Good morning … a friendly scheduling reminder, today’s note / update will be it until the weekend.

And by then, who knows where we’ll be on US / China relationships (or any others, for that matter) but for now, AND as the front end getting crushed, rate CUTS get priced back OUTTA town and 5s approach 4.10% ‘support’ detailed HERE over weekend, here’s what we think we know ‘bout the weekend just passed and THE DEAL …

ZH: U.S., China Reach Agreement To Lower Tariffs In 90-Day Cool-Off Period

… said another way …

… AND as you can tell, I’ve nothing to add and its likely a good time to step away from the keys for a few days but before I do … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are bear-flattening following Sunday’s ‘substantial’ US-China trade talks, with safe haven assets sharply lower (Gold -3%, long-end JGBs at new decade highs in yield). A mid-LDN session duration bounce did emerge, but has since been faded with light selling flows noted in the front-end on the desk offset by social buying in the long-end despite >125% normal volumes reported. S&P futures are showing +3% here at 7am, the DAX +1.1%, Crude +3.2%, UST 5s30s curve -7bps flatter, and DXY +1.5%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US and China agree to slash tariffs for 90 days sparking risk-on sentiment … Today’s session began with a bearish bias as APAC trade was focussed on the initial language coming out of the US-China talks and source reporting around it, remarks/reports pointed to a positive outcome … Thereafter, the US-China joint statement and accompanying separate press conferences saw 115ppts of reciprocal measures removed by both sides (US now 30%, China now 10%) for a 90-day period. An update which sparked immediate and continuing pressure in the fixed income space …Specifically, USTs down to a 110-06 trough from 110-13+ pre-release….

… The past two months have been sobering in that regard as recession fears ramped up, business and household confidence plummeted, annual stock market forecasts were slashed and fears of foreign investor flight mounted.

And few if any investors are confident about the eventual economic and inflation fallout from a global trade reset.

Graphics are produced by Reuters.

As Fed officials detailed at length last week, one problem comes from trying to parse both the shaky "soft" data from sentiment surveys and the more resilient "hard" data on spending, production and jobs.

Powell described the link between the two as "weak" but added: "This is outsize change in sentiment. None of us is looking at this and saying we're sure one way or the other - we're not."

And the compounding problem is that much of the hard data is lagged and skewed by the impending tariff shock itself.

Third month of CPI deflation with soft core and staged services CPI. PPI fell for 31 months, and escalate trade war may add to deflationary pressure. PBoC calls for coordinated push to boost inflation. We expect additional monetary and fiscal easing as governments closely monitor trade war impacts.

April: -0.1% y/y for CPI, and -2.7% y/y for PPI

Bloomberg consensus forecast (Barclays): -0.1% (-0.1%) y/y for CPI, and -2.8% (-2.7%) y/yfor PPI

March: -0.1% y/y for CPI, and -2.5% y/y for PPI

12 May 2025 Barclays China: PBoC easing ahead of trade talks

China's top financial regulators held a rare joint briefing to announce monetary easing actions and pro-capital market polices, following up on April's Politburo meeting. We think additional fiscal support is also likely by the summer, depending on economic developments.

Here’s a note written and sent before the deal announced yesterday …

11 May 2025 BNP: Sunday Tea with BNPP: The courage to not act

KEY MESSAGES

The FOMC kept rates on hold last week. We expect this to continue indefinitely as policymakers “pay the insurance cost in terms of second-best performance to protect against bad outcomes,” to quote New York Fed President Williams.

We see encouraging early signs of tariff moderation from the Trump administration, consistent with our base-case economic scenario.

Some early indications of tariff-fueled inflation should start to appear in this week’s US April CPI release.

… The slow burn begins: While the US April CPI report on 13 May might be too early to see significant tariff-driven price increases, we expect the data to show incipient signs of tariff-related effects.

Used car dealers were among the first to raise prices during the pandemic, and we think they can be first movers again this time. Highfrequency data on used car prices – both wholesale at auction and retail posted online – suggests that dealers have wasted little time adjusting prices since auto tariffs took effect on 3 April. While this data typically leads CPI by a couple of months, the lag tends to compress during supply shocks, raising the possibility of a faster pass-through and corresponding upside inflation risks. We note several downside risks in the report, however, namely unfavorable seasonal factors and falling energy costs that could keep categories such as airfares and hotels soft, in addition to some likely unwind in owners' equivalent rent (OER) after an outsized gain in March.

This leaves us with a rounded core CPI forecast of 0.3% m/m, with an anticipated decline in egg prices pulling the headline down to a rounded 0.2%. Our NSA forecast is close to the current market fixing (BNPP: 320.896, fixing: 320.910), though our expectations for headline CPI over the next year remain well above 1-year CPI swaps (4.0% versus 3.4%).

Germany weighing in on developments overnight … always worth slowing down to REID (see what I did there … ) and see what Saravelos is sayin’ … and hey, there’s a trade idea ahead of CPI, too …

… Let's start with all the weekend news which includes "positive" US/China trade talks, a Ukrainian and European (and US backed according to Macron) 30-day ceasefire plan for the war, and an Indian/Pakistan ceasefire (mediated by the US). The US/China talks seemed to go well but remember with tariffs currently at 145% and 125% it doesn't take much to improve the situation. Treasury Secretary Bessent and Greer (US Trade Representative) suggested "substantial progress" was made even if neither side has announced any specific measures. China’s Vice Premier He Lifeng stated that both sides had reached an "important consensus" and agreed to launch another new economic dialogue forum. Bessent had indicated that the US and China will jointly provide details on the progress at some point today so we will see if we get this…

… Staying with inflation, the main event this week will be US CPI tomorrow but generally we start the April hard data reporting cycle now and it'll be interesting to see any early impact of Liberation Day. It might be a bit too soon but watch CPI and PPI (Thursday), US Retail Sales (also Thursday) and Consumer Confidence and Housing Starts and Permits (both Friday), alongside some regional manufacturing surveys in the US. Within the Consumer Confidence data the inflation expectations will continue to be very important and something the Fed are looking at. Talking of which, Powell speaks on Thursday…

The US and China have this morning announced a huge rollback in bilateral tariffs. The highly stage-managed de-escalation is notable, with a simultaneous press conference by both sides and no "tweet" on tariffs from President Trump. All of this is a clear signal of negotiations moving into a more conciliatory and "respectful" (per Chinese demand) phase. Below we discuss the market implications, also taking in to account the UK trade announcements last week.

We now have both a likely cap and a floor on America's tariff rates. The UK has one of the least imbalanced relationships with the US and now has a universal tariff rate of 10%. China has one of the most imbalanced relationships and now has a tariff rate of 30%. It is reasonable that these two numbers now set the bounds of where American tariffs will end up this year, a material increase in visibility from just last week. The China ceiling is of course the most notable; it is materially lower than many market participants would have assumed at the start of the year. Also of note is the implicit open-ended nature of the 90-day tariff pause (Bessent: "as long as talks are on track") and persistent references to a desire to avoid economic decoupling.

The global growth outlook is improving. We have had three material economic developments so far in May. First, American trade policy has turned more conciliatory and there is now a better defined range of tariff outcomes. The peak of the trade war uncertainty is in. Second, the stage is being set for an easing in the global fiscal stance, helped by the conclusion of elections across many countries. The Euro-area (Germany), Canada, Australia, Japan, Sweden are G10 economies where an easing of fiscal policy looks likely or is already taking place, while China is front-loading fiscal stimulus too. Third, the very large drop in the oil price due to the OPEC+ market share war also represents a de facto fiscal easing to oil importing countries, most significantly in Asia and Europe. All told, our global growth view is becoming increasingly optimistic.

The Trump administration is shifting to a less aggressive stance across multiple fronts. We discussed trade policy above. Other notable developments include the departure of Elon Musk from DOGE, explicit statements from President Trump he will not seek Powell's removal, a more conciliatory stance towards Ukraine following the bilateral Zelensky - Trump meeting in the Vatican. The one policy area where uncertainty remains very high is the US fiscal stance, with visibility still low on how the Republican fiscal hawks and doves will reconcile their differences. The US budget is critical in obtaining greater medium-term visibility for US growth, the Fed and the dollar: it is likely the only material fiscal event during the entirety of the Trump administration.

Where does all of the above leave our dollar view?

The clearest conclusion from all of the above is that risky assets and by extension for volatility risk premium and carry trades in FX should have more lasting power heading in to the summer months…

After Liberation Day, markets sold off sharply as investors priced in a growing probability of a downturn. But almost 6 weeks later, there are few obvious signs of a recession, and the global economy’s resilience has been pretty remarkable. For instance, US payrolls were up +177k in April. In the Euro Area, the April composite PMI was still in expansionary territory. On trade, there’s been a notable recovery in container ships departing from China to the United States. And for markets, they’ve basically unwound the entirety of their losses since April 2, with the German DAX hitting a record high on Friday.

This has led to an unloved rally for risk assets, which has been met with plenty of scepticism. But looking forward, it’s important to remember there are still lots of factors pointing away from a recession, and this morning's news of lower US-China tariffs adds to that evidence. After all, the data has remained robust at a US and global level, and the underlying trend growth path was pretty strong beforehand. On top of that, the market’s resilience itself is making a recession less likely by easing financial conditions. And policymakers don’t want a downturn or market turmoil either, as we saw with the 90-day extension to the reciprocal tariffs. As such, if markets do continue to price out a recession, then risk assets can recover further, just as happened in 2023-24 as the soft landing was ultimately realised…

… Even on the trade front, since Liberation Day we’ve seen a stabilization and recovery in the amount of container shipping going from China to the United States (Figure 2). Again, this doesn’t look like a sharp global downturn, as the numbers remain broadly in line with their range from 2024.

… Conclusion … If a recession did happen today as a result of the trade war, it would be fair to put it in that policy-driven category, and there are still risks from the upcoming 90-day extension deadlines. But even so, the underlying robustness of the global economy and the incentives for policymakers to avoid a recession haven't gone away. Indeed, the newsflow towards trade deals, and the latest developments this morning on US-China tariffs, suggests that there remain plenty of forces that can help avoid a recession. So if markets do continue to price out a recession, then risk assets can recover further in that environment, just as happened in 2023-24 as the soft landing was ultimately realised.

We highlight 5 key takeaways for China from today's joint announcement on tariffs. (1) Today’s announcement significantly exceeded expectations; (2) Continued high-level dialogs could potentially lead to further de-escalation; (3) we see upside risks to our current 4.5% growth forecast for 2025; (4) policy tailwind will likely continue in the near term; and (5) the retreat from peak tariffs supports our long CNH recommendation made in April….

12 May 2025 DB: USD inflation strategy: going long 5y5y CPI

The repricing in USD inflation markets, driven by the negative supply shock of tariffs, has led to a significant twist-flattening of the CPI curve, pushing inflation forwards to levels unseen since 2021.

This cheapening has clearly been reflected in our valuation metrics. The 10y CPI currently trades at a substantial discount relative to our macro model (Figure 1), coinciding with a significant acceleration in both business and consumer inflation expectations. The primary counterargument, based on the specific pick-up in the UofM's long-term inflation expectations, is also being challenged, given the recent increase also in the NYFed's consumer-based inflation expectations measure (Figure 2).

From a valuation perspective, the degree of cheapening is further highlighted by the discrepancy between term premia measures in nominal markets and inflation forwards (Figure 3), while global fiscal policy has become more accommodative and there is no clear evidence of fiscal tightening coming up in the US. Finally, the recent positive news flow regarding US/China trade negotiations should further bolster risk sentiment, especially considering that the 5y5y CPI has already been underperforming relative to it (Figure 4).

We recommend initiating a long 5y5y CPI (indicative target: 2.60%, indicative stop: 2.30%).

Trade deal reaction pours in from overseas …

12 May 2025 ING: China-US trade ceasefire offers a welcome boost to the outlook

A 90-day ceasefire was agreed upon after China-US trade talks in Switzerland, with the US dropping tariffs on China to 30% and China dropping tariffs on the US to 10%. This was a larger-than-expected de-escalation and represents an upgrade to the outlook, though the negotiation process will likely remain challenging

… Rates markets: euphoric We've seen quite the market euphoria on the back of a potential deal between the US and China.

The 2Y swap rate is up almost 10bp, bringing the ECB landing zone back to 1.75%, which we think is fair. The 10Y Bund yield is up some 7bp today, now above 2.6% again. That level is still far from the 2.9% yield from pre-Liberation Day, however. Whilst we structurally think we could head back to those yields, there is still too much uncertainty outstanding to head there in the near term.

In US markets, we see the 5Y UST yield jump up almost 10bp in Asian and European trading hours, reflecting improved sentiment on the economic outlook in the medium term. US CPI numbers are expected to come in quite hot on Tuesday, keeping US rates supported. The rest of the data calendar is relatively empty, which means positive headlines can remain the main driver of global rates. Until told otherwise by data or headlines, the upward pressure on rates can hold for now…

This next grouping of notes offers one suggesting long / overweight duration, one on govt debt mechanics, a note on stocks and ALSO written and sent before the deal announced yesterday …

May 12, 2025 MS: Are You "Overweight" the USA? | Global Macro Strategist

If investors outside the US sit overweight US assets in aggregate, then US investors must sit underweight. The home bias of US investors challenges the popular view that foreign investors indeed sit overweight the US. Regardless, allocation and hedge ratio adjustments should still weigh on USD.

Key takeaways

Describing foreign exposure to the US as "overweight" requires use of a benchmark and analysis around it, not just a feeling based on recent price action.

Analyzing global equity markets suggests that an appropriate allocation to US equities relative to the global opportunity set ranges between 56-65%.

Some investors own a larger share of the US in equity portfolios than these weights suggest, but have a low level of foreign exposure in general: "home bias".

Complications that home bias introduces in assessing the degree of "overweight" do not impact potential investment conclusions driven by marginal flows.

USD should continue to weaken if investors – foreign or domestic – reduce US exposure via asset allocation shifts or changes in currency hedge ratios.

Last year, we published a look at the path for sovereign debt among developed economies. For the US in particular, the deficit and debt are high and rising. As importantly, debt service costs are rising, and so stability in the debt/GDP ratio is not in sight. We noted that primary fiscal deficits would need return to pre-Covid levels in the next 2-3 years to keep debt growth from accelerating in countries that have elevated debt/GDP levels, including the United States. We revisit this analysis to see how the debt mechanics have changed for the US and Germany, two countries that are in the midst of substantive fiscal policy changes.

In the US, the debt/GDP ratio remains at elevated levels, and the question is how quickly it will rise from here. Two aspects of the debt trajectory are striking. First, we view primary deficits as being the norm over the medium-term horizon. This is in contrast to what we have seen historically for the US: over the last three decades, the US first ran a primary balance deficit during the 2008 financial crisis. After reverting to neutral, the passage of the TCJA and the COVID measures pushed primary deficits into historically large territory. Estimates from the CBO over the 10-year horizon indicate that the primary deficit will revert to being a smaller percentage of the GDP in 2026, but not run a surplus.

The rising debt trajectory is also contingent on how interest rate expenses are projected to evolve. Interest expenses as a percentage of nominal GDP peaked in the late 1980s: although the stock of debt was much smaller, high nominal interest rates pushed these interest payments to record highs. Using the combination of the weighted average maturity of US government debt (5-7 years), and an interest rate path that sees a gradual drift down from the current levels, we still expect that nominal interest payments will surpass the late 1980s peak around 2030. The uptick will be even faster under a sharper increase in rates…

May 11, 2025 MS: Sunday Start | What's Next in Global Macro: Not the Fiscal Policy You’re Looking For

In our dialogue with clients over the past decade, we’ve often seen them project their greatest hopes and worst fears onto their expectations for the impact of US policy choices on the economy and markets. Understandably so, since over this period, public policy threatened and sometimes succeeded in causing durable disruption across the spectrum of taxes, trade, foreign policy, and many domestic and international institutions. Whether you saw value in these changes or not, it's hard to deny that policy uncertainty has been elevated. And we argue that in its first 100 days, the current administration has intensified this dynamic, with the market reaction to “Liberation Day” and ongoing tariff negotiations as Exhibit A. Investors’ focus on US fiscal policy has risen and, again understandably, their assumptions reflect both great expectations and grave concerns.

In our view, the outcome of current fiscal policy deliberations will matter but will likely defy both the highest hopes and gravest concerns. The closely watched effort in Congress to extend tax cuts and modify spending policies is inching forward. The Republicans’ slim majority will limit the range of potential outcomes. The fiscal package must gain near-unanimous support across the caucus and from the president, while the overall shape of policy must somehow satisfy both fiscal hawks and moderates worried that spending cuts will imperil their re-election bids next year. To that end, our base case assumes that a politically viable fiscal package will extend tax cuts that are set to expire at the end of this year and include incremental tax cuts mostly offset by "pay-fors" (full details here). The use of a “current policy” baseline would lead to an official deficit impact score that’s modest and viewed as politically manageable by Republicans.

Translating this from DC speak to what you need to know as an investor…

The deficit is likely to expand next year (mostly not due to the fiscal package)… We estimate that ~$220 billion of upward deficit pressure was baked into the 2026 baseline from factors such as inflation adjustments, rising interest on the debt, and weaker revenues from slowing growth. Our base case sees ~$90 billion added to that by the net effects of the fiscal package. Additional tariff revenue can mitigate those costs but would still leave the deficit expanding to about 7% of GDP in 2026. Furthermore, reducing the deficit for 2026 seems unlikely. A package with deeper cost cuts is possible, but this would likely dampen near-term economic growth and, hence, tax collections. In this scenario, we project a deficit of 6.8% of GDP (versus 6.7% projected for 2025).

…but the news flow on deficit impacts can miss critical context. Most press coverage on the deficit impact of extending the expiring tax cuts cites numbers above $4.5 trillion. They are tied to the CBO’s assessment of deficit expansion over a 10-year period in a scenario where the tax cuts expire next year (i.e., the "current law" baseline), leading to an increase in revenue. Hence, this number tells you little about how the deficit expands next year relative to this year, which investors tell us is what matters most. Furthermore, this number can be gamed in a variety of ways. For example, if tax cuts are extended for only a few years instead of 10 years or longer, the bill could be scored at a cost of $2 trillion, or potentially less, but the first-year deficit impact could be the same as under the “bigger” bill. And, of course, Congress can always change the fiscal trajectory with future policy.

Hence, investors should be wary of both overly positive and overly negative projections of the fiscal policy outcome. For bond investors in particular, the news is mixed. Deficits are increasing, and our economists don’t see this tangibly improving the long-term fiscal trajectory. However, concerns of a supply shock to the market need to be tempered, particularly if informed by CBO score-driven headlines. Another key point, particularly for risky-asset investors, is that our economists don’t see the budget package providing a meaningful fiscal impulse to the economy. True, the deficit is increasing, but the policy mix is largely a continuation of current policy, with incremental changes (tax and spending cuts) delivering a low net multiplier effect.

Of course, like any projection, ours requires continuous attention as events bring new information. This week, for example, a markup of the fiscal package in the House Ways & Means committee is scheduled. And news flow on the ongoing negotiations around changes to the state and local tax deduction (SALT) cap – a critical issue for moderate Republicans – involves preferences that shape our expectations for the final bill. We’ll keep an eye on all of it and let you know if our thinking evolves…

Sino-US talks over the weekend were described by US Treasury Secretary Bessent as making “substantial progress” on trade. Presumably so important a comment was cleared by US President Trump. The only real issue investors care about is how far the US will retreat on trade taxes. Current tariffs effectively halt bilateral trade. An 80% tariff (suggested by Trump) would also effectively halt bilateral trade. A tax of 20% would damage the US economy, but allow trade to continue.

China’s April export data, released late last week, showed ongoing growth in export values. This is being attributed to rerouting of trade, at least in part. During Trump’s first term, China rerouted about a third of trade via third countries, to help US customers avoid trade taxes.

Trump has suggested imposing a government cap on US pharmaceutical prices (presumably before imposing tariffs on imported pharmaceuticals). This will certainly produce legal challenges, which will add to the trade tax uncertainty in the sector.

With a quiet data calendar the Bank of England gets some attention—there are four speakers in the wake of the divided decision on rates. US Federal Reserve Governor Kugler talks on the economic outlook, but at this stage the US outlook relies on scenarios not certainty.

Finally, Dr. Bond Vigilante weighs in on mkts and econ in addition TO what was noted over weekend (recession odds DOWN, S&P tgt unch) …

Dealmaking is in the air. American and Chinese delegations met this past weekend to discuss how they might deescalate their trade war. Russian President Vladimir Putin on Sunday proposed direct talks with Ukraine on May 15 in the Turkish city of Istanbul that he said should be aimed at bringing a durable peace and eliminating the root causes of the war. A fragile ceasefire was holding between India and Pakistan on Sunday. That's after hours of overnight fighting between the nuclear-armed neighbors. President Donald Trump said he will work to provide a solution regarding Kashmir. This past week, Trump announced an agreement with the Iranian-backed Houthi militias in Yemen to halt US airstrikes against the militants, who agreed to cease attacks against American vessels in the Red Sea. Trump is negotiating with Iran's government to stop Iran from developing nuclear bombs.

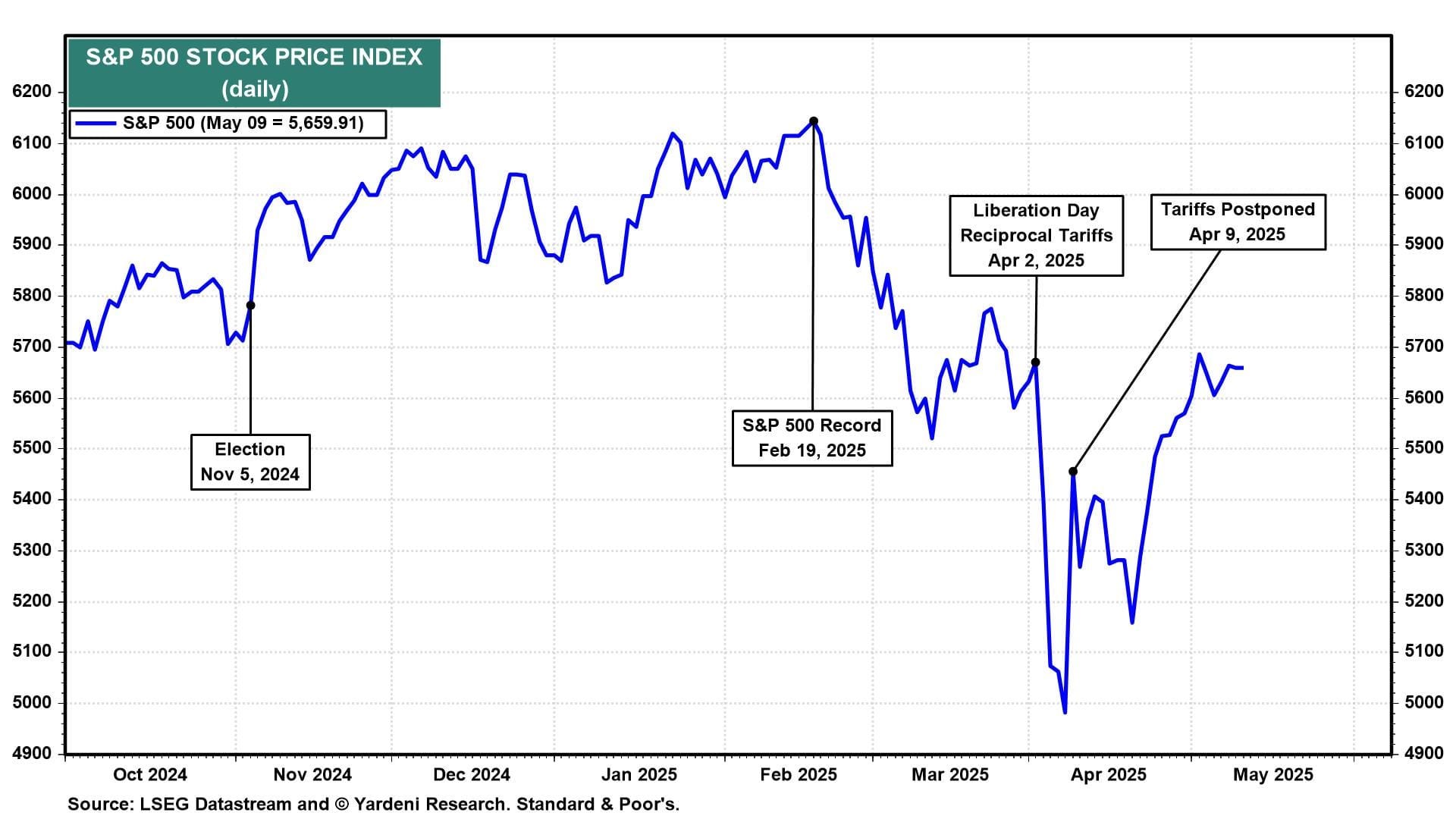

The stock market seems to have discounted the apparent simmering down of geopolitical tensions. It has been doing so since April 9. The S&P 500’s 18.9% correction since February 19 troughed on April 8, the next day, Trump postponed his April 2 Liberation Day reciprocal tariffs on April 9, except for China. The S&P 500 closed up 9.5% that day (chart). It is now up 13.6% since the trough and only 7.9% below its record high!

Wall Street's investment strategists are currently expecting the S&P 500 to end the year at 6,047 on average (chart). That would be essentially unchanged from last year. At the end of last year, the consensus expected the S&P 500 to rise to 6600 by the end of this year…

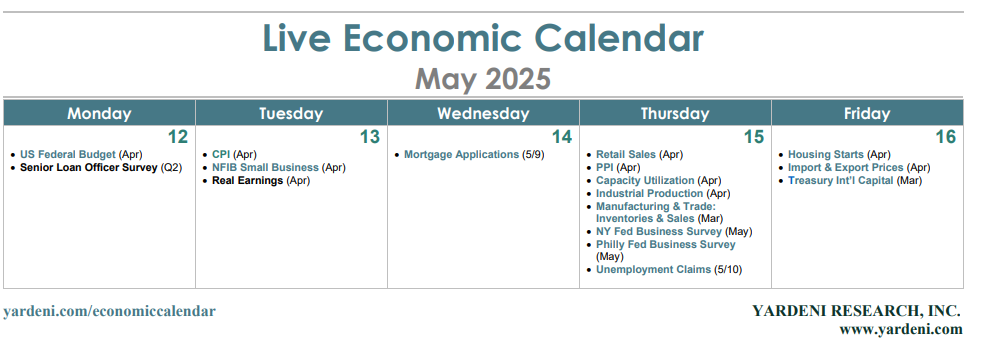

11 May 2025 Yardeni: Economic Week Ahead: May 12 - 16

The coming week is jampacked with several April economic indicators and a couple of May regional business surveys. On balance, they should show that the soft data turned even softer mostly in response to Trump's Tariff Turmoil. The hard data are likely to be mixed, though consumer-related indicators should show resilience. The week's headline inflation indicators may be subdued by stable energy prices, while the core inflation rates are likely to show that Trump's tariffs are starting to boost prices.

Let's have a closer look:

(1) Inflation. The CPI inflation rate should ease a bit further in April, according to the Cleveland Fed's Inflation Nowcasting. It has the headline CPI rising at a 2.3% year-on-year rate following March’s 2.4% gain. The core CPI is seen increasing 2.8%, the same as during March. Overall, inflation still appears to be a more immediate threat than a sharp economic slowdown. Along with the tariffs, increases like the 2.7% m/m jump in the Manheim Used Vehicle Value Index in April from March bear watching.

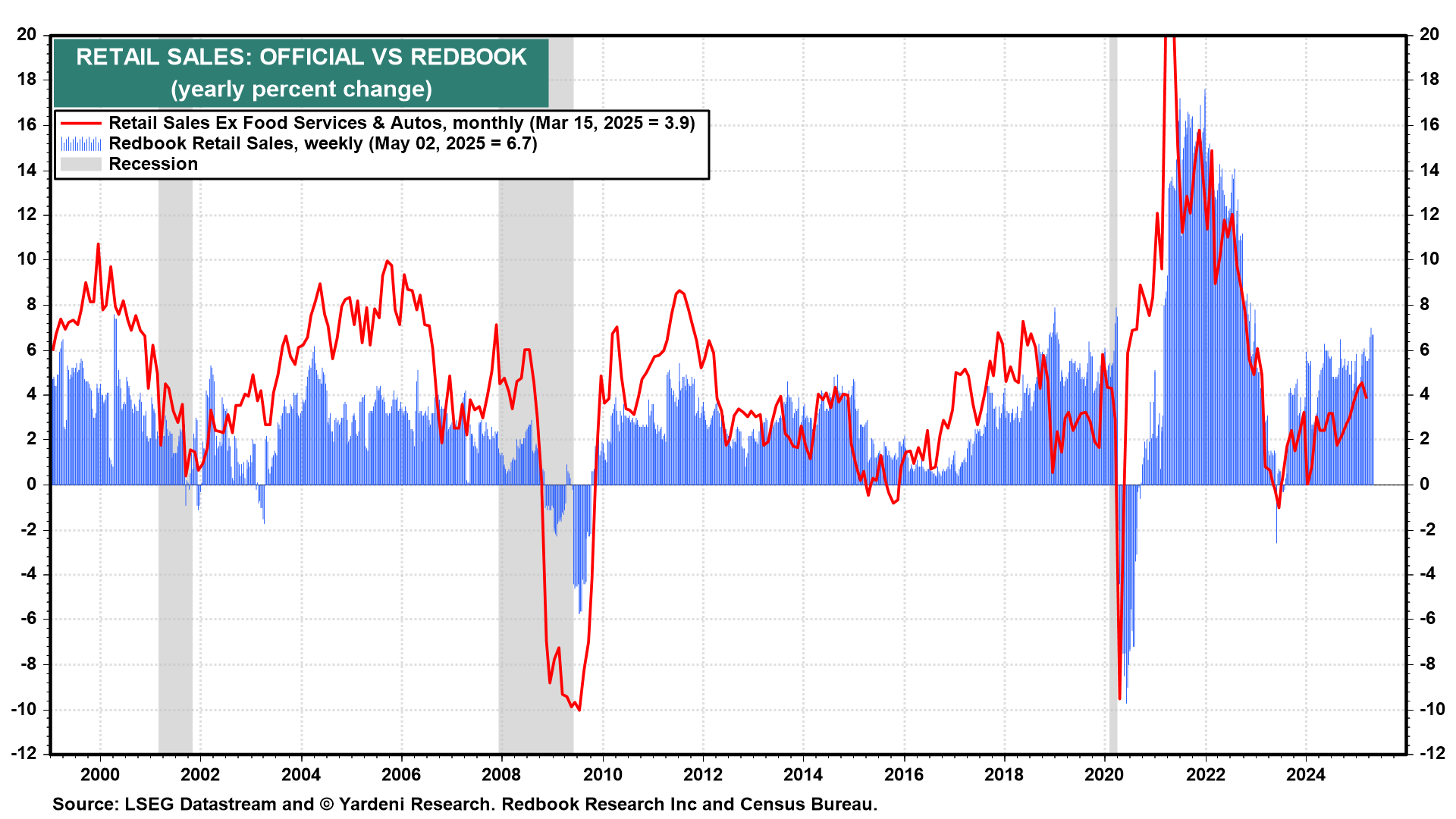

…(2) Consumers. Reports of the demise of the US consumer have been greatly exaggerated, thanks largely to a robust labor market. Case in point: a drop in new applications for unemployment insurance for the week ending May 3 to 228,000. Continuing jobless claims, meanwhile, were down 29,000 to reach 1.879 million. Though risks abound, there's little evidence that an untimely decline of retail spending is either afoot or coming. On the contrary, the Redbook Retail Sales Index has been growing at a solid pace recently (chart)

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

AND … banks seem to be having … issues … again …

May 12, 2025 Apollo: Banks’ Unrealized Losses Increase Again

FDIC data shows that the banking sector is currently holding almost $500 billion in unrealized losses on investment securities.

In a stagflation scenario, the risk is that rates will be higher for longer and credit losses will begin to accumulate, in particular for lenders to tech, growth, and VC, where borrowers are characterized by having no earnings and low coverage ratios.

One mans view … dunno I can agree WITH but we’re in a great country where ALL views are created equally and everyone allowed to share, for the most part …

… Trump blinked. 42 days after “Liberation Day” China gets a 10% base tariff level, putting it on better trade terms than the EU? It was a ramble of conflicting narratives, but the reality is the US may just have averted a catastrophic trade induced crash – it will likely still experience a stagflationary shock.

… AND another mans VIEW for your review…

May 12, 2025 at 4:00 AM UTC Bloomberg: Cynics About Trump Tariffs Should Focus on Markets An awful lot is now riding on the administration never having meant a word it was saying.

… THAT is all for now. Off to the day job … HOPE to be back to regular spammation over the weekend …

A wonderful breakthru......

Scott Bessent has been doing a fantastic job !!!!

Blain's very wise/smart but also a Marxist