while WE slept: USTs are steady in quiet newsflow; "... constrictive monetary and fiscal factors..." (=lower yields -HIMCO) vs "Where Is the Slowdown?" (Apollo)

DANGIT … I step away for a couple days and the entire world’s turned into a great big shook up giant snoglobe !!?? !!

Ok, I know … LATE (as usual) to the scene … I’ll move on then and lead w/a recap of Monday FUNday as weekend at Bernie’s news getting more officially (?) priced in and the dust settling …

… However, any 'Trump trade" unwind is NOT evident in bond-land...

...with the curve bear-steepening (as we would expect because Trump's “fiscal overstim / deregulation” bearish outcomes for Bonds are more problematic for the long-end of the curve)...

…Which suggests, perhaps the equity gains are due to other issues...

… In as far as the ‘Trump Trade’, here’s an infographic via Reuters (HERE)

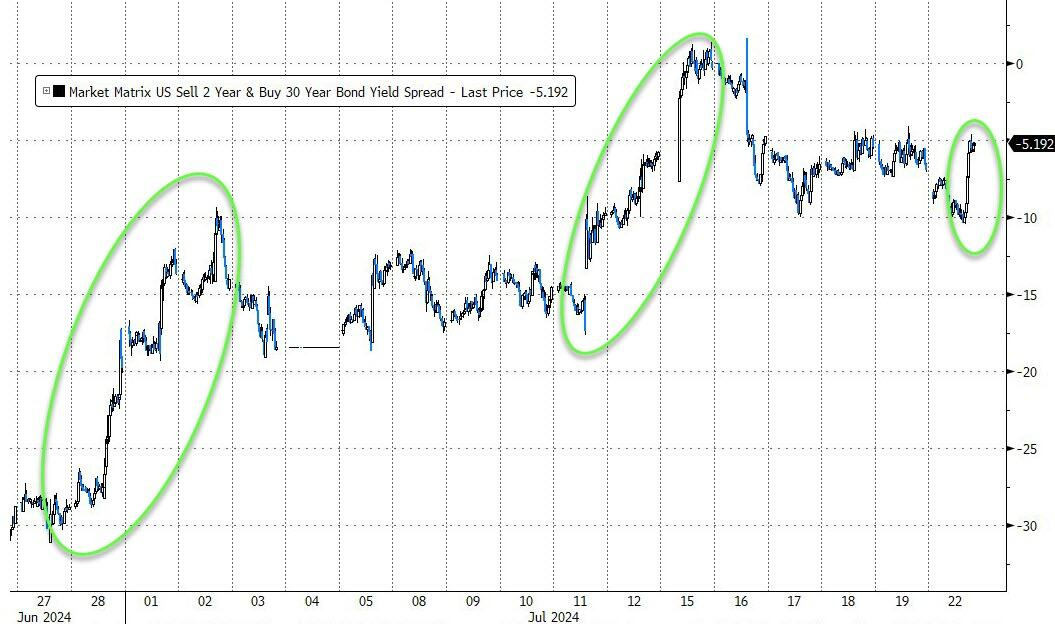

… at resistance with extended / extremely overBOUGHT — thanks, Team Rate CUT — momentum … last time this extended was heading in TO 2024 when there were what, 7 CUTS priced?

2yy DAILY

… overBOUGHT momentum correcting and rates moving marginally higher, offering a marginal concession — NOT the worst thing in the world — if only it would last until 1pm …

… moving right along and TO a couple / few things (in addition TO the obvious) which you might enjoy …

First and foremost on MY list of summer reading is HIMCOs Dr. Lacy Hunt.

He is perhaps one of the founding members of Team Rate CUT before there ever were such a thing … HIS views date back DECADES and for the most part, he’s been RIGHT … think of him as the bond markets Warren Buffet — IMO (which you didn’t ask) — and he pre dates ‘the bond king’ (PIMCOs Gross) and the current anointed king at DL, Jeff Gundlach) … and so, without further delay …

HIMCO Q2 2024 (1st sentence AND conclusion excerpted so as NOT to leave you in suspense … yes, he’s STILL BULLISH of bonds … )

Amidst a widespread deterioration in the economic landscape, it is crucial to underscore the current detrimental roles of monetary and fiscal policy…

… Cyclical economic deterioration and constrictive monetary and fiscal factors point to a weaker economy, less inflation, and lower Treasury bond yields.

… I cannot claim the wisdom of Dr. Lacy HUNT and I only knew few in command of facts who HAVE earned similar level of respect. First, Danielle DiMartino Booth of ‘The Daily Feather’ is one such person and Eric Basmajian of EPB Business Cycle Research another …

I’ll defer to his wisdom and steadfast bond bullishness as I try and come to grips with HIS ‘why’ and, as always, note how we’ve all got a right to an OPINION and, collectively speaking, all OPINIONS are created equally….

THIS4pg missive guides you through a look at worsening fiscal policy situation (think NEGATIVE NET SAVINGS) and how it is, then, in combination with tight Fed policy, by definition, CONTRACTIONARY … Think GDP and GDI as you’d imagine by tight policy.

MY simpleton view that because nothing visibly ‘broke’ (although March of 2023 we all thought … maybe), the economy is just fine … is, well, MORE than taken to task.

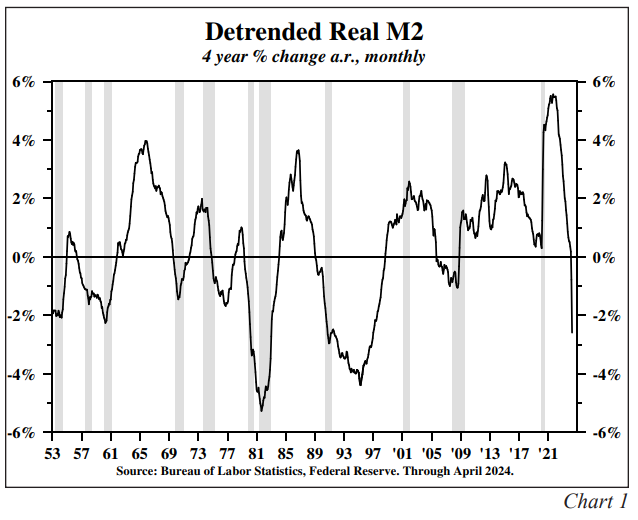

I’ll have to read THIS4pg missive a couple / few more times to come to grips with how deep are the wounds in the US economy but Dr. Hunt offers glimpse of dramatically slowing REAL M2 and ‘other deposit liabilities (ODL) … both extremely DISINFLATIONARY …

… Based on the annualized growth rate, detrended real M2 swung from slightly above zero in late 2019 to a post-1950 peak of 5.6% during 2021 to a deeply negative -2.6% in the last 48 months (Chart 1).

… continue reading THIS and know every one of us has an OPINION and we know how they are all created equally …

Its just that some OPINIONS are created more equal than others …

Have at Dr. Hunt’s latest OPINION (and defense / logic and REASONING) and scroll down to the bottom for a chartbook of, say, another such view (Apollo: Where Is the Slowdown?) offered over the weekend…

… here is a snapshot OF USTs as of 626a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: DXY flat whilst JPY gains, US equity futures mixed ahead of key Alphabet and Tesla earnings … USTs are caged within a tight range, Bunds are slightly firmer and surpasses 132.00 whilst Gilts lag … USTs are steady in quiet newsflow. There has been a lot of noise surrounding the Presidential election. However, there hasn't been much in the way of sustained price action to Harris entering the race. US yields are a touch softer in the belly but marginally so.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … in reaction TO THE election news and turn of events as well as a couple / few other developments helping to shape shift the markets narrative …

ABNAmro: Macro implications of the US Elections - Trump tariffs cause a recession | Insights newsletter

Democrat victory only marginally alters the US’ economic trajectory, Republican victory blows it off course. A full-scale implementation of the Trump-tariffs will increase inflation and put the US in a recession. The impact on the economy is as permanent as the tariffs, output and price levels do not recover. A partial victory, where Congress is divided, improves economic outcomes relative to full victories.

BARCAP: 'October surprises' come early this year, abruptly shaking up election campaign

In the last week, former President Trump survived an attempted assassination and President Biden announced his withdrawal from the campaign. We provide updated views on the state of the race and what to watch next.

BARCAP U.S. Equity Strategy: Mid-Year Outlook: Valuations Reset, Fundamentals Solid (another guesstimate being marked UP to market …)

Raise FY24 SPX PT to 5600 from 5300, 23x $241 EPS (from $235). Macro moderation to weigh on ex-Tech EPS, but Big Tech to continue offsetting upwards. Recent selloff looks contained, valuation reset leaves more room for preferred themes: Growth, Large over Small, services spending stocks & broadening beneficiaries.

… We introduce our FY25 S&P 500 price target at 6500, based on 24x our base case FY25 EPS estimate of $268. While substantial uncertainty surrounds FY25 estimates at this stage, we expect most of the macro inputs to our EPS framework to be smaller (but still negative) headwinds for earnings growth next year, with the exception of weak EM growth. Current Street consensus for FY25 is $280, which looks too optimistic to us.

BNP: US refunding preview: Addressing the deficit in the room (there’s a Trump / election trade in here … I’m quite certain of it…)

Treasury is expected to revise lower its borrowing estimates due to changes in QT assumptions while near-term deficit needs have likely increased, requiring further reliance on T-bills.

We expect Treasury to pause nominal coupon and FRN auction size increases again at the August refunding but will look for any indications on the timing of future increases in the medium-term.

Cash management buyback operations are likely to be announced heading into September tax season while liquidity buyback operations continue for the next quarter.

BNP: Sunday Tea with BNPP: Weakness rather than rotation?

KEY MESSAGES

We continue to believe that the belly of the rates curve will react asymmetrically to weaker economic data.

We remain positioned in 5y spread receivers and 5s30s steepeners.

Underlying price action in the US equity market looks worrying. We like protecting the downside via S&P500 puts.

… For markets, the reaction was mainly focused on a few specific assets, and it basically led to a partial reversal of the “Trump trade” that was evident last week. Although not everything behaved as you would have expected. In essence, the perception is that Biden’s withdrawal makes it more likely that the Democrats will keep control of the White House, and the Republicans are less likely to get the full sweep that would also see them win both chambers of Congress, so making Trump’s policies marginally less likely to be implemented. This theme saw a better day for assets that might do better under a Democratic administration, such as solar energy firms including Sunrun SolarEdge Technologies (+2.37%) and SunPower (+5.37%). Meanwhile in the FX space, the Mexican Peso (+0.76%) strengthened against the US Dollar, and was one of the top-performing global currencies yesterday.

Overall, while there were some clear moves in specific assets, it was difficult to detect a broader move to price in any political outcomes across equities and bonds. One classic “Trump trade” has been a curve steepening. While this saw some reversal early in yesterday’s session, with the 2s10s curve trading 3bps flatter intra-day, by the close it was actually +1.0bps steeper at -26.7bps. This came as a rise in yields around the European close sent yields higher across the curve, leaving the 2yr yield up +0.5bps at 4.52%, and the 10yr yield up +1.4bps at 4.25%. However in Asia this morning, yields on 10yr USTs are -1.6bps lower as we go to print. Over in Europe, yields on 10yr bunds (+2.7bps), OATs (+1.5bps) and gilts (+3.7bps) all moved higher…

… 1. Equity positioning is still elevated by historic standards… 2. We're about to enter the toughest part of the year on a seasonal basis… 3. Historically, it’s proven very difficult to maintain such a consistent run of gains after a relentless move higher.

4. Global political uncertainty is unusually high right now… 5. Plenty of tail risks are still out there, as shown with the massive IT outage on Friday…

PBOC unexpectedly cut the 7d OMO policy rate by 10bps to 1.7% this morning. The rate cut is likely the result of policymakers gathering efforts to achieve the 5% growth target for 2024, which has become more challenging after Q2 GDP missed expectations. PBOC also made some changes to its OMO and MLF facilities, which will likely enhance its control on both short-term and long-term interest rates. Looking forward, (1) whether PBOC will increase exchange rate flexibility in the coming days after the rate cut will, in our view, have important implications for its future rate decisions; (2) PBOC’s rate cut today also raises the expectations that the government may further ease fiscal and property policy at the upcoming Politburo meeting.

MS: US Public Policy: Biden Exits Presidential Race

… Given that outcome, we think the most impactful market takeaways are still those exposed to a potential Trump win, like curve steepeners from policy changes like tariffs & immigration. Policy changes under Democratic win scenarios skew more predictable, as most represent a continuation of the status quo and hence fewer exogenous factors to consider for the economy.

MS: L-igh-t-ning Crashes (steepening seasonality AND aligned with DJT probs … funTERtaining visuals for those with all capabilities…)

It was a live-ly week for airplanes and equities. Severe lightning in the Midwest and Northeast accompanied a sell-off in tech stocks and an "IT" crash that temporarily grounded flights across the United States. We stay in UST curve steepeners, which just began their climb toward cruising altitude.

… Additionally, the seasonality pushing yields higher, led by the back end, is even more amplified this year given the focus on the fiscal trajectory and the upward bias to term premia emanating from rising probabilities of President Trump in prediction markets (Exhibit 13). Overall, we think August seasonality will likely bias the yield curve steeper, keeping bear-steepening and twist-steepening in play in the coming weeks.

In addition, we think the front end is more likely to stay pinned, especially in the next two weeks with limited tier 1 data on the horizon and a July FOMC where the Fed will be commenting on the possibilities of rate cuts priced in the market, which currently is nearly 100% priced for September (Exhibit 14). Such pricing is also likely to stick given the recent data, especially inflation, where the confidence on inflation should be building. More on this below….

MS: Sunday Start | What's Next in Global Macro: Curb Your Enthusiasm

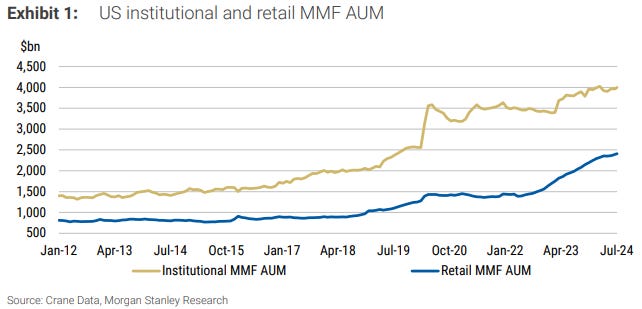

… The bottom line: While MMF AUM has grown meaningfully in the last few years, it is likely to stay high even as policy easing takes hold. Allocation toward risk assets looks to be both lagged and limited. Thus, this 'money on the sidelines' may not be as positive and as imminent a technical for risk assets as some expect.

MS: Weekly Warm-up: Does The Cycle Matter More Than The Election Outcome?

While markets have been focused on the rising odds of a Trump win, we believe that the state of the business cycle will ultimately be more important for equities. We're focused on earnings revisions breadth, which has softened recently overall but remains bifurcated at the industry level.

… The key beats are (1) there is no playbook for this in modern American politics and while we think Harris is the most likely choice, the party is not obligated by any law on how it chooses its nominee. (2) A change at the top of the ticket likely does not have material implications for policy – we already felt that the stakes in November for markets were about pricing in vs. pricing out Trump. (3) Odds of a Democratic victory may edge up considering Biden’s decision, although we think Trump will remain the favorite.

There is almost nothing happening on the economic data calendar today—things are so quiet even ECB President Lagarde and former US Treasury Secretary Summers are not speaking. As markets abhor a vacuum, there is a danger that idle investors may start listening to politicians.

US politics is certainly providing a lot of noise. US Vice President Harris has been picking up endorsements. A cynic might suggest that the timing of these aims to maximize media attention on Harris, but it would be very wrong of an economist to be cynical about the US political process. We still have some time to wait before markets receive news they might want to react to…

We maintain our view that the US economy is headed for a soft landing.

More moderate growth in consumer spending should help to keep inflation on a downward trend.

We expect the Fed to initiate a rate-cutting cycle in September.

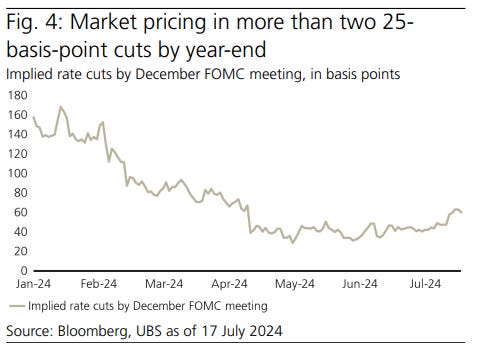

… Recent public comments from FOMC members, including Fed Chair Powell, suggest that rate cuts are likely to begin in September, in line with our base case. The recent data is giving the Fed more confidence that inflation will slow towards its 2% target, and the Fed is also becoming more concerned about potential downside risks to the economy. With the unemployment rate now above 4% and job openings well below their peak, any further reduction in the demand for labor could result in an undesirable rise in the pace of layoffs. As shown in Fig. 4, the market is now pricing in more than two 25-basis-point rate cuts by yearend, including a near-100% chance of a September cut. Our view remains that the Fed will cut only once per quarter in the quarters ahead. However, the Fed could cut much more aggressively if the economy takes a turn for the worse. On the fiscal side, we do not expect significant policy changes until after the election.

Wells Fargo: U.S. Election Update: Another Historic Development

President Biden's announcement yesterday that he will not seek re-election this fall provided yet another twist in what has been a historic past two months in U.S. politics. President Biden endorsed his vice president, Kamala Harris, for the Democratic nomination. It goes without saying that the current situation is highly fluid, and we would caution against jumping to conclusions about the path ahead. For now, we will not be making any major changes to our economic forecast in light of the news that President Biden will no longer be running for re-election. We still expect the FOMC to cut the federal funds rate by 25 bps at its September meeting followed by another 25 bps rate cut in December, with more cuts to come in 2025.

Wells Fargo: July Flashlight for the FOMC Blackout Period

We look for the FOMC to keep its target range for the federal funds rate unchanged at 5.25%-5.50% at its next policy meeting on July 31. But, with inflation trending lower and the labor market showing signs of softening, we expect the Committee will signal in its post-meeting statement that policy easing is coming into view.

… In our view, the presidential election on November 5 will not preclude a rate cut on September 18, if conditions warrant. The historical record shows that political considerations do not seem to enter the FOMC's calculus.

… And from Global Wall Street inbox TO the WWW,

Apollo: Where Is the Slowdown? (Team Rate CUT likely going to just gloss over this one)

Every Saturday going forward, we will provide an updated chart book with daily and weekly indicators for the US economy…

… The bottom line is that daily and weekly data do not show any signs of a drop-off in economic activity. Instead, the data shows ongoing steady growth around potential, similar to what we have seen over the past year. If the Fed starts cutting rates in September, then stock prices will rise further, credit spreads will tighten, and growth and inflation will start to reaccelerate …

Apollo: Extreme Disagreement Among Households About the Long-Term Inflation Outlook

the MACRO INSTITUTE: Macro Monday: Another Employment Recession Indicator (claims)

Last week was a busy one on the data front, and for the most part the releases were mixed. The first regional PMIs for July showed the Empire Fed Index lower, but then the Philly Fed Index came in higher. We will have to wait for some of the other PMIs to come out this week to get a better sense of things. The biggest story in our minds was disappointing claims data. Continuing claims came in near cycle highs and at levels associated with recession risk in the past. Indeed, a 20% rise in continuing claims off their most recent lows has often been followed by a recession. Now, this is just one indicator, but it makes this data especially prescient in the current cycle. Keep an eye out for it on Thursday.

STILL getting caught up … more later AND in my absence …

{kind=link}

"What did I miss? DANGIT … I step away for a couple days and the entire world’s turned into a great big shook up giant snow globe"....

Incredible.....definitely a year like 1968.....

Thanks for all your work !!!!!