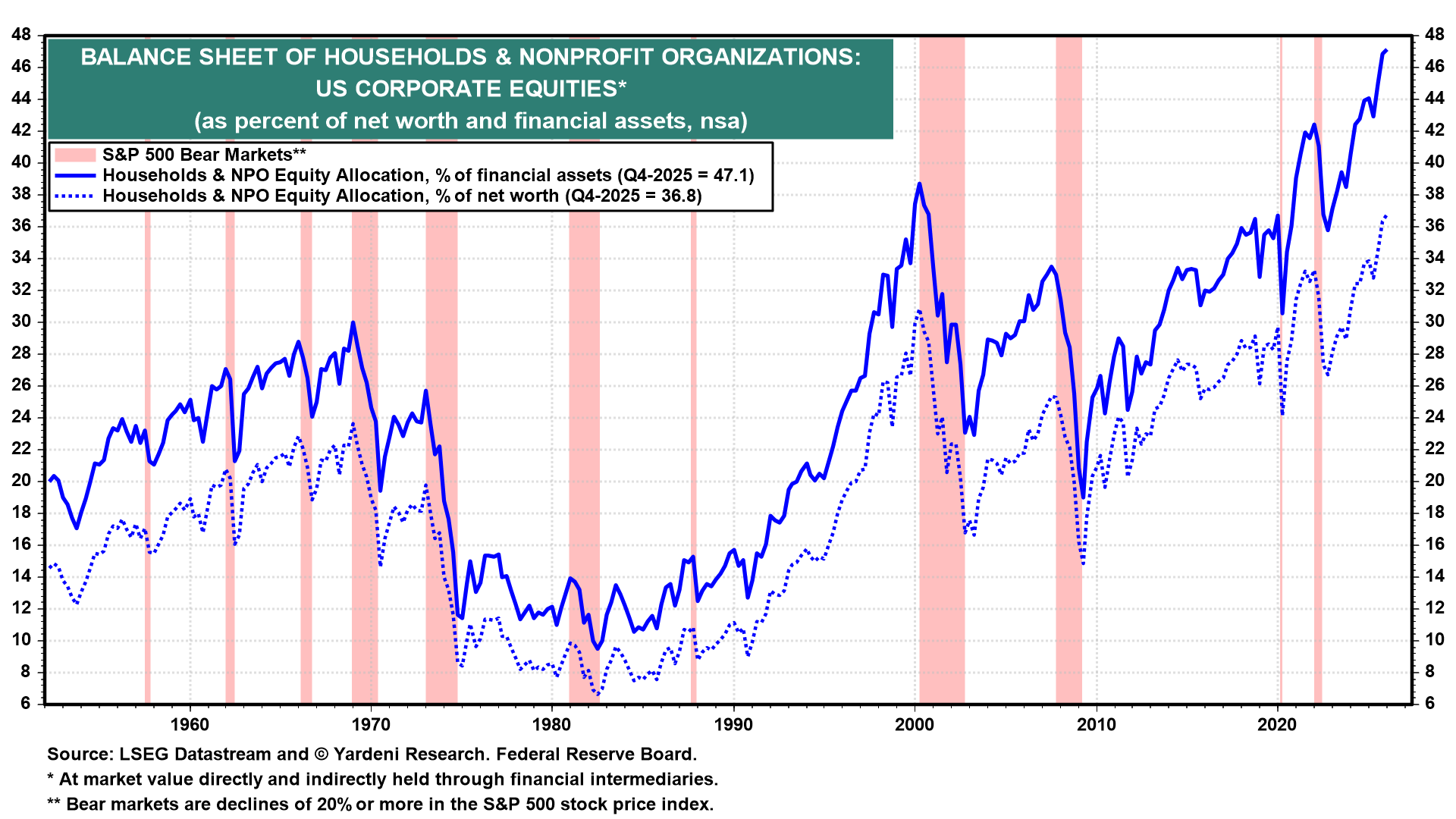

…At the end of last year, households (including nonprofit organizations) held a record 36.8% and 47.1% of their net worth and financial assets in equities, respectively (chart).

(4) Wall Street’s games. The index providers are rewriting their playbooks to accommodate new entrants to public markets. S&P Dow Jones is considering cutting the S&P 500’s seasoning requirement for mega-caps from 12 months to six and waiving the four-quarter GAAP profitability gate that has been in place since 2002. Further, the Nasdaq cut its inclusion window from 90 trading days to 15, effective May 1.

Bloomberg Intelligence estimates S&P 500 funds would need to absorb 19% of SpaceX’s public float within six months, with the Russell 1000 and Nasdaq-100 funds absorbing another 24%. Float at the IPO will be roughly 4.3%, as noted above. This is forced buying colliding with a very limited supply. (Where is the SEC?)

Allocation conventions are bending too. We have already personally received emails from our brokers inviting us to participate in the SpaceX IPO. Retail involvement of this scale is unusual.

(5) Burning cash faster than rocket fuel. The combined 2025 losses of the AI-3 topped $25 billion. SpaceX lost $4.9 billion last year. Much of its projected valuation is based on a $22.7 trillion enterprise AI market that does not yet exist as a revenue source. There has been no proof of concept for launching data centers into space.

AND …

… Moving along TO a few other curated links from the intertubes. I HOPE you’ll find them as funTERtaining (dare I say useful) as I do … …

First up, the good Doctor SLOK says AI creating jobs …

June 02, 2026 Apollo: AI Boosting Business Formation

The surge in new US business formation is being fueled by AI and large language models, which are dramatically reducing the cost and complexity of launching a company, see chart below.

But scale cuts both ways. As some firms grow and others get disrupted, we will over time see a meaningful impact on the US labor market, see also this piece from my colleagues in Apollo Thematic Investing.

An OpED on SpaceX …

June 2, 2026 at 4:12 AM UTC Bloomberg: SpaceX — To boldly raise money where no IPO has gone before The final frontier is efficiency, as some of the world’s biggest companies land on indexes.

…SpaceX’s quest for space, the final frontier, threatens to take capital markets crashing through the efficient frontier. Key assumptions about how companies should be governed, how funds should be invested, and how markets can be benchmarked will come under assault in the forthcoming wave of IPOs led by Elon Musk’s space exploration conglomerate…