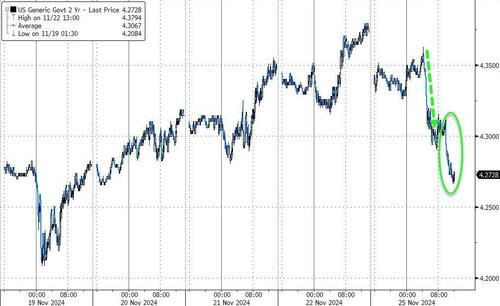

5yy DAILY: TLINE ‘support’ up nearer 4.35% and resistance down ‘round 4.10%

… momentum has moved from overSOLD in to overBOUGHT territory which makes some amount of common sense (which, they say, ain’t so common) with recent bid off 4.35 cheaps … this would then make it incrementally more difficult to see a strong bid for today’s 70bb 5yr auction unless, of course, Bessent bid and disinflationary forces were to continue to materialize …

…. and these prices ALSO include yesterday’s BID for a variety of reasons (oil, Bessent), some of which to be mentioned in a moment …. but FIRST, THAT didn’t last long …

CNBC: Trump vows an additional 10% tariff on China, 25% tariffs on Canada and Mexico

President-elect Donald Trump plans to raise tariffs by an additional 10% on all Chinese goods coming into the U.S., according to a post Monday on his social media platform Truth Social.

The post immediately followed one in which Trump said his first of “many” executive orders on Jan. 20 would impose tariffs of 25% on all products from Mexico and Canada.

Trump had threatened tariffs of 60% on Chinese goods while campaigning for president.

… NOW before we go off the rails on how ONLY inflationary these policies could possibly be (WSJ Blinder OpED, “Trump’s Economic Plan Has Inflation Written All Over It”), what IF these polices were dovish (Joseph Wang note HERE). What IF these short-term bargaining tools that, if enacted, did dent economic growth enough to elicit a Fed reflex (ie cutting of interest rates) … would one need to consider the de / dis inflationary forces OF said tariffs — INFLATIONARY to start, enough to be tempered by stronger dollar and LOWER margins and SLOWER growth? OR, is one pre wired to only and forever consider these as inflationary consumption TAX without other consequence?

Before jumping TO conclusions and falling fully into a backwards look at yesterday and 2yr auction results) as some sort of lead up TO the days 5yr auction, well, an interruption of regularly scheduled programming for what appeared to be good news …

... Trump policies aren’t happening in a vaccuum and the middle east tempering of tensions clearly a good thing … the markets moved before Trump tweet (or Truth Socialed … whatever you call it) and good news as good or bad, as always, depends on your very own P&L I suppose … but a bit of disinflation and risk OFF certainly in the air has KEPT bid for both stocks AND bonds early and actually raised enthusiasm a touch heading in TO the 2yr auction … and as the day came to a close, well … a couple from ZH as the dust settled …

… Yields were dramatically lower across the entire curve with the long-end outperforming (bid from early in the US session and didn't stop)...

A solid 2Y auction pushed yields lower from an already lower starting position...

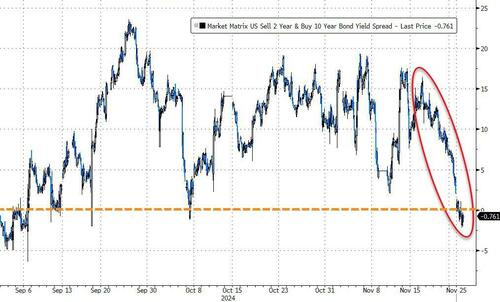

The Treasury curve (2s10s) re-inverted again today - first the first time since Oct 7th - and closed inverted for the first time since early September...

ZH: Small Caps Soar, Gold Crumbles, Dollar Wobbles

… Rising rates have been a drag on small caps. The Russell/SPX ratio has moved higher, but imagine what happens should rates take a move lower...?

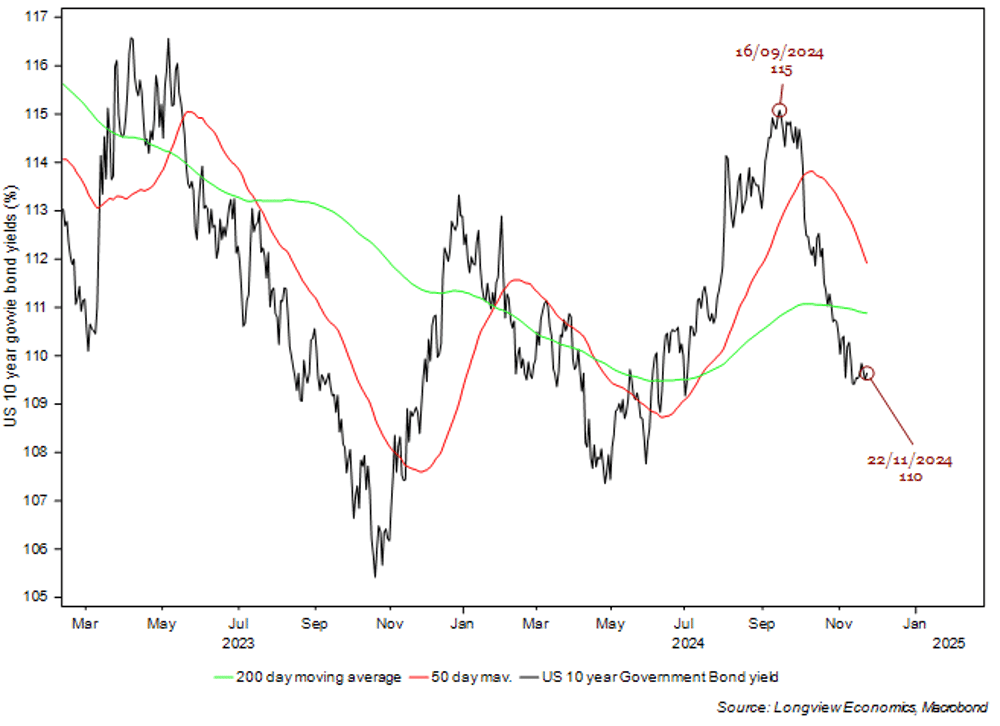

US 10 year with a perfect reversal off the big negative trend line.

ZH: Bonds Extend Bid After Solid 2Y Auction Demand Sees Big 'Stop Thru'

…Bidders were evidently happy to scoop up “cheap” paper as the offering stopped at 4.274%, nearly 2 bps through the when-issued yield...

… AND so, on to 5s we go … get those bids in early and often … here is a snapshot OF USTs as of 702a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries saw momentum stall at the Tokyo open, with UST futures slipping mildly lower, with the return of Tariff Man offsetting Fed Kashkari's ‘reasonable cut’ thesis for the DEC meeting. FX saw some significant reactions to the Trump administration announcement, with MXN -1.2%, CAD -0.8%, KRW -0.3%, AUD -0.3%. Crude is +1%, Copper flat, and BCOM +0.5%. The NKY (-0.9%) and KOSPI (-0.6%) weakened, with DAX futures -0.5% and S&P futures showing +1pt here at 6:45am. UST futures volume is ~80% the 10d average amid the modest belly-led cheapening (2s5s10s +2bps).

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: CAD & MXN hit by Trump’s tariff announcement, US futures impacted but are back in the green; FOMC minutes ahead … Fixed benchmarks in the red pulling back from Monday's gains though did see a shortlived move higher on the tariff announcement … Benchmarks in the red, pulling back modestly from the rally seen on Monday after Trump’s Treasury Secretary nominee. Stateside, the curve is yield curve is bear-steepening (vs bull-flattening on Monday) though there is some way to go for yields to recoup lost ground…Benchmarks saw a jump higher overnight on Trump's tariff update, but this proved shortlived with fixed fading across the board, modestly in the red and toward session lows.

Opening Bell Daily: Turkey Run … Thanksgiving is great for stocks — especially in an election year … Historical data points to a dip after Turkey day then a rally into 2025.

OPEC+ has once again postponed its plan for the revival of its production until January.

The outlook for next year is widely seen to be negative with the main international agencies expecting a surplus even if OPEC+ does not step up production as supply additions outpace demand growth.

Under the new Trump administration, we expect an increase in oil supply and further slowdown in demand following the proposed reduction in taxes and protective trade measures.

We expect significant downside for oil prices over the next year.

In the first half of the year, frontloading in demand starts to bring the market into better balance reducing some pressure on prices, though we expect Brent to head towards USD 60 by year end.

… here a large German institution weighs in on Bessent, the economy …

DB: What Bessent's nomination means for the economy

On Friday evening, President-elect Trump nominated Scott Bessent to be his Treasury Secretary. Bessent has had a long and distinguished career as an investor and brings to the Treasury position an impressive and unique resume spanning global macro and markets. He will inherit a fundamentally solid economy and market backdrop that nonetheless faces challenges and will also have to manage the transformative changes promised by the incoming Administration. In this note, we discuss what his nomination means for tariffs, budget deficits, Fed independence, and dollar policy.

President-elect Trump overnight announced the imposition of new tariffs on Canada, Mexico and China as soon as he comes into office. While the initial market reaction has been contained for reasons we discuss below, our overall read is that tariffs are clearly at the top of the Trump agenda. We see an implicit signal that they are likely to be used as a broad-based economic and geopolitical tool in this Administration. What's more, we would emphasize that uncertainty is the key transmission channel via which the economic impact of a trade war transmits to the world and the announcements overnight achieve just that: high uncertainty. As we wrote last week, we continue to believe that the the Trump policy mix remains significantly underpriced.

… same shop on this pick and the move in USTs yest (prior to last nights tweets) …

… Ahead of that news overnight, the 10yr Treasury rally (-12.7bps) was the main story yesterday, carrying on from the initial rally in Asia we discussed yesterday after Scott Bessent’s nomination as the new US Treasury Secretary late on Friday. But markets were also helped by reports suggesting that Israel and Hezbollah were close to agreeing a ceasefire, with Israel’s ambassador to the US saying that a deal “could happen within days”. So that led to a noticeable pullback in Brent crude oil prices (-2.87%), which also helped to ease investors’ fears about inflationary risks.

In terms of Scott Bessent’s nomination, we mentioned yesterday how markets were already reacting constructively in Asia, but that was evident across the US session as well. That’s because Bessent is seen as market-friendly and has supported a gradualist approach on tariffs, so his nomination is seen as a less aggressive option than some of the others would have been. In addition, Bessent has consistently argued in favour of cutting the federal budget deficit, so that was viewed as positive for Treasuries as well. Lower yields meant the dollar index (-0.69%) saw its biggest daily decline since August. For more info on Bessent’s views and what that could mean for the economy, our US economists published a note yesterday on the topic (link here).

The positive reaction was clearest in Treasury markets, where yields saw a clear decline across the curve. For instance, the 2yr yield was down -10.4bps to 4.27%, whilst the 10yr yield fell -12.7bps to 4.27%. There was also a particularly strong decline among real yields, with the 30yr real yield (-7.0bps) seeing its biggest daily decline since August. Nevertheless, after the US close, Minneapolis Fed President Kashkari said that, “knowing what I know today…considering a 25-basis-point cut in December — it’s a reasonable debate for us to have.” So that added to the questions about whether the Fed would cut at all next month, and the 2yr yield is up +1.7bps overnight to 4.29%. At the same time, Kashkari acknowledged “some confidence that (inflation) is gently trending down.”

Whilst that was happening, the other main story yesterday came from the Middle East, where reports suggested that Israel and Hezbollah were moving closer to a ceasefire deal. That led to a direct reaction amongst several assets, and the Israeli shekel strengthened +1.66% against the US Dollar, which is its biggest daily move up in four weeks. Moreover, oil prices saw an immediate move lower as the reports came through, with Brent crude falling -2.87% to close at $73.01/bbl. Overnight however, oil prices have stabilised, with Brent up +0.40% higher to $73.30/bbl as we go to press….

The S&P 500 has risen strongly for 2 years, raising questions about its drivers and valuations. We attribute the rally to low expectations for the cycle while growth turned out to be very robust, with the current combination of low unemployment and strong GDP growth seen only 6% of the time; a cross-asset inflows boom after households accumulated excess cash around the pandemic; and higher multiples driven by several factors.

We remain constructive on prospects for the cycle. Attention is focused on late cycle indicators, while early cycle indicators have been turning up. We see various aspects of the cycle yet to kick in, including de- to re-stocking; capex outside Tech; capital markets and M&A; loan growth; and rest of the world growth. With potential policy changes by the incoming administration having both positive and negative implications for growth, sequencing will be key, but we expect growth to remain the priority. Over several rounds of the last trade war, escalations saw equity selloffs which then prompted de-escalations.

Robust steady earnings growth to continue; high multiples to sustain if not push higher. Like our house economics view, we see steady robust momentum continuing into 2025, with EPS growth of 11.6% to $282. At 24x, the S&P 500 trailing multiple is well above the historical average of 15.3x and the 10x-20x range that prevailed. We see a number of drivers behind the rise: payout ratios running around 80% over the last decade, significantly above the 50%-60% historically; earnings growth over the last decade of 9%, well above the trend rate of 6.5%; the frequency of large (10%+) earnings declines has fallen notably.

2025 year-end S&P 500 target 7000. From a demand-supply perspective, positioning is already near the top of its long-run band with little room to rise. We see robust inflows continuing, though are factoring in some slowing. We see S&P 500 buybacks rising from $1.1 trillion currently to about $1.3 trillion next year, rising in line with earnings….

…Our S&P 500 target of 7000 is in the middle of the post-GFC trend channel

Recent data show the economy continuing to grow at a solid pace, led by consumer spending.

We expect shelter inflation to trend lower over time, helping to bring overall inflation down closer to the Fed's 2% target.

Our base case remains that the Fed will cut by 25bps in December, then slow to a once-per-quarter pace in 2025.

…Policy With the new administration taking over on 20 January, policy uncertainty is unusually high. Republicans will have only a narrow majority in both chambers of Congress, and it remains to be seen whether they can successfully pass major fiscal policy changes under the reconciliation process. Meanwhile, the ordinary budget will require 60 votes in the Senate and therefore can only pass with bipartisan support. In our view, the large structural budget deficit will limit the scope of any fiscal stimulus measures. Proposed policy changes that can be implemented under executive authority are more likely to actually happen, but these include mass deportations and tariff hikes, which we would expect to be negative for growth. Regarding monetary policy, the market has priced out some Fed rate cuts recently (Fig. 4), but we still expect the Fed to cut rates a total of 125 basis points by the end of 2025, bringing its target range to 3.25-3.5%, in line with our estimate of neutral. However, if inflation proves to be stickier than we expect, then the Fed would likely end up leaving rates closer to 4%.

Government by social media—US President-elect Trump pledged to hit US consumers with aggressive consumption tax hikes immediately on taking office. A 25% tax for consumers of Mexican and Canadian goods and an additional 10% tax on consumers of goods from China is proposed.

These taxes may be bargaining tools (they are linked to drug trafficking and immigration). That could mean they are a short-lived gesture. However, there is little time to stockpile goods. The taxes apply at point of import, so an additional 10% tax on goods from China implies consumers pay 4% more (on average) for those goods in stores. Areas like the auto sector, which has highly integrated supply chains across the Mexico-US and Canada-US borders, are very vulnerable.

The US conference board consumer confidence data is due, and will be distorted by partisan bias. Because Republicans tend to be more emotional than Democrats in survey responses, the net effect of Republican euphoria and Democrat despondency should be higher sentiment…

… and stocks for the long run guy says …

WisdomTree: Prof. Siegel: Economic Resilience Continues to Impact Rate Outlook

…The outlook on Federal Reserve rate cuts is continually being reassessed and recalibrated. The July 2025 Fed Funds Futures suggest rates may only decline to around 4.1% by the middle of next year, implying many fewer cuts than previously anticipated. This reflects a reassessment of the so-called equilibrium rate—what I call the "R-star (R*)." I estimate this equilibrium short-term rate to be between 3.5% and 4%, significantly higher than the Fed’s projections. The Fed is unlikely to reduce rates as aggressively as many hoped.

While one-year inflation expectations have moderated to 2.6%, longer-term expectations have ticked up, with the University of Michigan reporting a 3.2% reading for five-to-ten-year inflation. This is the highest since the pandemic and warrants attention, as it is well above the Fed’s 2% target. However, stabilized commodity prices and the prospect of rental rate deceleration provide a counterbalance, suggesting inflationary pressures are unlikely to spiral out of control.

… And from Global Wall Street inbox TO the WWW …

… First up, returns of stocks during this, the last week of November …

BESPOKE

The last week of November has been positive for six of the last seven years, but the one down week (2021) was the fifth worst of the post-WWII period.

US 10-year Treasuries have sold off sharply since their mid-September highs (by 4.3%, see fig 1). In the main, that’s been driven by rising inflationary concerns because of Trump’s plans to (i) impose tariffs (i.e. increasing goods prices); and (ii) deport ‘millions’ of undocumented workers (thereby tightening the labour market and, in theory, increasing wages & services inflation). Other factors have added to weakness in the bond market. US macro data, for example, has been better than expected (and rate cuts for 2025 have been rapidly priced out). There have also been concerns about the (coming) increase in US government indebtedness.

… Furthermore, our medium term models are generating a clear set of BUY signals for US Treasuries. That includes our medium-term technical scoring system, which has generated timely signals in recent months (see fig 1a), as well as measured sentiment readings (which are now bearish/back on BUY, see fig 1b). Elsewhere short positioning in 10 year Treasuries is crowded (fig 1c), while net shorts in 5-year bonds are at record-high levels (fig 1d). Short (or UW) bonds is now, therefore, a consensus trade (and a near-term rally is likely).

Fig 1d: 5-year USTs net speculative positioning vs. 5-year USTs futures price

… and did someone say 60/40 ?? why, yes, yes they did …

Paulsen Perspectives: The 60/40 Portfolio's 4% Trigger The "Relative Cost" of the 60/40 Balance Portfolio skyrockets when the 10-year Treasury bond yield is below the 4% Trigger.

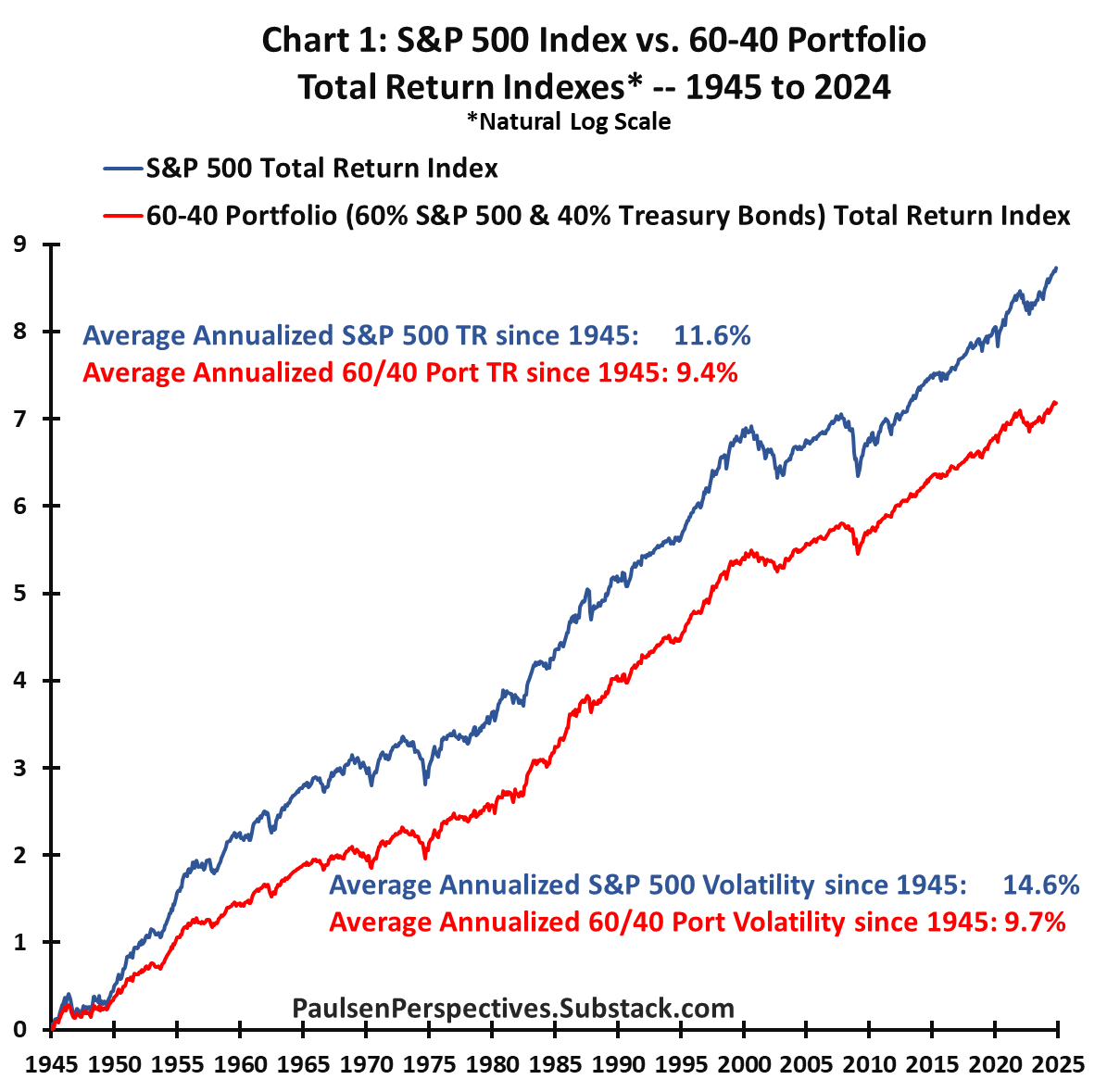

The 60% stocks, 40% bonds portfolio – the 60/40 – has long been a popular approach for investors. It succeeds in providing a decent growth in wealth over time but with a significant reduction in the emotional portfolio swings of an all-in 100% stock portfolio. Although the “balanced” 60/40 asset mix reduces volatility, it comes with the cost of a lower long-term return.

Since 1945 (chart 1), the 60/40 balanced portfolio has delivered a 9.4% average annualized total return, which is 2.2% less than the 11.6% total return achieved by the S&P 500 Index. However, the annualized standard deviation of monthly returns for the 60/40 portfolio was only 9.7% compared to 14.6% for the S&P 500 Index. This trade-off is well known by seasoned balanced investors – since 1945, the 60/40 portfolio has generated about 33% less volatility at a cost of about a 20% lower total return.

What may be less appreciated, however, is that the “cost” of the 60/40 mix (i.e., its underperformance relative to the 100% stock portfolio) varies widely over time depending most importantly on the level of the 10-year Treasury bond yield. Chart 2 demonstrates the specific impact the level of the 10-year yield has had on the cost of the 60/40 combination since 1945. This chart shows the average annualized return differential between the S&P 500 Index and the 60/40 portfolio (i.e., the “cost” of enjoying the lower volatility associated with the 60/40) for each Treasury Yield decile since 1945. The specific yield range for each yield decile since 1945 is displayed along the horizontal axis.

Clearly, the cost of investing in the 60/40 goes up considerably at lower bond yields and becomes much cheaper at higher bond yields. What is perhaps most interesting, however, is this relationship is far from linear. The average annualized cost of investing in the 60/40 portfolio when the bond yield is in its lowest four deciles is an alarmingly high 5.5% average annualized loss of total return relative to owning the 100% S&P 500 portfolio. By contrast, when the 10-year Treasury yield is in its historical top six deciles, the average annualized cost of implementing the 60/40 mix is only 0.73%.

As shown in chart 2, the upper end of the fourth decile for bond yields since 1945 is about 4%. For whatever reasons, the cost of owning a 60/40 portfolio has historically changed radically around a 4% 10-year Treasury yield. Below a 4% yield, the average cost of the 60/40 portfolio is nearly prohibitive whereas once the bond yield rises above the 4% level, its cost becomes almost de minimis. Essentially, at least since 1945, the 4% bond yield has acted as a “Trigger” or toggle switch significantly altering the cost of investing in the 60/40 portfolio.

I am not sure why a 4% bond yield impacts the cost of balanced portfolio so dramatically. But my guess is it has something to do with the relationship between the 4% coupon offering for bond holders compared to the growth rate of the overall economy and what this implies for corporate profit growth. Since 1947, overall average annualized U.S. nominal GDP growth has been 6.4%, comprised by 3.1% real GDP growth and 3.3% inflationary growth. Over time, corporate profit growth has been slightly greater than nominal GDP growth, rising at an average annualized pace of 6.9%. The balanced portfolio seemingly does okay as long as there is a meaningful buffer (a 4% or more coupon payment on the bond portfolio) to offset the boost the stock market receives from an almost 7% annualized profit gain. If the bond yield is less than 4%, it hardly covers the annual inflation rate and becomes a rather paltry return relative to average profit gains for stocks. But once the bond yield rises above 4%, the balance portion of the 60/40 can be expected to generate positive real returns and some reduction in the gap caused by profit gains accruing to stock investors.

Whatever the reasons behind its existence, 60/40 investors need to be mindful of the 4% Trigger!

The 10-Year Treasury Yield Currently Hovers Just Above the Trigger!

This Trigger would not be very important today if the 10-year bond yield were 2% or 6%. But, currently, the 10-year Treasury yield closed Friday at 4.4% and sits only 40 basis points from the toggle switch. If yields keep rising in 2025, then 60/40 investors can continue enjoying a relatively low-cost investment strategy offering returns close to an all-stock portfolio with lower volatility. However, should the 10-year yield soon again have a 3-handle, the cost of 60/40 investing is likely to skyrocket.

As I recently discussed in earlier missives, my expectation is for economic momentum and bond yields to decline again in the coming year. If correct, the returns from the 60/40 mix could prove more disappointing relative to overall stock market returns than expected.

Final Commet

The 60/40 balanced portfolio makes sense for many investors and there is no reason to abandon balanced management even if the 10-year Treasury yield does decline again below the 4% trigger. However, 60/40 investors may want to consider occasionally altering the balance mix depending upon which side of the Trigger they find themselves. If you generally are a 60/40 investor, perhaps you could adopt the simple rule of being 50/50 when above the yield Trigger and switching to 70/30 when below the yield Trigger. Depending on each individuals’ risk tolerance, this “toggle approach” may not be appropriate. But for those balance investors who may want to try and take advantage of the 4% Trigger and keep the “relative cost” of balanced management reasonable, adjusting the mix slightly around the toggle may prove profitable perhaps as soon as in 2025.