Good morning … There’s not much left to say / think / write / see / hear ahead of this afternoons meeting, DOTS and presser and so I’ll be brief…

10yy MONTHLY: 3.95 was ‘resistance’ now support …

moment has shifted from overSOLD to overBOUGHT and again, this is NOT any sort of imminent signal / warning but rather the nature of markets and TRADERS pricing in outcomes almost immediately … as in early 2019, momentum moved way ahead of the ultimate bottom in yields so this MONTHLY visual in effort to provide some longer-term context … with the Fed just about ready to CUT rates, what, if anything, is different this time …?

‘Bout ReSale TALES & Industrial Production … from someone / thing w/a Terminal …

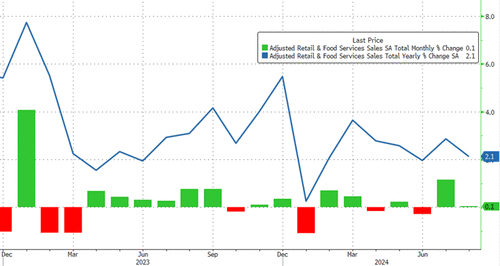

ZH: US Retail Sales Better-Than-Expected Thanks To Non-Store Retailers

,,,But.... just like in July, the headline retail sales print for August beat expectations, rising 0.1% MoM (with July revised up to +1.1% MoM) thanks to non-store retailers...

This slowed the YoY retail sales print to +2.1%...

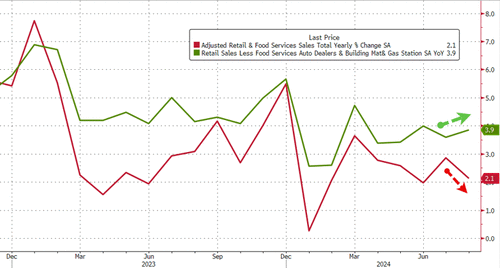

However, core retail sales (ex-Autos) rose just 0.1% MoM (less than the +0.2% expected), but the core YoY print rose to +3.9%...

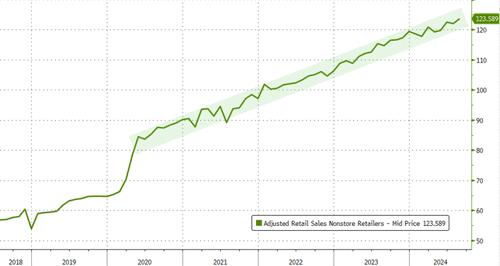

… on-Store Retailers hit a new record high...

Does anyone else think that line is just a little too linear for the real world?

Will any of this stop Powell and his pals from cutting rates by 50bps tomorrow? Of course not...

ZH: US Industrial Production Is Flat YoY In August, Despite Surge In Auto Production

… These points of light and data then set the table for a 20yr liquidity event…

ZH: Ugly, Tailing 20Y Auction Sends Yields To Session High

… Stopping at a high yield of 4.039%, the 20Y reopening yield was down from 4.16% in August, and even though this was the lowest 7Y yields since July 2023, it was the auction this month to still yield above 4% (thanks to the infamous 20s-30s kink, the 30Y trades at 3.96%). Notably, it also tailed the When Issued 4.019% by 2.0bps, the biggest tail since February's catastrophic - and record - 3.3bps tail, and followed 6 consecutive stop throughs.

The demand metrics were just as ugly: the bid to cover sank to 2.51 from 2.54, the lowest since February and naturally below the six-auction average of 2.68%. ..

… and so, here we are with only a couple / few hours to go before the Fed does / doesn’t deliver and so, someone surely to be let down by days end … For somewhat more on these ‘record wagers (and future let downs), scroll below and for now … here is a snapshot OF USTs as of 648a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: USD softer with fixed pressured pre-FOMC, US futures slightly firmer … Bonds are at lows, Gilts underperform following the region’s UK inflation report which saw Services & Core Y/Y print above expectations … USTs are lower and towards the bottom end of today's 115-06+ to 115-13+ parameters. All eyes are on the Fed. The odds of a 50bps cut are currently just above the 60% mark with just under a 40% chance of a 25bps move.

Opening Bell Daily: Fed Day. The world's fixated on the Fed’s first rate cut. Markets will react to something else entirely. Uncertainty runs high as the Fed gears up for its first policy cut in four years.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

By now you’ve likely heard or seen bobble heads on talking head TV refer TO this next SURVEY from America’s bank …

BAML Global Fund Manager Survey The Contrarian Play: Commodities

Bottom Line: global sentiment improves for 1st time since June on “Fed cuts = soft landing” optimism… cash level dips to 4.2%, BofA Bull & Bear Indicator dips to 5.4; but investors best described as “nervous bulls”… Sept FMS shows big rotation to bond sensitives (e.g. utilities OW highest since 2008) from cyclicals (e.g. commodity allocation @ 7-year low)… tactically Sept FMS says the bigger the Fed cut, the better for cyclicals …

… FMS on AA: equity OW unchanged (net 11%) but commodity allocation slumps to lowest since Jun'17 (Chart 1)

… On landings… FMS investor probability of a "soft landing" rose from 76% to 79%, while "no landing" dropped from 8% to 7% and "hard landing" from 13% to 11%.

… On monetary policy… 60% of FMS investors believe that global monetary policy is too restrictive, on par with levels last seen in the GFC and dotcom bubble.

… AND how ‘bout them ReSale TALES …

BARCAP: August retail sales: The 'totality' remains resilient

Retail sales increased 0.1% m/m, with strength at nonstore retailers helping to offset the drag from August's decline in auto sales. Today's data position consumer spending for another strong gain in Q3, which should help reassure an FOMC that is looking at the "totality of the data" that aggregate demand remains resilient.

Everyone how fully embracing the macro and some offering insights are worth a pause, point and click … this next one is such a note …

Market pricing is now leaning heavily towards the Fed cutting 50bp tomorrow. We think this is one of the few meetings where Fed policy will not validate the market; we still expect a 25bp cut.a

It's not clear that the Fed was behind last week's articles on their upcoming policy decision being a close call. It's also not obvious that the absence of Fed pushback to the stories and associated move in market pricing signals anything about the FOMC's leanings; while a significant hawkish surprise is unwelcome, re-steering expectations at this point is also not without costs. With the market now pricing ~42bp of cuts, or close to 70% of a 50bp cut, we no longer view the risk-reward to receiving the September FOMC as favorable and close the position out at a profit…

Here’s a note on how and why the 2yr yield dictates where the rest of the curve goes …

There’s a strong case to make that the money market curve should twist steepen if the FOMC cuts 50bp tomorrow, the underlying logic being that a more pre-emptive Committee reduces hard-landing risks and the likelihood of cutting through neutral…

… Paul Donovan chimes in … and seems that no matter WHAT we here on this side of the pond do, it’s never good enough …

Finally, several months later than it should, the Federal Reserve will cut rates today. Stressing data dependency when data are not dependable has led to this unnecessary delay. The Fed has been lucky the damage has been limited—middle-income borrowers locked in mortgages at absurdly low rates, and real rates for borrowers (deflated by income growth) have not risen too much.

Economists expect a quarter-point rate reduction—markets are less certain. This, with a clear signal of two further cuts this year, allows the Fed to follow inflation lower without signalling panic. We also get the fabled dot plots of FOMC members’ projections. These are misleading; the complexities of policy cannot be summarized in a few pixels on a chart…

… not sure what he’s advocating for — rules based policy so the rate then SHOULD be …? Anyways, moving along TO THE bank with the covered wagons …

Wells Fargo: Lost Swagger: Broad-Based Retail Weakness Despite Scant Gain

Summary The August retail sales report is the latest example of a choosy consumer continuing to spend even if the pace of growth is slowing sharply. Despite a big gain for ecommerce, broad-based declines across store types offer further confirmation of lost swagger in consumer spending.

Today, the Atlanta Fed's GDPNow tracking model raised Q3's real GDP growth rate to 3.0% (saar) from 2.5% following the release of solid retail sales and industrial production reports for August (chart). Leading the way was an upward revision in real consumer spending growth to a whopping 3.7% from 3.5%. The increase in real spending on capital equipment was raised to 11.6% from 10.8%.

Today's two reports, along with August's payroll employment gain, confirm that the Index of Coincident Economic Indicators (CEI) rose to yet another record high last month. The y/y growth rates of the CEI and real GDP are highly correlated, and both are rising at a solid pace (chart).

… 25? 50? ANYONES GUESS.

And from Global Wall Street inbox TO the WWW … heading in TO this afternoons FOMC meeting, this one written / sent before yesterday’s ReSale Tales data dropped …

Despite surveys showing that the consensus is expecting a soft landing, rates markets are pricing in a full-blown recession, see chart below.

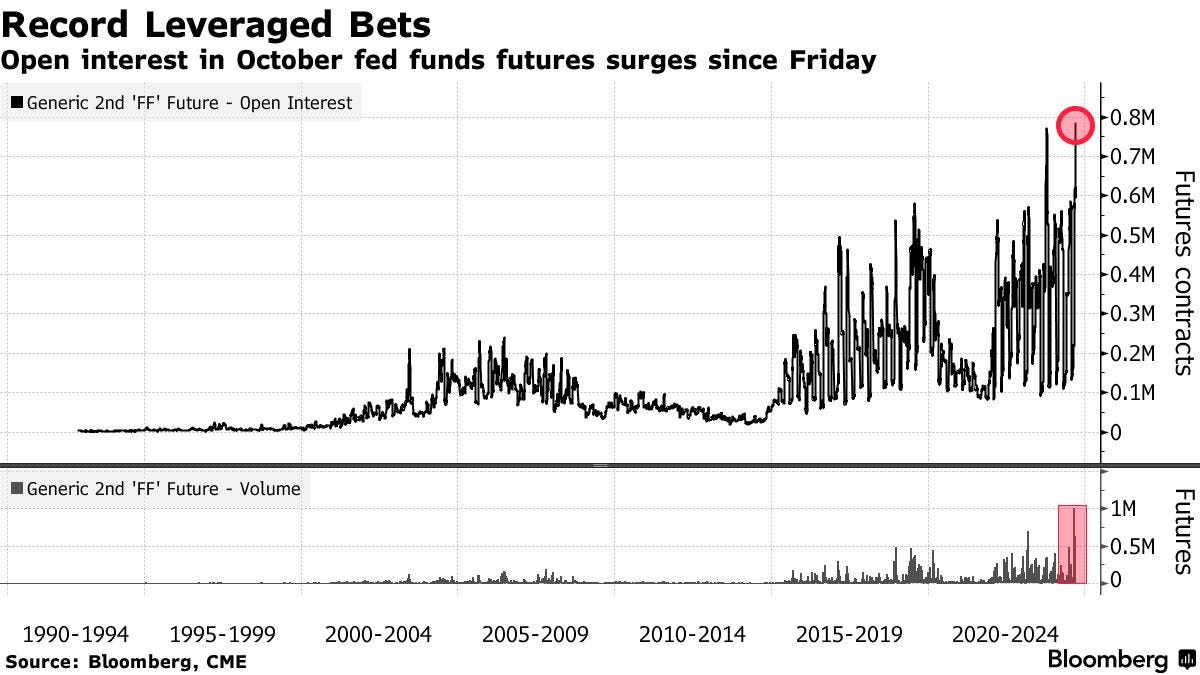

POSITIONS matter and none other than Bolingbroke to help one and all NOT go broke …

Bloomberg: Record Wagers on Fed Cuts at Risk If Powell Fails to Go Big

Bets on October fed funds futures top any activity since 1988

Positions will be upended if Fed only moves by a quarter point

… Activity in October fed funds futures, which investors are using to bet on this week’s policy meeting, has jumped to the most extreme level of any such contract since the derivative’s inception in 1988, according to data compiled by Bloomberg. The bulk of these new bets are targeting an outsized half-point cut, including a surge of positions put in place this week, the data show.

With the Fed set to begin lowering its target rate, debate among investors has centered on the size of the first cut and the scope of reductions.

and … a somewhat longer-term look and context TO recent new YTD lows for long bonds …

AND as far as those ReSale TALES go … to the Wolf…

WolfSt: Recession Not Yet: Retail Sales Help Push Up Atlanta Fed GDPNow to +3.0% for Q3 GDP

As retail sales rose despite dropping prices of goods, inflation-adjusted retail sales – adjusted for this deflation in goods – rose even faster: hence the jump in GDPNow.

Here we are … all at THAT crossroads or, as Yogi Berra once said … when you get to the fork in the road, TAKE IT … JPOW & Co are ‘bout to ‘take it’ …

… Feels like one of those moments in time when, if I had answers ahead of time, I still might not get the TRADE right and so … THAT is all for now. Off to the day job…

All this salivation begging for them CUTS seems like madness from my view, but I'm not levered up to the gills. I try to have empathy! Admittedly begging for deem CUTS has higher entertainment value than Dippin Dot Madness IMHO 😁

25

All this salivation begging for them CUTS seems like madness from my view, but I'm not levered up to the gills. I try to have empathy! Admittedly begging for deem CUTS has higher entertainment value than Dippin Dot Madness IMHO 😁