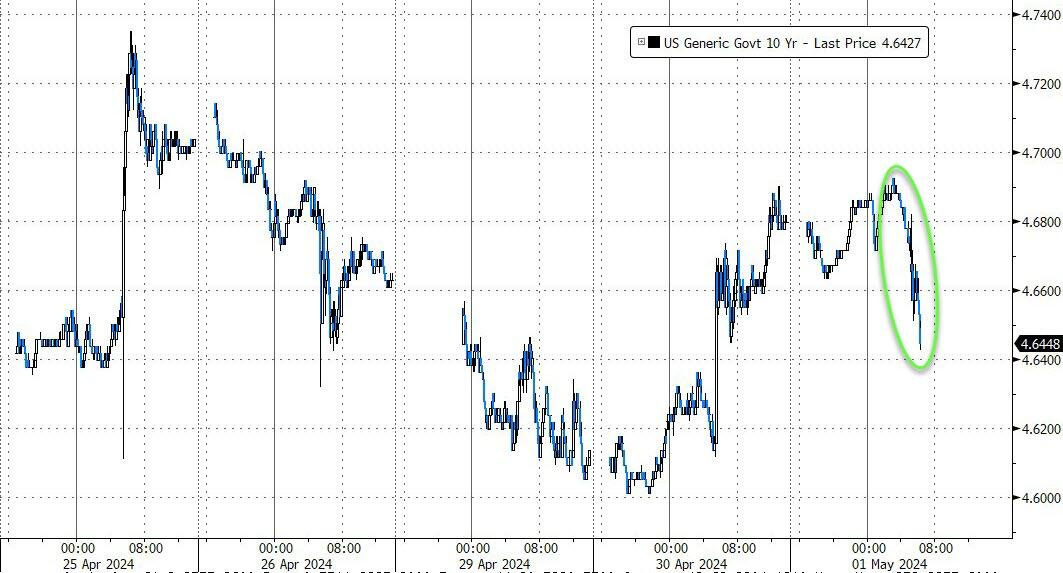

Good morning … what’d I miss? Perhaps a quick chart review will tell …

2yy: bottom of the UPTREND ~4.85%

10yy: as everyone starts talkin’ about / watching 5.00%, well, bottom of the UPTREND here ~4.40%

… I’ll summarize in a single photo below but for now, since I was outta pocket and couldn’t really catch but a glimpse of the presser, a daily RECAP from ZH with a couple choice excerpts maybe worth a look … idea being that he said NO HIKES and NOT the ‘ease’ you may be thinking this was to be and how it was that by days end, markets reversed some of the knee jerk reflex … should not be lost on any of us …

… By the close, all of Powell's pig-kissing lipstick had been wiped off (see below for the coordinated crypto/nasdaq take-down) as stocks saw solid gains erased in the hour after Powell stopped speaking... Small Caps and The Dow managed to hold on to the gains but Nasdaq and S&P closed nearer the day's lows...

… Treasury yields plunged 6-8bps across the curve on the day, with the short-end outperforming, dragging all yields lower on the week...

… The yield curve (2s30s) jerked flatter initially, then steepened dramatically back to flat on the week...

… click thru for visuals and snark you’ve come to know, love and expect … For somewhat more on topic and from Global Wall …

ZH: Wall Street Reacts To Powell Unleashing His Inner Dove

… now it’s worth mentioning follow up to QRA from Treasury as somewhat more details were shared today …

ZH: Yields Tumble After Dovish Refunding Reveals Debt Sales In Line With Expectations, No Coupon Auction Increases "For Several Quarters", And Treasury Buybacks Begin

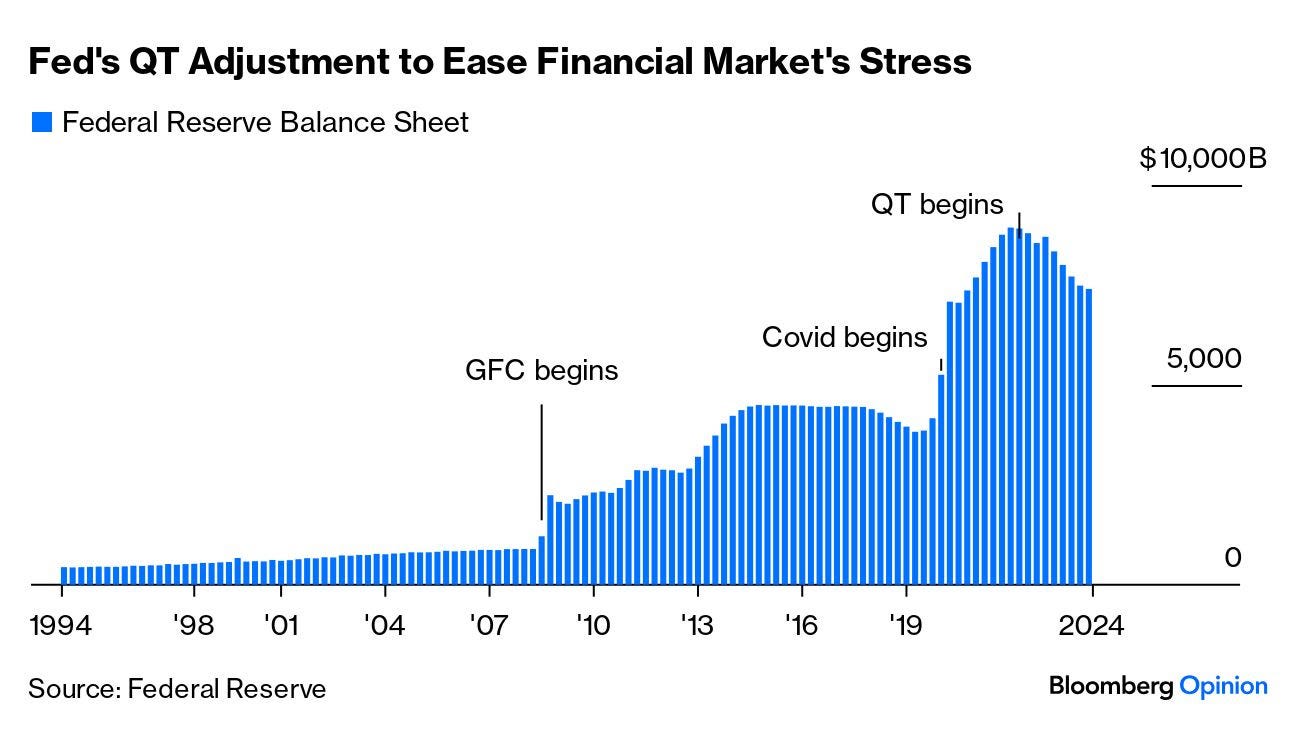

… And then there is the start of QT tapering expected to be announced later today: as a reminder, pressure on the Treasury is expected to further ease when the Fed reserve slows its run-off of US government securities holdings, something many dealers see likely to be announced later on Wednesday, as the Fed indicates that instead of $60BN in Treasury the Fed allows to run off its balance sheet every month, the Fed will taper the taper (so to speak) to just $30BN before it eventually tapers it to zero. In doing so, the gross funding need will drop even further.

Fed policymakers are set to release their policy statement at 2 p.m. in Washington. Chair Jerome Powell’s subsequent press briefing may offer clues on whether officials still expect to lower interest rates later this year — something that could further help the Treasury stem its surging debt-interest bill.

Until then, however, yields are dumping and thanks to the far more dovish than some had expected Quarterly Refunding, the 10Y yields is back down to 4.64%, down from 4.69% earlier and has erased almost the entire move following yesterday's red hot Employment Cost Index (thanks to soaring government and union wages).

And now we wait for the Fed to announce that it is tapering the taper, and sending yields tumbling even more

Now not ALL was well in Global Macro, at least not as the day began with ADP …

ZH: ADP Employment Report Strong In April, But Tech Sector Lost Jobs

… Finally, as a reminder, the ADP headline data has under-estmated the BLS magical print for eight straight months ahead of Friday's data...

So, with this kind of labor market, can The Fed maintain the illusion of any rate-cuts at some point this year? What will Powell say today?

… seems to ME that Global Wall got and saw exactly whatever it wanted to see … a NOT so hawkish JPOW (?) and a somewhat not so bearish QRA … at least NOT as much of an extreme (pick a direction) as was EXPECTED.

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly richer vs 5pm closes on ~110% volumes, the curve maintaining a steepening bias with some early front-end demand from real$ seen overnight post-FOMC. Better paying was seen going through in 5s-10s however, while fast$ was looking to sell 3s on 2/3/5 fly. USDJPY has seen a small bounce after the ~450pip intervention-derived drop post-Fed, while risk-assets are indicated a bit higher (S&Ps +0.7%, NQ +0.9%) after APAC bourses were mixed (HIS +2.5%, NKY -0.1%, KOSPI -0.3%). Commodities are also seeing a bounce, a lift seen in EUR energy prices (TZT +4.5%), while crude (+0.6%) and gasoline futures (+0.5%) lick wounds after technical breakdowns yesterday. The BBDXY is -0.4%, with 5y real rates -3bps, leading the AM rally.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: US equity futures in the green & Treasuries softer, but relatively contained post-FOMC, JPY underperforms … USTs softer but relatively contained in the fall-out of the FOMC; Bunds are higher and playing catch up … USTs in the red but action more modest than the marked two-way moves seen around the FOMC. Where the headline message was more hawkish than the last gathering but not unexpectedly so. Currently, USTs in a sub-20 tick range at 114-23.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … which is now all FOMC recap and victory lap until the very NEXT (NFP) narrative changing market moment …

The Fed kept monetary policy on hold today, but signaled that it would take longer to gain confidence that inflation is on its way back to 2%, in turn delaying the start of rate cuts. However, the Committee still sees a cut as being the more likely next move, not a hike. The FOMC also announced a slowing in its balance sheet runoff (QT).

May Is Usually OK In April, the S&P 500 delivered its first monthly loss in 2024 (about 4.1%, before dividends). But if the historical track record holds, stocks could return to a positive performance in May. The stock market typically rises in May, on average 0.9% and with a 71% winning percentage. We note that market returns in May have exceeded 5% on six occasions since 1980, including a 9.2% gain in 2000. Last year was at least positive, with a 0.8% advance. So the bullish market trend since October 2022 could continue. Still, there have been some clunkers in May, including 2022 (a whopping -8.4%), 2010 (-8.2%), 2012 (-6.0%), and 1984 (-5.9%). May starts as a busy month on Wall Street, as companies report first-quarter earnings, the Federal Reserve meets, and the nonfarm payrolls report is released. But once the retailers wrap up their results, investors will be left to ponder inflation trends, future Federal Reserve activity, the risk of recession, and the long Memorial Day weekend. Looking ahead, we are bullish on stocks for 2024, as interest rates eventually head lower, the consumer sector of the economy remains in growth mode, and earnings continue to grow into the second half of the year. To be safe, we recommend a continued focus on the stocks of quality companies with strong earnings trends.

The FOMC kept rates unchanged, indicated rates are likely to stay higher for longer given elevated Q1 inflation, and announced a QT taper. We keep our rate call unchanged, expecting one 25bp cut this year.

… We retain our baseline call that the FOMC will deliver just one 25bp rate cut this year, in September at the soonest. However, if inflation comes in stronger than in our baseline, we would expect the first rate cut to be postponed to December. We view this as almost as likely as our baseline scenario. For 2025, we continue to expect four rate cuts.

… Gone was any reference to rate cuts this year. Powell expressed less confidence about the near-term outlook for rates. He trusted that inflation would show progress this year. However, Powell was no longer willing to indicate whether this would allow the FOMC to cut rates this year:

"my personal forecast is that we will begin to see further progress on inflation this year. I don't know that it will be enough, sufficient [for rate cuts]. I don't know that it won't. We're going to have to let the data lead us on that." -- Chair Powell, May 1 press conference

Indeed, a conspicuous omission in today's remarks was the comment from the March press conference that "if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year."

Unsaid: rate hikes more likely than before

Interestingly, Powell also removed from today's remarks, the comment he had repeated again in March that "our policy rate is likely at its peak for this tightening cycle." That omission suggests that he views an additional rate hike as more likely than was the case previously…

The March estimates show that the ratio of job openings to unemployed continued to decline toward prepandemic readings, consistent with the premise of a soft landing. Estimates of the hiring rate, separations, and quits all point to less job market churn, suggesting that conditions remain in place to slow wage pressures.

BloombergBNP US May FOMC: Cutting bias remains despite higher inflation

KEY MESSAGES

We thought the May FOMC meeting leaned dovish, with the Fed retaining a rate-cutting bias and Chair Powell calling a future hike “unlikely”.

A more proactive QT taper than expected signals a cautious approach to winding down the Fed balance sheet.

We continue to see the first cut in December, with resilient inflation and election uncertainty forestalling an earlier move.

Recent price action and the monthly close in US stock futures reaffirms our view of a potential >5% move lower.

S&P e-minis Price has bounced off support-turned-resistance at the 55d MA (5148), and has was just shy of posting a bearish outside month. However, we still retain our bearish view:

We have initiated a 55-200d MA setup, suggesting ~6% losses. Weekly slow stochastics has crossed lower from overbought territory, suggesting momentum has turned around

Monthly slow stochastics has now crossed over as well.

First layer of support is at 4963.50 (April lows)

It is also worth pointing out that the test of 55d MA looks very similar to what we saw in Aug 2023, during which we also had a 55-200d MA setup.

… OTHER TECHNICAL DEVELOPMENTS WORTH NOTING

… US 2y yields: Yields briefly broke above resistance at 5.0% on April 30 as we had expected (discussed here), though we did not quite climb up to subsequent resistance at 5.08% (Nov 13 high). Now, we closely watch weekly slow stochastics for a turn lower to show fading momentum.

US 10y yields: Yields tested the upper end of 4.69%-4.73% (76.4% Fibonacci, November 13 high, psychological level) resistance, which held as we had expected. Here, we watch for indications of a potential turn on weekly slow stochastics.

DB: May FOMC recap: Hold the line, cuts aren't always on time

The Committee held rates steady and announced a reduction in the QT caps. Innovations to the statement and Chair Powell’s press conference emphasized that recent data have dented confidence regarding the pace of disinflation. Powell dialed back calendar guidance, removing the reference to rate cuts this year, and eschewed the signal from the March dot plot. Despite these hawkish changes, he also indicated that the Committee is focused more on holding rates steady for as long as needed, rather than resuming rate hikes.

Starting in June, the caps on Treasury runoff will be reduced from $60bn to $25bn, with the MBS caps remaining unchanged. The statement also noted that runoff in excess of the MBS cap – not currently an issue – will be reinvested into Treasuries.

The initial market reaction was consistent with a dovish signal from the meeting, with yields falling noticeably on the day. This reaction was likely a function of the Committee not being as hawkish as feared given the combination of 1) maintaining an easing bias, 2) suggesting rate hikes are not likely, and 3) announcing a (slightly) larger than expected reduction of the QT caps. Nonetheless, this dynamic is consistent with a broader trend of declining yields around FOMC meetings in recent decades (see "The long and the short of it: How the Fed drives long-term yields").

Our baseline outlook continues to anticipate one rate cut this year in December and that policy will very gradually return to a neutral level between 3.75-4% in 2026 (see “(Pushed) Back to December”). Hawkish risks to this view include a continuation of firmer inflation prints or an election outcome that delivers fiscal stimulus or inflationary policies. Dovish risks likely require an unanticipated weakening in the labor market

Goldilocks: May FOMC Recap: Powell Pushes Back Against Talk of Rate Hikes (NO HIKES 4 U)

The May FOMC meeting was mostly uneventful but dovish overall. While the Committee added a hawkish acknowledgment of the “lack of further progress” on inflation so far this year to its statement, Chair Powell offered a dovish message in his press conference. We have left our forecast unchanged and continue to expect two rate cuts this year in July and November.

The most notable aspect of the press conference was Powell’s strong pushback against the possibility of rate hikes. Powell said that he thinks it is “unlikely” that the next policy rate move will be a hike, that he is confident that policy is restrictive, and that the FOMC would need to see evidence that policy is not sufficiently restrictive in order to hike and is not seeing that. He also said that if progress on inflation stalled, the FOMC would respond by holding off on rate cuts, suggesting that the bar to hike is high.

Powell offered no major clues on the timing of a rate cut but struck a consistently dovish tone on inflation. Consistent with our views, he said he took little signal from the inflation uptick in Q1; highlighted the consistent progress on wage growth over the firmer Q1 employment cost index; noted that he did not see signs of reheating and that inflation expectations remain anchored; emphasized the “lag structures built into the inflation process”; expressed confidence that a decline in housing and continued supply-side healing would deliver further disinflationary dividends; and forecast that (sequential) inflation will move back down this year.

Goldilocks: ISM Manufacturing, Job Openings, and Construction Spending Below Expectations; Lowering Q2 GDP Tracking Estimate to +3.4% (see here whatever you want … “LOWERING” or “+3.4%”)

BOTTOM LINE: The ISM manufacturing index fell back into contractionary territory in April, below expectations. The composition of the report was mixed, with decreases in the new orders and production components but an increase in the employment component.Job openings declined by more than expected in March from an upwardly revised level in February. After incorporating today’s JOLTS data, our jobs-workers gap based on the JOLTS, Indeed, and LinkUp measures of job openings stands at 1.8mn in April. Construction spending decreased in March, reflecting a decline in private construction spending and against expectations for an increase. We lowered our Q2 GDP tracking estimate by 0.1pp to +3.4% (qoq ar) and left our domestic final sales estimate unchanged on a rounded basis at +2.8% (qoq ar). We launched our past-quarter GDP tracking estimate at +1.6%, unchanged from the advance reading.

Treasury’s 2Q24 refunding announcement contained no major surprises. Treasury announced privately held marketable borrowing of $243bn/847bn for Q2/Q3, while coupon auction sizes largely remained unchanged from the previous refunding cycle, except for slight increases in TIPS auction sizes, in line with our expectations.

Going forward, we continue to expect Treasury to maintain the current nominal coupon auction sizes for some time and slightly raise TIPS auction sizes over time in line with previous guidance, while managing any variation in financing needs via bills issuance. This should reduce uncertainty around the duration supply outlook. Incorporating Treasury's quarter-end TGA targets and our updated QT assumptions, we now expect $500bn of net coupon issuance to the private sector and $253bn in net bill redemptions for Q2, and $542bn/$214bn of net coupon/bill supply in Q3. Given elevated deficit projections, this should see bills as a share of outstanding USTs to remain above the TBAC-recommended 15-20% range for the foreseeable future.

Treasury also released details on its buyback program. Compared to previous guidance, the implied maximum amounts announced today are lower than expected, and we don't expect the current buyback sizes to have a material market impact.

We are watching the formation of a third peak for yields in the last 18 months. The two previous occasions did not prove to be definitive buying opportunities, so there is quite some trepidation around the current rise in bond yields (fall in prices)

A triple top is a term used to describe a chart pattern of three peaks, at approximately the same level, followed by pullbacks. In technical analysis, to qualify as a signal that there might be a change in market direction, the triple top should occur following a period when there was an uptrend.

The underlying assumption is that the yield peaks form a level of resistance against higher yields, and that if the yield were to fall below previous lows in the pattern, the triple top would be complete. At this point, investors and traders would look for a further decline in yields.

Our chart plots both nominal and real yields at the short end of the US curve. We use the one-year forward rate (1Y1Y) for Treasuries and inflation protected securities (TIPS), the latter capturing the real yield. Forwards help us remove the near-term cyclical noise, which is currently associated with the two-year spot yield, for example, and provide a more stable market estimate of where yields will be one year hence.

The nominal yield (red line) has not quite formed the third peak, but if the trend of recent weeks continues, this might be a triple top in the making. We see that the first peak was just before the regional bank stress in March 2023, and the second in midOctober 2023, coinciding with strong real economy data and a background narrative of a demand-supply mismatch in the Treasury market.

Why does it matter whether the 1Y1Y rate forms a triple top? It’s only a chart and, while there may be some psychological importance for the yield levels, surely investors should be more focused on the fundamentals?

Here are four reasons why it is worth watching.

… The move in yields this year has corresponded to the pricing out of rate cuts, from almost seven 25bp increments to less than two today. From investors’ perspectives, there is at least some comfort to be drawn from how little easing is now priced in. They will be hoping that the correct interpretation of our chart is the formation of a triple top, thereby signalling that the uptrend in yields is set to reverse.

NWM: April 30- May 1 FOMC meeting recap (updated call)

Update to our Fed Call: No rush to cut

As universally expected, the FOMC left the fed funds target range steady (5.25-5.50%)

Statement acknowledged stalling out in inflation progress

Powell sounded a bit more cautious than the last meeting

We raised our PCE inflation forecast after strong Q1 signaling less progress than we thought. We now project only one 25bp rate cut this year (and 200bps in cuts in 2025)

RBC: U.S. Fed held interest rates unchanged in May

… Bottom Line: Chair Powell continued to point to lower job openings as a sign that labour demand is softening, and said it is "unlikely that the next policy move will be a hike." Still, the policy statement reiterated that policymakers need to be confident that inflation pressures are moving sustainably back to 2% before shifting to lower interest rates, and it still looks increasingly unlikely that will happen quickly enough for the Fed to follow through on the 75 basis points worth of cuts to the fed funds target range by end of year expected by the median FOMC participant at the last meeting in March. Our own base case assumption is that the Fed won't cut the fed funds target until December, with that expected cut still contingent on economic growth and inflation pressures slowing.

The Federal Reserve announced a slower pace of shrinking its balance sheet. Context is important here—quantitative policy is about the balance between the supply of and demand for liquidity. Demand for liquidity was slowing significantly after the pandemic, requiring the Fed to shrink its balance sheet to match. Liquidity demand is now slowing less, so the Fed’s balance sheet can shrink more slowly.

The Fed’s statement noted a lack of progress toward the 2% target. Most inflation measures are within a reasonable range, and the market-based core PCE deflator (the inflation measure Fed policy actually has some influence over) continues to slow. It is hard to know what “higher for longer” is supposed to achieve. It is unlikely to bring down owners’ equivalent rent, or motor insurance, or medical inflation.

The OECD publishes the economic outlook. As with most international organizations’ forecasts, markets will have priced in the economic narrative several months ago. This is mainly a media and political event…

Summary As was widely expected, the FOMC left the fed funds target range unchanged at 5.25%-5.50% at the conclusion of its May meeting. It was evident, however, that the Committee believes inflation's return to its 2% objective likely has a somewhat longer and uncertain journey ahead. In the post-meeting statement, the Committee noted that "in recent months, there has been a lack of further progress" toward its 2% inflation goal. This setback in obtaining confidence that inflation is on a sustainable path back to 2% reinforces our view that any reduction to the fed funds rate remains at least a couple of meetings away.

The Committee announced that it will slow the pace of quantitative tightening (QT) starting on June 1. The monthly cap for Treasury security redemptions was reduced from $60 billion to $25 billion, while the monthly redemption cap for mortgage-backed securities (MBS) was left unchanged at $35 billion. The slow-but-don't-stop approach to balance sheet runoff is an attempt to keep normalizing the size of the Fed's balance sheet without creating money market stresses like the ones that occurred in September 2019. The move to a slower pace of QT was well-telegraphed by the Committee, and the outlook for the federal funds rate will be far more critical to determining the level and shape of the yield curve in the months ahead, in our view.

Summary On net, the March JOLTS data point to a jobs market that continues to normalize but is far from falling apart. Job openings at the end of March fell to 8.49 million, leaving them down 12% over the past year. The number of job openings per unemployed worker slipped to 1.32. While still above the 2019 average of 1.19, the declining ratio of openings per unemployed worker demonstrates that the labor market continues to gradually loosen.

Wells Fargo: Worst of Both Worlds: Are the Risks of Stagflation Elevated?

Part III: Where Is Stagflation Headed from Here? Summary

In the first installment of this series, we presented a simple framework to characterize stagflation and identified 13 instances in the United States since 1950. We briefly summarized past episodes of stagflation in the second installment. In this final report, we consider the risk of stagflation in the coming years.

Inflation gained significant momentum in 2021 and has remained persistent since, though the drivers have shifted. Gummed up supply chains and limited labor availability in 2020 helped push selling prices higher in 2021 and 2022. By our framework, the CPI broke into "severe" territory in Q4-2022 after spending six straight quarters more than three deviations above 2.0% on an annual basis. In 2023, supply chain and labor dynamics improved, but strong consumer demand continued to pressure prices higher.

Economic output has been mostly strong, and ample fiscal stimulus has supported household liquidity and consumption in the face of elevated price growth. That said, real GDP growth slowed below its prior cycle's average in the first half of 2023 and in Q1-2024, pointing to a moderation in growth and a gradual loosening in demand.

Though the Federal Open Market Committee has hiked the target range of the federal funds rate by 525 bps in just under two years, output growth remains respectable and inflation remains sticky. Fiscal support has ramped up over the past few years, further boosting aggregate growth, and the federal debt has increased to levels not seen since WWII.

We suspect government purchases will moderate in coming quarters, which will dampen its contribution to real GDP growth. Though the unemployment rate is at a decades' low today, we expect the labor market to gradually loosen as restrictive monetary policy continues to filter through. Less marked job growth will weigh on real disposable income, further dampening real GDP growth and inflation by pressuring consumer spending.

Should our forecast come to fruition, our framework says the current bout of stagflation will end in the fourth quarter of this year. What was once a severe episode of stagflation in 2022 has downgraded to a mild case in the opening innings of 2024, but the path of inflation remains uncertain. We suspect the risk of stagflation remains elevated in coming years, especially if the labor market does not loosen as presently anticipated.

Yardeni: Powell Says No Stag, No Flation. (everyone’s talkin’ EARL … to support an idea)

Fed Chair Jerome Powell wasn't dovish at his presser today. But he wasn't hawkish either. He said, "I think it's unlikely that the next policy rate move will be a hike." The 2-year Treasury yield fell back below 5.00% to 4.98%, consistent with one 25bps cut in the federal funds rate over the next twelve months. The S&P 500 closed down slightly, remaining below its 50-day moving average.

The big move today was in the price of a barrel of Brent crude oil. It fell sharply (chart). It had peaked at $91.17 on April 5. It was down almost $8.00 since then to $83.44 today. It cracked through a couple of support lines. Apparently, much of the geopolitical risk premium has come out of the price, which now reflects the perception that there is plenty of oil supply and weak global oil demand. The pump price of gasoline rose 13 cents per gallon during April. It could fall during May helping to keep a lid on inflation.

In economic news, the April ADP National Employment Report showed that private sector payrolls rose by a solid 192,000. It noted: "The average pace of hiring has accelerated over the last three months after slowing late last year, almost matching gains made in the first half of 2023. Pay growth continues to slow." …

… And from Global Wall Street inbox TO the WWW,

Bloomberg(via ZH): US Treasury's Funding Mix Will Be Pivotal For Fed's Next Moves (QRA QRA QRA … written / sent just about 730a)

Bloomberg 5 ThingsYou Need to Know to Start Your Day: Asia (it’s been rare)

… The chair noted that policy makers are growing more confident that an interest rate cut will take longer than previously thought. His comments didn’t really change traders’ wagers on rate cuts for 2024, where at least one rate cut is fully priced in. Here’s the thing though: The Fed has already kept rates unchanged in the 5.25%-5.5% range for about nine months, and Powell's comments didn't indicate a central bank that's willing to cut rates anytime soon.

Holding rates unchanged for longer than a year has been rare historically. For risk assets, the danger is the cumulative impact of rate hikes will hit the economy, endangering the much-desired soft landing as rates take a toll on consumers and businesses. It will still take time to play out so it isn’t an immediate concern for markets. But it’s a tail risk that should keep bulls at bay.

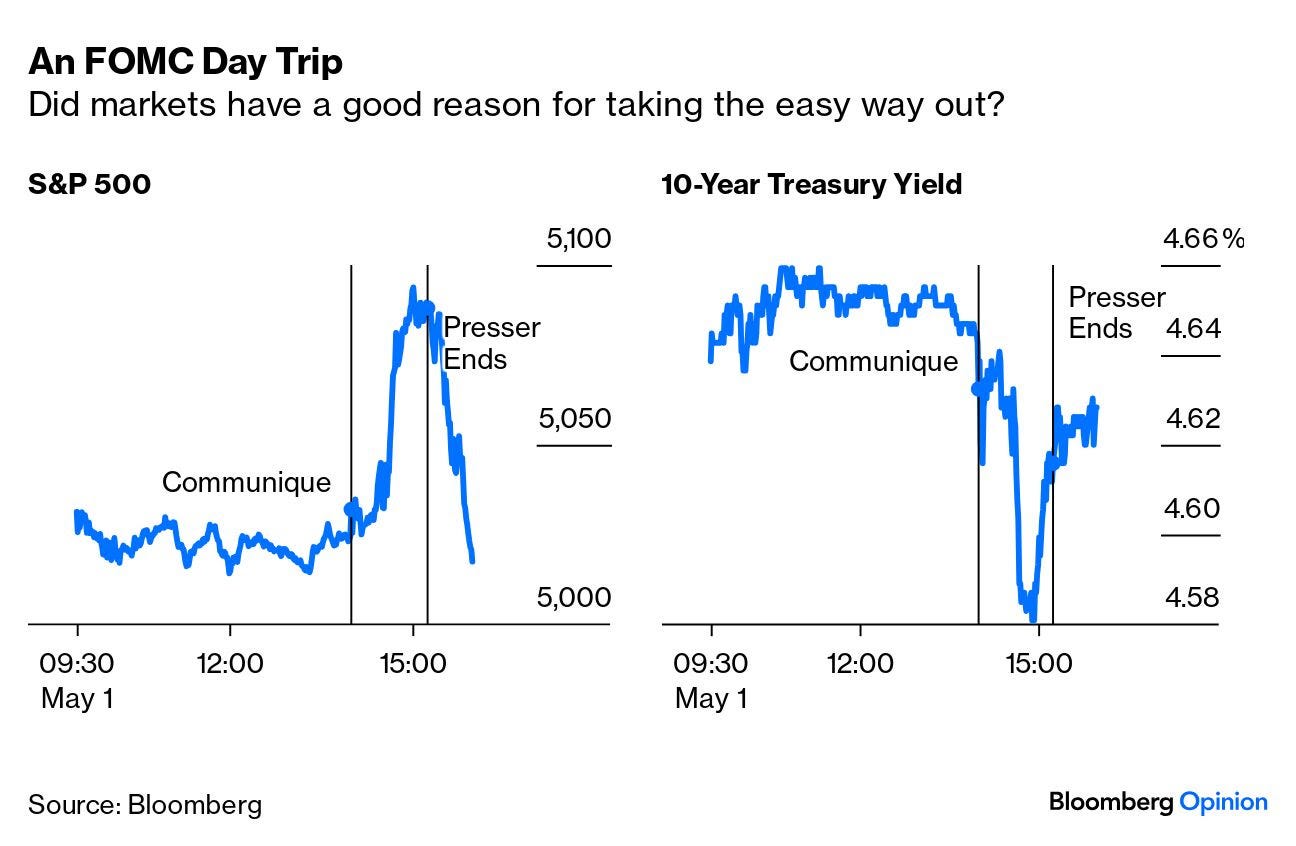

Bloomberg: You can't call Jerome Powell a big teaser (Authers’ OpED)

… The market reaction was at least quite entertaining. It went on what is known as a daytripper with stocks tumbling and bond yields tanking during the press conference, and then returning almost exactly to where they’d started by the end of trading:

Why the second thoughts? After the meeting ended, minds may have turned to the welter of data about to hit, with unemployment for April coming on Friday, and consumer price inflation still more than a week away. Unfortunately, a lot is going to be at stake on every fresh release. Data dependency could get fraught. To quote John Velis, Americas macro strategist at BNY Mellon:

To us, this decision to hold, and to still view an eventual cut as the most likely future move, sets the stage for a volatile summer ahead. Effectively, the Fed is data dependent, meaning every data release — especially as relates to inflation — acts as a referendum on where the Fed will go (or not go). There hasn’t been a lot to suggest inflation is going to moderate.

Has the Fed hit the right note? Arguably, it’s cut off its option to hike (barring extreme circumstances), which might be unwise. Rising bond yields this year, with minimal help from the Fed, suggest there’s some growth about. But as Steven Blitz of TS Lombard points out:

The market seems to understand that when the economy is raising interest rates rather than the Fed,it signals growth. The near-100-basis-points change in market pricing of the funds rate in January 2025 has rallied markets as opposed to the opposite last fall.

In other words, the stock market can get by without rate cuts if the economy keeps humming. Higher rates would throw a wrench into this — and if inflation rises further might be necessary. So we can still expect high jinks if the next few inflation readings surprise to the upside…

… Despite the significance of this policy tweak, the Powell press conference was focused on the path of interest rates. That’s fair enough. But looking beyond that would reveal more about QT’s broader long-term impact on strained liquidity. Pepperstone’s Senior Research Strategist Michael Brown argues that the adjustment allows the Fed to continue QT for longer, resulting in a smaller overall balance sheet comprised primarily of Treasuries. That would achieve the FOMC’s long-standing aim while minimizing the risk of significant financial market stress. Given last year’s regional banking crisis, and still vivid memories of the horrors of 2008, this is a well-timed tonic for market anxiety:

Inflation’s persistence over the last quarter has all eyes fixed on interest rates. But the Fed has other things to worry about. It doesn’t want to create a crisis, and it’s even prepared to risk a little damage to its anti-inflation credentials to get its way.

…Better a hawkish Fed than a dovish Fed until the inflation battle is won. The potential for reigniting inflation through action that is too early or too aggressive, as the Fed showed on multiple occasions under Chairman Arthur Burns in the 1970s, is not a risk they should be willing to take. The economy is still growing, and while we think the risk of recession is higher than market participants are currently pricing in, it is simply too soon for Fed action.

WolfST: Fed Holds Rates at 5.50% Top of Range, QT Slowdown Starts in June, Acknowledged Inflation is a Problem Again

New language: “In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.”

WolfST: Oh Deary, Where Did my Rate Cuts Go? Fed’s Wait-and-See Now Entrenched? And Suddenly Lots of Talk about “Rate Hikes”

What Powell Said about rate hikes, no rate cuts, rate cuts, and the QT slowdown while getting rid of MBS entirely.

Even by Roger Moore standards Jay's got just a bit too much grey for the part (BIG Bond nerd here!)....

In the words of someone much smarter/wiser: QT cuts = Rate Cuts for YOU!

Great article!!!

Hope JP knows what he's doing ??