Good morning … given all the ‘bla’ over the weekend (here and here), I’ll be brief this morning. I’ll also note there’s a non-zero chance of NOTHING tomorrow (may be in NYC for the day…). Sorry in advance and appreciate patience.

Now … on with the show … and by show I mean something to help pass the time between now and 9am Players playoff and brackets!

And on THAT note, off we go … First up, equity futures not allowed to capitalize on Friday’s momentum as Tsy Sec Bessent on MTP yesterday …

Mar 16 202511:35 AM EDT CNBC: Treasury Secretary Bessent says White House is heading off a ‘guaranteed’ financial crisis

… “I’ve been in the investment business for 35 years, and I can tell you that corrections are healthy. They’re normal,” he said. “What’s not healthy is straight up, that you get these euphoric markets. That’s how you get a financial crisis. It would have been much healthier if someone had put the brakes on in ’06, ’07. We wouldn’t have had the problems in ’08.”

“I’m not worried about the markets. Over the long term, if we put good tax policy in place, deregulation and energy security, the markets will do great,” Bessent added. “I say that one week does not the market make.” …

… AND with that, bonds are BID …

10yy DAILY: (green, down)TLINE approx 4.25% (4.22%) would be logical target…

… as momentum has moved out of aggressively overBOUGHT territory and not YET oversSOLD enough to make a compelling case, in and of its own, but clearly when one considers all the ‘techAmentals’ available, bonds are still NOT dead yet …

… AND the F2Q bid continues to gain facts as we like to say / think and constantly remind ourselves that narratives ALWAYS follow the price action …

Mar 17 20256:08 AM EDT CNBC: OECD cuts U.S. and global economic outlooks as Trump’s trade tariffs weigh on growth

KEY POINTS

Global growth is expected to slow from 3.2% in 2024 to 3.1% in 2025 and 3.0% in 2026, according to the OECD. It had previously forecast 3.3% global economic growth this year and next.

The U.S.’s annual GDP growth is also projected to fall to 2.2% in 2025 and 1.6% in 2026 — down from earlier forecasts of 2.4% this year and 2.1% next year.

… And for more, straight from the ‘horses mouth’ …

17 March 2025 OECD: Global economic outlook uncertain as growth slows, inflationary pressures persist and trade policies cloud outlook

The global economy has been resilient in 2024, but some signs of weakness are appearing against a backdrop of slower growth, lingering inflation and an uncertain policy environment, according to the OECD’s latest Interim Economic Outlook.

The Outlook projects global growth slowing to 3.1% in 2025 and 3.0% in 2026, with important differences across countries and regions.

GDP growth in the United States is projected at 2.2% in 2025 before slowing to 1.6% in 2026. In the euro area, growth is projected to be 1.0% in 2025 and 1.2% in 2026. China’s growth is projected to slow from 4.8% this year to 4.4% in 2026.

Inflation is projected to be higher than previously expected, although still moderating as economic growth softens. Services price inflation is still elevated amidst tight labour markets, and goods price inflation has begun picking up in some countries, although from low levels. Annual headline inflation in G20 economies is projected at 3.8% in 2025 and 3.2% in 2026. These projections have been revised upwards by 0.3 percentage points compared to our Economic Outlook in December.

… here is a snapshot OF USTs as of 720a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are bull-flattening in sympathy to Bunds (5s30s GMY -4.6bps) after the Asia reopening saw a firm start on geopolitical developments in the middle-east as well as Bessent/Trump comments. However, the early squeeze higher was quickly capped by regional accounts, with the LDN desk reporting better selling from fast$ and systematic accounts in 2s-3s. Trading volumes remain particularly thin, with a small WN buy block passing through in early London without much impact. Some long end demand was also noted from credit desks, but we've gradually backed off the flattest levels heading into the US session with volumes ~75% the 20dma. S&P futures are showing -10pts here at 7am, Crude +1.3%, Copper +0.25%, and DXY -0.2%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

Finviz (for everything else I might have overlooked …)

NEWSQUAWKUS Market Open: US equity futures are softer & Crude bid after Trump orders strikes in Yemen; US Retail Sales due … USTs await US Retail Sales before the latest update to Atlanta Fed's GDPnow tracker which is currently running at -2.4% though the gold-adjusted figure is -0.4%. Firmer by a handful of ticks but essentially contained with yields mixed and the curve flatter.

Yield Hunting Daily Note | March 14, 2025 | S&P Correction, Stay High Quality For Now, Avoid Private Debt

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

France sent this note yesterday and since it was resent, am feeling obligated due to the catchy title and in the case you missed …

17 Mar 2025 08:06 GMT BNP: Sunday Tea with BNPP: When doves cry

CORRECTION: Republished to correct reference to 10s30s EUR swap steepeners in the final paragraph.

KEY MESSAGES

Markets in the US have been attuned to rising growth risks, but at the expense of underweighting inflation risks – a bias that the Fed may not share at this week’s FOMC meeting. PCE tracking higher and rising inflation expectations suggest greater stagflation risks.

Europe’s watershed moment continues to have an impact. We now see EURUSD at 1.12 in 2025 and 1.20 next year. Key votes in the German parliament take place this week.

Against this backdrop, we see a flatter UST yield curve, lower US real yields, and a steeper Bund curve. We express EUR longs via EURCHF and EURTHB.

Here is a better-than-average run down for all our inner global macro tourists …

March 17, 2025 MS: Promises Made, Promises Kept | Global Macro Strategist

Coming to grips with the idea that President Trump is keeping promises made to reform US trading relationships, investor and consumer confidence cracked. If economic data slow, ratifying investor concerns, CEO confidence may crack next. As April 2 approaches, investor nerves may fray further.

Key takeaways

CEO confidence declined during the 2018-19 US-China trade tension alongside economic activity, but remained far from levels consistent with recession.

At the same time, global economic policy uncertainty in 2018-19 pales in comparison to the uncertainty felt today – driven by US trade policy.

Investors will look to how the Fed characterizes the growth vs. inflation trade-off and how it compares to market prices – which increasingly focus on growth.

We suggest investors remain defensive in their macro positioning. We like being long government bond duration in the US and the UK and short the US dollar.

A stock jockey began asking this question with a note yesterday and this morning finishes …

March 17, 2025 MS: Weekly Warm-up: Is the Correction Over?

With the S&P trading at the low end of our 1H range, a tradable rally is likely. Sentiment/positioning are lighter, seasonality is improving, and the DXY/10Y yield are down 6%/50bps over the last 2 months. This doesn't mean growth risks are extinguished. Volatility is likely to persist in '25.

5500 Holds, For Now…As expected and discussed in last Monday's note, negative earnings revisions breadth, fiscal headwinds, immigration enforcement, and tariffs took the index to the low end of our 1H range (5500-6100) last Thursday. However, indices also got as oversold as they've been on a daily RSI basis since 2022, sentiment/positioning gauges have lightened up considerably, and seasonals improve in the second half of March. Recent dollar weakness could provide a tailwind to earnings revisions, and the decline in rates should benefit economic surprise indices. We stand by our call from last week that 5500 should provide support for a tradable rally led by cyclicals, lower quality, and expensive growth stocks that have been hit the hardest and where the short base is the greatest. Friday's price action seems to support that call.

...But Growth Concerns and Volatility Are Likely to Persist...Policy uncertainty has only ramped up further recently, which means growth risks are likely to persist over the coming months. Perhaps even more importantly, this administration doesn't appear to be preoccupied with stock prices. In other words, we don't think investors should view a relief rally from oversold levels as a sign that volatility is subsiding in a durable manner. Not only is policy being sequenced in a more growth-negative way to start the year (in line with our views from last November), the speed and uncertainty around new policy introduction is denting investor, consumer and corporate confidence. As discussed in our Year-Ahead Outlook, we ultimately think the market will focus on the positive aspects of the Trump policy agenda (No Pain, No Gain), but the path is going to take time and is unlikely to be smooth (YE '25 base case S&P 500 target is 6500). The flip side is that the Fed does have fire power and will use it if growth (labor data, specifically) deteriorates materially, or we see stress in credit/funding markets, both of which are stable, for now.

What Are We Watching? So far this month, growth data has been ok—ISM Manufacturing and Services were above 50, payrolls were largely in line with expectations, and higher frequency initial jobless claims are not showing signs of labor market stress. To confirm that a more significant deterioration in the growth backdrop isn't taking hold, we would like to see payroll gains of at least 100k, a stable unemployment rate, ISM Manufacturing above the mid 40s, ISM Services above 50, and reaccelerating earnings revisions breadth (in line with seasonals). We also think it's important for the S&P 500 to respond to the ~5500 level given the fundamental and technical support there. If it doesn't, that's a potential sign that growth could be deteriorating faster than expected, and recession risk could be increasing along with the odds of our bear case outcome.

March 17, 2025 MS: The Weekly Worldview: Views from the other side

Divergence continues to be a theme; we revised up the growth forecast for Europe while revising down the forecast for the US for the first time in many years.

… But the bottom line is that German and therefore European growth looks better than it did just a couple weeks ago. So, it is understandable that the debates about “US exceptionalism” have been rekindled, with some speculation that Europe may overtake US growth. We do not think that will be the case, but for the near term we cannot rule it out, particularly because the risks to US growth are skewed to the downside. The market is finally realizing that the expectation for a fiscal boost in the US has been misplaced, especially for 2025. In fact, the cuts to outlays and employment from DOGE mean that we will have a contractionary impulse from fiscal policy this year. Tariffs have not peaked, but the fact that they have come faster and more broadly than we had originally thought implies a downside risk. And we continue to think that immigration restriction is an underappreciated factor that will weigh on US growth this year and next. So, we think the markets have generally taken the right macro signals, but some caution in extrapolation is needed.

This next note details the best of times and the worst of times … no, wait …

…The US government avoided a shutdown over the weekend that would have further damaged the US economy. US President Trump reiterated his intention to increase the tax burden on US consumers with widespread tariffs. Markets are not yet pricing in extreme proposals (weakness seems more about uncertainty caused by erratic policy).

US February retail sales include inflation—egg prices will increase sales values. There have been suggestions that Democrats “front-loaded” more expensive purchases last year in anticipation of trade taxes (with the negative pay-back occurring now). However, the reality for most US households has changed little—spending depends on whether generally stable fundamentals triumph over declining sentiment.

The dollar’s reserve status depends on a sense that money held in reserve in the US is “safe”. Topics like rule of law, liquidity, and the absence of capital controls create this sense of safety. Rule of law may come into focus, with weekend reports of the Trump administration ignoring court orders.

… same shop offering an educated guess

14 March 2025, 11:00AM UTC UBS: How do tariffs impact inflation?

Trade taxes, or tariffs, have been a burden for consumers for over four thousand years, pushing up prices as money is paid to the government. Today's trade is a lot more complex than it was even fifty years ago, and this makes the relationship between taxing trade and inflation more complicated than in the past.

There are eight ways in which trade taxes can impact inflation. In assessing the extent of the inflation damage, investors need to ask four questions:

How visible are the effects of the tax to the consumer, and how likely is it that the tariffs will stay in place?

How much of the tariff change will be passed directly to the consumer?

How significant will the second-round effects of the tax be?

How quickly can exporters adapt to help their overseas customers avoid paying the tax?

The net effect of tariffs will inevitably be higher consumer prices. The more complex way trade works adds uncertainty as to how much prices will rise.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

First up, one I can relate to since i’ve been doing it most of my adult life …

March 17, 2025 Apollo: Work from Home Is Here to Stay

Household surveys, entry swipes, and location data show that work from home has become a new permanent feature of the labor market, with all indicators moving sideways since 2023, see charts below…

Next up a couple OpEDS from The Terminal beginning with this statement of the obvious from one of the ‘fan favorites’ …

March 17, 2025 at 9:00 AM UTC Bloomberg: The US Economic Outlook Is Becoming More Uncertain Downward revisions to growth projections are just beginning.

Wall Street analysts and economists have converged on a more turbulent near-term trajectory for the US economy. The outlook is bumpier than anticipated, with lower growth rates, greater inflationary pressures, and more complicated international economic and financial interactions. However, opinions still diverge sharply on the longer-term prospects, with some believing the US is sharpening its “edge” as others fear it is eroding …

… While there is much more agreement now about the short-term prospects, it's too early to be confident about the US economy's destination. What seems undeniable is that the journey may get even bumpier as the world continues to react to US developments.

… AND this next OpED contains a MAY FOMC precap …

March 17, 2025 at 5:06 AM UTC Bloomberg: Selling the Family Silver, American-Style The easiest way to finance a US sovereign wealth fund could be through a massive sale of federal resources.

… A Skip to May’s Review

The next meeting of the Federal Open Market Committee is due Wednesday, but there’s a degree of assurance of its final decision. Virtually nobody sees any chance that interest rates will move, and the market has steadily converged on this view for some months:

This confidence is primarily inspired by the committee’s pivot to transparency in monetary policy since the early 1990s. The Fed adopted a form of inflation target in the middle of that decade, but it wasn’t publicly disclosed until 2012 after the Great Financial Crisis. It took numerous tweaks, such as the addition of the maximum employment mandate, before the landmark announcement under Ben Bernanke.

It’s hard to make a case against transparency as far as business decision-making processes are concerned. But exactly how inflation targets are supposed to work is tricky. This International Monetary Fund article does a better job of chronicling the journey of the framework since New Zealand first adopted it 35 years ago.

Some central banks target a numerical point, others a range. Their horizon to achieve them varies. The question is about the framework’s constraints, whether it’s too restrictive or loose to attain price stability, and whether it’s consistent with other targets of employment and financial stability. This was the focus of recent research by the Bank for International Settlements of targets at 26 central banks. Claudio Borio and Matthieu Chavaz concluded that other objectives are starting to matter more than price stability:

Under the surface, such frameworks’ flexibility has evolved significantly. On the one hand, the explicit weight on objectives other than inflation — real economy objectives such as output and employment and, to a lesser extent, financial stability — has grown. On the other hand, the pursuit of those objectives has been facilitated through greater flexibility of the horizon over which the target is to be achieved, even as the target itself has become less flexible.

Put differently, central banks are giving themselves more wiggle room. Flexibility means simply the degree to which the framework tolerates fluctuations in headline inflation and allows the pursuit of other objectives. The BIS quantified this. As more central banks adopted stricter numerical-points inflation targets (shown in the red line in the chart below), they gave themselves far more time to achieve them (in blue), granting themselves the opportunity to do other things:

Source: Bank of International Settlements

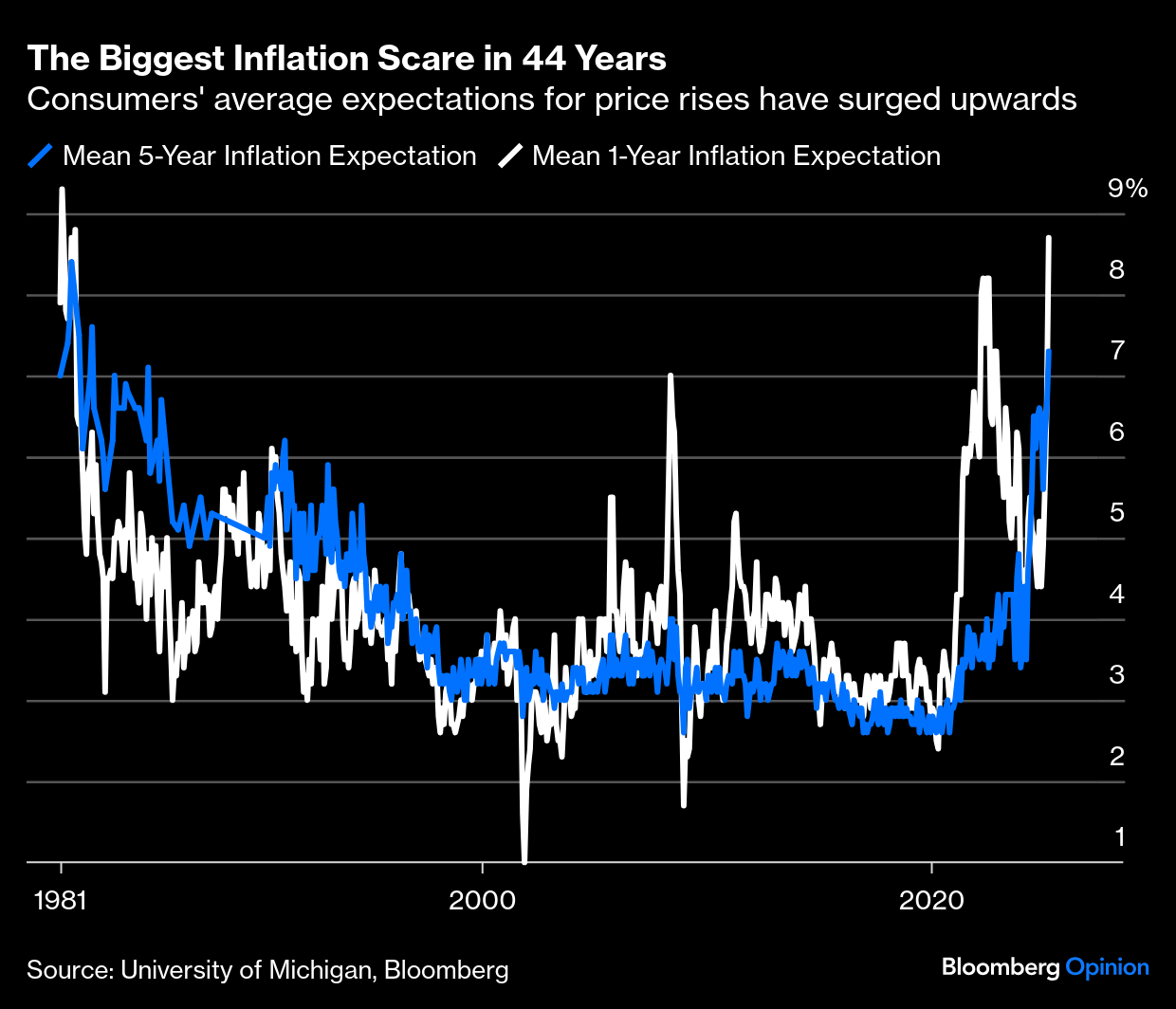

The angst about tariffs, which has come when the effects of post-pandemic inflation were only just beginning to settle, could make it harder for central banks to make their targets more flexible. The latest survey of US consumers by the University of Michigan shows that mean inflation expectations are their highest since 1981:

Expectations like that would normally require an inflation-targeting central bank to ratchet up rates. So even if its course for this week is clear, the Fed faces some difficult decisions. In May, it will host a conference as part of a regular review of monetary policy strategy. It’s focused on the FOMC’s Statement on Longer-Run Goals and Monetary Policy Strategy — which in 2020 switched to targeting an average for inflation rather than a fixed level — and its communications tools. The 2% longer-run inflation goal is under consideration, and indeed may no longer be realistic. But with inflation expectations coming unanchored for the first time in a generation, this could be a dangerous time to admit to being flexible…

… and on this St Pat’s day, my how things have changed …