This morning, I’ll attempt to be brief. There are all sorts of short-termer’s out there attempting to game the NFP because, you know, they have a better economic / trading mouse trap.

NFP may not be so weak BUT trust them, it’s weakening under the surface. OR, vice versa.

These days, being away from that type of role and not really needing to pretend to outguess markets (and those placing their bets on certain 10min window outcomes), I can’t help but be somewhat sympathetic TO Peter Lynch’s view on economic data (and economists).

… "I think if you spent over 13 minutes a year on economics, you've wasted over 10 minutes. It's not helpful. Everybody wants to predict the future, and I've tried to call the 1-800 psychic hotlines. It hasn't helped. The only thing I would look at is what's happening right now."

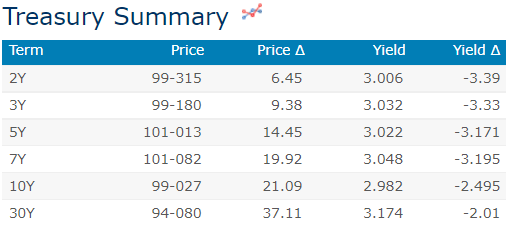

… here is a snapshot OF USTs as of 725a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are modestly higher and the curve a hair steeper this morning ahead of US June employment data. DXY is a hair higher (+0.13%) while front WTI futures are little changed this morning. Asian stocks were mixed, EU and UK share markets are all modestly higher (DAX +1.3%) while ES futures are showing -0.1% here at 6:50am. Our overnight US rates flows saw a quiet Asian session punctuated by a brief risk-off move after the terrible news about ex-PM Abe of Japan hit. We saw some Asian real$ selling in the long-end and buying in intermediates but that was about it. Our London desk reports the same thing: quiet, breath-held activity this morning. Overnight Treasury volume was indeed weak at ~60% of average volume with only 5yrs (104%) seeing near-average turnover overnight.

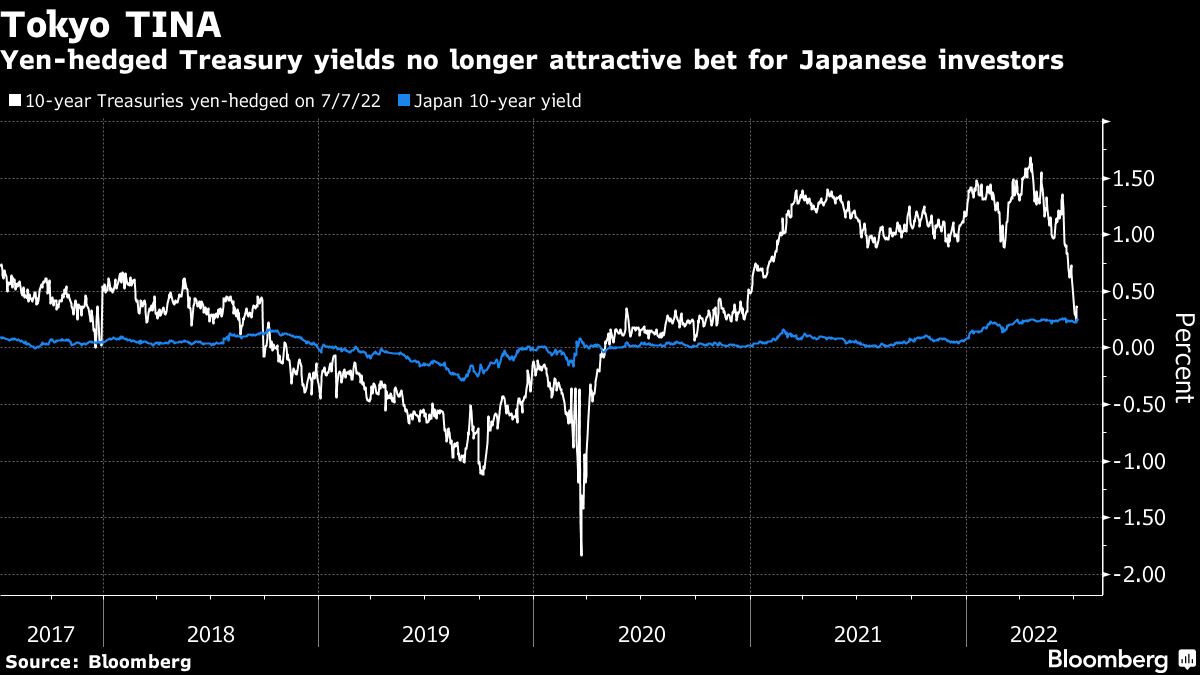

Yen-based investors, where art thou? More (about less) in a moment … for some MORE of the news you can use » IGMs Press Picks for today (8 July) to help weed thru the noise (some of which can be found over here at Finviz).

Now, setting aside Peter Lynch’s view of economics, a few things from the inbox which I’ve read and caught my eyes … all just some filler between now, NFP and then whenever it is Lacy Hunt’s Q2 missive eventually drops,

An about turn in the Fed’s preferred yield curve measure means traders should take the latest 2-year/10-year inversion much more seriously than earlier this year. The last time sections of the US yield curve inverted in March, Fed Chair Jerome Powell downplayed the significance arguing that traders were looking at the wrong metric. He stressed the case for his preferred curve — where three-month rates are now versus where they are expected to be in 18 months’ time — which at the time was still steepening. A Fed research paper in 2018 highlighted that this shorter-term curve adjusts for complicating factors like the so-called term premium, and thus gives a cleaner read on market expectations for future monetary policy. To quote Powell himself: “If it’s inverted, that means the Fed’s going to cut, which means the economy is weak.” This time round, the Powell measure is flattening rapidly. While the spread is still well in positive territory, the closer it gets to zero, the more seriously the central bank will have to take signals from other parts of the yield curve.

Meanwhile, a notable buyer in the Treasury market (other than the Fed) is conspicuously absent: Japanese investors.

As chronicled by Bloomberg’s Matthew Burgess and Daisuke Sakai, Japan-based investors still hold over $1.2 trillion worth of US sovereign debt, which is the largest hoard of Treasuries outside the US. Still, the sum has been shrinking: weekly data from the Ministry of Finance show just four weeks of net meaningful purchases this year.

A big reason why is exorbitantly high currency-hedging costs. The extreme differential between rock-bottom Japanese interest rates and those in the US means that yen-based investors have to pay more than 2.6% to hedge out dollar exposure for three months, compared to just 0.3% or so at the beginning of 2022, Bloomberg data show.

As a result, a relatively juicy 3% yield on 10-year Treasuries shrinks to just about 0.37% after factoring in the cost of protecting against currency swings. Hedged yields were as high as 1.7% in April, before the Fed’s hiking campaign kicked into high gear. Meanwhile, yields on comparable Japanese government bonds clock in at about 0.25% -- so perhaps it’s easier to just stay home.

A key condition for enticing Japanese buyers back into the US bond market is stability in the yen, according to Ian Lyngen, head of US rates strategy at BMO Capital Markets. The dollar has dominated versus virtually every major currency this year thanks to a combination of higher US rates and haven appeal, with the yen hovering near a 24-year low against the greenback.

Once the yen steadies, the dip-buying instinct abroad should kick in, Lyngen said.

“Anytime 10-year yields move above 3%, we’d expect Japanese investors to become reengaged in US Treasuries,” Lyngen said. “With a recession on the market’s radar, dip-buying in Treasuries will define the second half of 2022.”

The US employment report is due. The official employment data is revised a lot, and may miss some workers. The explosion of business creation in the pandemic may not be captured, and it seems unlikely that those employed dancing in front of their smartphones for social media are properly categorized. (This is a proper job—and as I play with Playmobil for a living, I will not judge).

Employment matters because job security underpins the economic recovery. Workers have falling real incomes, which should mean a consumer crunch. But job security gives people the confidence to save less each month, so they have more to spend, slowing the decline in demand. Today’s data should show some slowdown in job creation, but the payrolls and hours worked numbers have recently remained completely inconsistent with any idea of a recession...

A few days ago, these words and a visual from BBG (via ZH) spoke loud and clear and I think are worth sharing ahead of this mornings data. Once the data prints, all possible outcomes are priced (5-10mins?), I’d not be surprised to see activity FADE as folks anticipate / deploy ‘The Hamptons Hedge’ … Desks will get even MORE thinly staffed and those not already working remotely (from their beach locations), are likely to do so … leaving the rest of us here looking for something to read, watch on TV as we await next installment from HIMCO. On that note, beware,

The switchbacks that US rate markets have witnessed in the past few days have been quite breathtaking. It’s not just that the moves have been big -- we’ve been seeing a lot of that lately as traders adjust their views on inflation and growth -- but that the market has been turning so sharply within the space of a session, and seemingly out of proportion to any change in fundamental circumstances that data or central bank commentary might suggest.

The volatility underscores not only a lack of certainty about which way inflation and recession risks will play out, but also speaks to both the lack of liquidity within markets and a lack of real conviction among investors. The former has been a hot topic of discussion, particularly as the Fed embarks on its quantitative tightening program. And the latter is borne out by recent indicators that show many folks desperately clinging to neutral stances.

The big round number that is 3% provides a useful illustration for just how whiplashy things have been. Earlier on Wednesday, it was a key focus for the long end, with the 30-year breaking below that level for the first time in over a month. But by day’s end, the long bond was nowhere near there and it was the two-year rate pushing back above that level.

The 10-year yield meanwhile had a roundtrip of almost 19 basis points on the day Wednesday, having been down more than 6 and ending up by more than 12. And it had an even bigger journey the day before, albeit in a broadly opposite direction.

This doesn’t all happen in a vacuum, of course. Various economic indicators and the release of the most recent Fed minutes have provided plenty for traders to chew on. The vagaries of risk-taking in stock markets and elsewhere are also adding to the turbulence. But it’s still hard to see a catalyst for investors genuinely reassessing their views so much in such a short period of time.

And indeed, if you step back a little, you see they’re not. Despite all the sound and fury, the ranges for say, the 10-year yield, have been broadly similar for the past three days. Little wonder, I guess, that real money investors might look to stay on the sidelines a bit longer, at least until they summon a slightly more conviction themselves about which way the economy, policy and markets are headed.

The Credit Suisse House View recently turned neutral on Global Government Bonds on a 3-6 month horizon. The Credit Suisse House View comprises a range of inputs, including Fundamental and Economic analysis, as well as Technical Analysis. This report outlines the technical outlook for Bond Yields, generally over a shorter-term horizon of approximately 1-month.

Chart of the Day: The US 2s10s Bond Curve has flattened into inversion over the past few sessions, with the market now testing the prior 2022 low at -9.5bps. With the recent move lower supported by a turn lower in medium-term momentum, we look for the flattening trend to continue, with scope for a move to our long-held objective at -16.5/-20bps, which is the 2006 lows. We still believe this is likely to be driven by a deeper move higher in 2yr Bond Yields, which we believe will break to new 2022 highs.

That said, the firm has turned now tactically BEARISH 10s (3.255 and 2.855 are levels to watch) and WOULD turn tactically BULLISH bonds at support (3.395) … Interesting, if you ask me (which you didn’t. A curve trade? No. All bases covered? Maybe.