Good morning … I got nothing. I’m exhausted. Vol is back, Global Wall having a chance daily to change narratives and update models and calls and it seems to me there’s plenty of NOISE burying the signal…Here’s some signal:

Unfortunately, the source — Goldilocks — where I stumbled across this was randomly on LinkedIN and rest assured, if / when I come across the full note, I’ll pass it along. For now, though, the recent selloff in grander context, certainly doesn’t seem so bad AND, looking at rates back TO the 1700s makes them look like they are currently at / near levels they should HOLD … for whatever reason.

Perhaps one such reason will be this mornings noisy NFP. For now, some of the NOISE amidst the signal and ahead of payrolls, it’s worth noting how just yesterday, markets collectively paused …

ZH: 'Sell All The Things' - Markets Stall Ahead Of 'Most Important Jobs Print... Since The Last One'

… and that is OK. A couple of visuals and comments from ZH DO offer reason to pause and (re)read …

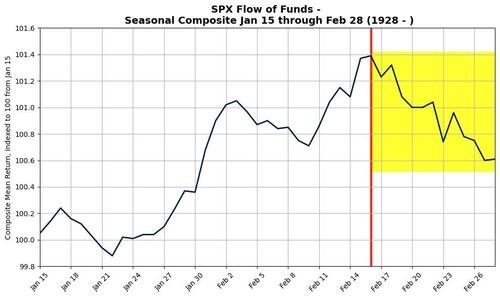

… bear in mind that the second half of February is 'seasonally; weak...

Source: Goldman Sachs

...and the spread between the S&P 500’s forward earnings yield and the 10-year Treasury yield has reached a 23-year low

Source: Bloomberg

Probably nothing!!

Speaking of prolly nuthin …

BoE rate CUT, anyone?? Hawkish as it were …

ZH: Pound Tumbles After Bank of England Cuts Rates While Warning Of Mounting Stagflation; Two Officials Vote For Bigger Cut

… always found IJC ahead of NFP to be relatively useless …

ZH: Initial Jobless Claims Tick Higher Off Multi-Decade Lows

AND, i’ll just quit while I’m behind and stop wasting MORE of your time … big day, recaps and victory laps to follow as everyone weeds through Jan revisionist history noise lookin for signals …

… here is a snapshot OF USTs as of 654a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: US Market Open: Stocks and bonds trade tentatively ahead of US NFP and ECB Natural Interest Rate; AMZN -2.6% on weak guidance … USTs are flat and are awaiting today's US NFP report, as well as the benchmark payroll revisions. Firstly, the pace of payroll additions is expected to ease towards recent averages with consensus looking for 170k; though, hurricane, wildfire, cold weather and industrial factors could all impact and weigh on the headline. Into the release, USTs hold in a particularly narrow 109-13+ to 109-20 band with yields mixed and the curve itself a touch flatter.

Opening Bell Daily: January jobs moving stocks … How the January jobs report could make or break stocks … Economists don't expect much change in unemployment or new jobs.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

First up, ahead of the payroll data, a CPI precap …

We forecast January core CPI increased 0.30% m/m amid payback from the soft December prints, and headline CPI increased 0.38% SA (2.9% y/y). We estimate the NSA index at 317.471. Separately, we expect only minor revisions to the past years' SA data, and modest updates to category weights.

Same shop on stocks …

BARCAP: U.S. Equity Strategy: Food for Thought: Miss and a Swing

After downward revisions into the print lowered the bar for beats, stocks have sold off harder than usual in response to EPS misses this reporting season, despite the misses being of average magnitude. Next-quarter estimates are already taking a hit.

Best in biz with an honest confession ahead of NFP …

…. Headline payrolls will be a wildcard, as is so often the case, but the recent outperformance of the series versus forecasts makes it difficult to expect that this will finally be the month in which the labor market buckles under the weight of Powell’s ongoing restrictive policy bias. For context, three of the last four reports have seen headline payrolls surprise on the upside with the October series disappointing due to the hurricane impact…

…In contemplating the recent price action, the most striking aspect is the flattening of the yield curve. 2s/10s dropped to 20.6 bp – through the 50-day moving-average. Our bias is for further steepening from current levels, if for no other reason than such a move would be consistent with a supply concession. The recent uptick in volatility surrounding key macro events implies that Friday will see choppy price action and potentially better placement to enter a 2s/10s steepener – although we’ve already added at 23 bp and 35 bp, leaving us in the steepener, and nervous…

This next CPI precap wraps in TARIFFS …

BNP US: Brace for second-round effects of tariffs on CPI

KEY MESSAGES

We reiterate our long-held view that US tariffs will materialize in size and have a significant impact on domestic prices.

We expect US tariffs to produce persistent second-round effects on US inflation.

We use a structural vector autoregression (SVAR) model to help quantify the magnitude and duration of those effects. The model suggests that a 1pp import price shock has a persistent impact on prices and adds around 0.40pp to CPI over a two-year period.

Looking forward to 830a THEN 4p, the end of the week is finally in sight …

ING Rates Spark: Bessent and payrolls key as we end a tumultuous week

What a week! Tariff threats switched on and off, Bessent laser focussed on the 10yr yield, and next up is payrolls Friday. Meanwhile, a 25bp cut by the Bank of England safely delivered, and a dovish aftertaste, supports three more 25bp cuts this year. The ECB will publish a report on the neutral rate – potentially interesting. Lots to chew on over the weekend

Same shop offers a note on FX but its title was reason to pause and investigate…

The dollar faces downside risks today as US payrolls should slow and annual benchmark revisions could be significant. That could more than offset some safe-haven flows on the back of souring China sentiment. In the eurozone, we’ll watch the ECB’s new estimate for the neutral rate. Central banks in CEE maintain a hawkish tone but rates diverge

This next note would seem to address a topic from a Captain Obvious point of view …

The MSBCI moved lower in January. Services growth slowed while manufacturing activity remains stable. Respondents believe higher interest rates in the financial markets will be a headwind this year…

Calm before the storm … partly ahead of the NFP and also with regards to … TRADE. Read …

An Eerie Calm Trade war whiplash continues to be a driving force for markets. Trump surprised on Saturday by setting a tariff implementation deadline on Canada/Mexico/China much sooner than we had expected. But he left enough time for Mexico and Canada to negotiate a one-month delay in implementation which, on balance, set the deadline for tariffs on each much closer to our original expectation before Saturday’s announcement. That delay has sent a significant calm over markets and weighed on the USD, even though a 10% increase in tariffs on Chinese imports did go into effect this week. A lack of significant counter-escalation from China as well as no overt attempts to weaken the yuan in response to Trump’s tariffs has fed into market speculation that a short-term “deal” to remove or delay these tariffs is only a matter of time. But Trump doesn’t appear to be in any hurry, unlike with Canada and Mexico, and we think political capital plays an important role here. Markets are rejoicing that Trump’s first trade war salvos suggest his bark is worse than his bite. But another wave of tariff threats are likely still on the way, with studies of trade policy coming due in 2Q. That wave may be more disciplined and structured than Trump’s current strategy of “will he / won’t he” trade war escalations.

We expect the January employment report as a whole to still be fairly solid, even though we don’t expect payroll growth to come quite as close to matching the December gain of 256,000. Our point estimate is only for a gain of 100,000 (consensus 170,000) in January, given that winter storms hit several regions of the country during the employment survey reference period (i.e. the pay period that includes the 12th day of the month). If payrolls prove weaker than expected in January, the question will be how much was temporary (due to bad weather or payback for the prior month’s above-trend gain) and how much was fundamental.

Meanwhile, on the flip side, the NFIB hiring plans measure for January—released today (Thursday afternoon)—signaled another very solid gain (albeit down from December's pace) in private payrolls in January (~175,000 or so—see chart below). While the NFIB's pre-COVID track record wasn’t great, the series has done a very good job at signaling the monthly directional change in payrolls since the pandemic.

Unfortunately, the BLS will not be able to precisely quantify the impact from inclement weather. Still, typically, when bad weather in the winter distorts the pattern of economic activity, the effects wash out relatively quickly…

On revisionist history (aka today’s JOBS report) …

Today witnesses the extreme hype of US employment data. Today’s data also has annual benchmark revisions, which will confuse the headlines. Weirdly, the US Bureau of Labor Statistics has cancelled all briefings explaining data. This is not necessarily helpful as data becomes more complex, inaccurate, and misunderstood. It has also fueled disquiet that the new US administration might politicize the way data is calculated (survey responses are already partisan).

Investors often run models comparing economic data to market reactions (rightly so—economics is central to everything and economists should be revered). However, these models tend to use post-revision data, when markets react to first-releases. Today’s benchmark revisions are likely to be large; large revisions remind investors of the inaccuracy of comparing revised data to real time market moves…

Productivity GROWTH moderating. OR perhaps you see it as growth MODERATING. Whatever you wanna see, here’s a hot take …

WELLS FARGO: Catching a Breath: Productivity Growth Moderates at the End of 2024

Summary Nonfarm labor productivity increased at a 1.2% annualized rate in the fourth quarter. While Q4's gain was softer than the past few quarters, labor productivity rose 2.3% in 2024 and continues to look stronger on trend relative to the prior cycle.

The more subdued reading on productivity growth in Q4 along with a pickup in compensation costs pushed up unit labor costs growth to a 3.0% annualized rate over the quarter. While this measure points to labor cost running a bit hot relative to the Fed's 2% inflation goal, we take more signal from the medium-term trend in productivity growth and the Employment Cost Index, which makes labor costs look like less a threat to the Fed's inflation objective.

Source: U.S. Department of Labor and Wells Fargo Economics

Same shop with a CPI precap in the moments and hours ahead of NFP …

WELLS FARGO: January CPI Preview: A Strong, But Less Jarring Start to 2025

Summary Inflation's early strength in 2024 was a jarring reminder that restoring price stability would not be a quick affair. The January CPI report is likely to show that inflation remained stubbornly strong at the start of 2025. We estimate the headline index rose a "high" 0.3%, which would leave the year-over-year rate unchanged at 2.9%. The core index also looks set for a 0.3% advance that we expect to be driven by the ongoing rebound in goods prices and a pickup in non-housing services.

We expect some lingering issues around residual seasonality to buoy January's core reading, but we think this dynamic will be less pronounced than last year. Seasonal adjustment factors will be updated with the upcoming release to reflect the most recent year's price movements. The incorporation of 2024 figures should lead the seasonal factors to "expect" more strength in January and February. Meantime, the somewhat calmer price environment of the past year should lessen the need for businesses to push through big price increases at the start of the calendar year.

If realized, more moderate price increases at the start of this year would unlock favorable base effects and lead to a slowing in the year-over-year rate of inflation in Q1. Yet, we expect the 12-month rate of inflation to move sideways through the remainder of the year, as further services disinflation is offset by higher goods inflation now that additional tariffs are in the works.

Finally, Mr. Bond Vigilante himself, weighing on another …

Trump 2.0 is borrowing a page from the Clinton administration's playbook, specifically the one in which Robert Rubin and James Carville warned Clinton that he had to respect the power of the Bond Vigilantes and maintain fiscal discipline. US Treasury Secretary Scott Bessent yesterday said that he and President Trump are less concerned with the federal funds rate (FFR) and instead are hoping to contain the 10-year Treasury yield. Bessent's message to the Bond Vigilantes was that he has explained to President Trump that they have the power to stymie his fiscal agenda.

That makes sense to us, especially since premature Fed rate cuts helped boost long-term yields, and therefore borrowing costs, over the past six months. The Bond Vigilantes protested the lack of monetary discipline.

A major component of the administration's economic plan is to bring down oil prices. As long as Trump 2.0 can increase oil supply enough to lower oil prices, the tight correlation between breakeven inflation and crude oil prices suggests this strategy might work (chart).

As long as bond yields are falling for good reasons (i.e., disinflation) and not bad ones (e.g., a recession), then that's a positive setup for the stock market…

… And from the Global Wall Street inbox TO the WWW … a few curated links …

Here’s a story from The Terminal which details comments from Fed’s Logan…

BLOOMBERG: Fed’s Logan Is Skeptical That More Rate Cuts Are Necessary

Higher neutral level means that officials could hold rates

Flags risks of new government policies for economy, inflation

Another room with a VIEW and as these cross the desk AND contain funTERtaining visuals, well … sharing, they say, is caring …

BLOOMBERG: Bessent's goals won't work unless DOGE does, too It’s becoming clear how much the Trump economic plan needs significant federal spending cuts.

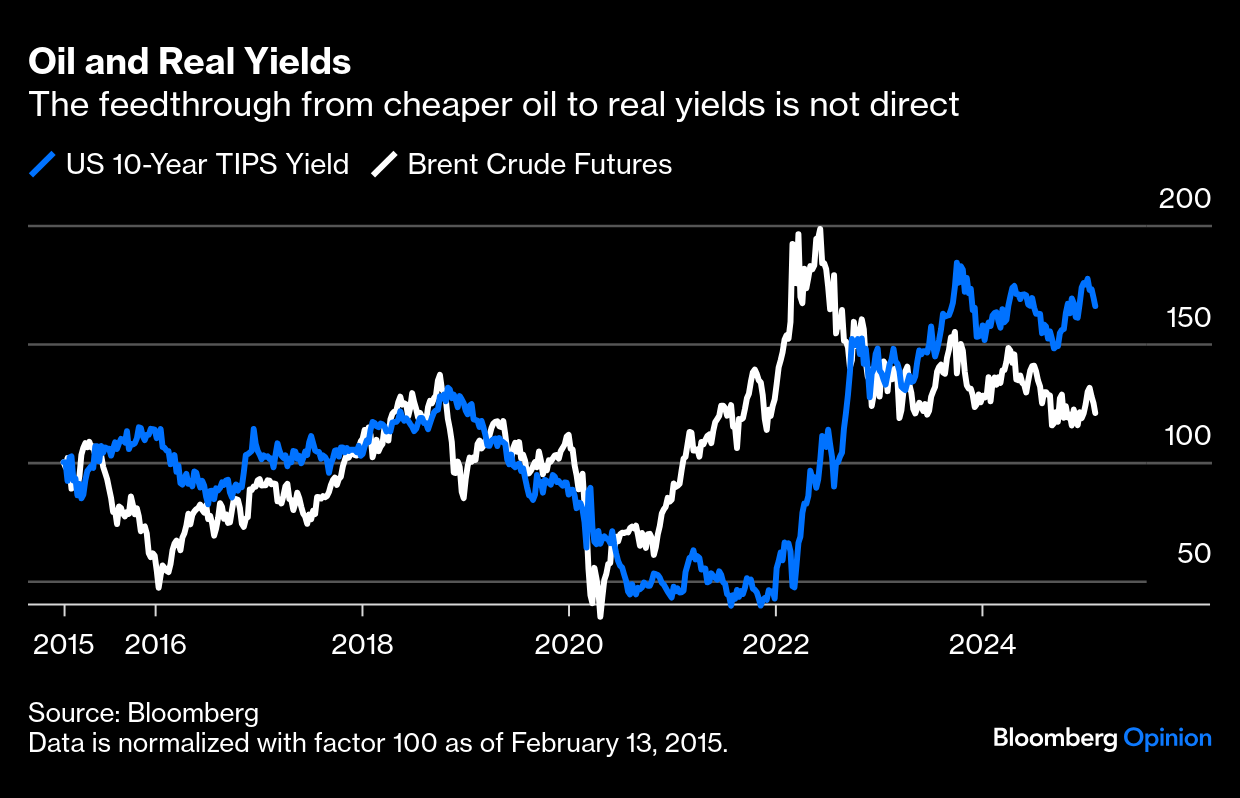

…Oil: During the campaign, “drill, baby, drill” was presented rather tenuously as a means to bring down inflation. The oil price has a big effect on 10-year inflation expectations, in what has been a durable anomaly — logically, if oil fluctuates and it’s a high price today, the odds increase that it will be cheaper in future and so inflation will fall, but that’s not how the bond market reacts to it. That means that getting oil prices down can theoretically help to bring down the allowance the bond markets make for inflation, and hence bring down yields:

But it’s unclear that this relationship, a quirk of the way traders in TIPS use energy futures as a hedge, can reduce the real weight of borrowing costs on the economy. Real yields suggest that cheaper oil doesn’t directly feed through. That’s logical as cheaper oil should theoretically act like a tax cut, and spur greater spending on everything else — which would be inflationary, and prompt yields to rise:

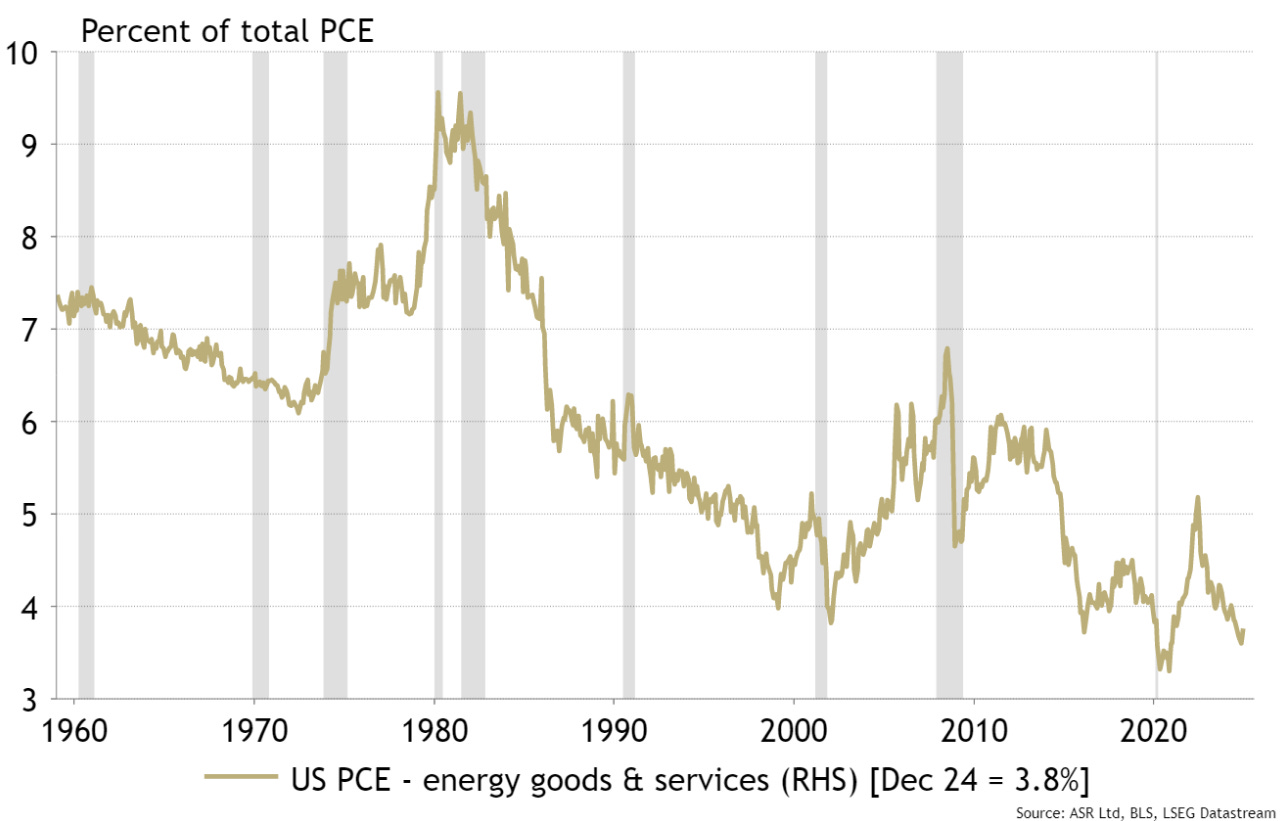

Another important question: What difference does it make? The oil price is far less important to a far less energy-intense US economy than it used to be — the cost of energy makes up a much smaller share of overall production costs, even at times when prices are high. The share of energy in gross domestic product, graphed here by Absolute Strategy Research, makes the point:

The oil price could double from here and still not inflict anything like the pain wrought in the late 1970s. Still, Absolute Strategy’s Ian Harnett points out that reducing energy prices — particularly as AI may be making the economy more energy-intense again — is “the only way to incentivize the private sector and relevering.” Pushing down the price won’t be easy. Trump’s intention to refill the Strategic Petroleum Reserve, depleted as the Biden administration battled inflation, will increase demand. And Jean Ergas of Tigress Financial Partners points out that OPEC won’t simply stand by as prices drop.

More things change the more they …

LPL: Will History Rhyme? Fixed Income Themes During the First Trump Administration

Early in the second Trump administration, tariff threats have revived market volatility. Recent Treasury yield curve movements reflect this uncertainty, with markets reacting to both threatened and postponed tariffs against key trading partners. Short-term yields rose as markets pushed back expectations for Federal Reserve (Fed) rate cuts, while long-term yields declined on economic slowdown concerns and potential trade tensions. These yield curve dynamics mirror patterns seen during the first Trump presidency

During the first Trump administration, trade tensions between the U.S. and China moved both interest rate and credit markets (more below). As tariffs escalated, two key trends emerged in the rates market. First, investors grew worried about economic growth, pushing them toward safer assets like U.S. Treasury bonds. This pushed long-term bond yields lower, even as the Fed kept raising short-term rates.

Second, international capital flows have shifted dramatically. China reduced its U.S. bond holdings by over $100 billion as tensions peaked. However, global uncertainty actually increased overall foreign demand for U.S. bonds, as investors sought safety from trade-related market volatility. Manufacturing slowdowns and supply chain disruptions reinforced these trends. As global factory activity declined, investors grew even more cautious, further compressing long-term yields. The result was a flatter and eventually inverted yield curve — where long-term rates fell below short-term rates.

Finally, food for thought …

ZH: Tomorrow's Jobs Report Will Finally Capture The Surge In Illegal Aliens, Lead To Another Big Negative Payrolls Revision

All of this, of course, is in the context of the massive downward revisions to 2024 payrolls which we discussed last night, and which look as follows: roughly 600K jobs lost every month last year.

Incompetence or just Blatant Fraud at Biden's BLS ????

All of this, of course, is in the context of the massive downward revisions to 2024 payrolls which we discussed last night, and which look as follows: roughly 600K jobs lost every month last year.

Incompetence or just Blatant Fraud at Biden's BLS ????