Good morning … quick note this morning ahead of the all important ‘flation data the Fed watches.

Overnight, it is being said that we are ‘GETTING CLOSER’ to a BoJ rate hike.

Bloomberg …

… Getting Closer Bank of Japan Board Member Hajime Takata sent a strong signal that the case for ending the negative interest rate policy is gaining momentum, comments that pushed the yen and government bond yields higher. “There are uncertainties for Japan’s economy but my view is that the price target is finally coming into sight,” Takata said in a speech to local business leaders in Shiga, western Japan Thursday. The comments will likely underpin speculation in the market that the bank is poised to conduct Japan’s first rate hike since 2007 in the coming months.

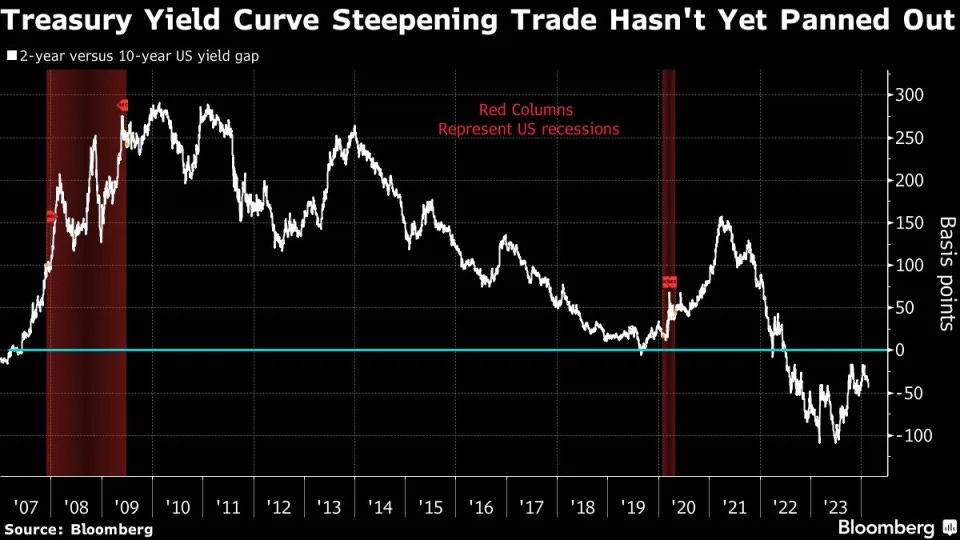

… For (somewhat)more, see (complete story / link) below but for now, how about that big bond bull steepener here in the USofA … it was to be THE trade of 2023 and again 2024 … how’s it going …

Bloomberg: The Big Bond Steepener Is Flopping as the Fed Delays Rate Cuts

Swaps traders now see first Fed cut most likely coming in June

Yield curve remains inverted; long-rates are lower than short

What was supposed to be the darling trade of 2024 has unraveled, thanks to the Federal Reserve upending predictions over how fast it would lower interest rates.

The market entered January aggressively betting on sharp rate cuts. By doing so, traders looked to profit from the US Treasury yield curve returning to a traditional upward slope, a transition known as a steepener. That would put longer-dated yields back above their short-term equivalents, reflecting the usual need to be compensated for risk over time.

Bill Gross, the co-founder of bond giant Pacific Investment Management Co., has been assuming such steepening would occur for nearly two years. When Goldman Sachs Asset Management rolled out its 2024 investment outlook, it declared the steepener, or the return to normality, the “easiest trade out there in rates.”

Such calls have backfired as short-term yields went even further above long-term ones as a resilient economy and sticky inflation led Fed officials to push back hard against market speculation cuts would begin in March…

A key measure of the shape of the yield curve is the spread between the rate on two-year Treasury notes versus those with ten years to maturity. At present, theshorter tenor is about 40 basis points higher than the longer — an inverted curve, in bond speak…

… For example: With a typical two-year and 10-year steepener trade, such carry costs amount to a loss of 40 basis points a year, assuming no other changes. This means an investor who initiated the trade a year ago and held onto it would have barely made any money, despite the fact the curve moved in the right direction and steepened about 50 basis points during the period.

So for the trade to work, Fed rate cuts have to come sooner than later, Ben Emons, a senior portfolio manager at Newedge Wealth, explained. “If there’s no rate cuts, steepening is just not going to happen. It’ll just fizzle out,” he said…

… “There’s really about no investment you can do right now betting on a return to normalcy that has positive carry,” Bhansali said. “And yeah, when the curve flattens you get hurt and you are paying annually about 50 basis points in carry, but it’s worth it. You just need to be able to hold it.”

A couple links and PRECAPS ahead of today’s more important Core PCE Deflator …

CalculatedRISK: Q4 GDP Growth Revised Down to 3.2% Annual Rate ZH: US GDP "Grew" $334 Billion In Q4.... That Growth Cost $834 Billion In Debt

… AND here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower ahead of PCE this morning and after BOJ Board member Takata said that spring wage momentum is picking up- lifting JGB yields and the yen. The flash readings in Europe's core inflation were firmer than expected as well. DXY is little changed while front WTI futures are modestly lower (-0.45%). Asian stocks were mixed (nice rebound in China's shares), EU and UK share markets are mixed (SX5E 0.00%) while ES futures are showing -0.2% here at 6:50am. Our overnight US rates flows saw little movement during Asian hours and little action during London's AM hours as Treasury 5's and 10's settled in at ~4.30% ahead of PCE. Overnight Treasury volume was unavailable today, sadly.

… This morning's PCE data could change things in a flash but... we have one idea that the wanting buyers might want to consider. Keep an eye on the reasonably well-formed bear trends in place this year where, if taken out, the breakouts should be a warning that the peak in this corrective(?) move to higher rates may be in and behind you. For example, we next show the weekly chart of Treasury 10yrs and how the opening/closing candles (red and green bodies) have been drifting upward in ~linear fashion since the start of this year. This steady grind upward is what corrections often look like (macro trend changes tend to start more slowly then accelerate) where a bullish breakout through/below the bearish rates uptrends might/should signal a renewed leg to lower yields….

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities mixed, Dollar weighed on by JPY, Bonds pressured on European CPIs ahead of US PCE … Bonds are pressured following the hotter-than-expected European CPI data …

Finviz (for everything else I might have overlooked …)

…before moving on from the news you can use, I wanted to make certain you did NOT miss the Timiraos story yesterday (which I stumbled on AFTER hitting SEND … it’s a feature on Waller — appointed by Trump — and who’s apotential to replace JPOW when his term expires in 2026 …

WSJ: The Fed Contrarian Who Saw the Soft Landing Coming Influence of Christopher Waller, a Trump appointee, rises as he challenges economic orthodoxy

Federal Reserve governor Christopher Waller laid out a novel economic framework two years ago showing how the central bank could bring inflation back to its 2% target without the usual jump in unemployment, stirring furious pushback from economic heavyweights.

Two years later, with inflation edging closer to 2% and unemployment still near a half-century low, Waller is looking prescient. It is one of the reasons the academic economist-turned-central banker is one of the Fed’s most closely watched officials and a name now floated to chair the Fed one day.

In recent years, Waller has been a hawk—a central banker who worries more about high inflation than high unemployment in setting interest rates. One of the reasons for this is a framework that gave him confidence inflation could be brought down without high unemployment, contrary to some standard economic theory.

His theory: In a hot labor market, tight monetary policy would lead employers to slow hiring by scrapping vacancies rather than by laying off employees they had worked so hard to hire.

At the time, in 2022, the Fed had just started raising rates rapidly from near zero after realizing inflation, contrary to its initial view, wasn’t transitory. Critics accused Waller of putting lipstick on a pig of policy mistakes.

His supporting research was rife with “misleading conclusions, errors, and factual mistakes,” wrote Lawrence Summers, a former Treasury secretary, and Olivier Blanchard, former chief economist at the International Monetary Fund, in an August 2022 essay that followed an earlier takedown of the work.

An extremely high 7% of jobs were vacant at the time. Summers and Blanchard showed how in every economic cycle since World War II, unemployment had risen notably two years after the job vacancy rate had peaked. Inflation wouldn’t get close to 2% without sustained higher unemployment, they and other critics said.

Yet since then the vacancy rate has declined to 5.4%, while the unemployment rate is no higher. Inflation fell to 2.6% in December from 7.1% in June 2022, using the Fed’s preferred price index.

In retrospect, the analysis by Waller and a fellow Fed economist “looks quite prescient,” said Jonathan Pingle, a former Fed economist who is now chief U.S. economist at UBS. He said wage growth would probably have to drop further to ensure 2% inflation, “but, wow, they have made a lot of progress in what they foretold.”

… A burst of demand greeted employers as the economy reopened from the pandemic in 2021. Pandemic disruptions meant they couldn’t find workers, so vacancies soared. Inside the Fed, Waller had begun pushing for an earlier exit to the central bank’s ultra-easy stimulus policies. While some colleagues worried that could upend the labor market, Waller argued demand for workers was so strong they wouldn’t have to worry.

Fed Chair Jerome Powell began publicly echoing that view in early 2022 as officials prepared to raise rates from near zero.

At lunch with Powell that spring, Blanchard pointed to the textbook Beveridge curve in dismissing the Fed’s rosy outlook. Staff briefings to senior Fed officials followed, including one by Andrew Figura, a Fed economist who specializes in labor dynamics, suggesting the Beveridge curve wasn’t stable.

… In an interview, Summers said, “Certainly, the data so far has run in Waller’s direction, but…we’re still some substantial distance from confidence that we have enduring, 2% inflation.”

In his speech last month, Waller also said his earlier framework argued for caution against keeping rates too high for too long. If the vacancy rate, instead of stabilizing, falls below 4.5%, unemployment would likely rise sharply, he said. While falling vacancies, as predicted, have yet to signal broader labor-market stress, Waller said, “We argued this couldn’t go on forever.”

… And NOW I’ll be just moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Over 2024 so far, there’s been a notable uptick in market expectations of near-term US inflation. For instance, the 2yr breakeven closed at 2.75% yesterday, which is the highest since last March. Bear in mind it had been at just 2.02% at the start of the year, so a decent jump.

Interestingly, if you strip out Covid, and the subsequent inflationary impact period up to the end of Q1 last year, 2yr breakevens are now at the highest level since before the GFC some 15 plus years ago. The recent spike accelerated with the strong January CPI print, with a +14.1bps increase that day. But alongside that, we’ve had continued good news on growth and the labour market, which has added to the sense that inflation could prove more persistent as demand remains strong. Gasoline prices have also shifted higher this year as well, after significant declines in Q4.

To be fair, the 10yr breakeven is at more “normal” levels, and closed at 2.32% yesterday which puts it back in the 2010-2014 range, albeit with Fed Funds now above 5% rather than zero back then. Nevertheless, 10yr breakevens don’t suggest there’s a longer-term concern for investors at the moment. But the short-term jump goes some way to explain why markets have shifted from pricing nearly 7 Fed rate cuts this year in mid-January to just over 3 now, and that might be why 10yr breakevens are better behaved as the market currently thinks the Fed will do what it takes to ensure long-term price stability.

Goldilocks: Immigration: Slower but Still Above Trend (think ‘bout this here for a bit … there are seasonal adjustments and BIRTH / DEATH rate stuff — personal fan fav — but now we’ve got to incorporate another factor into 'the model’ ?? check out the visuals and specifically one below … gosh what a coincidence in the timing of the increase, no?)

The immigration rebound that helped rebalance the tightest labor market in US history continued in 2023 but appears likely to moderate in 2024. The foreign-born labor force grew a rapid 110k/month in 2023—about 70k/month faster than in 2010-2019—but recently declined back to trend levels as the foreign-born participation rate fell.

Elevated visa issuance accounted for roughly half of the above-trend growth in immigration last year. Green card issuance and temporary work visas to new arrivals remained above pre-pandemic levels, with around 11k/month more of the former and 20k/month more of the latter in 2023 than 2019. However, total visa issuance was only about 20k/month (SA) above pre-pandemic levels in H2 (vs. 40k above in H1) and the immigrant visa backlog began rising for the first time under the Biden administration…

… Taken together, we estimate the foreign-born contribution to monthly labor force growth will moderate from 110k/month in 2023 to around 70-90k/month in 2024, still roughly 30-50k/month above the 2010-2019 contribution.

… CBO estimates that net immigration flows—particularly unauthorized immigration— surged in 2022 and 2023, will plateau in 2024, and then decline towards historical levels “as the immigration system adjusts.” They project net immigration was 3.3mn (275k/month) in 2023, much higher than the 2.3mn (190k/month) increase in the foreign-born population (from Dec. 2022 to Dec. 2023) measured by the Current Population Survey (CPS).4

USD exhibits broad strength; USTs bull-steepen, personal consumption revised; JGBs twist-steepen amid weak BoJ purchase operation result; Hacienda sales continue, CLP gains; RBNZ shows lower OCR projection, AUD/NZD rises; Fed's Logan remarks on QT; DXY at 103.92 (+0.1%); US 10y at 4.264% (-3.9bp).

… US Treasuries mildly bull-steepen, through an upward revision to 4Q23 US Personal Consumption, in a continuation of a countertrend mini-steepening within this month's broader flattening trend.

Yesterday’s US GDP revisions did not add much to investors’ stock of knowledge. The US consumer proved stronger than initially thought, as US consumers so often are. The market-based personal consumer expenditure deflator has slowed quite notably over recent quarters. What good old fashioned supply and demand is doing is creating a quite powerful disinflation story.

We get US consumer spending and the monthly expenditure deflator for January today. Weak retail sales have depressed expectations for overall spending, but of course there is more to consumer spending than what happens inside the shopping mall. Having fun may support spending. The deflator is expected to show more price increases—this is quite common in January as companies test what price changes they can get away with…

… Bringing in today’s data, we now estimate that the monthly data released tomorrow will show a 2.9% (2.87%) 12-month change in core PCE prices through January and 2.4% (2.42%) increase in headline PCE prices ---- both 12-month changes are only one basis point lower than prior to today’s release. Our projection for the January change in PCE is unaffected and we continue to expect headline PCE prices increased 35bp in January and core PCE prices increased 42bp.

…If there is an error the BLS would likely issue an errata Some clients have floated the idea that the BLS might adjust next month's CPI to correct any OER data that might have been off in January. We disagree. If there is a clear error then the BLS is likely to issue an errata rather than leaving incorrect data in the CPI history. Such corrections are done quite frequently (though usually for less visible series). That said, as of yet we have no indication that an error has occurred, and it is possible that none did occur. Odd macroeconomic data occurs all the time.

We have made no changes to our forecast, but note upside risks to OER We await further clarification from the BLS and at this point have made no change to our OER projection

UBS: Feeling hot hot hot: Trading a 'higher for longer' environment

XOP/XLU relative has traded in lockstep with US 10y real yields over the last 1y+

… Now, let's look at historical data. Since the New York Stock Exchange adopted the five-day trading week in late 1952, the S&P 500's average performance on the last trading day of February has been flat, with a median change of 0.00%. However, when the last trading day falls on Leap Day (February 29th), performance has been weaker. The S&P 500's median performance dips slightly to a decline of 0.13% compared to a small gain of 0.06% on the last trading day of non-leap year Februarys. Interestingly, the last trading day of February, regardless of being a leap year or not, has shown weakness in recent years, experiencing negative returns in each of the past nine years. Whether or not the pattern plays out this year remains to be seen, but even if it does, it would be a small price to pay for an extra day!

Bloomberg: BOJ Board Member Signals Exiting Negative Interest Rate Policy Is Closer

Says it would be fine to shift monetary policy gear lower

Reiterates BOJ pledge to keep policy settings accommodative

… “There are uncertainties for Japan’s economy but my view is that the price target is finally coming into sight,” Takata said in a speech to local business leaders in Shiga, western Japan Thursday. Japan is “at a juncture for a shift in the entrenched belief that wages and inflation won’t rise,” he said.

Takata added to that message during an afternoon press conference by telling reporters, “It’s fine to shift the gear one notch lower” for monetary policy to be consistent with economic conditions.

Takata also reiterated a message previously conveyed by Governor Kazuo Ueda and Deputy Governor Shinichi Uchida among others that even if the bank ends the negative rate, policy settings would remain accommodative.

“We wouldn’t just keep hiking over and over,” Takata said…

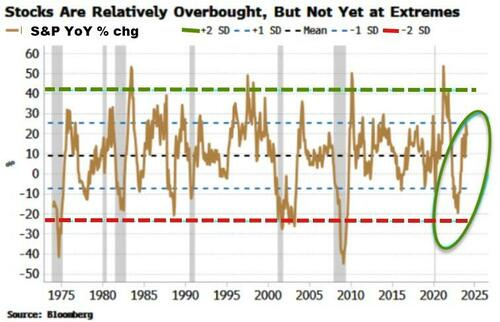

Bloomberg: Overbought Stock Markets Often Become Even More Overbought

… The S&P today is displaying signs of overboughtness. Annual returns in the index are mean reverting. The market recently reached its one-standard deviation line, but as the chart below shows it can become more overbought still. That’s especially the case when the market is bouncing from very oversold conditions, which the S&P 500 was in late 2022.

Don’t worry. This isn’t a post about how the 60/40 portfolio is “dead”. We talked about how that was nonsense last year and a 60/40 portfolio was up 20% last year right when everyone was declaring it dead. Instead, we’re going to talk about a new framework for thinking about any diversified multi-asset portfolio and where it does and does not make sense…

… The problem with a 60/40 portfolio is that it cannot give you near-term certainty since it’s structured as a long-term instrument. This is great for the patient investor and a behavioral mine field for the impatient investor. So you have to be aware of the sequence of return risk that any all stock or multi asset portfolio creates. Investors want two things from their portfolio:

Short-term certainty

High returns

The problem is that these two things create a temporal conundrum. It takes time to generate high returns because it takes time for businesses to grow and innovate. So there’s an inherent trade off in the way financial assets work. If you want high returns you need to own long-term assets. And if you want short-term certainty you need to own short-term assets. This is why diversification works. Diversification reduces volatility by reducing time horizons. This is the defining positive characteristic of a 60/40 portfolio. But you need to be aware of what you own because a 60/40 portfolio can go through extended drawdowns at time that will amplify cash flow uncertainty.

The easy solution to this is to know what you own and disaggregate your diversified portfolio as needed. If you need funds for the next 12 months then a bond allocation in the Bond Aggregate makes no sense because that’s a 5 year instrument that could expose you to cash flow uncertainty within 12 months. So, while the Bond Aggregate is great within the context of a longer-term portfolio like 60/40 it is not a sufficient cash flow instrument for anything shorter than 5 years. It could be totally appropriate to tear down the Bond Aggregate so you have a more tangible set of cash flows that are within the 40% component. This might include owning T-Bills or Money Market Funds, but you need to strip those pieces out of the aggregate in order to actually be able to obtain the cash flows and the certainty they give you over the short-term because the diversified 40% component will move like a 5 year instrument even though it might have lots of short-term instruments inside of it.2

In short, 60/40 is a wonderful portfolio for anyone with an intermediate or long-term time horizon of 5-15 years. But if you are expecting that portfolio to provide you with optimal short-term certainty then you are creating an asset/liability mismatch within your own financial plan that could result in significant behavioral risk.

1 – I’ve found that breaking this down into four specific buckets creates a very clear asset allocation approach that covers all potential time horizons an investor might have. This includes the 0-1 year bucket, 2-5 year bucket, 5-15 year bucket and 15+ year bucket.

2 – This could also create the opposite risk for more aggressive investors where the investor feels like they don’t own enough long-term assets at times. This is further reason to disaggregate the stock piece and own another complimentary slice of stocks outside of the 60/40.

FirstTRUST: Data Watch - Real GDP Growth in Q4 Was Revised Slightly Lower to a 3.2% Annual Rate

… In other news from yesterday, the M2 measure of money supply declined 0.2% in January and is down 2.0% from a year ago, and 4.2% lower than the peak in July 2022. Monetary policy operates with a lag, and we are likely to feel the negative economic effects of these declines in the year ahead.

Thanks for that, this seems relatively good news, although I'd like to know Waller's thoughts on retail CBDCs. If Goolsbee were to gain the FOMC chair Armageddon can't be far behind LOL

Thanks for that, this seems relatively good news, although I'd like to know Waller's thoughts on retail CBDCs. If Goolsbee were to gain the FOMC chair Armageddon can't be far behind LOL

Fantastic letter!!!

I have to read it 2 or 3 times,

to try an absorb all the information.