Good morning … scheduling note — outta pocket tomorrow (Thursday) and hopes to resume regular spammation on Friday morning … That said, and ahead of this afternoons upcoming $16bb 20yr auction, a picture (worth a thousand words?) …

20yy: 5.00 support and ~4.75 resistance and here we sit, stuck in the middle with…

…momentum (stochastics) remains a BEARISH input at moment and 50dMA (4.82) is a level worth watching … for MORE levels of interest, see this mornings techAmentals by CitiFX just below …

Meanwhile, think steeper / cheaper as concession / dipORtunity … and with 20s in mind, a quick recap of some of drivers of the price action…

ZH: Empire State Manufacturing Survey Surges Higher On Heels Of Soaring Inflation Fears

… But I’d be remiss to NOT mention what everyone else is talkin’ about this morning …

Bloomberg: Trump Floats 25% Tariffs on US Auto, Drug, Chip Imports

New duties would widen trade war, hit key consumer products

Trump has proposed reciprocal tariffs, duties on metals

… here is a snapshot OF USTs as of 713a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are moderately cheaper and steeper after the RBNZ delivered another 50bp rate cut, guidance tempered by Orr’s statement that the next cut would likely be 25bps. A speech from the BOJ’s Takada proved the mirror image, unable to out-hawk the JGB market with talk of the "gradual" tightening pace ahead the April meeting (7.5bps priced). Trump’s consideration of import levies on foreign vehicles added to the inflationary risk-off tone, with DAX futures -0.9%, Crude +0.9%, USDCNH +0.2%, and 2bp steepening of 2s10s. S&P futures are showing -7.5pts here at 6:45am, with TYs near session lows after a 1m/01 block FV-TY steepener around 6:30am after the same structure was seen at 5:25am for half that size.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: Sentiment hit after Zelensky comments, Bunds hit by hawkish ECB speak … USTs are marginally in the red but essentially flat when compared to EGBs and in particular Gilts. Docket ahead features 20yr supply, FOMC Minutes and remarks from Jefferson (voter) but with the latest building permit/housing start data first. Thus far, specifics for USTs are a little light and as such the benchmark is steady in a slim five tick overnight band between 108-22+ and 108-27. However, it is worth highlighting that long-end benchmarks, particularly the 20yr, trade a little heavy pre-supply.

Opening Bell Daily: Cash hits 15-year low. Investors expect the S&P 500 to keep breaking records: 'Long stocks, short everything else' … Bank of America's latest fund manager survey showed cash levels hit a 15-year low.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

First UP, a question. IF there’s all this inmoneymarketmutualfundsandatthesametime,there′sno to be had …

BAML: Global Fund Manager Survey Cash levels at 15-year lows | 18 February 2025

Bottom Line: investors bullish, long stocks, short everything else; cash levels (3.5%) plunge to lowest since 2010 and equity investors rotate to bond sensitives & Europe as 82% say no recession, 77% expect Fed cuts, US exceptionalism peaks (89% say US stocks overvalued), and trade war seen as no more than a (#1) tail risk…

… water water everywhere yet not a drop to drink?

From one chart (of cash levels) to another (of RATES) … this / these from the very best techAmentalists out there…

As we had thought in our publication last week, yields headed higher, but held under support ranges. We retain our view of lower yields in the longer term, especially after weekly closes reiterated this.

US 2y yields As we highlighted last week, 2y yields rose and met resistance at 4.37%-4.42% (55w MA, November high, January high).

This means that we are still firmly range-bound between 4.07% (Dec low) and 4.37%-4.42% (55w MA, November high, January high).

The medium term picture remains the same - we still expect yields to head lower. Weekly slow stochastics has already crossed lower from 'overbought' territory, suggesting longer term momentum for a move lower.

…US 30y yields We have still not seen a weekly close below 4.70-4.71% (55d MA, November high) on a weekly basis.

Weekly momentum is already ticking lower from overbought territory, suggesting momentum for lower yields. IF we see a break below 4.70-471%, it would reinforce a bias for lower yields towards 4.47-4.48% (55w MA, 200d MA).

Short term resistance is at 4.86% (Feb 12 high).

… if yer NOT confused, yer NOT payin’ attention. Rates are going UP? Yep. Down? Yep, that too … no matter what happens, we told ya so … seriously, though, these guys ARE best in show and their (BBG) charts far better than mine …

This next one’s for all the ‘money marketeers’ amongst us …

We delve into the world of money market funds. Distinct dynamics are at play in the US, eurozone, and UK. In the US, repo rates are more attractive, and bills are expected to appreciate. It's also worth noting that the Fed might cut rates more than anticipated, similar to the UK. In the eurozone, unsecured rates remain elevated

… this next one’s a fun one, saying most of what you need to know in the title …

MS: Staying Long Duration While Raising UST Yield Forecasts | US Rates Strategy

Fewer and later rate cuts from the Fed in our US economics baseline raise our US Treasury yield forecasts – which we keep well below consensus and the market forwards. We see the 10y Treasury yield ending the year at 4.00%, with risks skewed to lower, not higher, yields. Stay long 5y Treasury notes.

Key takeaways

We raise our year-end 2025 10-year Treasury yield forecast from 3.55% to 4.00% on a major change in our US economists' projected outcome for Fed policies.

We continue to suggest investors adopt overweight or long duration positions concentrated in the 5-year maturity or key rate duration point.

We suggest avoiding duration-neutral yield-curve trades, as neither steepeners nor flatteners look appealing to us given recent growth data and FOMC rhetoric.

The GAO estimates the US federal government made $236bn in improper payments in FY23 – spotlighting an opportunity for DOGE to reduce spending.

US political focus should turn toward the government shutdown looming on March 14 and the automatic 1% discretionary spending cut on April 30.

… have cake. eat cake, too…Cake aside, how about some more … taxes!? …

US President Trump threatened more taxes on US consumers, focused on autos, pharmaceuticals, and semiconductors. Trump rapidly retreated from trade taxes that would be very visible to US consumers—Gen Z would notice tariff-induced inflation for avocado on toast. Less visible taxes (like aluminum) have endured. The new proposals are partially visible—taxing new cars raises second-hand car prices and the cost of car insurance—but probably sufficiently disguised as to prevent a repeat retreat.

General inflation perceptions may impact the willingness to tax US consumers further. Consumers’ inflation perception is guided by high frequency purchases (food and fuel). Egg prices are an example of a relatively unimportant part of consumer spending that has a disproportionate impact on inflation perceptions. The Trump administration recently fired a number of people trying to contain Avian ‘flu…

…The Federal Reserve January meeting minutes are due. Reactions to tariff proposals will be looked for, but uncertainty around government policies limits the value in any forward-looking statements.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

This week we get a glimpse of the first LEIs for January. Both the NAHB and the Empire Fed Index drop today, and we see preliminary numbers from the Markit survey on Friday. After last week's "less cold than expected" inflation data, we are looking forward to inflation expectations from the final Michigan Survey of Sentiment on Friday as well. The preliminary data two weeks ago was a huge inflation surprise to the upside. This series is highly influenced by gas prices, so it was a bit unusual to see it pop this much when energy prices were mostly range-bound last month. There may be something more serious brewing here, and we should all keep a close eye on inflation data going forward.

The Macro Week Ahead

Recap Of Last Week:

Last week’s data painted a concerning picture of rising inflation. Key indicators, including Core CPI, ISM Manufacturing & Services Prices, University of Michigan Inflation Expectations (1-year), and PPI, all showed an uptick in January and February. Year-over-year trends continue to run above the Fed’s 2% target, fueled by stronger Leading Economic Indicators (LEIs), a robust labor market, and less restrictive monetary policy compared to last year. This Friday, the final Michigan inflation survey for February is expected to confirm a 4.3% annual jump, up from the preliminary shock.

Despite these hot numbers, Fed Chair Jerome Powell remains firm that patience is essential to curb inflation, stressing that monetary policy is still restrictive. As a result, rate cut expectations for 2025 have dropped, and traders now expect zero rate cuts until September. Chicago Fed President Austin Goolsbee added that if inflation persists like this, the Fed’s work is far from over.

Short Week, Packed With LEIs:

With the U.S. equity market closed on Monday, Tuesday brings February’s Empire Manufacturing data at 8:30 am. While volatile, it’s worth watching after a rollercoaster of multi-year highs in November followed by sharp declines in December and January. More stable LEIs like the ISM Manufacturing Index have shown recent strength.

Other key LEIs this week include the NY Fed Services Business Activity (Wednesday), Philly Fed (Thursday), and S&P Global US Manufacturing PMI (Friday). Based on the NFIB Small Business Optimism Index, we expect continued growth in February, though month-over-month figures might cool slightly.

Housing Market ... Any Hope?:

The average U.S. 30-year mortgage rate is sitting at 6.87%, down from May’s peak of 7.22%, but still stuck at year-ago levels - leaving homebuyers struggling to remember the days of 3% rates. On Tuesday, the National Association of Home Builders (NAHB) will release February’s Housing Market Index, which is expected to dip slightly to 46 from January’s 47 number. One positive note: a key forward-looking component has surged from the mid-40s to low 60s since mid-2024, though prospective buyer traffic remains sluggish in the low 30s.

Housing starts and building permits will be reported on Wednesday, and existing home sales follow on Friday. With affordability still a major hurdle, we’re not expecting a major housing rebound anytime soon.

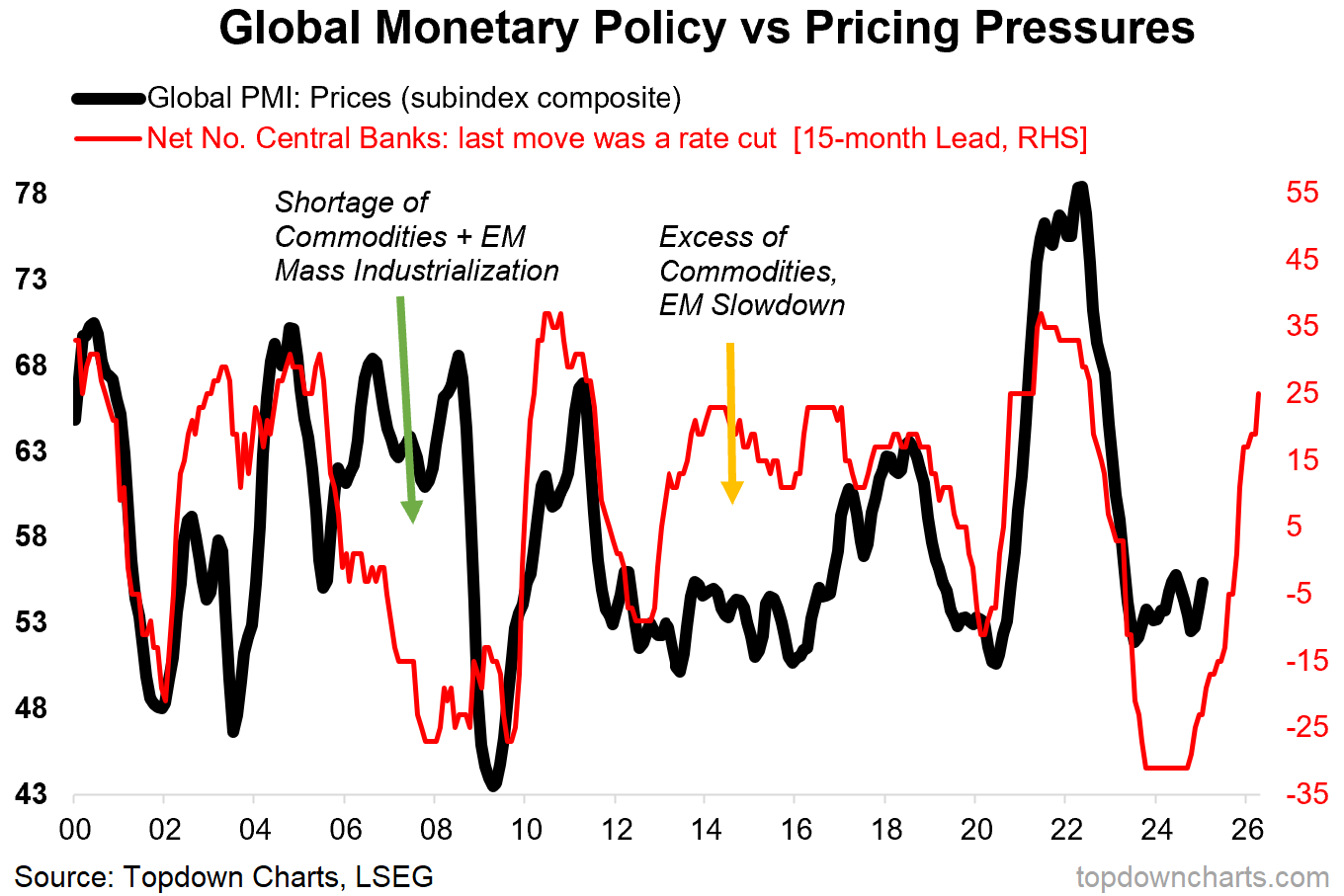

Finally, a(nother) chart …

Topdown Charts: Chart of the Week - Inflation Resurgence You need to become very familiar with inflation resurgence risk very soon...

Something very interesting is happening in the macro world right now.

Central Banks have undertaken a mass-migration from hiking rates to cutting rates.

Normally this type of policy pivot would only be seen as a panic response to recession, crisis, and downturns. And to be fair there are some weak spots out there, but there’s no crisis, no full blown recession, and asset markets are charging higher.

Inflation has come down —there is that; so you can argue that this pivot makes sense from the standpoint of pulling back on previous panic tightening…

And yet the rate cuts continue, with more central banks joining the movement (e.g. Australia + India commencing cuts this month).

That brings us to the chart below.

The red line shows the net number of central banks globally whose last move was a rate cut.

The recent surge in that indicator just goes to show how resolute the global rush to rate cuts has been.

The problem with that is the black line (pricing pressures).

The red line leads the black line (logic = rate cuts stimulate demand, higher demand tightens capacity and puts upward pressure on prices, inflation rises).

In other words, the core thesis is: stable growth (remember no recession or crisis forcing their hand this time) + global monetary policy easing = global growth reacceleration.

With commodities cheap and a decade of underinvestment in supply by commodity producers, I could not be more bullish on the outlook for commodity prices in this context. That’s a really important point — from a macro standpoint rising commodity prices means upward pressure on inflation…

From an investing and portfolio management standpoint that means a major upside opportunity (for commodities, but not much else; stocks and bonds might actually stumble in this scenario), and at the very least commodities are a logical and obvious hedge to a near and pressing risk.

So keep an eye on inflation resurgence risk and keep in mind commodities as a hedge against this rising risk.

Key point: The global rush to rate cuts mean resurgence risk is rising.

CHART NOTES: n.b. I have added notes to the chart because there was 2 major breakdowns in this relationship; first was the 2000’s emerging markets boom which saw demand for commodities explode against a constrained supply backdrop. The second is in the mid-2010’s where the opposite happened — commodity producers responded to the commodity price supercycle of the previous decade by overinvesting in supply… and then emerging markets hit the growth wall and rate cuts did next-to-nothing to offset that deflationary force.

And did you catch THE interview last night …

… THAT is all for now. Off to the day job…back Friday.

You're full of surprises never would've thought your an Iron Maiden fan Powerslave was their last Great album IMHO long live Eddie!