while WE slept: USTs a little firmer finding some reprieve following 20yr weakness; earnings - strong start to weak year?; JGBs warn; pensions funding secured (the upside of bond bloodbath...)

(BN) *HOUSE PASSES REVISED TRUMP TAX BILL, SENDS IT TO SENATE

AND … In markets, there is (usually)some truth and so, a quick check of the front-end pulse …

2yy WEEKLY (daily, inset): 4.15% resistance and approx 3.60% support:

I’ll just leave this marinate as bonds are said to fare much worse if the BBB (Big Beautiful Bill) were to succeed — higher debt / deficits, more USTs and so, a Fed <on hold, cutting, tightening … please choose one> …?

… with bonds helping solve the equation and being the ‘goat for all that troubles GLOBAL Wall, a couple quick hits …

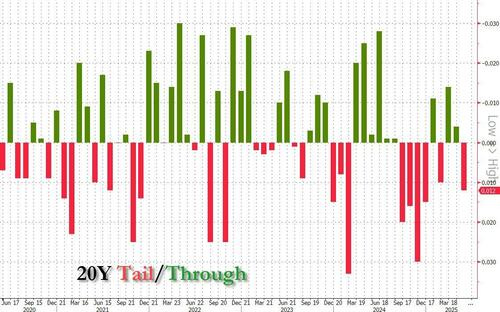

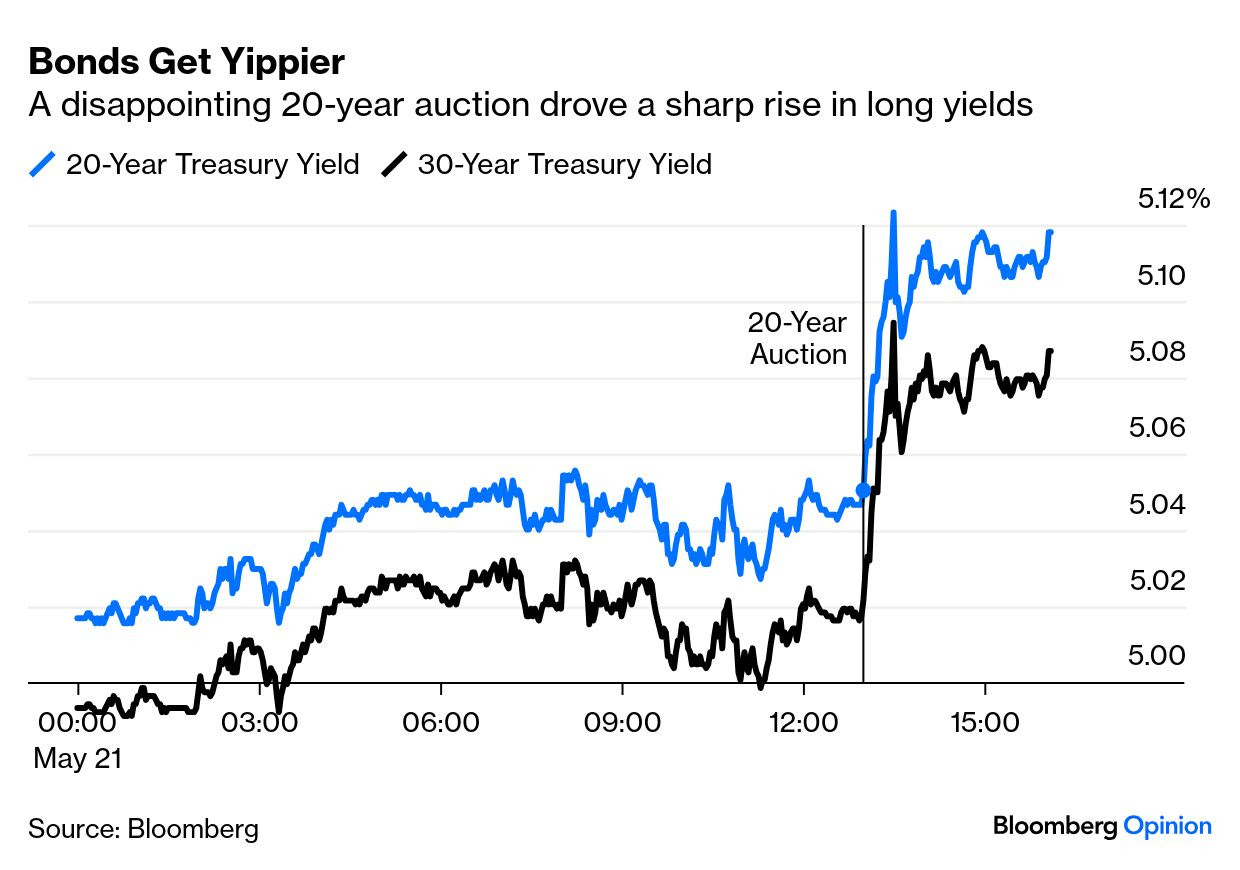

ZH: Yields Soar, Stocks Plunge After Ugly 20Y Auction Sees Biggest Tail Of 2025

Good morning … unless, of course you WERE long … of anything, including 20s above 5.00%.

Renting to own ANYTHING at moment, does not — repeat NOT — appear to be such a swell idea. Perhaps you wanna just lean in to everything and be greedy when people are fearful but at moment … i’ll just say, the fearful is real and palpable … safe havens didn’t feel to safe or haven’ee and in fact, are now being cited as the root cause of all that is evil … CONTEXT … 20s weren’t good but the tail wasn’t historically bad …

ZH: Ugly Auction Triggers Bond Bloodbath; Big-Tech & Black Gold Dumped As Bitcoin & Bullion Jump

'Japanic' attacks continued overnight in the JGB market as 20Y yields hit their highest since Oct 2000...

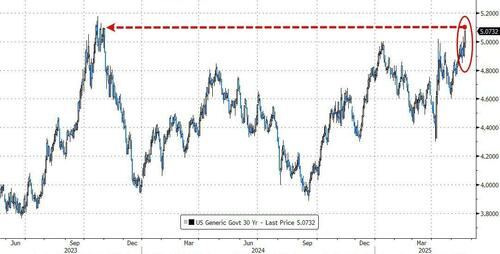

...was the straw that broke the camel's back of the last bit of confidence in the US bond market post-credit-downgrade today, sending 30Y yields soaring back above 5.00%, to its highest since Oct 2023...

Source: Bloomberg…

… AND … I’ll quit while I’m behind as I’d imagine I’m not alone and the only one in a foul(weather) mood…

… here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US equity futures gain alongside strength in USD/USTs as traders await US Budget updates … USTs are a little firmer, attempting to recover following the hefty losses seen in the prior session following a weak US 20yr auction. Focus firmly is on the fiscal front. Overnight, the House Rules Committee passed President Trump’s tax/spending bill. Thereafter, the broader floor voted to open debate on the tax bill, a debate process that lasts for around two hours (started approx. 08:00BST) and is followed by a vote on the bill. Progress on the bill is bearish for USTs as it will increase the US’ debt level, a figure which has been increasing and was the driver behind the Moody’s downgrade last week. USTs currently trading around 109-19.

Opening Bell Daily: Boring warning signals … An auction for 20-year Treasury notes saw weak demand on Wednesday.

… After a poor 20-year government bond auction in Japan on Tuesday, it was the turn of a weak sale of 20-year U.S. debt on Wednesday to cast a cold, dark shadow over world markets and put investors on the defensive.

The trouble is, when supposedly safe-haven sovereign bonds are at the root of the deepening market angst, the selloff takes on a more worrisome significance. And when it's U.S. Treasuries specifically, the cause for concern is even greater…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

First UP a look at … earnings (sorry, not sorry) …

22 May 2025 Barclays: U.S. Equity Insights: 1Q25 Earnings Learnings: Strong start to a weak year?

1Q25 results were good (in some aspects very good) but could be the last carryover of 2024 momentum as we head into slower growth and tariffs; Big Tech story intact but consumer weakening; guidance cuts + beta-driven rally fueling significant valuation expansion.

…Figure 4. Breadth and depth of EPS surprise was better than LT average

Best in show invoking idea of a Truss moment … with some context …

…It isn’t as if the Treasury market really needed further motivation to selloff – after all, the budget deal has already left investors on edge in anticipation of a Liz Truss style repricing toward higher yields (recall the 2022 budget-inspired spike in gilt rates). While we’ve been on-board with the selloff in the longer end of the curve, the 20-year auction didn’t provide any clear evidence of lackluster demand – overseas or otherwise. For context, dealers took 16.9% of today’s 20-year auction compared to the refunding average for the sector of 15.1%. Moreover, if one is inclined to use indirects as a proxy for overseas demand (which we tend not to), such bidders were awarded 69.0% compared to the 67.9% norm. The auction tailed by 1.1 bp versus an average of 1.0 bp. In short, the only aspect of the 20-year auction that could be construed as a warning shot for the borrowing plans of Congress was the subsequent price action. In the wake of the auction, the long bond cheapened to 5.095% – solidly in the October 2023 range – a selloff that was also inspired by growing issuance concerns.

Recall that in August 2023, Yellen increased the 10-year refunding auction size to $38 bn from $35 bn – followed by another $2 bn boost in November. After the selloff in early 4Q 2023, the Treasury Department scaled back auction size increases further out the curve – at least compared to the market’s expectations. It was a similar macro environment in that the real economy was still struggling with sticky realized inflation and the Truss episode was fresh in the minds of many market participants. What the 2023 episode revealed was that the Treasury Department (or at least Yellen) was willing to shift borrowing decisions based on the spike in term premium and respond more dynamically to the US rates market than it had in the recent past. Bessent is faced with a different setup as the most recent refunding announcement confirmed that auction sizes will be stable for at least several quarters – which, in practical terms, means the market isn’t looking for larger coupon auction sizes until Q1 2026 at the earliest.

Given that Bessent already wasn’t planning to increase auction sizes for the time being, the Treasury Department isn’t able to address higher term premium in 10s, 20s, and 30s by not increasing auction sizes. What’s left? Larger liquidity buybacks were floated as a possibility in the most recent refunding communications, although the extent to which that would reverse the negative sentiment in duration at the moment is unclear. After all, buybacks are not equivalent to QE – the latter simply monetizes the deficit.

It goes without saying that if Trump is, in fact, looking to the Treasury market as a barometer of investors’ approval of the action in Washington, then the recent selloff that brought 30-year yields from as low as 4.65% earlier this month to 5.095% is without question a troubling development. We’ll be watching the overnight session for any hints of a stabilizing bid and are wary the severity of Wednesday’s move will keep overseas investors sidelined for now. In the event of another leg higher in yields as the holiday weekend approaches, wobbles in the equity market will become more severe and we’d expect the moves to be addressed by Trump and/or Bessent. Whether this comes in the form of calming rhetoric or something more concrete is the true wildcard in the rates market…

German institution with a couple / few notes … one on a big beautiful bill and some relationships and stability of debt … but first, a few thoughts and an opinion — and as we know all opinions are created equally and that some are simply more equal than others. Many ‘out there’ love Saravelos and so …

The market has reacted very negatively to a poor US bond auction about an hour ago. We would make a few observations:

1. The most troubling part of the market reaction is that the dollar is weakening at the same time. To us this is a clear signal of a foreign buyer's strike on US assets and the associated US fiscal risks we have been warning for some time. At the core of the problem is that foreign investors are simply no longer willing to finance US twin deficits at current level of prices.

2. It is hard for US equities to stay resilient in this environment. The 2023-24 period saw a combined rise in US yields and equities as the market was revising US growth expectations higher. This was entirely reasonable. Today is very different. It is all a building fiscal risk premium in to US assets. It is hard to make the case that such a (negative) driver of the rising cost of capital is positive for risk assets.

3. The Asia investor base is key. Under our net external balance framework, Asia is the key provider of capital to US deficits, followed by Europe. The behaviour of US fixed income and the exchange rate therefore becomes critical during the non-US time zone. As we wrote earlier this morning, accelerated downside in USD/JPY during the Tokyo trading hours would be a strong signal of capital repatriation away from the US back to domestic markets.

4. "Solving" this problem is not easy. We have had multiple conversations with clients on what can turn this evolving negative dynamic around. Financial repression in the form of SLR "reform" and a shortening of US Treasury issuance maturities at the next refunding announcement have been mentioned most frequently. To the extent that a shortening in the duration risk of the US debt profile helps attract foreign buyers, this may indeed be helpful. But lower duration also implies higher debt rollover risk.

5. Only Congress, not the Fed can solve this. Extreme dislocations we believe will also prompt Fed intervention ("emergency QE") to preserve market functioning. Fed monetization of debt will not however resolve the core of the issue and may end up being counterproductive by increasing inflation expectations. Ultimately, there are only two "solutions" to this problem: either the US has to sharply revise the current reconciliation bill currently sitting in Congress to result in credibly tighter fiscal policy; or, the non-dollar value of US debt has to decline materially until it becomes cheap enough for foreign investors to return. Brace for more volatility.

…. Yesterday saw the 30yr Treasury yield (+12.3bps to 5.09%) close above 5% for the first time since October 2023, and only 2bps away from its highest level since 2007. Even during the inflation peak at 9.1% in 2022, 30 year US yields didn't climb above 4.40% that year. The only time they've been briefly above 5% since 2007 was at the peak of the Treasury sell off in autumn 2023, when yields rose by over 100bps in under three months following an increase in the supply of long-dated bonds and delay of Fed rate cut expectations. It took a change in issuance duration from the Treasury to calm the long-end.

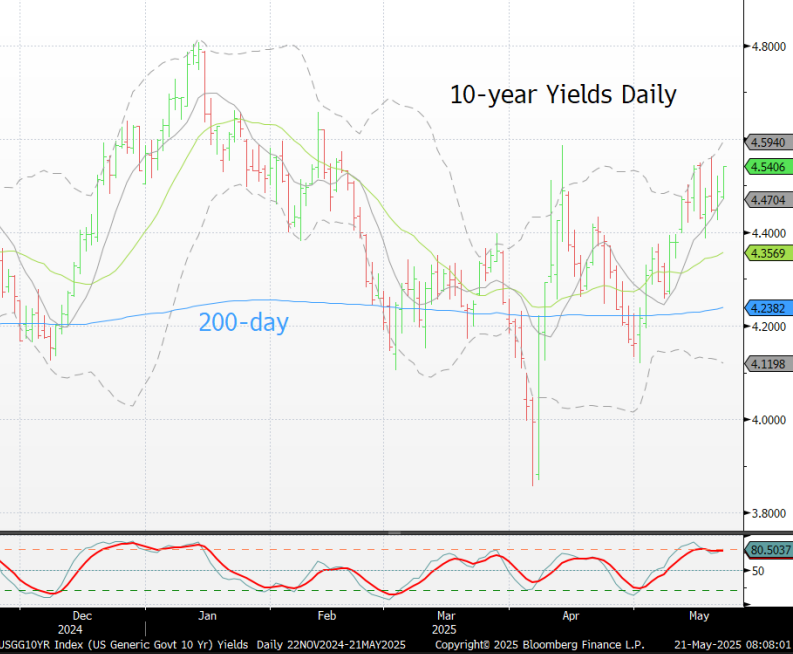

While Treasury yields were already trading around 5bps higher midway through yesterday’s session, they took another major step higher after a soft 20yr auction, which saw $16bn of bonds issued at 5.05%, +1.2bps above the pre-sale yield. This ended a pattern seen in the previous two sessions of an early Treasury sell-off reversing during US trading hours. Real yields led the move higher, with 30yr real yields rising +11.2bps to 2.78%, their highest level since 2008. Elsewhere along the curve, the 10yr yield (+11.2bps) rose to 4.60% and even the front-end wasn’t immune to the selloff, as the 2yr yield (+4.7bps) also moved back up to 4.02%. And in a repeat of concerns over US ability to attract foreign investors to fund its twin deficits, the rise in yields came while the dollar index (-0.56%) lost ground for a third session running. This morning US Treasuries are quieter, trading 1-2bps lower across the curve.

The soft 20yr auction was also a trigger for a broader market slump, with the S&P 500 falling from -0.2% on the day to -1.61% by the close, its worst day in the past month. This was a very broad-based decline with only 18 advancers in the whole index and the equal-weighted version of the S&P down -2.15%. The Mag-7 (-1.03%) saw a relative outperformance, mostly thanks to a +2.79% advance for Alphabet. Over in Europe, markets had closed before the US sell-off, with the STOXX 600 (-0.04%) little changed, while Germany’s DAX (+0.36%) reached another record high that took its YTD gains to +21.16%. European futures are around two-thirds of a percent lower as I type.

All those moves came amid an increased focus on the fiscal implication of the US tax bill going through the House of Representatives, which includes tax cuts that would increase the deficit over the years ahead. Initially, it had looked as though we might get a vote on the bill yesterday, which Speaker Johnson said he was planning on. But the chances diminished as the day went on, as various Republican members were still signalling their opposition. As a reminder, they only have a 220-212 margin in the House, so it only requires a handful of votes against (along with the Democrats) to vote down any bill…

21 May 2025 DB: The dark matter determining debt stability

As fears have subsided about an imminent economic downturn and steep Fed rate cuts that would have come along with it, markets have re-focused attention on the US fiscal outlook. This shift comes at a challenging time for US policymakers, as a market narrative has built around investors reducing allocations to USD assets over time. Although the acute concerns around this topic subsided with the Trump administration's tariff de-escalation, our client conversations indicated lingering worries from foreign investors about US debt dynamics (see "Notes from the road" and "Macro MATTers podcast: Trade de-escalation and notes from the road" ).

In this piece, we revisit our recent work deriving a simple debt stability condition comprised of inflation surprises and measures of liquidity / safety premia embedded in the US yield curve (see "Debt stability: Role of inflation is inflation, term premium is paramount"). This framework makes clear how a reduction in foreign demand translates directly into worse debt dynamics by putting upward pressure on the "dark matter" of the yield curve – the "other determinants" component of r-star and the 10-year term premium.

Under current conditions, we find that the US would need to run a primary budget deficit-to-GDP ratio that is no larger than 1.2% to keep debt-to-GDP stable over the long-run. A similar calculation last year determined that the this ratio could have been double that (2.4%) and yet would have kept debt stable given the levels of term premia and "other determinants" at that time. This worsening of debt fundamentals is almost entirely driven by the sharp rise in term premia over this period, with the ACM metric nearly 100bps above March 2024 levels.

With the fiscal package currently in front of Congress estimated to keep budget deficits as a share of GDP between 6.5% and 7% over the next few years (see "Tax bill details suggest still elevated budget deficits in the near term"), our analysis confirms that, unsurprisingly, deficits of this size are inconsistent with debt-to-GDP stability over the long run.Absent a clearer commitment towards putting deficits on a downward path, investor concerns about US fiscal dynamics are likely to persist.

21 May 2025 DB: Tariffs and the US Trade Deficit, Where Are We Headed? Peter Hooper

As US debt to the rest of the world has expanded to unprecedented heights, the Trump Administration has shocked the global trading system by resorting to trade policies not seen since the Great Depression. This paper aims to provide a basis for understanding the various forces that have driven the US trade deficit to its current depths and how the current tariff policy could influence its future course.

We begin by reviewing the various approaches to analyzing the US external balance and documenting the actual factors that have driven it into persistent deficit in recent decades. These include most importantly an overvalued dollar reflecting the combined effects of a persistently large US budget deficit and higher saving rates abroad; China’s export-led growth strategy has also contributed importantly.

Turning to the impact of tariffs, we find that, contrary to the conventional wisdom, they could actually narrow the deficit to some extent. This is partly because foreign retaliation to aggressive US tariff policy may prove to be more hesitant and muted than in the past, at least on the part of some US trade partners. It is also because the Trump tariffs have led to dollar depreciation rather than the appreciation that normally accompanies tariffs.

But tariff policy comes at a substantial cost in terms of increased prices and reduced output that are scheduled to show up in the months ahead and potentially to last for years.

While there is no painless path to deficit reduction, we outline a likely more effective and less painful one. This preferred path may be politically unviable for now. But we also see popular pressure building to reverse the current tariff-focused approach as its negative economic impacts become more evident in the months ahead.

Good news is all this may be worse for USD than UST … wait, what?

21 May 2025 DB: US fiscal risks may be worse for the dollar than Treasuries

A big challenge. The US fiscal policy uncertainty index has risen to record levels amidst debates about the tax bill and the long-term outlook (Figure 1). And this comes against a backdrop of unusually large (and unsustainable) deficits relative to the state of the economy. The budget deficit has been tightly correlated to the unemployment rate for many decades, and if that relationship held the budget would be close to balanced right now (Figure 2).

Foreign retreat. With the government showing little inclination to shrink these deficits, bond yields have marched higher. Both the 30y and 20y have risen above 5%, with an auction for the latter going poorly today. 5%+ yields have rarely been sighted in the past 15 years. This may be a function of foreign investors retreating from the US (as high frequency data suggests), after heavy investment for many years. Where would the marginal buyer then come from?

Domestic institutions may step in – they do hold less of the Treasury market now than they did a few decades back (Figure 3). And these yields may look enticing for a domestic investor who may be less uncomfortable with fiscal risks than foreigners. Plus SLR reform could incentivise more buying by banks. But even if domestics were to provide support for Treasuries at some point, it’d still leave the dollar lower as foreigners step back from the norm of solid buying. After all, we’re unlikely to see offsetting FX flows from domestic institutions repatriating, because they don’t own much – the US only owns one-quarter as much foreign fixed income as foreign investors hold of US debt (Figure 4). Instead, domestic institutions might consider rotating away from equities, since they account for a historically high share of their assets (Figure 5).

In sum, Treasuries may get some eventual support as domestics rotate away from equities, but the retreat from foreigners would still play dollar-negative.

IF you needed even MORE on the bearish steepening …

21 May 2025 ING: Rates Spark: Steeper curves amid US concerns

With the US tax bill making its way through the House, scrutiny of the country’s fiscal trajectory will remain a headwind for long end rates, with weaker auction results only providing occasions to push rates higher. We doubt that markets will place much weight on PMIs as the trade backdrop remains volatile, even though it points to de-escalation for now…

… Global bond markets matter and here’s something on all our radar screens …

May 21, 2025 MS: 30-year JGBs Send Concerning Signal for 30-year US Treasuries | US Rates Strategy

Investors looking for alternatives to longer maturity USTs should be aware of the potential value trap forming in long end JGBs. If attractive currency-hedged 30y JGB yields can't prevent further cheapening, then 30y USTs should continue to cheapen given poor yield-to-duration risk characteristics.

Key takeaways

Investors outside of Japan see value in longer maturity JGBs, but the bonds keep getting more 'valuable' by the week - a classic value trap we warned about.

Hedged back to EUR or USD using 3m tenor currency hedge, 30y JGBs offer a yield pick up of 160bp and 215bp vs. 30y DBRs and 30y USTs, respectively.

30y JGBs continue to cheapen because of a large and persistent mismatch between heavier domestic supply and weaker domestic demand.

Similarly, the yield on the higher supply of longer maturity US Treasury DV01 risk compares unfavorably to the yield-to-DV01 risk ratio on shorter maturities.

The cheapening of 30y JGBs strengthens the case for a significantly steeper US Treasury curve. Stay in UST 3s30s and 1y1y vs. 5y5y term SOFR steepeners.

… The value in 30y JGBs compares favorably to that in 30y US Treasuries. For investors with euros or yen, 30y Treasuries currency-swapped back to those currencies offer much less yield than 30y Treasuries offer an investor with US dollars (see Exhibit 3).

A(nother) recap — if we don’t learn from history, we’re doomed to repeat — and one more thing — looking for an updated middle of the year outlook for stocks

Weak 20y UST auction spurs weakness across US markets; UST bear-steepening continues; beat in UK CPI; long-end JGBs continue to underperform; BI cuts rates by 25bp; DXY at 99.60 (-0.5%); US 10y at 4.599% (+11.2bp)

A disappointing 20y UST auction which tails by 1.2bp intensifies broad weakness across US assets; long-end yields rise (30y: +12bp), SOFR swap spreads tighten (30y: -3.5bp), equities fall (S&P 500: -1.6%), and MBS basis and credit spreads widen.

UST bear-steepening accelerates (2s30s: +7bp) after the weak auction with ongoing uncertainty around US fiscal policy and its requisite impact on UST supply continuing to weigh on the long-end…

May 21, 2025 MS: US Equities Mid-Year Outlook: Focus on Rate of Change Michael J Wilson

Tougher 1H 2025, Better 2H 2025 and 2026...Coming into 2025, we were of the view that the first half of the year would be more challenging as policy was likely to be sequenced in a more risk-off way initially ahead of a more constructive 2H 2025/2026. While we've been surprised by the magnitude and speed of the growth headwinds in 1H tied to tariffs, the cadence of our view around policy sequencing still holds. From our perspective, the level of tariffs announced on 'Liberation Day' was so dramatic, it led to what can only be described as capitulatory price action. As a result, we think that the price lows are in assuming we don’t experience a deep recession (our bear case). This makes sense in the context of the average S&P 500 stock already enduring a 30% drawdown this year.

Focus on Rate of Change…Given equities' tendency to focus on the next 6-12 months, markets are now looking forward to a more accommodative policy agenda for stocks over the course of our forecast horizon – including incentivizing infrastructure investment, tax breaks, de-regulation, and rate cuts. Most importantly, the recent reduction in the headline tariff rate on China from 145% to 30% significantly lowers the risk of a recession. Our economists do not see a recession in their baseline, but they do forecast seven rate cuts in 2026, which is supportive of higher-than-average valuations. Having said that, we see back-end rates as the main risk to stocks in the short term, with the 10-year yield hovering around our key 4.50% level – the point where rate sensitivity should increase for equity markets. If back-end yields remain elevated, they can keep a lid on multiples for now, and keep the S&P 500 in our 1H25 range of 5500-6100, tactically, before upward progress continues to our 12-month price target of 6500.

We Reiterate Our 12-Month S&P 500 Price Target of 6500...The drivers of our 6500 base case price target are a 21.5x P/E multiple on 12-month forward EPS of $302. We have not adjusted our target throughout the recent correction, and reiterate that its achievability is more likely by the middle of 2026 versus the end of 2025 given the magnitude of the 1H drawdown and the lagged impacts of tariff uncertainty on earnings over the next couple of quarters. We see 2025 EPS of $259 (7% growth), 2026 EPS of $283 (9% growth), and 2027 EPS of $321 (13% growth). It's important to point out that we've already experienced rolling earnings recessions across wide swaths of the equity market for the last ~3 years. This makes comparisons less onerous and sets the stage for a more synchronous EPS recovery over the course of our forecast horizon. The earnings path should be aided by Fed rate cuts in 2026, dollar weakness, as well as a broader realization of AI-driven efficiency gains. We think that valuation stays elevated at 21.5x as our work shows that it’s rare to see multiple compression in periods of above-median EPS growth and a declining Fed Funds rate, which is our base case house view by the middle of next year. Our bull case price target of 7200 assumes a faster recovery from the tariff overhang, and our bear case target of 4900 considers a deep recession.

Investment Recommendations...We continue to advise staying up the quality curve in cyclicals. For defensive hedges, we would stay selective and focus on stocks with less leverage and cheaper valuation. We include screens on both fronts in today's report. After downgrading Industrials to equal-weight before 'Liberation Day' in an effort to position more defensively, we’re now upgrading the sector to overweight once again. We see Industrials as the sector best positioned to benefit from the administration’s focus on a domestic infrastructure build-out. We move Utilities from overweight to equal-weight as we reduce defensive exposure. We continue to recommend large cap over small cap equities as large caps have superior pricing power and supplier bargaining power, as well as less sensitivity to sticky back-end rates. Finally, we continue to prefer US over international equities as earnings revisions start to inflect higher for the S&P 500 relative to MSCI ACWI Ex US—a call we've been making more recently.

…Finally, where we expect to get the most push back on this view relates to valuation. Having learned this lesson the hard way, the starting point matters for forecasting valuations—i.e., if the starting point is high, the ending point is likely to be high as well. In short, valuations adjust on a rate of change basis as opposed to converging to a historical average or median unless we are talking about a generational shock to markets (not our view). While some might argue tariffs and de-globalization represent such a shock, we would argue this shift began many years ago during President Trump's first term and continued through the Biden administration to some extent. Furthermore, with the recent roll-back on China tariffs, this "shock" appears much more manageable. It's worth noting that the equity risk premium reached nearly the exact same level witnessed after 9-11, marking the recessionary high (trough in the multiple) for that cycle, ahead of a final high in 2002. While ~150bps of equity risk premium isn't high in a historical context, there is precedent for it marking a high in the midst of a recession—equity markets bottom on bad news. Bear in mind there is scope over the next few years for the ERP to increase again and perhaps well above last month's levels. However, we think that is unlikely if back-end rates fall in line with our rates strategists' forecast—3.45% 10-year UST yield 12 months from today. Perhaps most interesting is the comparison to the Long Term Capital Management (LTCM) shock in late 90s that did not lead to a formal recession. The ERP subsequently fell to all-time lows after that false alarm. Bottom line, valuation is a good guide in the long term but tells us very little in the short term. Given the magnitude of the deleveraging we witnessed last month, it will take a lot to get that kind of pressure again on price, and it's not clear that a mild recession would even lead to that outcome now. See our base case write up below for more detail on why the current environment is likely to lead to valuation support around current levels (21.5x).

… AND a(nother)USD update from across the pond …

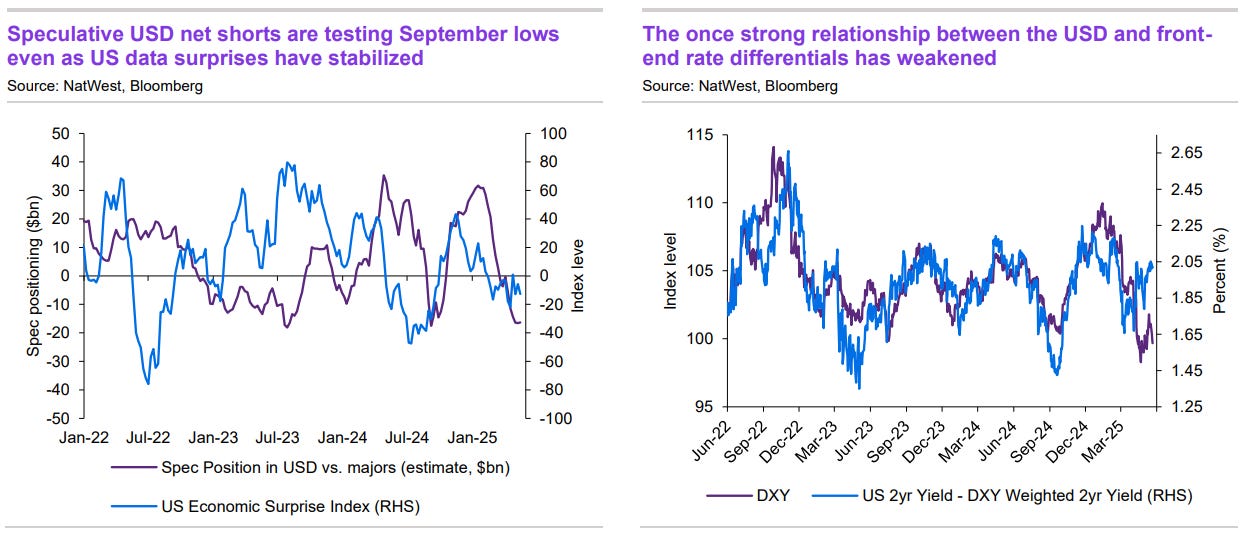

21 May 2025 NatWEST: USD Update One Big Beautiful Bill

The near-term cyclical backdrop for the USD has improved as tariff de-escalation and solid economic data combine to reduce recession tail risks and lead markets to price out Fed easing expectations. With the USD remaining a high carry currency within the G10, we see risk of further consolidation near-term. But we continue to think mediumterm concerns about USD exceptionalism still linger, and next month’s data present a fresh test of the US economic consensus that has adjusted higher. We also believe that hedging USD exposure of US asset holdings is a durable theme that can continue even if the USD doesn’t lose its mantle as the global reserve currency. This week, Moody’s downgrade of the US sovereign credit rating came during the heart of US tax law discussion, re-invigorating questions about US Treasury supply / demand imbalance and shifts in term premium. In this note we review our outlook for the USD and our expectations on the Republican tax law working its way through Congress.

This next fella is taunting us and I think it’s all ‘cuz Lizz Truss moment … feeling like he’s willing it to happen here and, well, we all best be careful what he’s wishin’ for cuz we might just get it …

US President Trump labelled the budget proposal trying to pass Congress a “Big Beautiful Bill.” BBB might be an unfortunate alliteration given concerns about the US credit rating. The details of the budget are constantly changing, so their effects are hard to judge, but the broad impact is to push the US further along a rising debt path. Bond investors are less than happy.

Economically quite a lot of the budget is extending existing tax cuts, which does not add to growth. Removing taxes on tips might push inflation higher than reported. If employers reduce pay (included in consumer price data via prices) and encourage tipping (not included in consumer price data), the cost of living will rise more than reported inflation…

Finally, from the HEAD of the vigilante dept …

May 21, 2025 Yardeni: Is A US Government Debt Crisis Imminent?

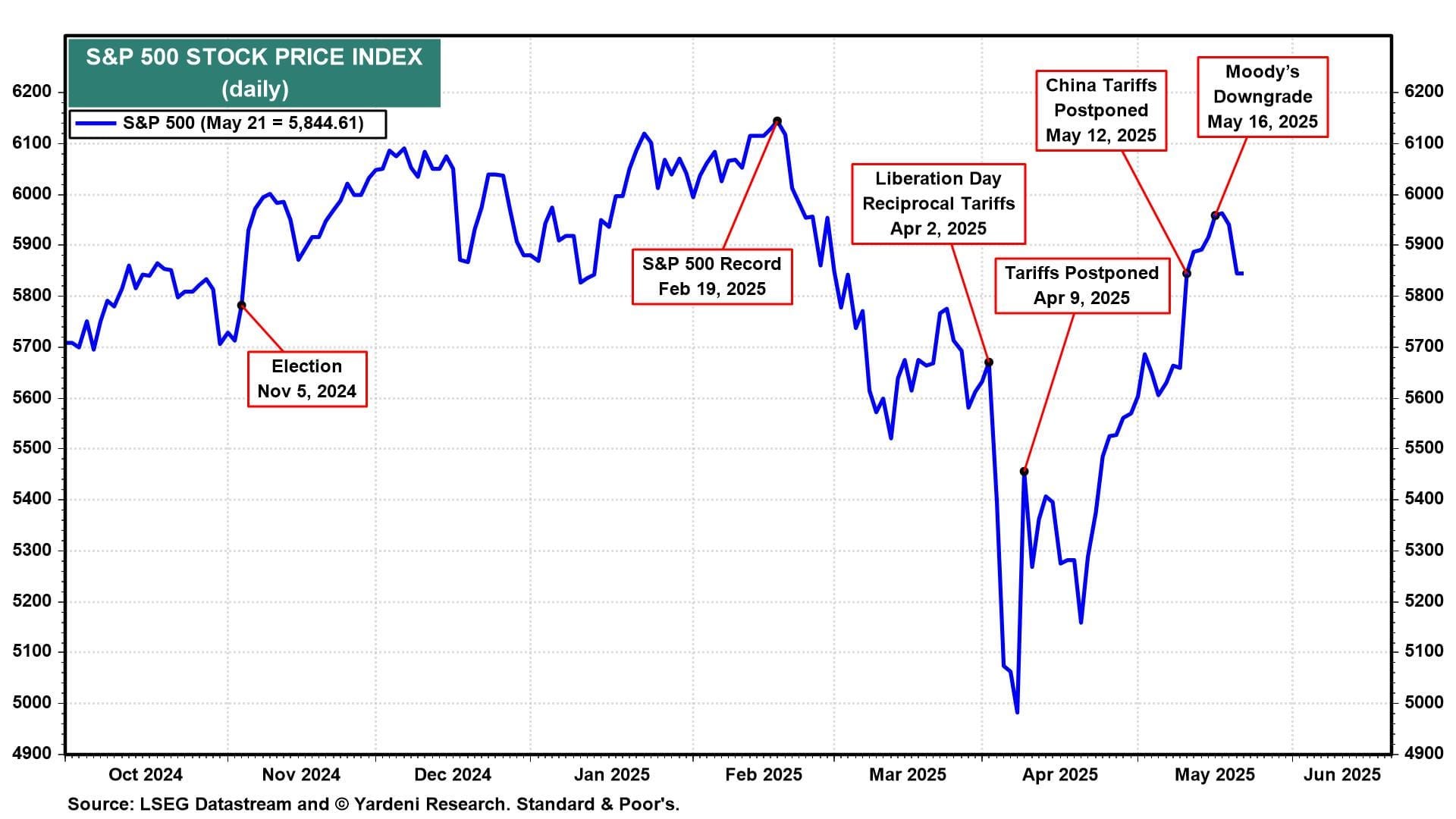

Stock investors have been less "tarrified" about President Donald Trump's tariffs since April 9, when he postponed most of his proposed reciprocal tariffs by 90 days (chart). However, they may now be getting spooked that the bond market might be on the verge of a debt crisis, especially after Moody's downgraded US government debt on Friday and Japanese bond yields soared in recent days. The S&P 500 fell 1.61% today mostly after the sloppy results of the 20-year US Treasury auction.

In addition, the 30-year US Treasury bond yield closed above 5.00% today for the first time since late October 2023 (chart). The 10-year yield is still well below its October 2023 peak, but the financial press rang the alarm bell about the 30-year yield exceeding 5.00%.

Furthermore, stock and bond investors may be starting to get jittery over the implications of Trump's "Big Beautiful Bill" for federal deficits and debt. The debt is up to a record $36.2 trillion with $28.6 trillion in marketable securities held by the public…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Earnings. All things eventually will be blamed on bonds. Earnings …

May 22, 2025 Apollo: The Negative Impact of Tariffs on Earnings

While tariffs on China have declined from 145% to 30%, the headwind to corporate earnings from tariffs remains significant because of the overall jump in the average tariff rate from 3% in January to 18% today, see the first and second chart below. We are already beginning to see weakness in the economic data with a significant decline in the earnings revisions ratio since Liberation Day, see the third chart.

Note: Includes IEEPA tariffs on Canada, Mexico, and China (with USMCA exemptions); April 2 “reciprocal” tariffs; and steel, aluminum, auto, and auto parts tariffs. Tariff revenue estimate uses an elasticity of -0.997 and a noncompliance rate of 8 percent. Sources: US Census Bureau; Historical Statistics of the United States: Colonial Times to 1970, Part II; US International Trade Commission, “U.S. imports for consumption, duties collected, and ratio of duties to values, 1891-2023, (Table 1)”; Tax Foundation calculations; Apollo Chief Economist

… dunno, but this next VIEW sounds like (bond market)HATE speech to me …

May 22, 2025 at 5:00 AM UTC Bloomberg: The bond vigilantes may need a lot of rope All around the world, investors are more reluctant to lend to governments over long terms.

…The proximate trigger for the US bond market (described as “yippy” by President Donald Trump last month as rising yields prodded him into delaying tariffs) was a lackluster auction of 20-year debt. That had an instant effect:

There were good candidates to explain the nerves. Moody’s downgrade, announced Friday, has little practical effect, but dampens sentiment. Confidence was also shaken by negotiations in Congress over what is now officially namedThe One Big Beautiful Bill Act.On its face, as Justin Fox explains, the bill is pretty ugly — cutting services for the poor and using the savings to cut taxes mostly for the wealthy, even as the deficit rises. Inequality doesn’t particularly bother bond investors, but the way legislators don’t seem even to be trying to cut the deficit is a big problem. Much remains up for negotiation, but the outcome will almost certainly be bond-negative.

The question, according to TS Lombard’s Steven Blitz, is: “How much of a haircut are bondholders willing to accept, from dollar depreciation and/or inflation?” The proposed deficit rise for next year is $472 billion. Even if tariffs raise $250 billion in revenue to alleviate this, that would still leave a 13% increase compared to earlier estimates, Blitz says, before counting interest on the debt.

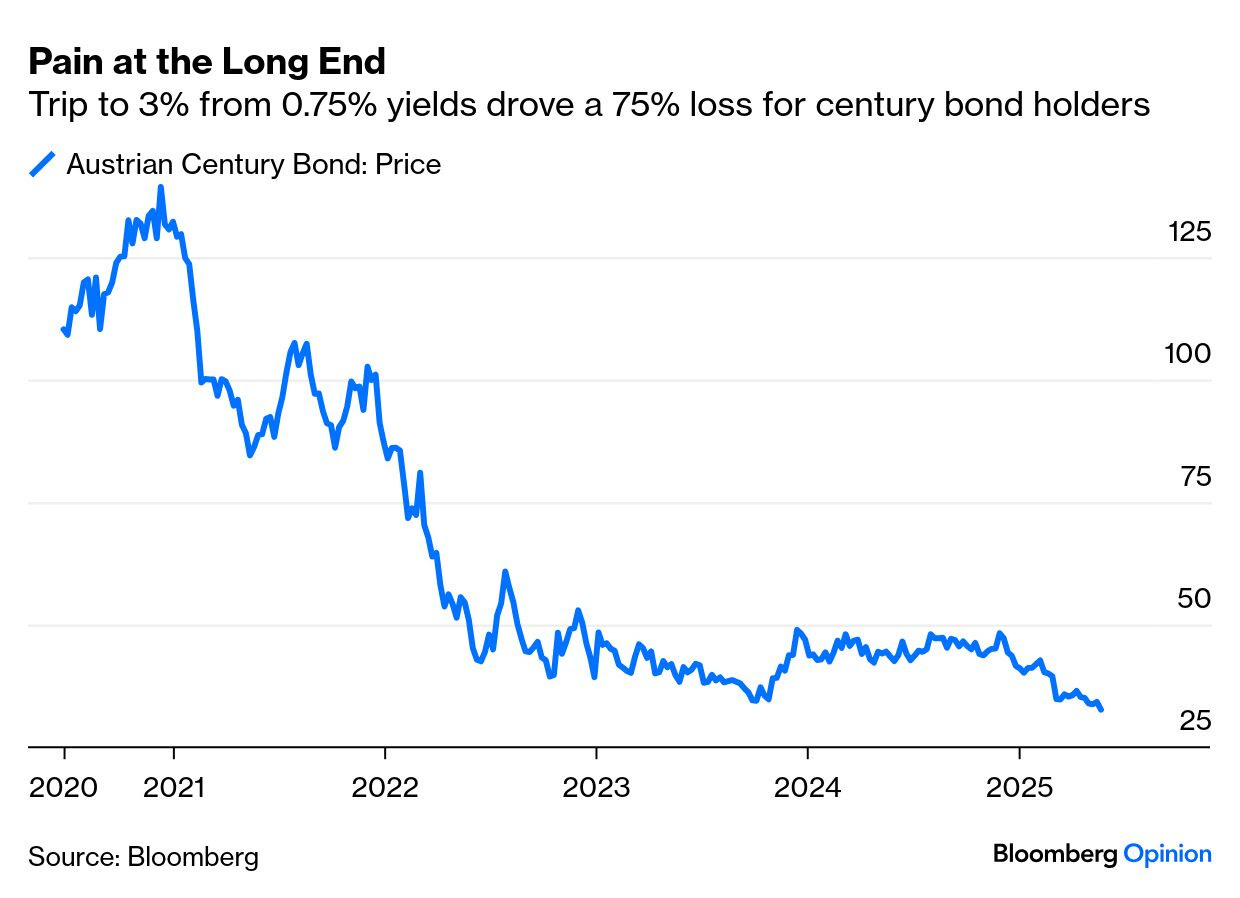

Bond math means rising yields for the longest issues inflict particular pain on those holding them. To illustrate, this is the price of the Austria century bond, not due to pay out until 2120, over the last five years as its yield rose to 3% from 0.75%:

Usually, rising yields help a currency, as they attract capital…

… Finally, any analysis of rising yields would be incomplete without a reminder that they’re good news for someone — pension fund managers and their pensioners. Higher yields make it cheaper for defined benefit plans to fund the guarantees they have made to savers, and mitigate falling equity prices. As the consulting actuary Mercer shows in this chart, corporate pensions run by S&P 1500 companies are now fully funded, meaning that their assets are worth more than their liabilities. In 2019, they were starting at a deficit of more than 20%:

It’s an ill wind. But for most of us, the upward drift in long yields is a problem that can no longer be ignored…

… and today’s ‘exclusive’ is, if not mistaken, YESTERDAYS news …

Updated on May 22, 2025 at 4:59 AM UTC Bloomberg: Dimon Warns of US Stagflation Risk, Says Fed Right to Hold

… “I don’t agree that we’re in a sweet spot,” the chief executive officer said in a Bloomberg Television interview from the lender’s Global China Summit in Shanghai. He added that the US Federal Reserve is doing the right thing to wait and see before they decide on monetary policy.

Bonds. They are a ‘thing’ and ALL over the intertubes … 10s, weekly, back to 1913 …

at howtoswingtrade

Rates have broken out of a 40 year downtrend.

If this were a stock, we’d call it a Stage 2 uptrend.

And like any new trend, higher highs attract sellers who aren’t convinced — leading to weaker auctions, hesitant capital, and more volatility along the way.

Since rising bond yields appear to be back in focus, here's a helpful (updated) chart @MichaelKantro sent to us for the @YahooFinance Chartbook back in January.

May 21, 2025 LPL: Tactical Update: Checking In on the 60/40 Portfolio

…Tactical Summary: Stay Nimble, Stay Diversified

The STAAC’s latest tactical shifts reflect a market caught between competing forces — slowing growth, persistent inflation, and geopolitical and policy uncertainty. In this environment, we believe that staying close to benchmark in areas of low conviction, while leaning into quality and diversification, remains a prudent approach while we wait for more visibility into the potential effects of the new tariff environment on earnings and economic growth. We continue to believe the demise of the traditional 60/40 portfolio has been greatly exaggerated, and it is still an important portfolio construction tool, lending itself to capturing opportunities in both the equity and fixed income markets, but a tool that works best when stock-bond correlations are negative. Periods of elevated inflation have historically been associated with positive stock-bond correlation (the 21-day rolling correlation has recently flipped positive) supporting our belief that on a tactical basis, the traditional 60/40 can be supplemented through the addition of an allocation to diversifying alternative strategies with lower correlations to traditional asset classes.

While EVERYTHING was sold aggressively yest, this next note topical and something for all of us … key point made — bonds are CHEAP …

May 21, 2025 Topdown Charts: Chart of the Week - Stocks vs Bonds

Following the tariff tantrum turnaround stocks are up and bonds are down — and we’re right back to stocks being expensive (+bonds cheap) again.

Charts like this week’s are probably about as unpopular as it gets at the moment.

On the equity side, emboldened bulls point out earnings resilience, AI/tech blue skies, and prospects of deregulation and tax cuts driving the bull market onwards and upwards after a late-cycle reset.

On the bond side, bearish narratives around deficits, debt, and downgrades hang overhead along with policy uncertainty and tail risks for foreign holders, and the prospect of “outgrowing debt“ meaning higher nominal growth and higher for longer interest rates.

But here’s the point to ponder this week: the way valuation charts like this resolve is almost always unthinkable at the time.

In 2000 no one thought stocks would fall or bonds rise.

in 2003 no one thought stocks would recover or bonds lose luster.

In 2022 no one thought stocks and bonds would both get dunked.

But the clues where there in the valuation indicators.

So sometimes it’s not about coming up with grand narratives and macro forecasts, sometimes it’s just as simple as putting together good objective indicators and studying where the pressures are building up.

Key point: our indicators are saying stocks are expensive and bonds are cheap.

https://www.zerohedge.com/news/2025-05-21/how-trump-can-calm-bond-markets