Good morning … the BoJ has thrown in the proverbial towel and while not exactly the same as the ECB circa 2011 … Google searched and AI helped …

In the first quarter of 2011, ECB president Jean-Claude Trichet raised the benchmark rate by 25 basis points (bps) due to concerns about inflation. In July 2011, the rate was increased again to 1.5%. However, on November 3, 2011, the ECB cut interest rates to 1.25% due to growing fears of contagion…

… for MORE, a quick walk back down toothpaste / tube analogy memory lane …

Bloomberg: ECB Unexpectedly Cuts Rate as Draghi Rules Out Debt Backstop

The European Central Bank unexpectedly cut interest rates at Mario Draghi’s first meeting in charge even as the new president signaled no plans to backstop the region’s most vulnerable nations as the escalating debt crisis threatens to splinter the euro region.

“What makes you think that becoming the lender of last resort for governments is what you need to keep the euro region together?” Draghi asked reporters in Frankfurt today. “That is not really in the remit of the ECB. The remit of the ECB is maintaining price stability in the medium term.”

… and a star then was born …

… un hiking trying to put the toothpaste back in the tube, it’s likely as close we’re gonna get to seeing the BoJ PUT reemerge at this point …

Bloomberg: BOJ Sends Dovish Signal After Rate Hike Sparked Market Meltdown

Uchida notes importance of keeping policy easy for now

Sees no risk of BOJ falling behind the curve on rates

… “I believe that the bank needs to maintain monetary easing with the current policy interest rate for the time being, with developments in financial and capital markets at home and abroad being extremely volatile,” Uchida said in a speech Wednesday to local business leaders in Hakodate, northern Japan…

AND another star was born ? I’ll continue (sorry) …

ZH: Capitulation: Yen Plunges, Nikkei Soars After BOJ's Uchida Says "Will Not Raise Rates When Markets Are Unstable"

… For confirmation one has to look no further than the yen which immediately tumbled by more than 2% against the dollar...

.... and Japanese stocks soared immediately after his comments...

... which were not only the first public remarks by a BOJ board member since the bank hiked interest rates on July 31, but also the first remarks to admit that last week's rate hike had been a catastrophic policy error.

…. and since I missed DIP-ortunity yesterday to have a look at 3yy ahead of the auction and so, here’s a quick review of how THAT liquidity event came and went …

ZH: 3Y Auction Stops Through Despite Yield Plunge To 16 Month Low

… Overall, this was a solid if not spectacular auction, one where despite today's jump in yields, demands was clearly present, if hardly spectacular. And even though the auction left little to be desired, the continued unwind of the recent flight to safety meant that yields rose to session highs despite the solid reception …

… time will tell BUT momentum (overBOUGHT / SOLD not great indicator in a bull market — see end of 2023 for reference / context) has crossed and BEARS currently in control ever since ISM …

… #Got10s? … here is a snapshot OF USTs as of 636a:

… and for some MORE of the news you might be able to use…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

ABNAmrofixed income - when US recession fears ebb, credit spreads will make a comeback

In this comment we analyze the sell-off in various spread sensitive European fixed income markets. European credit bond markets were obviously not immune to Monday’s market turmoil and the key gauges for synthetic credit spreads moved sharply, with 5y CDS spreads on the Itraxx main and cross-over widening by 5bp and 35bp respectively since Friday. Swap spreads and semi-core / peripheral country spreads reached levels seen during the French snap election. One could perhaps argue thin holiday liquidity as the key culprit behind the sharp moves. Looking back at summer months (July and August) over nearly 25 years, 16bp of widening in spreads on the broad corporate debt index actually looks reasonable in comparison to the spread widening during 2018 and 2019 for example. Actually, the absolute level of spread widening today is not meaningfully different than to 2018 when there were fears about too much central bank policy tightening as well.

OPEC+ retains its plan to revive production starting October. Chinese lower than expected demand in the second half of 2024, fears of recession in the US along with higher supply by Non-OPEC+ producers have put downward pressures on prices. However, the geopolitical premium following the resurgence of tensions in the Middle-East is keeping prices in check. Our outlook for Brent is to average 85 $/b in Q3 and Q4 as the economic recovery in main markets takes more time to gain momentum.

BARCAP: China: Exports lose steam (as goes China, so goes rest of world?)

China's export growth missed consensus by a wide margin, reversing the upward trend, with slowing shipments to EMs. We see signs of headwinds to exports in H2, with a reversal in the global manufacturing upcycle, a slump in the exporter-oriented Caixin manufacturing PMI, and rising trade tensions with EMs.

US equities have moved from a healthy correction into a full panic: We wrote in Selling triggers (07/24) that we would be cautious buying into the first leg lower in the market, given the fragility in positioning. The risk was that a more correlated move could elicit more index volatility and in turn systematic selling. That has played out at the start of this week with 95% of the names in the SPX and all eleven sectors down on the day. The VIX had a huge spike, hitting over 60, before reverting to 30s intraday on Monday. In the short term, the move might point to a capitulation. The SPX drawdown has reached a 10% peak to trough move in under a month. We think this could now offer opportunities to tactically add risk in higher conviction names. We have produced a basket of stocks (BNPUBWBW index) that had greater than +3% one day move on the respective earnings releases dates, but are now trading lower through the earnings season. For these names there is a risk of ‘throwing the baby out with the bath water’.

Throwing the baby out: The three largest names in the ‘Baby With Bath Water’ basket (BNPUBWBW index) are AMD, BAC and META. These are candidates for owning upside optionality to play a rebound the market. Our preferred implementation is trading either call spreads for names that have had a significant correction, or 1x1.5 call ratios. Call spreads line up well to play a quick bounce back towards highs. But call ratios could mark better on a slower rebound given we see scope for vol to soften if spot rallies.

After a Manic Monday, the Eternal Flame of optimism was relit yesterday with a sizeable rebound in risk that started with the Nikkei up over 10% and ended with the S&P 500 gaining +1.04%, ending three days of consecutive losses that wiped out around 6% of the index’s value. As equities recovered, 10yr Treasuries sold off as demand for safe assets faded…

…This is part of a wider risk-on move in Asia with the Topix (+3.30%) leading gains with the Nikkei also rising +2.28% following BOJ’s Deputy Governor Shinichi Uchida sending a strong dovish signal by playing down the chances of near-term rate hikes when markets are this volatile. As a result we are seeing a sharp decline in the Japanese yen, down -2.20% to trade at 147.60 against the dollar while the yields on the 10yr JGBs are -4.2bps lower standing at 0.845%. Remarkably Japanese equities are now flat on the week so far. Elsewhere, the KOSPI (+2.42%) is also edging higher with the Hang Seng (+1.36%), the CSI (+0.19%) and the Shanghai Composite (+0.31%) also trading in positive territory…

… Today’s CoTD is mostly for us to consider whether the moves in markets and particular the stunning moves in the VIX yesterday were actually a normal response to the stage of the cycle we are or whether it's simply a coming together of unique temporary forces that have been exacerbated by terribly thin August trading liquidity.

The chart is one we’ve used for the last couple of Fed cycles showing the 25-month lag between the VIX and Fed Funds, and one we repeated at the start of this year. It suggests monetary policy impacts the VIX with just over a 2-year lag. For the record it was back in June 2022 when the Fed moved rates up by the first of their four 75bps hikes before the end of November that year.

Clearly the graph only has a track record of a few cycles and is better at suggesting potential turning points rather than predicting exact numbers. However given we’re just over 25 months from the start of the period where the Fed started to move rates up by 300bps in 5 months, the relationship has been remarkably predictive in this cycle whether that’s completely coincidental or not.

The biggest caveat here is that this is a 3-month moving average series for the VIX and also takes month end points…

…My base case is that these violent moves of recent days are being massively exaggerated by illiquid August conditions but I wouldn’t dismiss the lag of monetary policy being a factor to some degree. One to watch as we go back to school even if we’ve calmed down by then.

DB US Economic Chartbook - Monthly charts: Fed hoping to take the long view as markets burn out on soft landing

… Financial conditions consistent with sturdy private domestic demand growth in near-term

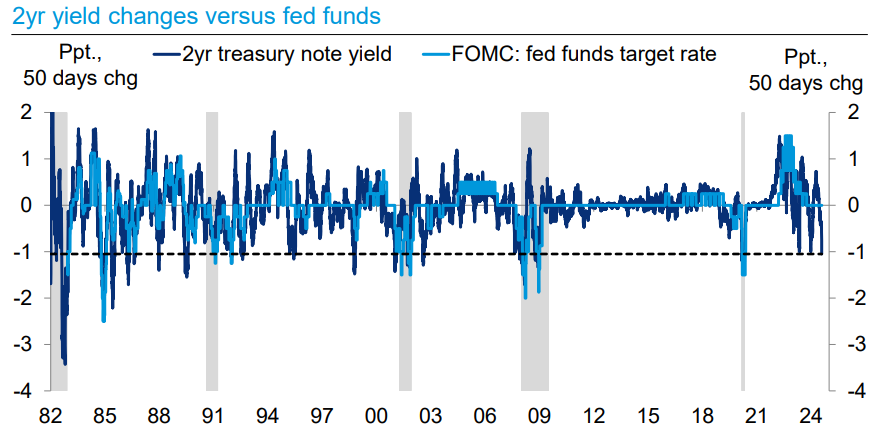

… Decline in 2-year yields around magnitudes where rate cuts typically follow

Real monetary policy stance reaching elevated levels from a historical perspective, raising downside risks

Bank of Japan Governor Uchida indicated that there would be a pause in interest rate hikes in the wake of the strong financial market reactions. Central banks are not supposed to create disorderly markets, so this is not necessarily surprising (the last rate hike will not be reversed). The political pressure on the BoJ to raise rates was not properly backed by economic fundamentals—there is a lesson there for all central banks.

Japanese equity markets have now almost entirely erased the plunge on Monday. Economic fundamentals have not changed that much this week. Draw your own conclusions about markets’ relationship to economic reality.

China’s July export data was weaker than expected—there are still discrepancies in the details (China exports 16% more to the US than the US imports from China). German export data for June also disappointed. Consumers preference for fun over goods is an ongoing trend, and Germany and China export goods rather than fun. Weaker exports from China raise questions over the 5% GDP growth target.

US June consumer credit data is due. While the Federal Reserve is late in cutting rates, the real cost of borrowing money has not really moved this year (borrowers’ real interest rates are discounted by income growth).

UBS: US Equity Strategy (Golub — one of Global Walls popular kids … assures)

Once Again, Reiterating 5600 YE 2024 Target

In mid-July, as the S&P 500 surpassed our 5600 target, we explained why we were sticking to our forecasted year-end level (effectively calling for a flat market through December). In that note, we highlighted a number of tailwinds including: (1) an economy that was slowing but non-recessionary, (2) S&P 500 profits that were robust and broadening, and (3) interest rates and inflation that were on the decline. We also explained that a depressed Vix and elevated valuations were headwinds.

The S&P 500 is down -8.5% since that time. On the positive side, valuations are lower and volatility higher, both supportive of positive forward returns. With 78% of market cap reported, 2Q EPS are expected to have grown 9.8%, 10.6% assuming continued beats. Companies have surprised by 4.7%, in line with long-term averages. However, payrolls and claims continue to deteriorate at a modest/steady pace…

BREAKING NEWS: Deputy BOJ Governor Uchida said that the central bank won't raise interest rates when markets are unstable. His dovish remark gave a broad lift to risk-on appetite in Asia. We wrote the following before this news came out.

The global stock market panic calmed down today as the most overleveraged trades seem to have been washed out. We didn't view the extreme selloff over the past two trading sessions as being fundamentally driven. So we suggested that investors remain Zen rather than panic over the rebound in the yen, which triggered the unwinding of carry trades around the world.

Perversely, had the hard landers calling for the Fed to cut interest rates in July gotten their wish, the fallout from the carry trade unwind would have been even worse. The yield spread between the US and Japanese 10-year government bonds would have narrowed, putting even more upward pressure on the yen (chart). Some of those same hard landers are calling for an emergency rate cut now, all while the US economy remains in good shape, in our opinion.

Meanwhile, the 10-year US Treasury yield is already back to 3.91%, confirming there's no recession looming. The S&P 500 is 10.5% higher ytd. We expect some sideways chop over the coming months and are mindful of looming risks in the Middle East, but we remain positive on US economic growth and on US equities…

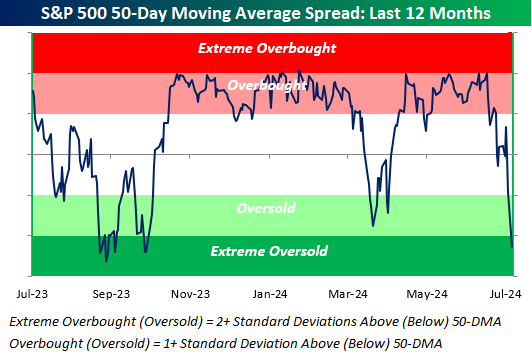

After three straight days of 1%+ drops, the S&P 500 finally hit extreme oversold territory yesterday by moving more than two standard deviations below its 50-day moving average. Below is a chart that's included in our Morning Lineup every day to help investors gauge overbought/oversold levels. It's a helpful way to get a quick check-up on the market. Sign up for Bespoke Premium with our Dog Days Special to receive our Morning Lineup in your inbox for a 50-day trial.

In addition to the chart above, we also featured the chart below in today's Morning Lineup. Here's the text that was included for subscribers:

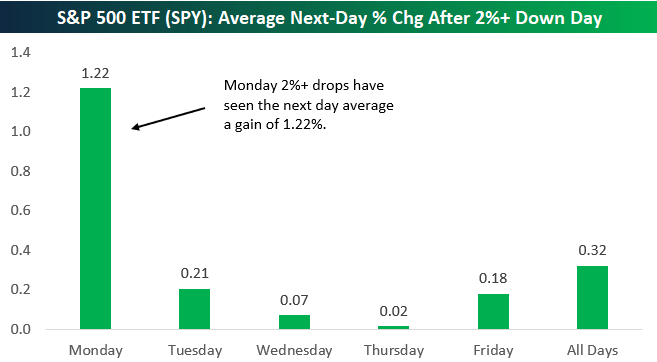

Yesterday was the 330th time that the S&P 500 ETF (SPY) has seen a one-day drop of more than 2% (since it began trading in 1993). It was also the 61st time we've seen a 2%+ decline on a Monday. Below is a look at the average next-day percentage change seen for SPY after 2%+ drops by weekday. As shown, Monday drops of 2%+ have by far seen the biggest bounce back on the following day, with an average next-day gain of 1.22%. As we've said in the past, there's a reason the term "Turnaround Tuesday" exists.

We'll be watching the tape closely this afternoon to see if this morning's bounce can hold into the close. …

Bloomberg:The Fed’s Wild Ride Has Just Begun (Dudley OpED basically an I TOLD YA SO)

Is the US in a recession? Expect more volatility as markets and central bankers figure it out.

… Two weeks ago, I switched allegiance from hawk to dove, dropping my support for higher interest rates and arguing for immediate cuts to avert a recession. Not a moment too soon, it turns out. Since then, evidence of a weakening labor market and moderating inflation has accumulated rapidly, strongly suggesting that the Fed is behind the curve…

… Many economists — including Claudia Sahm herself — argue that the Sahm rule doesn’t necessarily apply this time: Strong labor force growth, rather than firing, has driven the rise in the unemployment rate. “A statistical regularity is what I’d call it,” said Fed Chair Jerome Powell, when asked about the rule. “It’s not like an economic rule where it’s telling you something might happen.”

They might be right, but I wouldn’t base monetary policy on that assumption…

Bloomberg: Markets must navigate well beyond one bounce (Authers’ OpED)

The selloff’s damage to the tectonic plates of global finance won’t be clear for weeks.

ING Rates Spark: Recovery of market sentiment helps yields nudge up

An improvement in market sentiment stemmed the equity sell-off and helped yields stabilise or nudge higher. Bund yields are likely to remain trading at lower ranges as eurozone recession risk is in the back of the mind of investors. US CPI numbers next week will be the next key data point to decide on the direction for rates

… and with THAT in mind, a quick pictoral review of ‘How Wall Street Works’ via X

… Emergency CUT they said … AND … THAT is all for now. Off to the day job…