Good morning … A couple of things overnight warrnt mentioning before jumping in to this afternoons 5yr auction…

Bloomberg: PBOC Will Cut RRR for Banks in Early February, Governor Says

…Lowering the RRR frees up liquidity so banks can extend loans to customers and buy more bonds to support economic growth. The central bank cut the RRR twice in 2023, with the last reduction taking place in September.

Bloomberg: Japan Bond Yields, Bank Shares Jump on BOJ Rate Hike Bets

It’s clear BOJ hawkishness has increased: MUFJ Asset’s Kato

JGB 10-year yield climbs to its highest in more than a month

… The timing and extent of expected Federal Reserve rate cuts this year have dominated markets in recent weeks with less attention paid to Japan’s central bank. That left economists looking more bullish over the BOJ’s looming move than market players.

… The hawkish signals from the BOJ included Ueda’s remark that the board has confirmed that the economy is progressing in line with the previous inflation outlook, according to economists from Morgan Stanley MUFG Securities Co. They also highlighted comments that the Jan. 1 quake has not had significant negative economic impact and the so-called second force of inflation from rising wages is increasing slowly.

Speaking after the policy decision, Ueda also said any rate increase would initially aim to leave BOJ policy supportive of the economy and avoid causing too much disturbance. His remarks supported the prevailing view among economists that the BOJ will raise rates at some point in the first part of this year, with meetings slated for March, April, June and July. The question is when…

… For somewhat more on China, see John Authers’ latest OpED (below) … Now in as far as this afternoons ‘liquidity event’ (aka AUCTION) goes I offered some thoughts over the weekend as a couple heavyweights offered BUY recommendations. With ‘my career’ as defined by 5yy in mind, a somewhat shorter term tactical view …,

… couple things strike ME and my now extremely far removed eyes — momentum rolling over and crossing BULLISHLY from overSOLD levels (bullish — so the Global Wall maybe right on this one) AND were simply NOT as overSOLD back in Dec (13th — the JPOW PIVOT, noted).

Nothing here to suggest a layup as far as this afternoons 5yy auction goes BUT perhaps THEY (foreigners) are as interested as they were with that 2yr auction …

ZH: Solid 2Y Auction Sees Most Foreign Buyers Since Last Summer

… Where the auction was especially strong was the internals, which saw Indirects, i.e., foreign buyers, take down 65.3%, up notably from 61.9% in December and the highest since last July (and clearly well above the six-auction average of 62.8%), And with Directs awarded 19.9% (modestly below the recent average of 20.9%), Dealers were left holding 14.8%, the lowest since last September.

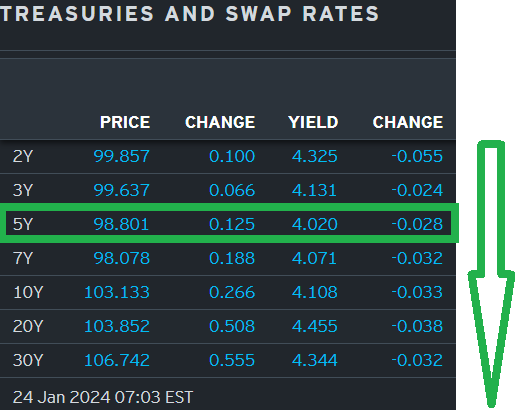

… here is a snapshot OF USTs as of 703a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher with the curve steeper again after mixed (but still weak) European PMI data and a 50bp cut in China's RRR that was announced at the start of London's trade. DXY is lower (-0.45%) while front WTI futures are little changed this morning. Asian stocks rose, led by Chinese exchanges, EU and UK share markets are higher (SX5E +1.65%) and ES futures are showing +0.45% here near 6:30am. Our overnight US rates flows saw better real$ buying in intermediates during Asian hours amid muted volumes overall. During London hours, an ~11k block buy of TY futures set the tone early before systematic sellers in the front end nudged prices off their highs. Overnight Treasury volume was about average overall.

… and for some MORE of the news you can use » The Morning Hark - 24 Jan 2024 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BNP: US rates: Close long 5y breakevens at revised stop (another trade bites the dust and will re-enter at ‘more favourable levels’ — and cuz it’s spelled that way, well, you know, gotta believe ‘em it’ll work out THEN cuz it will be different that time)

Our 2.255% stop has been reached and we close the trade at a 2bp loss (-USD50,000) including negative carry. While we are respecting our stop and closing the trade, the combination of inflation pricing and a wide core CPI/PCE wedge leaves us still constructive overall on traded inflation. We keep a close eye on the market and may look to re-enter the trade at more favourable levels.

DB China Macro: PBOC steps up monetary policy support

The PBOC will cut its reserve requirement ratio (RRR) on banks by 50bps, Governor Pan Gongsheng announced at today's press conference. The size of today's RRR cut is larger than in the recent past (25bps each for the last three cuts). In addition, the PBOC will cut the interest rate on its relending and rediscounting facilities by 25 bps to 1.75%. Short-term market interest rates will likely drop after the RRR cut. We continue to expect that the PBOC will cut its 1y MLF policy rate by 45 bps in 2024, with the first rate cut likely happening in or before March.

DB Mapping Markets: What’s driving the optimism, and can this be sustained? (not excerpted are REASONS CURRENT SETUP WILL BE DIFFICULT TO SUSTAIN … worth a click / read)

… In this piece, we look through 4 factors that have helped drive the recent optimism, and then question how sustainable this current set-up is.

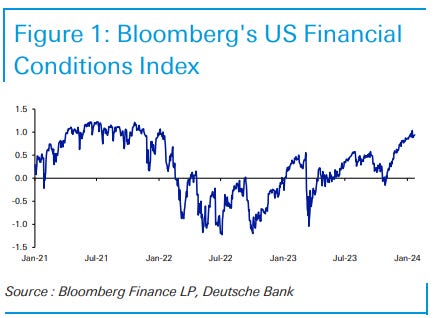

1. Broadly speaking, measures of financial conditions are easier than at any time in the last two years.

2. Data releases have been impressively resilient over recent months… 3. Rate cuts in 2024 are now being openly discussed by central bank officials… 4. For the first time in a long time, there is the promise of serious upside potential to growth, thanks to artificial intelligence.

Since the GFC in 2008, a persistent theme has been how economic growth has moved lower over previous decades, which ultimately has meant living standards have risen more slowly. That has been the backdrop to several other challenges, including rising debt levels. This is evident from Figure 4, where you can see from the log scale and previous trend lines that real disposable incomes per capita have not kept pace with the trend over previous decades in the US.

… Conclusion We've had a lot of good economic news over recent months, which has been very welcome for markets. But with the good news being priced in, and financial conditions now at accommodative levels, it may be difficult to maintain this optimism for long. Moreover, given the number of leading indicators that still point in a negative direction and inflation still above target levels in several countries, there are still plenty of reasons to remain cautious.

PBoC unexpectedly announced a 50bps RRR cut and 25bps targeted cuts on relending & rediscount rates today

We view this as a positive signal that Beijing is responding to recent market weakness, in addition to reported stock market stabilization efforts.

This is in-line with our view of a modest pace of reactive easing.

But as deflation persists, we think this may need to be followed up with more aggressive easing, particularly active fiscal easing to boost consumption.

Today’s calendar is plagued with business sentiment survey opinion, and little else. Surveys attract media attention because if you assume the survey does what it says it does, it can produce a more dramatic story. However, survey evidence has been a progressively less reliable description of reality across various measures. The UK government’s ONS says its labor force survey is unreliable—why would sentiment surveys of employment be more credible?

It is easier to answer a survey with perception rather than reality (reality requires thought). This helps explain why consumer surveys report more inflation than exists—US vending machine inflation is over 13% y/y, distorting inflation perceptions (falling television prices leave perceptions unaltered).

If survey response rates fall, people who fill in surveys are more likely to be strange. What motivates the dwindling numbers of respondents to fill in surveys? Loss aversion, in a different form. Bad news is more powerful than good news, so those who want to complain have an incentive to fill in a survey. This helps account for survey evidence tending to under-report economic activity.

Surveys also matter to investors’ political perceptions. In a year where politics matters, the unreliability of survey evidence in a more polarized landscape presents a challenge.

Richmond Fed manufacturing index slows in January, employment weakens… Services business activity remains soft in the 5th district too…

… And from Global Wall Street inbox TO the WWW,

Apollo: Taylor Rule Points to a Fed Cut in March (‘nuff said)

The main argument for the Fed cutting rates in March is that the Fed’s workhorse model says that because of the sharp decline in inflation over the past six months, the Fed funds rate today should not be 5.5% but 4.5%, see chart below. Specifically, the Fed has used the Taylor rule framework for decades to understand what the Fed funds rate should be, and inserting the current level of inflation and unemployment into the Taylor rule shows that the Fed funds rate today should be 4.5%, see chart below and Daily Spark here.

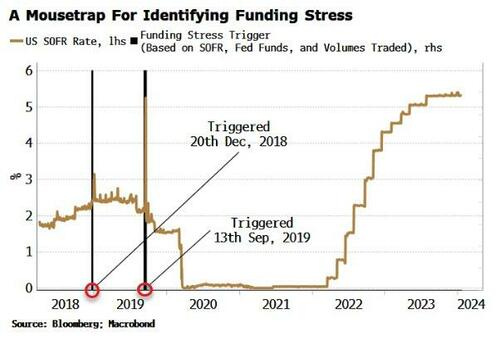

Bloomberg(via ZH): Watch This Signal For When The Fed Will End QT

… The trigger is shown in the chart below. It uses only four criteria based on the above points, bearing in mind Einstein’s maxim that models should be “as simple as possible, but no simpler.”

It has only activated twice: in 2018 and 2019. In 2018 it triggered on the 20th December. This was several days before the sharp rise in funding rates at the end of that year. The normal, year-end turn when demand for cash rises was exacerbated by Basel III regulation for GSIBs (Global Systemically Important Banks), who stockpiled reserves to ensure their loss-absorbency requirements did not rise.

The trigger also activated in the 2019 funding episode, perhaps appropriately on Friday the 13th of September, ahead of the acute stress seen the following week that led to the Fed’s emergency repo provisioning.

No signal is perfect and all are necessarily subject to retrofitting bias: there’s no guarantee the next funding flare-up will manifest itself in exactly the same way as prior episodes. The possibility of a false negative means maintaining vigilance to funding-market conditions is essential even in the absence of the signal being active.

Furthermore, the Fed introduced a standing repo facility in 2021 allowing banks to access funding at a punitive rate, while it has also been trying to de-stigmatize the use of the discount window.

Nonetheless, there is no guarantee either of these would see notable use before the funding-stress cat is out of the bag. The trigger, on the other hand, uses daily price and volume data that ideally captures general signs of funding distress before it significantly worsens.

In the current environment of deeply intertwined fiscal and monetary policy, assets are increasingly sensitive to funding markets, while the latter are more prone to abrupt meltdowns.

Butterflies flapping their wings in the monetary plumbing should therefore be taken seriously by traders and investors across all asset classes.

Bloomberg #5Things (Asia — with a note on BREAKS which goes hand in hand with BNP just above)

The confrontations in the Middle East are threatening the immaculate disinflation narrative that has been backing expectations for soft economic landings and central bank interest-rate cuts. The starkest and scariest signs of the danger are the astounding spikes in the rates to ship fuel from the Middle East. Asian routes have seen costs almost triple since the Jan. 12 launch of US and UK airstrikes on Yemen’s Houthi rebels.

Those rates could ease back down as supply chains adapt, but the rebound in crude oil is steadier and has scope to extend even if shipping charges decline. The moves have become a bit lost in the whipsawing that has afflicted the bond market at the start of 2024, but traders’ expectations for inflation have also been climbing. The two-year breakeven rate — reflecting bets on the average annual consumer-price gains over that period — reached about 2.3%.

That’s heading for the biggest one-month increase since February of last year, even if it is well short of that period’s 85-basis-point surge. The increase in inflation concerns in the bond market adds to the likelihood that investors may still be overestimating the depth of rate cuts policymakers will end up delivering this year.

Bloomberg: China may need a bigger bazooka (Authers’ OpED)

City Journal: The Fed’s Monetary Handover (written by a friend of a friend and so, to MY friend — THANK YOU, BP, for mentioning / sending me this one — HIGHLY RECOMMEND a read or two)

… We haven’t seen this up to now because for most of the past year, the Treasury Department has offset QT by increasing the share of total issuance for bills far beyond the norm. The increased duration risk that QT supplies to the market has been nullified by the reduced duration risk supplied to the market by changes to Treasury’s issuance profile, and political actors at Treasury have managed to run roughshod over the stance of monetary policy.

The heart of the current problem is that the Fed wants QE to be perceived as monetary policy, but not QT. Indeed, former Fed chair Janet Yellen notably said that she thought QT would be “like watching paint dry.” Suppose QT is monetary policy and the Fed is targeting a given total level of restrictiveness: then an intervention by Treasury to offset QT should be countered by even more QT from the central bank. However, if Fed Chair Powell believes QT is merely technical in nature and not monetary policy, then they will ignore Treasury’s intervention, as he seems to have done.

Moreover, even if the Fed aimed to increase its balance sheet reductions meaningfully, it would have to actively sell assets from its portfolio rather than allow them to roll off at maturity, as it currently does. Doing so would realize the enormous mark-to-market losses on its securities profile, implicitly saddling taxpayers with the burden for the central bank’s monetary follies…

… Worse, the Fed has handed Treasury the power to force it to bring forward the date at which it slows the pace of QT and potentially ends QT altogether. Years of unorthodox policy and the Basel III bank regulation process have forced the Fed to create a reverse repurchase facility, or RRP, through which the Fed borrows overnight from market participants. The Fed created the RRP as an arcane matter of monetary plumbing. Because Fed RRP and Treasury bills are both short-term assets with no credit risk, they are near-perfect substitutes—by increasing bill issuance, Treasury ensures the RRP drains more quickly.

By keeping bill issuance high, Treasury is able not only to counteract the QT performed by the Fed but also to force the Fed to taper QT. This is an abomination: monetary policy under the control of fiscal authorities….

1/ S&P 500 All-time highs. For all the debate about whether stocks should go up, or can go up further, one thing is certain, they just made all-time highs. At all-time highs, there are no investors sitting in a losing position on their exposure and instead, it’s the short sellers who are on the wrong side and who sit with losses. And those short sellers remain fuel for the future, given they represent forced buying vs. the rest of investors who can make their own informed decisions. When prices push past prior highs, which can offer resistance, they take away another piece of the bearish narrative that some have clung to, since the market bottomed 15-months ago.

WolfST: D.R. Horton Sheds Some Light on the Massive Costs of Mortgage Rate Buydowns as a Hedge Went Awry. Stock Tanks (not usually a stock specific spot on the web BUT there’s something here that is more macro …)

2 Words (h/t Lyn Alden): Fiscal Dominance! Thanks for that link looking forward to it. Should less have been expected of Yellin? She's been acting like Fed Chair since named Treasury Sec (h/t Michael Every).

Yup a Great Read indeed, thank you. There's nothing more permanent than a 'temporary' Gov program some wise-ass once said :)

2 Words (h/t Lyn Alden): Fiscal Dominance! Thanks for that link looking forward to it. Should less have been expected of Yellin? She's been acting like Fed Chair since named Treasury Sec (h/t Michael Every).