5yy DAILY: momentum becoming overBOUGHT (again) BUT this makes some amount of sense as mkts price in rate cut(s) with an FOMC meeting this week to lay the foundation (but then again, if so certain needed, why WAIT — Dudley?

… 5yy in mind, seems as though markets celebrating moves Friday (despite / because of the PCE data) and way too early for ME to offer any reason to the contrary. In fact, over the weekend, when filling up the fleet here in the Garden State, regular changing hands at $2.95/gal at local Costco — price not seen in … well ..

AAA: Summer Brake? Gas Prices Stationary at the Station

WASHINGTON, D.C. (July 25, 2024)—Barely budging since June, the national average for a gallon of gas squeaked out a two-penny increase to $3.52 since last week. The national average has hovered around $3.50 per gallon since June 26th. “Some of the uptick in gasoline prices may be due to a reported storm-related outage at the ExxonMobil refinery in Joliet, Illinois. …

Good news personally, is good news! What is going on ‘out there’ is, as always, far more important … Can / will Fed help (hurt)? REMAINS TO BE SEEN and so too does my 2nd gallon of coffee and so, without further delay … here is a snapshot OF USTs as of 640a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Tepid tone emerged to the benefit of fixed and USD, earnings & Reeves ahead … Fixed benchmarks benefit from the more tepid tone, EGBs, Gilts & USTs all at/probing recent highs … USTs are bid and approaching the July high of 111-15, within half a tick of the mark at best thus far. Session’s highlight is the Treasury Financing Estimate, ahead of Wednesday’s refunding which is expected to see coupon sizes maintained for a second consecutive quarter

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ (in addition TO a couple / few weekly observations NOTED HERE) …

We expect the FOMC to lay the ground for a September rate cut at this week’s meeting. Going into the event, the Treasury refunding announcement, and nonfarm payrolls, we see 5s30s steepeners as attractive.

We look for a hawkish hold from the BoJ this week and see QT tweaks as likely to flatten the JGB curve. In FX, we think it is too soon to buy the dip in USDJPY.

In US equities, we see risks of further positioning unwinds as Q2 earnings season continues

… With the three-month average run-rate of private payrolls falling to 146k in June from 203k as recently as March, we still see risks to US rates asymmetrically skewed to the downside heading into this week’s July NFP print and favor 3m5y A/A-30bp receiver spreads and 5s30s UST steepeners. The belly of the curve should be the most vulnerable to surprises in activity data. Labor market deterioration may force the market to price in a deeper cutting cycle. We noted the asymmetry regarding the 5y point heading into last month's NFP report, where 5s react more aggressively versus the rest of the curve on downside surprises while demonstrating unclear directionality through upside surprises. We maintain this outright duration view along with a steepening bias as historical analysis shows us steepening of the curve is all but inevitable once the first rate cut is three months away. Potential upside risks to Treasury's borrowing estimates and any indication about future coupon auction size increases should support structural steepening of the curve, especially in 5s30s …

… Recapping last week now, and a sanguine PCE print on Friday saw equities recover, trimming losses from earlier in the week. The core PCE index for June rose +0.2% month-on-month, in line with expectations and a relief after the GDP report the day before hinted at a higher inflation reading. The year-on-year increase in core did come in slightly above expectations at +2.6% (vs +2.5% expected) due to upward revisions, but otherwise, the release pointed to a resilient but not overheating US economy. Supporting this, real personal spending grew by +0.2% month-on-month (vs +0.3% expected but with an upward revision to May), and personal income by +0.2% (vs +0.4% expected).

The PCE data reinforced a Fed-cut friendly market narrative, with the amount of rate cuts priced for the remainder of 2024 rising by +5.9bps over the week to 68bps (+1.3bps on Friday). The growing conviction in rate cuts drove a rally in fixed income, with 2yr Treasury yields falling -12.9bps (and -4.9bps on Friday) to 4.38%, their lowest since February. 10yr yields fell -4.5bps, thanks to a -4.7bps decline on Friday. This saw the 2s10s curve steepen +8.5bps (+0.1bps on Friday) to its steepest weekly close since last October at -19.1bps, and earlier in the week reaching its steepest level (around -12bps) since the initial inversion in July 2022 …

MS: Global Economic Briefing: The Weekly Worldview: All about consumption

Varying consumption outlooks are a big part of the differences in our growth outlooks around the world.

We want to put an economic lens on recent market moves. Equity rotations and yield curve movements have increased the focus on US economic growth, particularly the consumer. There is no question that the US economy is consumer led, and our forecasts anticipated the current slowdown. The question is whether the slowing goes too far. But the current market narrative also reveals an implicit assumption that the US is the only consumer led economy. While Europe and Asia have a larger manufacturing and export sector relative to the size of their economies, they are still “consumer led” economies in that the single greatest contributor to GDP is consumption – even in China. Differences in consumer outlooks around the world help define our views of growth around the world.

We expect US consumer spending to slow but then stabilize. The last two years of US consumption have been stronger than consensus expected, partially because of continued dissaving and partially because of the labor supply shock. Our mid-year outlook anticipated both trends ebbing and then stabilizing near this year. The Fed will welcome the slowing in the economy, because while inflation has fallen mostly through normalization of Covid frictions, they believe some slowing is necessary to make sure the last mile of disinflation happens. For the Fed, the slowing economy is a feature not a bug. We wrote about false signals in the economy a few weeks ago and the fundamentals remain solid. The unemployment rate has edged up, but to a still-low level. Consumer spending is set to slow this year, but from an unsustainably fast pace last year.

MS: Sunday Start | What's Next in Global Macro: New Candidate, Same Implications

… It’s back to looking like a close race…so get comfortable again with outcome uncertainty and the impacts of multiple scenarios …

… The impacts we’re tracking in the event of a Democratic presidential win haven’t changed, even though the ticket has …

… The business cycle is likely to matter more to markets than the election cycle in the next few months…

… Of course, this doesn’t mean that the election will have no impact on markets…far from it. We think it’s possible that market moves based on existing fundamentals could be further energized. For example, our US rates strategy team’s call for a steeper yield curve driven by lower yields in shorter-maturity bonds is underpinned by our economists’ long-standing view that inflation would ease enough to open a clear path toward Fed rate cuts this year. Such a market move could be boosted by, but does not require, market expectations of a Republican win leading to higher tariffs and related growth pressures. And following the election, history tells us the policies set in motion will matter a lot across markets. In particular, we’re eyeing impacts for Treasuries, the US dollar, and key corporate sectors that vary based on the outcome. We’ll continue to track them and keep you in the loop.

In Part I of this two-part series, we laid the groundwork for understanding what r* is, how it is measured and what the key factors are that determine it. In Part II, we attempt to tackle a more difficult challenge. How has r* evolved since the pandemic began in 2020, and where is it headed in the years to come?

Summary

In our view, r* probably has risen from the 0.50% or so that prevailed on the eve of the pandemic, but we are skeptical it has returned to the 2.50%–3.00% range that was prevalent before the 2008 financial crisis. Our working estimate for r* is currently 1.00%–1.25%.

Why do we believe that r* has not risen even more? First, labor productivity has not accelerated relative to its pre-pandemic trend. Second, the pace of globalization appears to have stalled out, but it has not fully reversed, at least not yet. The United States continues to run a sizable current account deficit, and the corresponding current account surpluses elsewhere in the world leave foreigners positioned to keep buying dollar-denominated assets in size, including Treasury securities.

Fiscal deterioration is one potential source of upward pressure on r* since 2019. Using the rule of thumb that each percentage point increase in the debt-to-GDP ratio increases long-term rates by two to three bps suggests that r* has increased by roughly 38–57 bps, all else equal, from the growth in U.S. public debt since 2019. However, we believe that at least some upward pressure on the natural rate from fiscal deterioration has been offset by structural demographic trends, namely the aging of populations in the U.S. and elsewhere.

The behavior of the U.S. economic data since the FOMC started tightening monetary policy backs up the idea that the current stance of monetary policy is restrictive, i.e. the policy rate is currently above its neutral equilibrium. The yield curve has been inverted for two years now, including shorter-dated maturities that are less influenced by term premium effects. Inflation in the United States has slowed considerably since the FOMC began increasing the federal funds rate, while the labor market is no longer as hot as it previously was.

Although r* may still be low by historical standards, we think there is a more plausible case that it may rise further in the years ahead. The outlook over the next decade is naturally more speculative, but we think the risks are clearly tilted to the upside for r*. This is in sharp contrast to the 2010s, when the risks to r* were perpetually skewed to the downside.

Labor productivity may accelerate in the years ahead as the impact from generative AI is slowly felt across the broader economy. Geopolitical tensions and protectionism are on the rise, and a steady slide and/or a sudden shock on this front could lead to a higher r* if FX reserve managers, sovereign wealth funds and foreigners more broadly pull away from the U.S. Treasury market.

The daunting federal fiscal outlook is another potential source of upward pressure on the natural rate, and a lack of action from Congress and the president could lead to a higher r* and, by extension, higher rates more broadly in the years ahead.

Is a return to r* values in the 2.50%–3.00% range possible? We believe it is possible, just not probable. The outlook for variables such as new technologies and geopolitics is highly uncertain, and demographic headwinds likely will exert a structural downward pressure on r* in the years ahead under all scenarios. As a result, we think a 2.50%–3.00% r* value is more of a tail risk than a base case, with 1.50%–2.00% perhaps more realistic.

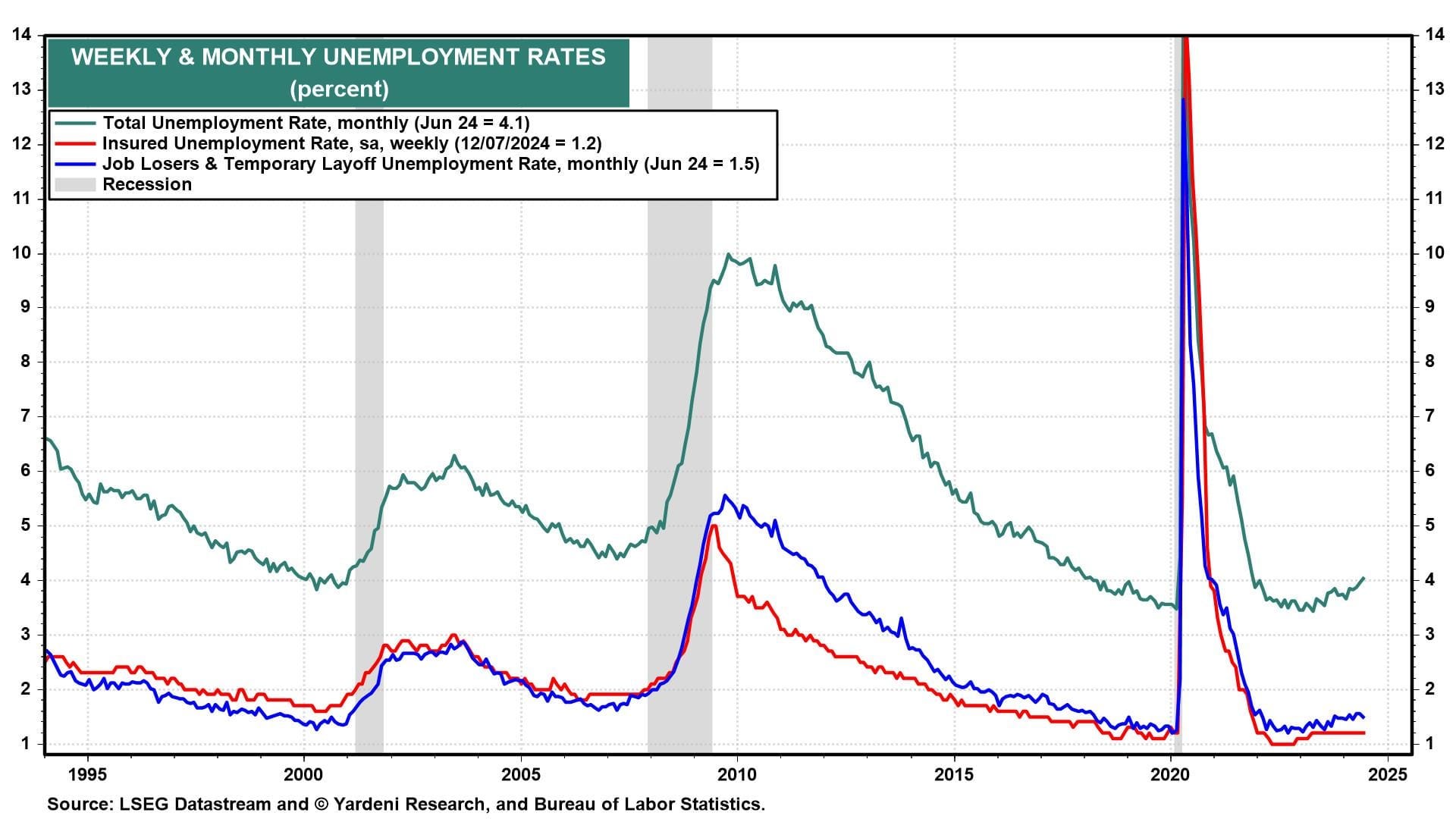

Yardeni: The Economic Week Ahead: July 29-Aug 2 (calendar in addition TO what was offered HEREover the weekend and … visual of REAL FF)

The week ahead is packed with economic indicators …

…but all eyes will be on the Fed's interest rate decision on Wednesday and payroll employment on Friday. We don't expect the Fed will alter the stance of monetary policy at the July meeting, but Fed Chair Jerome Powell could signal that a September cut to the federal funds rate (FFR) is likely. That's because as consumer inflation has fallen, the real FFR has risen (chart).

We don't subscribe to this view of measuring the restrictiveness of monetary policy, but won't ignore it since many Fed officials use it as a barometer. It's possible that the Fed holds back any signals of a policy pivot until the Jackson Hole symposium in late August. Here's what we're expecting in the week ahead:

(1) Employment. July's employment report (Fri) should show payrolls rose by 150,000-200,000 to another record high. Still, there's a decent chance the unemployment rate ticked higher to 4.2% in July. We wouldn't be concerned as rising unemployment has been fueled by a growing labor force rather than job losses (chart).

June's JOLTS report (Tue) will likely show job openings and quits remain historically high even as they fall from pandemic peaks. These series, which lag other labor market indicators by about a month, are highly correlated with the jobs-plentiful series in the Consumer Confidence survey (Tue).

… And from Global Wall Street inbox TO the WWW,

Bloomberg5 things to start your day: Europe (for visual of USTs and bond traders HOPING …)

… Bond traders are hoping the Federal Reserve will provide a dovish outlook this week which will keep the Treasuries rally going, although risks from crude oil are building. Geopolitics in the Middle East is back in focus with Turkish President Recep Tayyip Erdogan escalating his rhetoric against Israel.

That comes at a time when oil prices are edging lower on fading demand, with China a major concern. Moreover, with WTI crude sitting below $80 per barrel there is very little margin for error should traders turn defensive, considering that levels above $90 per barrel have been commonplace in the past two years.

The latest PCE core data fits the narrative of a soft landing which will help to steepen the Treasury curve. That has emboldened some bond traders into betting on a jumbo interest rate cut in September as the Fed may be seen as being behind the curve by then.

Should the view of a 50-bps reduction become consensus that will be a powerful tailwind for Treasuries. But all the while bond traders will be looking across to the oil complex for any signals that could disrupt their buoyant mood.

Bloomberg: Traders Fret as 32-Hour Central Banking Spree Hangs Over Markets

Policymakers from Japan, US and UK are set to meet this week

Decisions may send waves through bonds, stocks and currencies

…Federal Reserve Investors will scour the Fed’s policy announcement and Chair Jerome Powell’s remarks on Wednesday for anything that supports expectations for a first interest-rate reduction in September.

Such a move would align with the view of economists and swaps traders, who are fully pricing in at least two quarter-point cuts this year. The Fed’s benchmark is now in a range of 5.25% to 5.5%, a peak reached a year ago,

Policymakers have been pointing out a balanced labor market and ebbing inflation for several weeks, an indication they see an growing case for lower borrowing costs in the world’s top economy.

“The upcoming FOMC will be used to lay the groundwork for a September rate cut as the Fed makes the case for moving policy from restrictive territory toward a more neutral footing,” said James Knightley, chief international economist at ING.

Some market watchers — from former New York Fed president William Dudley to Mohamed El-Erian — have even laid out the case for more-aggressive easing than what’s currently expected. In separate Bloomberg Opinion columns, Dudley said the Fed should consider reducing rates this week and El-Erian warned of a “policy mistake” if the central bank keeps rates too high for too long.

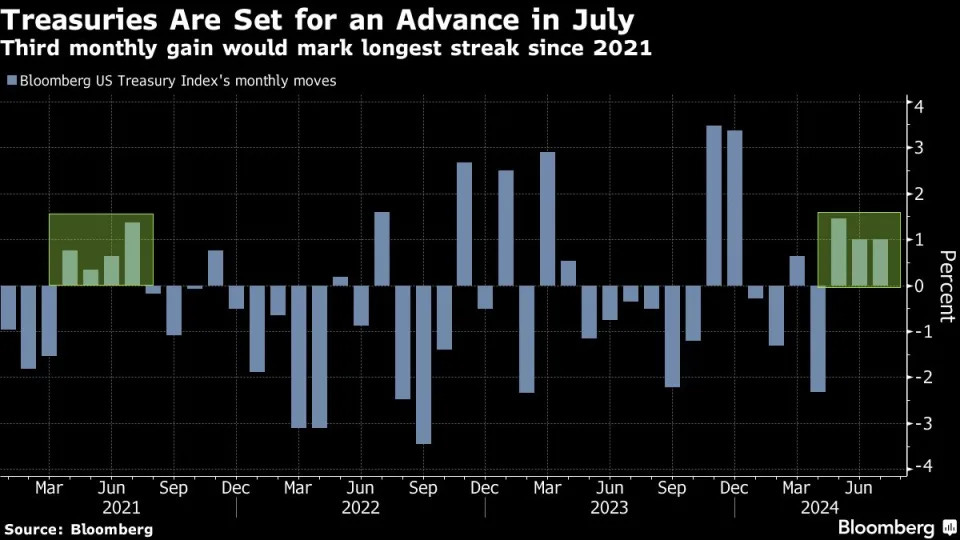

Treasuries are on pace to end July with a three-month winning streak last seen in mid-2021. Rising conviction surrounding rate cuts helped a Bloomberg index of US government debt touch a two-year high this month. Two-year yields have declined on the bet easier monetary policy is coming, leading to a narrowing of the gap with 10-year notes.

US stocks, however, enter the week on somewhat shakier footing, in part because several corporate earnings reports raised doubts over the strength of consumers. The S&P 500 Index on Wednesday ended its longest stretch without a 2% decline since the start of the global financial crisis in 2007.

A look at the volatility market shows just how important the week — which will also feature a US jobs report and corporate results from Meta Platforms Inc., Microsoft Corp. and Apple Inc., among others — is for traders.

A gauge of implied price swings in the S&P 500 in the next week jumped to almost 1 point above the expected volatility two weeks from now, a signal that the here-and-now uncertainty is higher than that further down the line.

Bloomberg: Pro wrestling's bad-guy scenario leg-drops markets (Authers’ OpED for the visual of Trimmed MEAN)

… There’s much more to it, however. Inflation continues to cloud all else for financial markets, and the latest news is unambiguously good. Last week saw publication of the June Personal Consumption Expenditure deflator, the inflation measure that the Federal Reserve officially uses as its yardstick. As Omair Sharif of Inflation Insights points out, 10 of the last 13 months have produced average month-on-month inflation of 0.168%, which is equivalent to a 2.0% annual rate — exactly in line with the Fed’s target. Using the Dallas Fed’s measure of the trimmed mean, excluding outliers in both directions and taking the average of the rest, we find inflation clearly trending downward, below the 3% upper range of the Fed’s target:

That has driven huge optimism for imminent rate cuts. Ahead of the last Federal Open Market Committee meeting in June, fed funds futures suggested no rate cut until the November meeting. Now, there is certainty that there will be at least one by then, with speculation about a cut as early as this Wednesday’s FOMC. If not a face-heel turn, the market has made a hawk-dove turn effortlessly:

Part of the market’s big turn, then, seems to be the conviction that easier money lies ahead…

Sam Ro from TKer: Why the Fed's first rate cut wouldn't be that big of a deal

… “Previously, with inflation far from its objective and employment closer to its objective, the Fed's focus was on inflation,” BofA’s Michael Gapen said on Thursday. “Now, with smaller deviations in inflation and employment from target, the Fed's attention can be more balanced. Cuts can happen because the economy cools, because inflation slows, or both.“

The Fed’s preferred measure of inflation is down significantly from crisis levels. (Source: BEA via FRED)

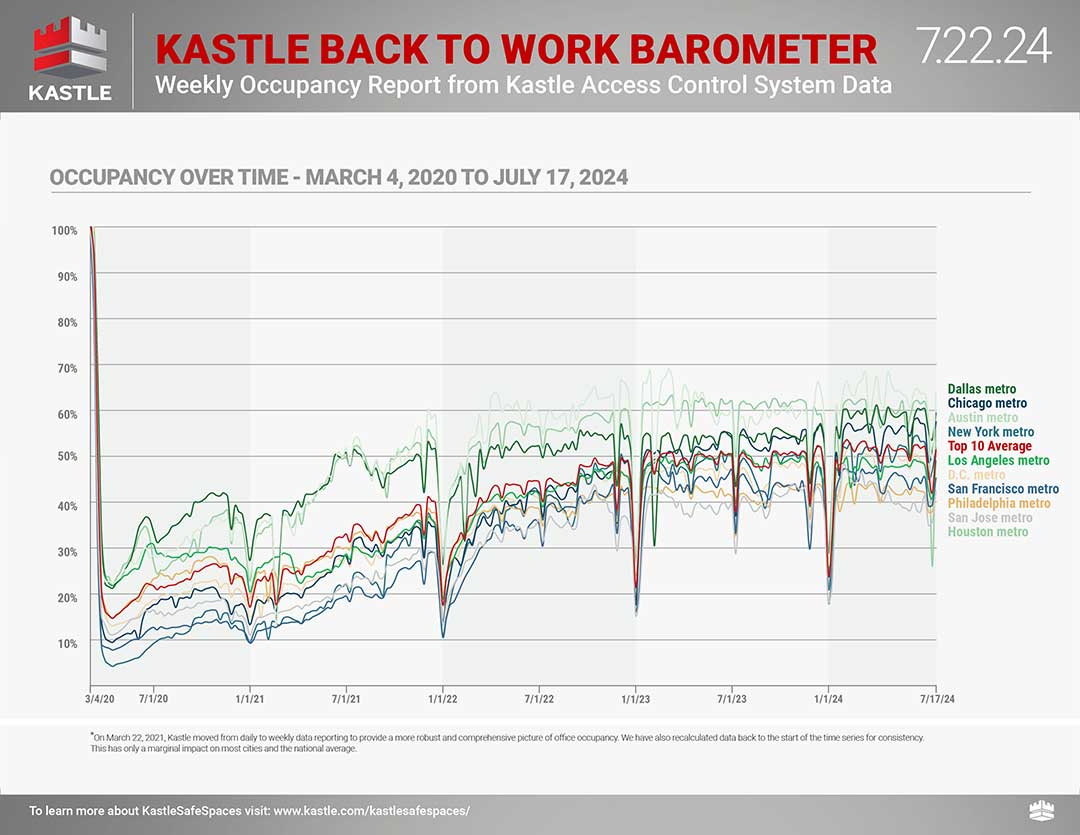

… Offices remain relatively empty. From Kastle Systems: “Occupancy Rises Across Cities After Weeks of Holiday and Weather Disruptions: The weekly average peak rose over five points to 61% on Tuesday this past week, as workers returned to the office in larger numbers after weeks of holiday and weather interruptions — especially throughout Texas. The weekly average low across all cities was Friday at 32.4% occupancy.”

$4.35 a gal at my local Costco in the burbs of Sacramento....'I'm a Zit!' will always be my favorite line from childhood, I have the soundtrack cd buried in a moving box :)

$4.35 a gal at my local Costco in the burbs of Sacramento....'I'm a Zit!' will always be my favorite line from childhood, I have the soundtrack cd buried in a moving box :)