Good morning … out tomorrow due to travels, sorry for the inconvenience. Todays note / thoughts may then be longer than normal … market conditions, though, really NOT any sorta feeling of guilt. Well. Whatever … remember … Freedom isn’t free but this ‘Stack is, so please keep that in mind should you require any sort of prorated reFUNd.

And speaking of reFUNding (covered wagon preview below), while only 2s, 5s and 7s this week, a quick recap of 2yr auction …

ZH: Buyers Strike Arrives: Foreign Demand For 2Y Treasury Auction Craters To 2 Year Low

5yy: stability (resistance) in / around 3.90% for the moment …

… I’ll redraw TLINES at some point, when the facts change, one moves the goalposts, something something — the saying goes — meanwhile, momentum appears to be more noise than signal and yields finding some … stability … for now.

… that in mind, a look ahead to 7s since i’ll be outta pocket …

7yy: 4.13% is resistance …

… as momentum here, too, giving NO signal …

That’ll have to hold ya over ‘til Friday … AND a quick couple other items as the dust settled where we might have just witnessed the Trump Put excercised (again).

Trump sayin’ he’ll play nice in the Beijing sandbox, Bessent ALSO signaled de-escalation and Trump backs down from firing JPOW…

First, Bloomberg a short while ago …

April 23, 2025 at 12:55 AM UTC Bloomberg: Trump Floats Cutting China Tariffs ‘Substantially’ in Trade Deal

… “It will come down substantially but it won’t be zero,” Trump said Tuesday in Washington, following earlier comments from Treasury Secretary Scott Bessent that the standoff was unsustainable. Trump added that “we’re going to be very nice and they’re going to be very nice, and we’ll see what happens.” …

… sorry but … that smile … AND ‘bout intent with regards to JPOW …

ZH: Stocks & Bitcoin Pop, Gold Drops As Trump Says "Had No Intention Of Firing" Powell

Stocks surged into the green for the week, erasing yesterday's losses at 1200ET following this hopeful headline:

*BESSENT SEES DE-ESCALATION WITH CHINA, SITUATION UNSUSTAINABLE

The shortly after that, the following headline ruined the party:

*MAY TAKE MONTHS TO REACH FINAL TRADE DEALS: POLITICO

The White House trued to maintain some momentum and positivity:

*LEAVITT: BALL IS MOVING IN RIGHT DIRECTION WITH CHINA, DOING WELL ON POTENTIAL DEAL WITH CHINA

All the majors ended higher on the day, rallying all the way up to unchanged from Friday, but struggling to make any progress from there. Late-day gains lifted all the majors positive from Thursday's close... barely...

… Treasuries were mixed again today, flip-flopping from yesterday with the long-end outperforming today (versus the big lag yesterday). On the day, 2Y yields rose 4bps (after a weak auction) while 30Y yields fell 4bps. All yields are higher on the week now...

The yield curve (2s10s) flattened today, reversing most of yesterday's steepening...

… and oh, yea, there was the IMF (which nobody cares much ‘bout but …)

ZH: IMF Slashes Global GDP Forecasts, Warns Of Trade War Fallout For China, US

#Got5s? 7s? Want some? Get those bids in early and often and … here is a snapshot OF USTs as of 655a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Positive risk tone with stocks in the green, TSLA +6.5% after CEO Musk signals a step back from DOGE … USTs are bid with markets encouraged by two primary inputs. 1) optimism around the trade war following more upbeat comments from US President Trump overnight, reporting on Tuesday suggesting that Treasury Secretary Bessent sees the current levels of tariff on China as unsustainable and comms from the White House that it is nearing deals with China and India. 2) comments by US President Trump overnight that whilst we wishes for the Fed to lower rates, he is not looking to fire Powell. Focus now turns to US PMI, a slew of Fed speakers and 2yr FRN and 5yr auctions - as a reminder, Tuesday's 2yr outing was soft. Jun'25 contract has ventured as high as 111.00+ with the next resistance point coming from the 21st April peak at 111.09.

… The Administration’s sensitivity to the vote of no confidence provided by the stock market selloff seen in recent weeks has been less than we had anticipated. In general, the President tends to look toward the performance of equities as a barometer for investors’ read on policy moves.

This dynamic seems to be shifting and Trump appears to be comfortable with a certain degree of pushback on the trade war by investors via lower stock valuations. The quick succession of headlines since the Liberation Day tariffs were announced has only served to further complicate the process of estimating the ultimate impact on the real economy. Even setting aside the ever-increasing list of new levies, Trump’s decision to openly criticize Powell has been viewed as the equivalent of Julius Caesar pausing on the shore of the Rubicon River and tossing a stone to test the waters, as it were. There is still time to reverse course and downplay reports that the Administration is exploring ways to remove Powell, although de-escalating isn’t likely to be Trump’s preferred course of action. Instead, the absence of provocative social media posts might be the closest thing to an easing of tensions with Powell that the President can (or is willing to) deliver.

Risk assets certainly welcomed the reprieve. The conciliatory tone was also supported by reports from Washington DC that Bessent sees the standoff with China on tariffs as unsustainable and he expects the situation will improve. Bessent’s comments that the goal with China isn’t to decouple, rather to rebalance were also viewed as a net positive for the outlook on the trade war. At the risk of being too cynical, investors have become less willing to view the Treasury Secretary’s calming words as the ‘real’ agenda, only to have the President reverse or negate Bessent’s comments through a social media post. The White House press conference noted that there are now 18 proposals from other countries on trade – progress, without details…

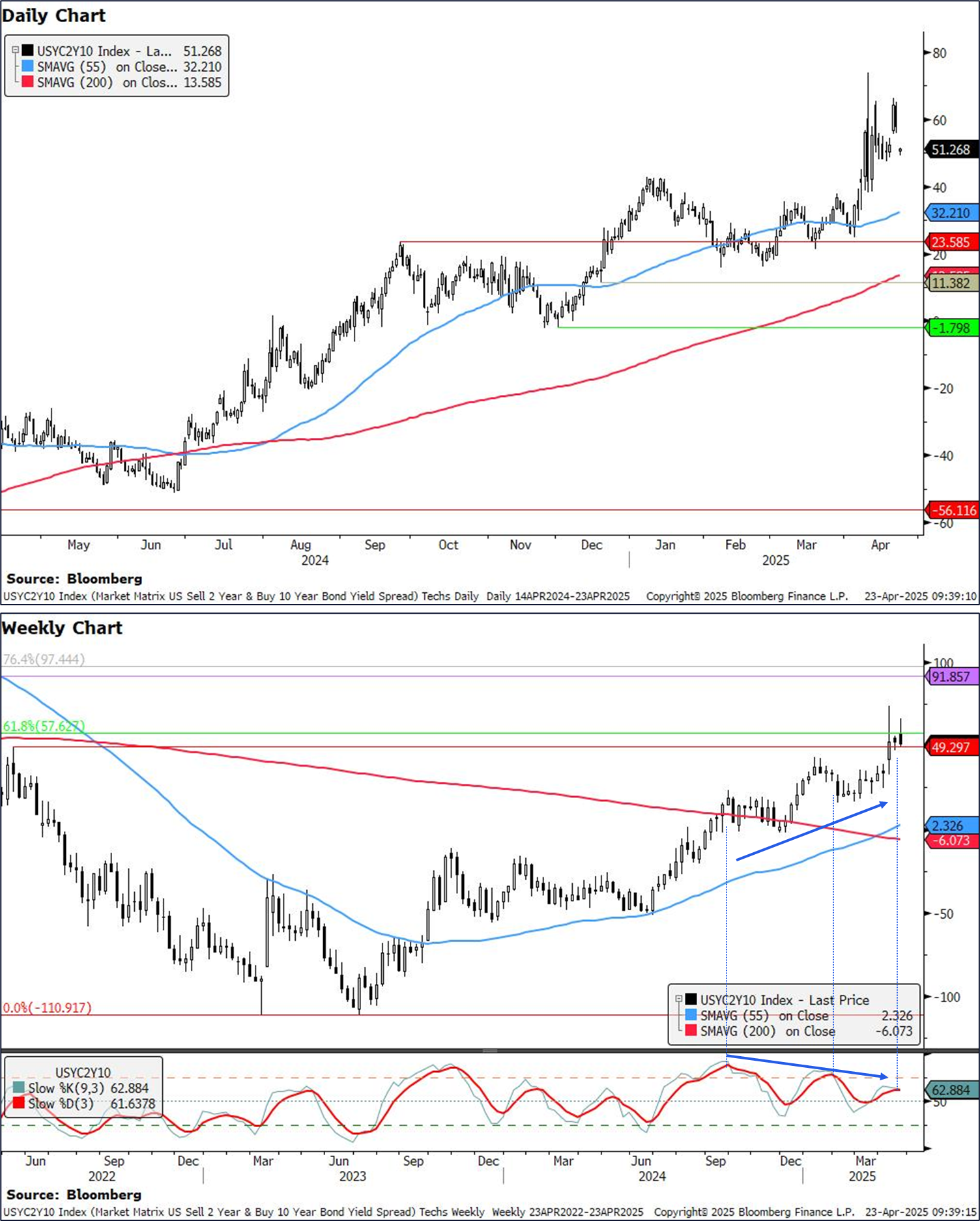

Here are a few words / an update of a techAmental variety … highlighting today’s auction item along with the curve …

The latest developments overnight (both around China talks, as well as Trump's comments around Powell) emphasize ideas that market pessimism may be overdone. Current steep yield curves, as well as tech indicators suggesting trend exhaustion, suggest that there could be an opportunity to fade steepening moves. Elsewhere, resistance levels in US yields continue to hold as well…

…US 5y yields US 5y yields are ticking higher. However, we expect the key resistance to hold at 4.14% (55w MA), which we failed to close above on a weekly basis over the last two weeks.

We think that a move higher looks limited in the short term at least. We support at 3.82% (October 16 low), followed by 3.38-3.39% (2024 low, 200w MA).

…US 2s10s With curves steepening sharply, our traders had already discussed that the steep yield curve presents potential opportunities for investors to fade the move.

In techs, we also see a strong signal for a potential flattening bias. We have held below the 57.63 level (61.8% Fibonacci) on a weekly basis twice now. We are also on track to post an inverted hammer weekly candlestick. More importantly, we are coming close to posting triple momentum divergence with the weekly slow stochastics as well. This is one of our favorite indicators of trend exhaustion.

This suggests that we could see a short term flattening bias. We think if we see 2s10s back towards the ~70 levels, it could be a good area to fade the steepening move.

On one of the more funTERtaining days in recent memory and here are a couple notes / thoughts from Germany after the day that was …

… Markets have started to sync up much more positively over the last 24 hours after Easter Monday's fraught US session (S&P 500 -2.36%) when fears of Powell being replaced by Trump dominated. Yesterday was already seeing most of those losses erased before markets powered past them just after Europe went home as Treasury Secretary Bessent suggested at a private event that the stand-off with China was unsustainable and that he expects de-escalation. The S&P 500 closed +2.51% higher with the strongest performance since the 90-day tariff extension was announced on April 9th. Elsewhere the Dollar index (+0.65%), US HY (-15bps) and 30yr USTs (-2.5bps) also rallied…

…An even bigger story for markets after the close was Trump’s comments that he has “no intention of firing” Fed Chair Powell, which has helped the rally continue. Equity futures on the S&P 500 and NASDAQ are trading +1.43% and +1.65% higher as I type. The 10yr Treasury yield is -5.3bps lower at 4.35% after a modest -0.9bp move on Tuesday, while the dollar index is another +0.40% higher. The Hang Seng (+2.40%) is leading gains in Asia, stretching its gains to a third consecutive session with the Nikkei (+2.04%), the KOSPI (+1.56%) and the S&P/ASX 200 (+1.48%) also among the top performers. Meanwhile, mainland Chinese stocks are far more muted with the CSI (+0.24%) and the Shanghai Composite (+0.05%) only just above flat…

…US Treasuries were another asset that unwound the previous day’s move, with a notable curve flattening as investors grew a bit more optimistic on the US outlook and took out some of the risk premium they’d been assigning to long-end Treasuries over recent days. The 30yr yield (-2.5bps) fell back to 4.88%, moving off from its 3-month high on Monday, with the 30yr real yield down by a larger -4.8bps to 2.63%. By contrast, the 2yr yield (+5.5bps) moved up to 3.82% following the risk-on tone as well as a soft 2yr auction…

23 April 2025 DBDaily: Bessent: China trade war "unsustainable"

…US equities were stronger Tuesday, S&P up 2.5%. US10yr yields down 1bp to 4.40%. Helping sentiment: press reports that US Treasury Secretary Bessent indicated to an investor summit that he expects the trade tension with China to de-escalate and that a trade war with China was "unsustainable". The USD index rose a little under 1%, gold fell about 2%.

Fed's Kashkari: Seeing "sharpest fall in confidence since March 2020", tariffs are "at least somewhat inflationary". Fed's Barkin: inflation expectations "may have loosened" …

… Amid a spike in some measures of US inflation expectations - most notably the Michigan consumer survey - Fed officials have taken comfort in the more sanguine signal from market-based measures. But Matt Luzzetti thinks this signal should also be treated cautiously because of sensitivity to equities and spot oil prices. The Fed staff's common inflation expectations index should be attracting more analytical weight.

Overall, changes in 5s10s term premium across G10 countries since 1 April have been broadly in-line with history rather than pointing to a flight from the US driving non-US TP down. But Germany, Switzerland, and Japan stand out, suggesting these countries may be benefiting from actual or expected portfolio reallocation and a strengthening in safe-haven demand. Francis Yared with the details…

23 April 2025 DB: Mapping Markets: How far are markets actually pricing in a recession?

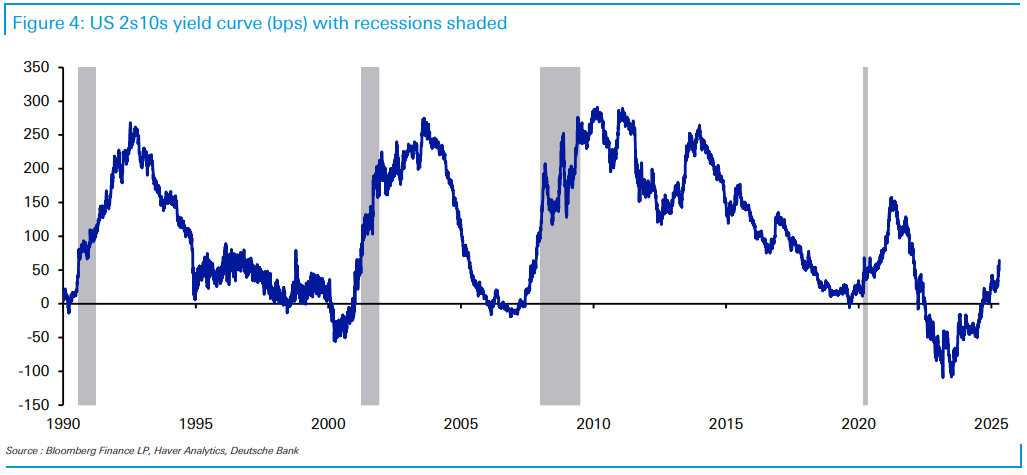

Since the Liberation Day tariffs, investors have rapidly reassessed the likelihood of a US recession. Equities saw one of their fastest declines since WWII, and we’ve also seen wider credit spreads, steeper yield curves and lower oil prices.

But despite those moves, it’s clear that investors aren’t fully pricing a recession in just yet. After all, the equity declines have been shallower than recent recessions, as have the widening in credit spreads and the declines in oil prices.

So markets clearly don’t see a recession as inevitable, particularly if the tariffs don’t come into force after the latest 90-day extension. But of course, the flip side is that with markets not fully pricing in a recession, that opens significant downside risks if we do get one, as none of the major asset classes have seen moves consistent with the other recessions of recent history.

…Credit: Spread widening well beneath levels seen in previous recessions…

…Oil prices: Decline not on the scale of recent recessions (excluding recessions like 1973 or 1990 where higher oil prices directly contributed to the recession)…

…Rates: More ambiguous signals, as curves normally steepen into a recession and we're seeing that today. But then again, this steepening has been ongoing since mid-2023 as the soft landing became more likely…

…As such, the hard data over the coming days will be crucial. Investors have been reluctant to fully price in a recession because we don't have enough evidence that one is likely. But if that changes and we start to see contractionary numbers (e.g. a negative payrolls print), that would lead to a fresh reassessment that could open the way for a fresh selloff. That risk is particularly acute precisely because markets haven't witnessed a recession-like selloff so far. So history clearly demonstrates that if we did get an actual recession, then there's still a lot of scope for risk assets to see further downside.

Same German operation with some thoughts common inflation expectations …

22 April 2025 DB: Why CIE-ing may not be believing with market inflation expectations

Although some measures of inflation expectations have lurched higher, Fed officials have taken comfort in the more sanguine signal from market-based measures of inflation expectations. In this short note we discuss reasons this signal should be treated cautiously, including excess sensitivity of these market measures with equities and spot oil prices.

This analysis suggests a more holistic approach is needed, such as the Fed staff's CIE (common inflation expectations) index, and that alternative survey-based measures should receive some additional weight in monetary policy decisions (e.g., NY Fed consumer survey and Survey of Professional Forecasters). We provided an update of the CIE in our recent outlook report (see Tariff-struck).

I thought a new video game was comin’ out when I saw this next note hit the inbox (guessing that was the point…)

April 22, 2025 MS: Global Tariffs: Call of Duties — Past, Present, and Future

This note focuses on the big picture context of tariffs, marks to market the current situation, and begins to outline global sensitivities to the recent tariffs. Three sections encompass the past, present, and future, followed by a summary of tariff basics.

…(1) The Smoot-Hawley tariff of 1930 compares most closely to the tariffs announced on April 2, 2025. During the Hoover administration, the Tariff Act of 1930 increased tariffs from ~13% to ~20%. The overarching experience of Smoot-Hawley was that trade collapsed by over 50% and US tax revenues fell for three years after the implementation of the tariff. The Reciprocal Tariff Act of 1934, passed early in the Roosevelt administration, reversed Smoot-Hawley by giving the president the power to lower tariffs. Average tariffs fell from ~20% to ~10% before World War II.

(2) The introduction of GATT (General Agreement on Trade and Tariffs) after World War II catalyzed the shift toward free trade by providing a baseline to organize global tariffs. The watershed moment in global free trade came with the Uruguay Rounds, conducted between 1986 and 1994, where both developed and emerging economies agreed a basis for tariff-free (or -reduced) trade. Following the Uruguay Rounds, the World Trade Organization (WTO) was created in 1995. Many argue it was China's participation in the WTO in 2001 that catalyzed that country's manufacturing revolution.

(3) The first Trump administration's use of Sections 201, 232, and 301 of the Tariff Act of 1962 to impose broad-based tariffs on China (and proposed against Mexico) in 2018 will likely be historically viewed as an inflection point. It provides a benchmark to frame current tariff orders and negotiations.

…Exhibit 68shows the sensitivity in value add at a country level. Remember, value add is not specifically measured in the same way as GDP but the two are linked. Again, we emphasize that the results should be read directionally. It is not surprising that China is the most impacted given the tariff focus. What is perhaps interesting is the countries that follow because of their secondary impact due to supply chain exposure to China. While the results are intuitive, quantifying the risk is notable. Outside of Asia, there are a number of European economies given their trade orientation and exposure to global supply chains.

The Art of the Deal, they said. It’s gonna be great, they said …

With investor concerns growing, US President Trump demonstrated the art of the retreat. They stated they had “no intention” of firing Federal Reserve Chair Powell. Trump may not be able to (legally), but markets will still have lingering concerns about Fed independence. Trump also said they would be “very nice” in any trade negotiations with China, raising hopes that the tax burden on US consumer may lessen.

Markets reacted positively to these retreats, which signal that the coming US economic slowdown plus market moves may limit extreme policy positions. Nonetheless, the erratic threaten-retreat-threaten-retreat cycle has economic consequences. The uncertainty this causes may impact consumer and business decision-making.

The Fed’s Beige Book is likely to pick up some of this uncertainty. This is based off anecdotal evidence, which is subject to bias—businesses know their comments are heard by policy-makers, and may exaggerate their reported views to try to sway policy. Nonetheless, the comments will be looked at for signs of the impact of erratic administration policies, and the potential for second-round inflation effects from trade taxes.

No fewer than 14 central bankers are jostling for media attention today—the Bank of England’s Bailey and Pill may get attention as markets speculate on the speed of policy easing.

April 22, 2025 Wells Fargo: Treasury Refunding Preview

Summary

We do not expect any major policy shifts at the upcoming quarterly refunding announcement from the U.S. Treasury. In our view, existing gross coupon auction sizes are raising enough money that changes are unlikely to be announced until the January 2026 refunding.

Our forecast for the federal budget deficit in fiscal year (FY) 2025 is $1.70 trillion. If realized, this would be a modest narrowing from the $1.83 trillion budget deficit recorded in FY 2024. Robust spring tax collections and an anticipated increase in tariff revenues are the main factors driving the near-term deficit narrowing in our forecast.

We expect the federal budget deficit to widen to $2.0 trillion in FY 2026 as the result of a weaker U.S. economy, structural growth in federal spending and new tax cuts.

We look for the Federal Reserve's quantitative tightening (QT) to run at its current pace through the end of the year and then cease. The era of QT putting additional pressure on Treasury's auction sizes is slowly coming to a close, and this will help delay the next round of coupon auction size increases.

We are shifting our debt ceiling "X date" forecast from early August to early September. There is still considerable X date uncertainty given the clouded outlook for the U.S. economy and trade/fiscal policy. A more pessimistic scenario would place the X date toward the end of July, while a more optimistic outcome could push the X date into October.

Once the debt ceiling has been lifted, net T-bill supply will surge as Treasury replenishes its cash balance and resumes normal operations. We project net T-bill supply will total a bit more than $500 billion over the second half of the year.

That said, it is important to remember that this surge in supply will reverse the reduction in Treasury bills outstanding that took place in the first half of the year. On an annual basis, we expect net T-bill supply to be roughly flat for the year.

Finally, one mans trash is anothers treasure?

Apr 22, 2025 Yardeni: Is The Dollar As Weak As They Say?

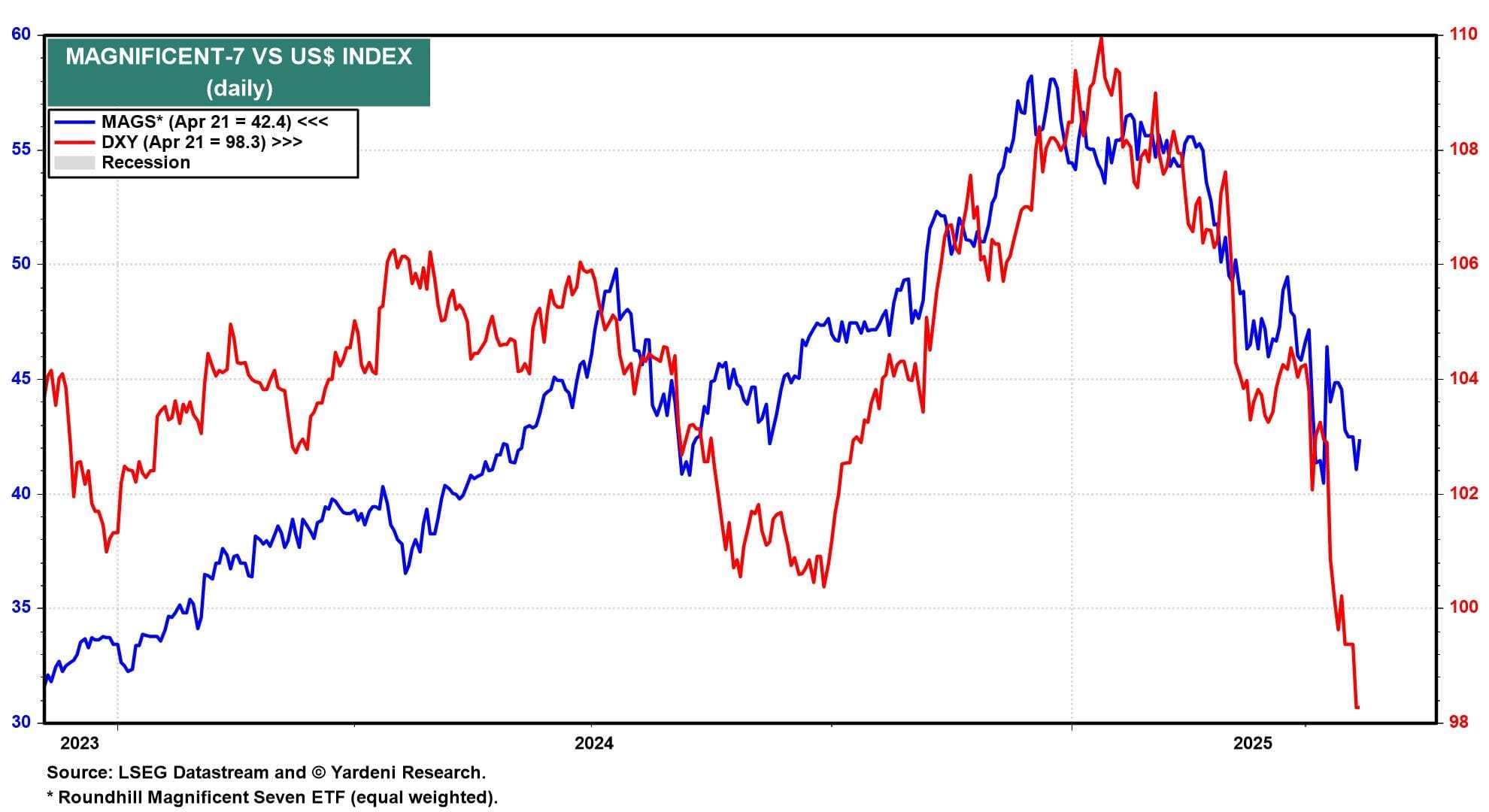

The US Dollar Index (DXY) is down 8.8% since the start of this year (chart). That has sparked lots of angst, the worry being that this might be just the beginning of a secular decline in the dollar because the US seems to be on course to decouple from the global trading system and become more self-sufficient. If Washington's policies reduce America's trade deficit, there will be fewer dollars for foreigners to invest. That could cause bond yields to soar in the US, possibly triggering a debt crisis if nothing is done to narrow the federal government's budget deficits. In this narrative, the dollar will increasingly lose its reserve currency status. The US is just the latest in a string of historic empires that have seen their currencies fall along with their global power.

Sorry, we aren't buying the latest eulogy for the United States and its currency. DXY remains on an upward trend that started around 2010, when it became increasingly obvious that the US recovered from the Great Financial Crisis better than the other major economies and financial systems (chart). The US capital markets remain the biggest and most liquid in the world. That's not going to change anytime soon.

The recent weakness in the dollar is mostly attributable to the selloff in the Magnificent-7 stocks, in our opinion (chart).

Foreign investors plowed a record $475.3 billion into the US stock market over the 12 months through February (chart). Undoubtedly, lots of those funds were spent on the Magnificent-7 at their record valuation multiples at the start of this year. Trump's Tariff Turmoil unnerved foreign investors (along with domestic investors). As a result, foreigners reversed course and bailed out of US stocks, especially the Magnificent-7.

…The Fed disaggregates its broad dollar index to show the foreign exchange value of the dollar relative to the currencies of advanced economies and emerging market ones (chart). The dollar has been mostly moving sideways relative to the former for the past couple of years, while soaring to new highs relative to the latter.

We conclude that the recent weakness in DXY mostly reflects the strength in the euro, which we don't think is sustainable. A strong euro could very well push the Eurozone into a recession, forcing the European Central Bank to continue lowering interest rates while the Fed remains slow to do the same.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

A couple from the terminal — on positions AND on Kevin Warsh vs JPOW … an OpED …

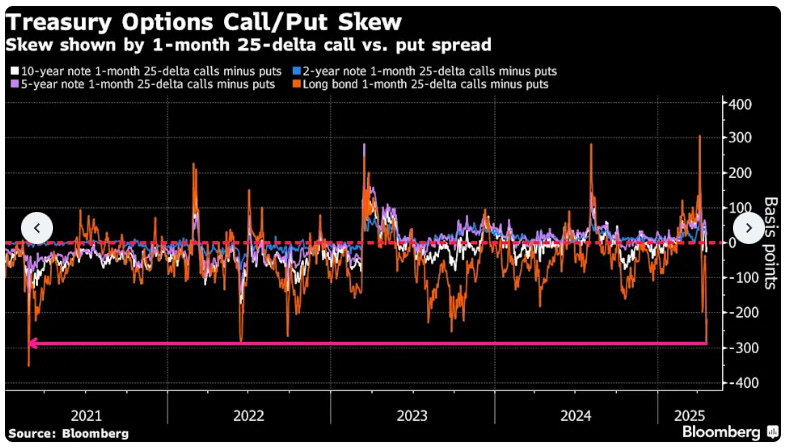

April 22, 2025 at 8:30 PM UTC Bloomberg: Treasury Options Show Biggest Worries Since 2021 ‘Flash Crash’ By Edward Bolingbroke

The growing unease around US assets that has sparked a selloff in long-term government bonds and sent yields soaring is showing up in the options market, where premiums to protect against even bigger losses are at their highest since the “flash crash” of 2021.

The so-called option skew on Treasury bonds has blown out considerably, with investors aggressively driving up the price of puts that hedge against the risk of a yield spike relative to call options that would profit from the opposite. The last time the skew was favoring puts this much was Feb. 25, 2021 — the day of an unusual “flash” event in US Treasury markets that featured a sudden drop in prices amid strained liquidity conditions.

The extreme positioning reflects a deepening angst among many investors, whose confidence in US assets has been shaken by concerns over the potential economic and market fallout from US President Donald Trump’s aggressive trade policies and his increasing pressure on the Federal Reserve Chair Jerome Powell to cut interest rates. Meanwhile, the US fiscal outlook remains challenging, leading traders to demand more compensation for the risk of owning long-term Treasuries. That can be seen in the rise in so-called term premium…

April 23, 2025 at 5:00 AM UTC Bloomberg: We Need to Talk About Kevin (and Jerome) Powell survives, there’s an obvious successor, and Trump’s drama was pointless.

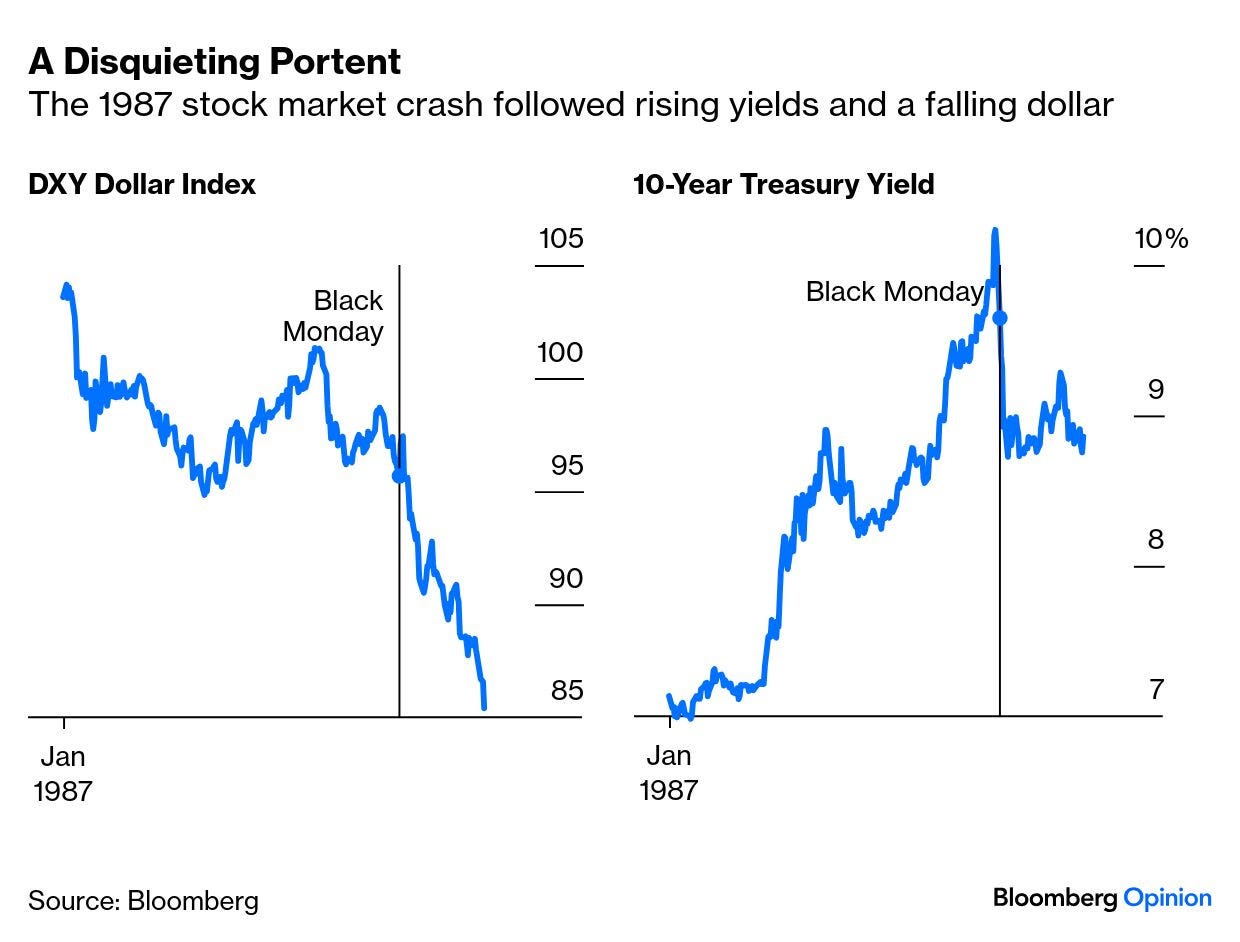

… One final concern is the way that this selloff has happened. Away from the stock market, there’s been a rare combination of rising bond yields and a falling dollar. As higher yields generally attract money into a currency, that’s a bad sign that confidence is dwindling, and it can signal trouble for equities. For a potent example, one reader pointed that the great Black Monday crash of 1987 was preceded by just that combination:

If the divergence persists much further, it will provide more evidence that investors really do require a bigger risk premium to invest in Treasuries. But overall, Parker’s arguments are well taken. There’s good reason to fear that the policy missteps of the last few months have ended US exceptionalism, but it’s way too soon to be sure…

One of the brightest bulbs who’s only just begun to shine … a young version of Dr. Lacy Hunt in some ways …

Apr 22, 2025 EPB Research: How to Improve Building Permits as a Leading Indicator Learn how a sequential Business Cycle process can turn building permits into one of the most reliable early warning signals for the economy.

New residential building permits are one of the best leading indicators of recessions. With a sequential Business Cycle process, as we’ve outlined in our last several posts, you can make them even better.

Building permits are a powerful early warning tool because they mark one of the first steps in the residential construction process. Residential construction plays a critical role in the Business Cycle.

If you can get an early lead on changes in residential construction, you can anticipate broader economic shifts before they happen. When building permits decline sharply, it signals an upcoming fall in construction activity — and eventually, a decline in residential construction employment.

Since 1962, building permits have declined more than 10% from their 24-month peak 340 times. In those cases, about 44% of the time, a recession was either already underway or occurred within the following 18 months.

(It's important to note: housing-related cycles can have long lead times.)…

AND … question EVERYTHING …

April 22, 2025 LPL: Treasury Market Haven Status Is Safe...For Now

Over the five trading sessions during the week of April 7, intermediate to longer-term Treasury yields were sharply higher in one of the largest moves higher in yields since 2020. Moreover, U.S. Treasury markets have sharply underperformed other developed government bond markets recently, calling into question the relative attractiveness of U.S. Treasury securities. However, despite recent volatility, U.S. Treasuries remain the world’s preeminent safe-haven asset (for now), in our view, underpinned by the dollar’s global reserve status (for now) and the market’s depth and liquidity. This month’s Treasury market sell-off, while severe, does not signal a "regime shift" away from this status, as some have suggested. Instead, we believe it mostly reflects temporary deleveraging pressures rather than a fundamental rejection of Treasuries’ safety, although there is no doubt foreign selling out of U.S. dollar assets has occurred and added to market volatility. Throw in concerns about Federal Reserve independence and potentially an unforced policy error by cutting rates too soon, and it makes sense longer maturity Treasury yields have continued to move higher. But if the U.S. economy does contract (and especially if it takes other economies with it), we think the U.S. bond market will remain the haven destination due to its size and liquidity.

U.S. Treasuries Have Significantly Underperformed Global (ex U.S.) Government Bond Markets Recently

Ratio of the Bloomberg Treasury Index to the Bloomberg Global Treasury ex U.S. Index

…Alternatives and Their Limitations

German Bunds. While highly rated, the German bond market is significantly smaller (approximately €2.4 trillion total) and less liquid. China’s $760 billion of U.S. Treasuries, for example, only represents approximately 3% of Treasury debt outstanding, whereas a similar amount invested in Bunds would represent approximately 28% of Bunds outstanding.

Japanese Government Bonds (JGBs). JGBs suffer from low but increasing yields and Japan’s high debt-to-GDP ratio, raising long-term solvency concerns. Their market is also less accessible to foreign investors.

Chinese Government Bonds. Despite China’s economic size, its bond market lacks transparency, faces currency convertibility restrictions, and carries geopolitical risks, making it an unsuitable haven.

Gold. While a traditional safe-haven, gold lacks income generation and faces storage and transaction costs, limiting its scalability for institutional investors. However, the move into gold recently likely, at least partly, reflects central banks diversifying their reserve assets.

Cryptocurrencies. Digital assets like Bitcoin are highly volatile and lack the stability or institutional acceptance needed to rival Treasuries. Once markets develop more depth, these types of securities could also be used to diversify away from Treasuries — just not yet, though, in our view.

Why This Time Could Be Different Though

That said, there is a specific risk to Treasury markets with respect to foreign demand for U.S. Treasuries. If the stated goal by the Trump administration is to truly reduce or eliminate trade deficits (remember one country’s trade deficit is another country’s trade surplus), that would likely mean a big loss of demand from foreign buyers. Foreign investors own roughly $8.5 trillion of the $26 trillion in marketable Treasury debt outstanding, with roughly half of that due to trade surpluses. Most countries use the dollar inflows from trade surpluses to invest in U.S. Treasuries (along with other U.S. assets). No trade surplus means no excess dollars, which means less demand for Treasuries. While we don’t think foreign investors are boycotting Treasuries currently, it does represent a big risk to the Treasury market, especially if a viable alternative can be found. However, further supporting the argument that foreign buyers haven’t yet boycotted Treasury markets altogether was the phenomenal demand — from both domestic and foreign investors — for the recent 10-year and 30-year U.S. Treasury auctions and the lackluster demand for the recent 5-year German Bund and Japanese Government Bond auctions. This was further confirmed with the recent Treasury International Capital (TIC) data that showed foreign investment in U.S. bonds picked up in February (the latest data available). This week’s $183 billion (total) in Treasury auctions will be important to watch for continued foreign demand. So far anyway, investors continue to prefer U.S. Treasury securities.

Non-Domestic/Foreign Investors Are an Important Buyer of Treasuries

{kind=link}