while WE slept: 'Treasuries lower but above Tuesday's 109-07 base'; Trump Re-election Odds & 30y Realz (Citi); "Taking time means tightening" (UBS) and ... {WSL ELECTION<Go>}

Good morning … with even less than a little to add ahead of what many / most market participants will view as a 5d weekend ahead (think ‘Hamptons Hedge’ shortly after the 10a data … IF folks last that long), a look at 2yy

2yy: bullish momentum on longer-term charts and now a couple data points creating a new (green)TLINE …

… this is accompanied by a DAILY look as it is, in my view, the very definition of ‘time at a price’ whereby bearish momentum ‘resolves’ not by trading much HIGHER in yield … that proves a desire to not stray too far from the Team Rate CUT stable and willingness to buy dips (?) … in any case, SUMMER = narrow range and one we shouldn’t likely infer too much from …

… In as far as some current math, JPOW + JOLTS = bond BID …

CalculatedRISK: BLS: Job Openings "Little Changed" at 8.1 million in May

ZH: Job Openings Unexpectedly Surge, Driven Entirely By Government Jobs

… added together, ZH made this of it all …

ZH: Bonds & Stocks Bid As Government Job Openings Suddenly Surge

Despite the near-perfect track record of downward revisions over the last 17 months, the market seemed buoyed today by a better than expected JOLTS print - which was juiced almost entirely by government jobs

And that was enough to send rate-cut expectations (dovishly) higher

Which pulled stocks and bonds higher in price...

… here is a snapshot OF USTs as of 646a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Europe bolstered by the Wall St. handover heading into a frontloaded US docket … Stateside, Treasuries lower but above Tuesday's 109-07 base as we enter a packed and frontloaded session on account of Thursday's US Independence Day; data, FOMC Minutes and 3,10,30yr size announcements the highlights.

Openings retraced a downward revision to the April reading, placing the level close to March's reading. Meanwhile, the hiring rate firmed a bit from April, with the quits and separation rates unchanged. Signs of stabilization should dampen speculation about deteriorating demand as we await Friday's payrolls.

Citi US Rates Reveille | July 2nd, 2024 (incl yesterday’s note as it hit AFTER I hit send — mentioning gone now for NEXT 2wks — AND ‘cuz it’s got a great chart of PredictIt Trump Re-election Odds & 30y Real Rates…main stream picking up on ONLY this and important to note, this only one of the inputs … still, a great visual IF in a binary world…)

… While the linear comparison between long-end real rates and Trump re-election odds show spurious correlation over the last few quarters, the recent sensitivity is hard to ignore, alongside the churn higher in the USD despite contained rate differentials. Still, we see a few more contributing factors in the selloff that is now within striking distance of notable trend supports (like 4.50% in 10s).

… US Rates: The market’s Fed expectations remain the dominant driver of Treasury yields, and are likely to be the key factor in determining the direction of travel over 2H24. We forecast a 25bp cut in November, followed by a quarterly cadence of cuts. It remains likely this easing cycle will be shallower and perhaps more closely resemble the 1995 and 2019 easing cycles rather than the aggressive easing cycles during the 2001 recession and the GFC in 2007-2008.We believe there is still room for yields to decline. We forecast yields biased somewhat higher through the summer as markets push back on the expected timing of the first cut, but then declining again in the fall as the first ease approaches, with the curve bullishly steepening in the process.

UBS: Taking time means tightening (Team Rate CUT weighing in here…)

Federal Reserve Chair Powell said yesterday that the strength of the US economy and labor market meant the Fed could take its time in cutting rates. This is a rather risky point of view. US inflation has collapsed more than eight percentage points, and the harmonized measure is below 2%. Taking time means tightening policy further. Can the US economy withstand more tightening?

Powell seems to have a rather trusting belief in the precision of economic data. The declining accuracy of data reduces certainty about the state of the US economy. While a soft landing seems to have been achieved, looking across a broad range of indicators there are signs of strain (perhaps especially in the labor market)…

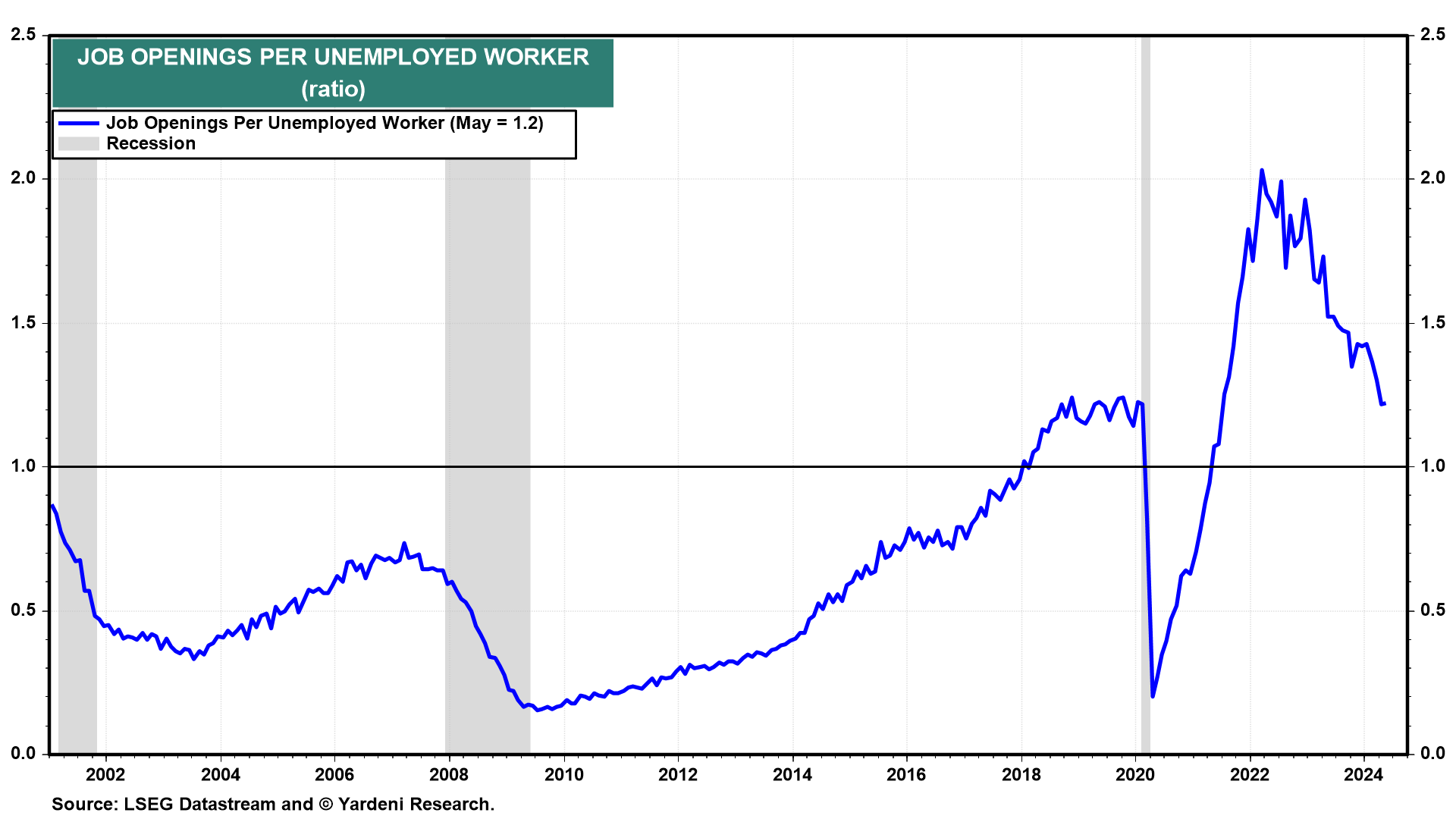

Summary May's JOLTS report showed a labor market that in many ways looks like its pre-pandemic self. Job openings partially rebounded from the three-year low hit in April, but the number of job openings per unemployed worker remained unchanged at 1.22, essentially back in line with its 2019 average. Turnover, meanwhile, remains depressed. Gross hiring stayed near the lowest share of total employment since 2015, and businesses are reluctant to cut ties with existing workers as indicated by the layoff & discharge rate remaining near a historic low at 1.0%. The share of workers quitting their job also remains below the rate registered prior to the pandemic, which, along with the downward trend in demand for new workers, should continue to temper wage growth.

Overall, the JOLTS data suggest that the jobs market continues to move toward its pre-pandemic state, but at a pace that warrants caution more than alarm. The resumption of inflation's downward trend in recent price data along with the reduction in inflation pressures stemming from the cooler jobs market leads us to continue to look for the Fed to reduce the fed funds target range as early as its September 18 meeting.

Source: U.S. Department of Labor and Wells Fargo Economics

Wells Fargo: Benefit of the Doubt: Consumer Confidence & Elections

Summary Despite widespread expectation for the U.S. economy to be in recession in 2024, that fate has been avoided thanks to a resilient U.S. consumer. Yet it is difficult to square this undaunted spending with consumer confidence and sentiment readings that are lackluster at best. How can economic conditions be adequately supportive of actual spending but insufficient to imbue a greater degree of confidence?

Perhaps it has to do with the fact that while inflation has come down, prices themselves largely have not. It may also have to do with a labor market in which the jobless rate remains near all-time lows, but the signing bonuses have mostly gone away and record wage growth has largely cooled. Yet, we would be remiss not to acknowledge the upcoming general election in November. Politics aside, households face uncertainty over the presidency, the makeup of Congress and what those outcomes imply for future policy paths. In previous general election years, this has resulted in declining consumer confidence measures in the months leading up to the election in November and a trend recovery in the months following an election. Should we expect the same this year?

The S&P 500 jumped to a new record high of 5509 today on better-than-expected Tesla vehicle deliveries. In addition, today’s JOLTS report showed more job openings. Nevertheless, two Fed officials suggested today that the Fed Put is back because they are worried that the Fed might cause job losses if monetary policy stays too tight for too long. Their dovish comments reinforced expectations that the Fed will cut the federal funds rate by 25bps at least once and maybe twice over the remainder of this year (chart).

Here's more on today's economic developments:

(1) Job openings. The labor market remains relatively strong. Job openings rose 221,000 to 8.14 million in May. Job openings per unemployed worker remained steady at 1.2 in May (chart). That's well off the 2.0 peak during March 2022. But it remains relatively high.

… I’m sure there’s more ‘out there’ and if you see / have something you’d like to share, by all means … phone lines are open, 2 traders NO waiting :) and in meanwhile, I’ll move along and away from Global Wall Street inbox TO the WWW,

Bloomberg: Powell Welcomes Recent Data But Fed Needs More Confidence to Cut

Latest price data offer signs US back on disinflationary path

Fed chief speaks on panel in Sintra with Lagarde, Campos Neto

Bloomberg: Markets are raining on Biden's Fourth of July (Authers’ OpED)

Betting and bonds deliver cold, harsh truths about the odds of Trump 2.0 since the presidential debate disaster.

… The Dreaded Bear-Steepener The theory that’s taken hold in the last few days is that Trump 2.0 is moving the bond market. The US yield curve has been inverted — meaning that short-dated bonds yield more than longer-dated ones — for a long time, but of late there has been what is known in bond market lingo as a bear-steepener. Yields have gone up (hence bearish), but that’s almost all been about a rise at the long end (hence steepening).

We shouldn’t make too much of this. The curve is still inverted, and the 10-year yield is lower than only a few weeks ago. But the wayit has jumped while the two-year has stayed in place is unusual, and there might be a political cause. If Trump goes through with tax cuts, the odds are that he will be very good for stocks, but not bonds. Larry McDonald, of the Bear Traps Report newsletter, puts it as follows:

The curve steepens because a new Trump term would mean more tax cuts, higher budget deficits and, almost by definition, higher GDP growth. But if that is the case, the Russell needs to outperform. So either bond vigilantes are wrong or equity investors are wrong, but this divergence cannot last for long.

Certainly the main elements of the Trump economic platform — tariffs and unfunded tax cuts — look like a recipe for inflationary growth. This shouldn’t all be loaded onto Trump, as Biden is adopting key parts of that agenda. McDonald quotes a portfolio manager who told him that in the debate, both candidates “tipped their radical protectionist hand, trying to out-trade-hawk each other.” Saying that Biden was all in on Trump’s protectionism: “This is far more inflationary. The long end of the yield curve took notice; we are bear steepening.”

If Trump’s chances have clearly improved, how does this show up for stocks? Dan Clifton of Strategas Research Partners said that traders had put 50-50 odds on Trump for most of this year, but in the short run he had moved into the favorite column. He offered a list of assets that should benefit from Trump 2.0: financials, LNG exports, Medicare Advantage, for-profit education, India, and Israel should all outperform, while the victims would include anyone exposed to Mexico or China…

Bloombergs at M_McDonough (troubling but interesting but troubling, at same time)

Kamala Harris and Joe Biden's odds of securing the Democratic presidential nomination have converged: {WSL ELECTION<Go>}

The economist John Maynard Keynes supposedly said: "Markets can remain irrational longer than you can stay solvent".

My variant considers why newly-issued MBS continue to trade nearly 145bp over US Treasuries, a distress level only exceeded in the past twenty years during the 2008/09 GFC and 2020 Covid panic; a level nearly double the historical average near 75bp.

In today's Commentary - "Of Horses and Water", I drill down on this topic and offer strong support for the notion that newly-issued MBS are the best risk-adjusted bonds in the market. Moreover, I predict this pricing disconnect will resolve as Investment Managers review the six-month performance of such bonds…

ING: US jobs market reverting to pre-pandemic norms

Job openings improved, but the trend is still softening. At the same time the soft quits rate suggests the jobs market has normalised and means that inflation pressures emanating from the jobs market should continue to cool, keeping the door open for rate cuts later this year

ZH: Financial System 'Plumbing' Starts To Show Signs Of Stress Again

… Nothing out tomorrow (unless, of course something of note over holiday which I cannot resist) and at this point unsure if worth wasting your / my time to gather / send anything Friday … DEF something out ahead of Sunday evening open and in meanwhile … Happy Independence Day — THE original BREXIT!!

Happy 4th all!