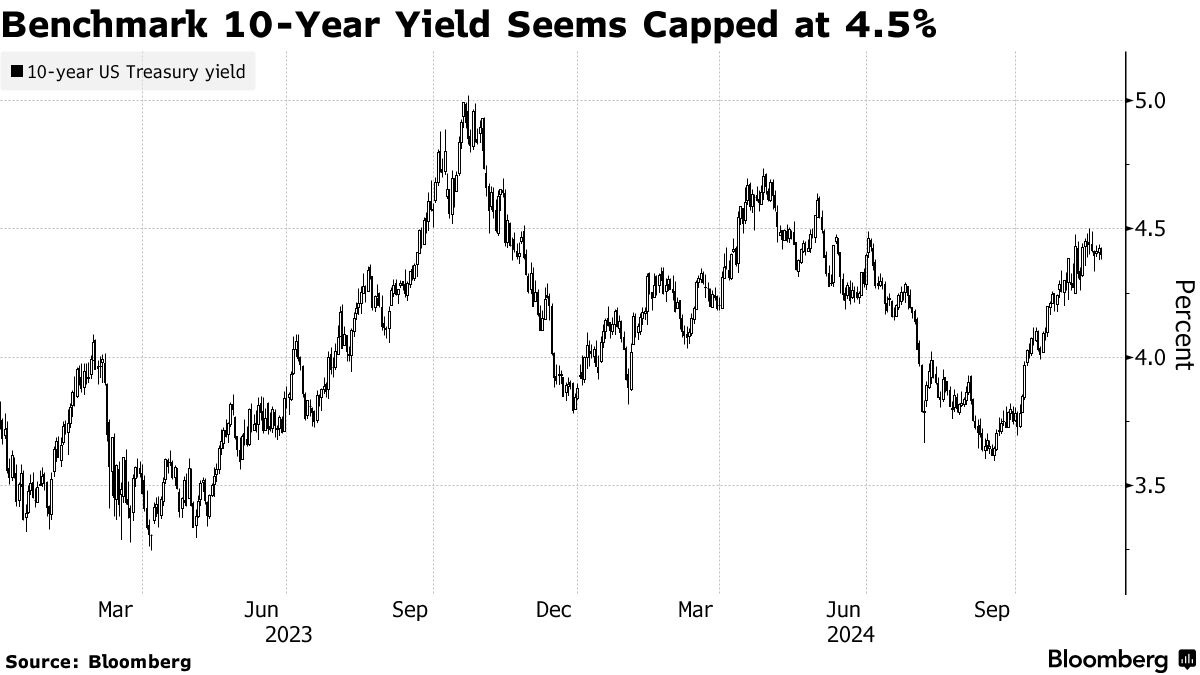

Good morning … staring into the holiday shortened week today will see $69bb of 2yr USTs up for sale and as global markets celebrate Bessent for Treasury, stocks AND BONDS are bid while the USD is lower, here’s a look at 2yy …

2yy: 20bps trading range — 4.40 to 4.20 …

… momentum overSOLD and a bit of a Bessent blessing being offered robbing the market of approx 3bps of concession previously priced in …

… AND so it goes … not much else to labor over and with lots just ahead, crammed into what is a defacto 4d weekend coming up I won’t delay and … here is a snapshot OF USTs as of 657a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Stocks firm, USD pressured & USTs bid on Trump’s Treasury appointment … USD pressured and USTs bid following this, with the DXY sub-107.00 and the US yield curve bull-flattening … USTs outperform following US President-elect Trump selecting Scott Bessent as the next Treasury Secretary, an update which has sparked pronounced bull-flattening.

Opening Bell Daily: 2025 stocks look good … Wall Street expects the S&P 500 to keep climbing in 2025 … Trump Trade aside, Yardeni Research is nearly twice as bullish as Goldman Sachs on stocks.

Reuters Morning Bid: US 10-year yields drop to 2-week low as bonds rally on Bessent pick

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … First up, a word on … stocks (sorry)

BARCAP: U.S. Equity Strategy: 2025 Outlook: Bridled Enthusiasm

Unbridled enthusiasm? Hold your horses. Macro slowing to still-healthy levels should support more US equity upside next year, albeit a deceleration from '23-'24's breakneck pace. Positioning looks constructive, and policy uncertainty creates room for stock and sector selection.

Raise 2025 S&P 500 PT to 6600 from 6500, based on 24x our FY25 EPS estimate of $271 (up from $268, vs. current consensus $275). PT implies 10% upside from our revised 2024 year-end PT of 6000 (up from 5600); EPS implies +11.5% Y/Y growth from our FY24 EPS estimate of $243 (up from $241); US Tech exceptionalism and "virtuous cycle" between income and consumption remain intact…

…Positioning looks supportive from here; discretionary investors have room to add, with potential upside pressure from systematic funds if vol normalizes amid a grind higher. Retail inflows to US equity funds hit a record last month.

…Macro looks "glass half full" into 2025 For US equities, we think macro positives outweigh the negatives heading into next year. Post-election uncertainty has been resolved, oil prices have shrugged off the Middle East war for over a year, jobless rates remain low, household wealth is up some $48trn from COVID to mid-2024 and the Fed is cutting rates. Mild slowdown in labor supply and payroll gains next year should pave the way for US growth to decelerate to a still-healthy 2.1% from the near-3% growth of 2023 and 2024 (Glass half full, 13 Nov 2024)…

…Risks of stubborn inflation (or even re-inflation) are on the other side of the coin. After all, consumer spending momentum into Q4 defied a relatively weak October payrolls number (Much depends on November payrolls, 1 Nov 2024) and hotter-than-expected core inflation keeps Barclays' economists call for December FOMC a close one, with another 25bp cut as the base case but risks increasingly skewed toward a pause (October core PCE estimated at 0.28% m/m, 14 Nov 2024).

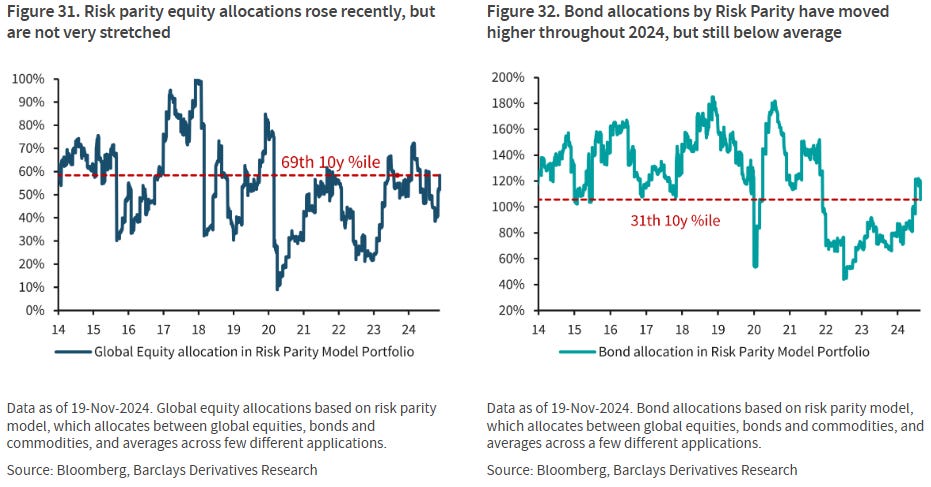

… Risk Parity funds trimmed equity exposure for a majority part of 2024, but have recently begun rebuilding exposure as vols have come down. However, the current allocation of c.60% is still not too stretched, and in fact close to the 10y average of ~52%. On the other hand, the funds have built back bond exposure throughout 2024 from historically depressed levels (c.40%), although the current allocation (~105%) is still historically low.

The financial and geopolitical world changed dramatically overnight on November 5th with Trump’s election victory and the Republican sweep in Congress. The outlook is now far from “business as usual” and this opens up a wider range of outcomes for the global economy and financial markets. These span from a potentially much more positive US outlook on the one hand, to a much more negative European outlook on the other. President-elect Trump has several potentially conflicting economic policy goals, and how he weights them in office will influence global growth and asset prices in 2025 and beyond.

If the primary focus of the new administration is boosting growth, there’s every chance that this can be very positive for the US, with spillovers elsewhere across the globe. But that would likely require less of a focus on campaign promises like the deportation of undocumented immigrants and on tariffs. Mr Trump’s unpredictability means we will only know in real-time the way he balances these priorities once in office.

The main downside risks are more likely to emerge if greater weight is put on aggressive trade and immigration policies. This could be more negative for growth and push up inflation. That would lead the Fed to cease the cutting cycle and possibly even contemplate restarting rate increases which would likely put upward pressure on bond yields. This would have implications for the US and even more so to the rest of the world. A maximalist Trump trade agenda and a Europe constrained to act because of fragmentation is a huge but realistic risk for the continent. The German election in February could become a pivotal event.

Our base case for 2025 is stronger US growth and inflation and a higher Fed terminal rate than previously expected with the opposite conditions for Europe. This is driven by the assumption of modest US tax cuts, a strong deregulation push, and more supportive financial conditions. On trade we assume a 10 percentage point increase in the tariff rate on imports from China in the first half of the year (ratcheting up a further 10pp in H2) and an equalisation of tariff rates on motor vehicles with Europe. The forecast also assumes a 5% universal baseline tariff, though that is more likely to be implemented late 2025/early 2026.

This report contains all our global economic and asset price forecasts for 2025 and into 2026, with a continuation of US exceptionalism the most likely path. Uncertainty is high and as we said at the top, business as usual is the least likely outcome.

…United States Summary: The Republican sweep of the 2024 US election promises to bring transformative changes to the policy landscape. Details about the exact timing and parameters around these policies are highly uncertain. And shifts in fiscal and trade policy will provide crosscurrents to the growth outlook. We ultimately anticipate that modest tax cuts, a strong deregulation push, and more supportive financial conditions will produce faster growth in 2025, which we now see at 2.5% (Q4/Q4) versus 2.2% previously. Beyond next year, adverse effects from the trade war and a more restrictive monetary policy setting reduce our growth estimates modestly. This policy mix will stall progress on inflation, with core PCE expected to remain at or above 2.5% over the next two years, leading the Fed to undertake an extended pause. We now see the fed funds rate above 4% through 2026, a modestly restrictive stance relative to our elevated estimates of neutral (3.75-4%). Given the substantial policy uncertainties, we also detail how a more adverse trade scenario would impact our forecasts…

… Rates … In the US, the assumed policy mix should result in a combination of a positive demand shock (net fiscal easing), a positive supply shock (regulatory reforms) and a negative supply shock (tariffs and immigration controls). The impact on US growth and inflation will depend on the timing and scale of the various policy levers. For the purpose of our forecast, we assume that these policies will raise the nominal neutral rate to approximately 4% and lead the Fed to remain above neutral for longer. Moreover, term premia should rise further as the market reassesses inflation risks and increased supply. Taken together, these factors support our forecast of a 10-year US Treasury yield peaking around 4.75%.

… in this next note, a European shop details how it is tariffs will harm ‘Merica first …

ING: How American consumers will bear the burden of Trump’s tariffs

Now that Donald Trump has won the US election, the focus is shifting to his fondness for tariffs. However, history suggests that American consumers may bear much of the cost again

… Morgan Stanley on Merica …

MS: Sunday Start | What's Next in Global Macro: 'Merica

… Focusing on valuation and sentiment, one needs to be a bit wary of the heavily owned and well-loved nature of the US equity market. However, as we argued in our 2025 Outlook, valuation can remain elevated for extended periods of time when earnings growth is above average and the policy rate is down on a year-over-year basis (our house view over the next 12 months). Furthermore, while the election outcome has boosted the equity market overall and the pro-cyclical tilt we have been recommending, the reversal of hard-landing fears this summer and an aggressive start to the Fed cutting cycle were also important factors – i.e., we’ve priced a lot of good news in a short period of time. On another topic, I’ve been surprised at how skeptical many are about the prospective administration’s commitment to streamline the government, particularly given Elon Musk’s role and his track record of executing on challenging goals. A successful outcome on these efforts could support a broadening in earnings growth and stock performance that has been absent, until recently. Bottom line, we are likely entering a higher-beta environment based on the sequencing of the policy changes (some good, some bad for equity markets) and execution on stated intentions. It should also be a highly reflexive environment, as equities will likely take their cue from other markets more than they normally do, especially rates and FX.

Given this setup, we will continue to focus our US equity strategy research on relative value, factor, style, sector, and stock recommendations. On that score, financials remains our preferred sector within our favored cohort – quality cyclicals, followed by industrials. Quality and operational efficiency are still our preferred factors. Our favorite pair continues to be software over semis, while small caps are still neutral post our upgrade in the summer. See our 2025 Outlook for more details, including screens of single stocks that match these preferences, along with potential M&A targets which should see greater activity as regulations ease in 2025. As in 2024, with macro outcomes and policy still highly uncertain, we will not hesitate to revise these preferences if growth, inflation, or policy expectations deviate from the current Goldilocks outcome. To that point, the greatest risks to American equity market dominance in the short term are (1) a persistently stronger US dollar against easy comparisons into year-end that put pressure on global liquidity and multinational earnings, (2) a further rise in back-end rates driven by the term premium rather than growth, and (3) higher inflation data that dissuade the Fed from cutting rates in December or lead to materially less dovish guidance.

… same shop reflecting on conference during a very long trip home …

Conversations with investors last week at our Asia Pac Summit indicate an increasingly strong preference for US vs. rest of world equities. Questions on our outlook have centered around our valuation target (21.5x), our low-teens EPS growth outlook, our OW on Financials and our UW on Consumer Goods.

What's Going to Keep Valuation Levels Historically Elevated?Our work shows that in 12-month rate of change terms, it's very rare to see meaningful multiple compression in periods of above average (>8%) EPS growth (our base case) and a declining policy rate on a year-over-year basis (our economists' base case view). Further, the median stock multiple trades at a ~3 turn discount to the cap weighted multiple and should see upside if the earnings growth recovery broadens in 2025 as expected. Of course, we're balancing these factors with the notion that the level of valuation is extended relative to history (top decile)—a phenomenon we're also respectful of. All told, we think our 12-month forward P/E target of 21.5x (vs. 22.0x today) reflects the balance of these factors and is a reasonable assessment of fair value in an environment of broadening EPS growth and subdued interest rates in the base case….

MS: The Weekly Worldview: Thoughts from 40,000 Feet

…For the US, we framed the key policy implications coming out of the election in four categories: fiscal, deregulation, tariffs, and immigration. A key challenge to many clients’ views was that the first two are not likely to have any material effect on the economy in 2025. Deregulation is very likely to have important microeconomic effects, and equity investors are rightfully heavily focused here. But deregulation takes a great deal of time to change rules, and regulations are the embodiment of legislation, so to eliminate regulations requires legislation. More broadly, I remain unconvinced that there is a substantial macroeconomic component, even abstracting from the timing.

For fiscal policy, the potential macroeconomic effect is clear, but the timing and the composition matter a lot. The Morgan Stanley house view is that the bulk of the fiscal changes will be extension of extending expiring tax cuts from the Tax Cut and Jobs Act (TCJA). We do see some modest further fiscal expansion, mostly in the SALT deduction cap elimination, but a few points are critical. The tax cuts do not expire until 2026, and the legislative process will likely take all of next year. Second, extending tax rates at the current level does not boost economic growth, it merely maintains the current policy. Finally, the additional policies will similarly be delayed, and most of the benefit accrues to the top end of the income distribution, making for a small multiplier.

Tariffs and immigration policy, in contrast, are instituted in 2025 in our baseline, but the effects on the economy build over time are biggest in 2026. I spent time with clients discussing our assumption that tariffs start to be implemented early next year but ramp up over the year, so the drag on growth and the boost to inflation only become noticeable in the second half and only become substantial in 2026. Some clients argued for big and broad tariffs implemented on day one. If so, the boost to inflation would be bigger, and observed much sooner, and our view of growth is too optimistic in 2025.

The conversation on immigration was similar. In our forecast, immigration falls notably due to new policy, but remains positive. In discussions with clients, particularly with some of our guest speakers on the topic, the prospect of negative net migration in 2025 came up as a clear risk. In that outcome, we would have to revise our forecasts, increasing the stagflationary shock to the economy, shifting 2025 from a year of modest deceleration to one of weak growth and rising inflation.

The title for our Outlook, Pieces of the Policy Puzzle, was very intentionally chosen. I opened the first panel of the conference noting that in years past, we had laid out our forecasts as a road map for investors. This time, our document is more of a guide to the array of issues and risks, because the uncertainty around any point forecast is greater now than just about any time I have ever seen.

We factor in phased tariffs on China, where most goods are tariffed, but only a small portion of goods see tariffs raised to 60%. In the US, we see real spending growth slowing throughout 2025 and 2026.

Markets reacted positively to US President-elect Trump nominating the financier Bessent as treasury secretary. Investors prefer orthodoxy, predictability, and coherence from economic policy; there were fears that some of the candidates may not possess those attributes. Bessent does. Bessent has said he regards taxing US consumers via trade tariffs as a bargaining tool—essentially the stance in Trump’s first term. Others in the cabinet disagree, but investors will be pleased there is one voice of trade tax moderation.

Last Friday the US Michigan consumer sentiment data soared to the highest level in almost four years—if you were Republican. Democrat sentiment collapsed. This is, obviously, nothing to do with the questions asked about the economic situation. Today’s Dallas Fed manufacturing survey offers insights into political distortions to data via its comments section. The German ifo business sentiment poll is also due.

The US “Black Friday” festival approaches—and indeed has already begun as retailers extend the promotion period. The shift from spending on goods to having fun has been in evidence all year—does the fevered pursuit of Black Friday bargains constitute fun? In Japan, Tokyo department store sales dropped in October…

… And from Global Wall Street inbox TO the WWW …

First up, Apollo Global … shedding some light, sharing some views …

As home prices continue to rise, more and more households are taking out HELOCs to finance consumer spending, see chart below.

In other words, homeowners are liquifying their home price gains and using the proceeds for consumption.

Combined with low jobless claims, strong wage growth, high stock prices, and solid cash flows from fixed income, including private credit, the US consumer continues to do well.

When growth is strong, corporate earnings are high. When growth is weak, corporate earnings are low. This makes it difficult to find out if companies are cheap or expensive.

One way to analyze if stocks are cheap or expensive is to remove the business cycle by taking the 10-year average of earnings, and doing so shows that stocks are very expensive at the moment.

Specifically, the cyclically adjusted price earnings ratio at 38 is near all-time highs, significantly above its long-term average at 17, see chart below.

Apollo: US Households Have Never Been More Bullish on Equities

The Conference Board asks US households about their outlook for the stock market, and a record high of 51.4% say that stock prices will move higher, see chart below.

Our chart book with daily and weekly indicators for the US economy is available here.

Source: Conference Board, Haver Analytics, Apollo Chief Economist

… then there’s some BBG intel …

Bloomberg: Bond Market Halts Brutal Run as Buyers Pounce on 4.5% Yields

Traders still see uncertainty over US fiscal, Fed policy paths

Options traders are placing wagers to profit if yields do rise

… Treasuries are “a very low volatility asset with a high return,” Pimco’s Erin Browne said in a Bloomberg Television interview, adding that if the 10-year yield rose back to 5% she would “really get interested in buying more aggressively.”

The last two months mark another turbulent shift for the bond market, which has defied expectations that it would rally once the Fed started cutting interest rates. Instead, since the central bank’s first move in September, yields have pushed higher as the strong economy and Trump’s victory drove traders to recalibrate how far it would go…

… AND finally, as relatives set to arrive for Thursdays meal, some good news / relief …

Sam Ro from TKer: Wall Street strategists are nailing one of their more important forecasts for 2024

… Thanksgiving dinner got cheaper. From the American Farm Bureau: “The American Farm Bureau Federation’s 39th annual Thanksgiving dinner survey provides a snapshot of the average cost of this year’s classic holiday feast for 10, which is $58.08 or about $5.80 per person. This is a 5% decrease from 2023, which was 4.5% lower than 2022. Two years of declines don’t erase dramatic increases that led to a record high cost of $64.06 in 2022. Despite the encouraging momentum, a Thanksgiving meal is still 19% higher than it was in 2019, which highlights the impact inflation has had on food prices – and farmers’ costs – since the pandemic.“

balances have increased")