while WE slept: risk is off, bonds are BID and not a deep fake but rather due to DeepSEEK; China PMIs, DeepSeek, what COULD go wrong ... and finally, Barrons sounds the 'Bond Alarm'

Good morning … at least for the bond market … China / AI news along with Trump v Colombia weekend tariff volley seem to be taking the wind OUT of equity futures at the moment …

Bloomberg: What Is China’s DeepSeek and Why Is It Freaking Out the AI World?

CNBC: Stock futures fall ahead of key earnings; tech firms tumble as China’s DeepSeek rattles AI space: Live updates

CNBC: U.S. puts Colombia tariff, sanctions threat on hold after deportations deal

Equity futures moving lower helping supply a bid to the bond market AND this bid arrives, greeting an aggressive Treasury Auction Schedule this week, moved up with 2s and 5s today, 7s tomorrow to get out the FOMC way (Wed) and allow for a day before Friday’s month-end settlement …

It is with this in mind, and in addition to some actually very good charts from CitiFX HERE, where they are “Contrasting short & medium term indicators”, which ultimately suggest longer-term indicators are bullish and offset shorter-term impulse towards HIGHER yields … so, think dipORtunity…

I’ll lead with a shorter-term look at 2s (realizing the aforementioned more bullish longer-term setup) …

2yy DAILY: moving back down towards bottom of recent range…

…doing so as momentum has gone from overSOLD to now more overBOUGHT (without signs of exhaustion) and just ahead of this mornings liquidity event …

… times like these remind me of that saying once again whereby supply creates its very own demand. On THAT note, I’ll quit while I’m behind … here is a snapshot OF USTs as of 626a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: NQ down 5% & NVDA -11% pre-mkt as Chinese startup DeepSeek threatens US AI dominance … Fixed benchmarks benefit from the above and partially on better-than-expected German Ifo; Central Banks coming into focus … AI updates drive haven allure while Central Bank meetings move into focus; USTs post gains in excess of 20 ticks at a 109-07+ high into frontloaded supply on account of the FOMC this week.

PiQ Overnight News Roundup: Jan 27, 2025 (w/CME Fedwatch and their very own HEATMAP …)

Opening Bell Daily: China threatens Mag 7 … The S&P 500 hasn't boomed like this since Reagan … Animal spirits resemble 1985 but a new AI risk out of China looms.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ and a few things I’ve stumbled across since hitting SEND over the weekend …

We think the likelihood of a tariff hike in Q1 is small as President Trump ordered the USTR to assess China's performance under the Phase One deal (due 1 April) and expressed an interest in visiting China. We review the Trade war 1.0 timeline and recent official comments to gauge what's next.

The broad-based deterioration in the PMIs – manufacturing, services and construction – point to a weak start to 2025. The 5y low in the construction PMI was alarming amid a deeper contraction in housing and lack of new infrastructure. We expect GDP to slow to 2% q/q saar in Q1 from 7.9% in Q4.

A few (technically inclined) words (and a visual) from the very same bank which got lambasted by ‘47 at WEF last week …

24 January 2025 BAML: Global Rates Weekly Tariff-ic

…Technicals: US10Y yield uptrend while > lines at 4.50% 10Y yield uptrend underway to 4.74% (reached), Oct 2023 high at 5.02%, overshoot level 5.30%. Short term risk of a head and shoulders top if yield rolls over below 4.50%.

Missed waking up early to watch the AO finals but I’d be willing to guess the authors of these ‘Sunday’ notes caught ‘em … First up from France …

We have turned tactically neutral on the USD (from long) for the first time since the US presidential election as we see scope for a deeper positioning squeeze.

We expect the US economy’s strength and nascent inflation risks to keep the Fed on hold during 2025, despite likely increased pressure from President Trump to cut rates.

We see scope for further momentum in AI-linked stocks into a very busy US earnings week.

… ALSO written and send likely while it was SINNER for the DUB …

MS: Sunday Start | What's Next in Global Macro: Testing Our Assumptions

When we wrote our 2025 Outlooks in November, a key theme was uncertainty and in particular that our assumptions about the timing and implementation of policies from the new administration were critical, but just that … assumptions. A week after the inauguration, the information flow seems largely consistent with our public policy colleagues' call for “fast announcements, slow implementation,” but the uncertainty is far from resolved. Of the four key policy channels – tariffs, immigration, fiscal policy, and deregulation – the first two have received a bit more attention, and we think they are negative for growth this year. Fiscal policy remains uncertain, but recent comments by the Speaker of the House set the stage for a lot more information in the coming months. We maintain our view that deregulation will not move the needle on headline growth, but watching the news flow closely will be critical this year…

… I continue to believe this year will require monitoring the news flow and making revisions to forecasts. So far, our call on “fast announcements and slow implementation” is working, but details are yet to come. The key view, however, is that changes in immigration and tariff policy – the channels that are likely to come first and where the president has most direct control – are both more negative for growth than may be widely perceived. And they both boost inflation, though possibly temporarily. This means that when the inflation arrives, the Fed will be sidelined from cutting rates. Additional rate cuts may ultimately follow, but only if the economy slows so much that the central bank fears a recession.

Moving along and back to the inbox and away from China … almost, sorta, as this next note from Germany lays out what could possibly go wrong and derail the rally … timely in wake of DeepSeek …

DB: Mapping Markets: What factors could take this rally down?

Despite this morning’s selloff, it’s worth remembering that risk assets look in a relatively strong position right now, all things considered. Only last week, the S&P 500 and Europe’s STOXX 600 hit all-time highs, US credit spreads were around their tightest levels since the GFC, and Europe’s were at their tightest in 3 years as well. Moreover, the S&P 500 hasn’t seen a 10% correction since October 2023.

But as the last 24 hours have demonstrated, markets remain very sensitive to downside news. That’s particularly the case on AI-related topics given how it’s driven the rally since late-2022. Last summer also demonstrated that if economic data starts to soften, that could be a key catalyst for a correction. In particular, that combination of bad news on tech and broader economic data has the potential to cause big problems, as it’s worth remembering the bursting of the dot com bubble took place amidst a broader economic slowdown that culminated in a US recession in 2001.

Nevertheless, periodic selloffs are a normal feature of markets, and as we look forward, several factors that could have caused issues in the recent past are now looking more positive, if anything. For instance, it’s been 18 months since the Fed last hiked rates, so we’re moving past the period where monetary policy lags would normally have their peak effect. Otherwise, the rally has been impressively resilient against the higher long-term borrowing costs of recent weeks. And economic growth itself remains robust, with no sign yet of the negative data surprises that preceded the turmoil last summer.

…1. The lagged effects of past rate hikes are finally felt, and higher real rates cause issues we’re currently unaware of.

…One example of this can be see via the unrealised losses on balance sheets. By the end of Q3, these stood at their lowest since hikes began (admittedly before the Q4 bond selloff). So on paper, the risks of a repeat are diminishing, and the rate cuts since September will help further.

…2. Higher inflation/long-term borrowing costs take the steam out of risk assets.

…

…3. The more aggressive tariff scenarios play out, which dents growth and raises inflation…

…4. Economic data starts surprising on the downside like last summer…

…5. The hype around AI starts to fade.

As we go to press, US equity futures have seen a sharp move lower this morning, which follows Chinese firm DeepSeek’s announcement about their latest AI model. It requires less-advanced chips and is more cost effective compared to models from the US tech giants.

This is raising questions about the requirement for major capital expenditure on AI, as well as US tech dominance more broadly. From a market perspective, that’s led to questions about the valuations of these companies, particularly given the Magnificent 7 group are up +256% since the end of 2022.

Much of the recent equity rally has rested on these companies, as it’s been an unusually narrow rally by historical standards. Indeed, even though the S&P 500 was up +24% in 2023 and +23% in 2024, the equal-weighted version of the index was only up +12% and 11% respectively.

Equally, it’s worth noting that these selloffs do happen periodically. Back in July/August, the Magnificent 7 fell by over -18% in the space of a month, before rebounding again to all-time highs

…6. A negative geopolitical surprise or escalation…

…Conclusion …Nevertheless, even with this latest move lower, it's worth remembering that equities are coming off from all-time highs last week, and credit spreads are around their tightest levels in years. So in absolute terms, risk assets are still in a strong position right now. Moreover, as we move past the peak lags from monetary policy tightening, and actively feel the effects of easing, there are some positive tailwinds that lie ahead. Plus risk assets have already shown an impressive resilience against the bond selloff since late-September, so it doesn't appear that higher long-term borrowing costs have to cause a selloff per se.

This next note asking question more and more seem to wanna ask (but are afraid to say the words outloud …)

MS: The Weekly Worldview: Could a hike be the next move?

Tariff and immigration policies are likely to boost inflation, nonetheless, the bar is very high for the Fed to hike.

We think the Fed will continue to cut, albeit more slowly, for as long as disinflation continues, that is, until disinflation is disrupted by tariffs. We expect one or two more cuts in the first half of the year, and last week’s CPI print was on our side. Before that print, client conversations began broaching whether the next move could be a hike. I have frequently drawn parallels to the 1990s, where the Fed hiked aggressively, paused at the peak, had a very shallow 75bp cutting cycle, and then after a pause, did in fact hike. What would it take for that to happen this time? And why do we not see it as likely?

Employment and spending data for the past couple of months should have erased the growth scare from last summer. So, the focus has shifted fully to inflation falling toward the FOMC’s 2% target. Is the FOMC convinced that disinflation is still strong enough to confirm our base case for a rate cut in March? Probably not yet, and so we will need another confirmatory print to give us more conviction. But concerns that inflation is rising should surely have been allayed. Several FOMC participants have made it clear that they see more cuts forthcoming, the question for them is simply when.

The leap from here to a hike, is big. A subtle, but important point is that central bankers tend to think in levels more than changes when it comes to policy. The minutes of the December FOMC meeting stated that a “substantial majority” of the Committee believed that the level of the federal funds rate was still “meaningfully restrictive.” In a central banker’s mind, holding that level of policy rates should continue to exert pressure to bring inflation down, so stickier inflation could rule out rate cuts. But ruling out more cuts this year is very different from initiating hikes. If the Fed concluded they need to hike, it would likely start a series of hikes. That conclusion would require several months of accumulated data to change their belief on the trajectory of inflation and to change their belief on whether policy is neutral. That bar is very high.

What caused the speculation? Our rate strategy colleagues have consistently noted the strong incoming data, and the reaction to the election surely have contributed to this view. But based on conversations with clients, I see a few key areas where market participants have a different view than I about the effect these shifts will have on the economy and thereby the Fed…

Same shop on stonks (and an excerpt / visual on RATES) …

MS: US Equity Strategy: Weekly Warm-up: EPS Revisions, Pricing Power and Policy Inform Our Industry Preferences

We favor industries with strong EPS revisions, resilient pricing power and limited policy headwinds. Financials, Media & Entertainment and Software stand out on the EPS revisions front. We're also bullish on Consumer Services over Goods and feature a long Consumer Services screen in today's note.

… Over the past several weeks, we've stressed that the direction of interest rates has been (and continues to be) the key variable for index level performance. We've increasingly received questions around why that’s the case and what could change that relationship. In our view, the reasons behind the move in yields are even more important to explaining equity market performance than rate levels (though as we noted in early December, 4.50% was a key level where we thought rate sensitivity could return). In Exhibit 13, we narrate the recent rise in yields, offering context by also showing economic surprise, term premium and S&P 500 valuation. From September through November, the rise in the 10-year yield coincided with persistent upside in the Bloomberg US Economic Surprise Index as macro data beat lowered expectations following the weak July ISM and payroll reports. Index multiples rose and cyclicals (i.e., economically-sensitive areas of the market) outperformed, offering confirmation that there was momentum behind the recovery in macro data. Rate cuts were getting priced out of the bond market, and the term premium was up slightly, but the equity market was focused on prospects for a cyclical recovery—this was a "good is good" environment.

What changed in December? Upside in yields was driven by a higher term premium, and economic surprises fell. Multiples, in turn, compressed amid the rise in the term premium and less dovish Fed guidance. Rate sensitivity had returned as the 10-year yield pushed above the 4.50% level we had been focused on (also the point at which rates weighed on stocks in April of last year). Since mid-January, stocks have stayed inversely correlated to yields, but that rate sensitivity has shifted in the other direction post the lighter than expected December CPI report. As Exhibit 13 shows, yields have come in more recently as the term premium has fallen. Meanwhile, the economic surprise index has risen. The equity market has liked this combination as rates have stopped their ascent and growth data has been somewhat more resilient relative to expectations. Perhaps unsurprisingly, cyclicals have traded better, but it hasn't been a lower quality rally and small cap relative performance has yet to pick up. This is in line with our view and suggests the market is still respectful of the idea that we remain in a later cycle environment and that rates remain elevated.

Exhibit 13: The Reasons Behind the Move in Yields Are Even More Important to Explaining Equity Market Performance than Rate Levels

In the wake of WEF, we’ve got this coming from Switzerland now (and having absolutely nuthin’ to do with WEF, other than locale …)

China’s industrial profits grew in December, with profit margins seemingly more or less stable. This has a bearing beyond China’s borders because if China were “dumping” products by exporting below cost, profitability would suffer. Dumping might still happen in certain sectors, but the official data does not support it happening generally…

…There are sentiment polls from the US—the Dallas Fed manufacturing survey comments section, as always, gives insight into how biased supposedly objective survey responses can be. New home sales data is also due —housing is becoming a politically important area in many economies.

Markets may get some positive signals from US immigration and trade tax policies. So far, US President Trump’s migration policies do not appear to be deporting significantly increased numbers of people (although the publicity, which has increased, may have some economic consequences). The speed with which trade tariff threats against Colombian imports were withdrawn over the weekend also suggests that some tax threats are deal focused.

… And from the Global Wall Street inbox TO the WWW … a few curated links …

Barrons on rates and stonks …

Jan 24, 2025, 3:51 pm EST BARRONS: High Interest Rates Are Hammering Investors. What Lies Ahead Could Be Worse.

Rising rates would be bad news for bondholders and borrowers of all stripes, particularly the U.S. government. They cast a shadow over stocks, too.

… Then there’s the stock market. Equities will suffer if bond yields keep heading higher. Late last year and into early January, stocks stumbled as the yield on the benchmark 10-year Treasury note shot up from 3.6% to 4.8%. Then equities rallied as the Treasury yield fell back by a quarter of a point on better-than-expected inflation news. The S&P 500 index hit another record this past week…

… The current near-5% Treasury yields only look high compared with the 1.5% to 2.5% yields levels that prevailed in the decade following the financial crisis of 2008-09, notes Richard Sylla, who literally wrote the book on the subject, A History of Interest Rates.

One of the lessons of this history is that long-term interest-rate cycles typically run for 20 to 40 years, Sylla tells Barron’s. Yields bottomed around 0.3% during the Covid-19 market panic of March 2020, says Michael Hartnett, chief investment strategist at BofA Global Research. Although Hartnett predicts that bond and stock markets will rally later this year as the 10-year yield dips under 4%, he sees rising bond yields as the No. 1 long-term risk faced by investors….

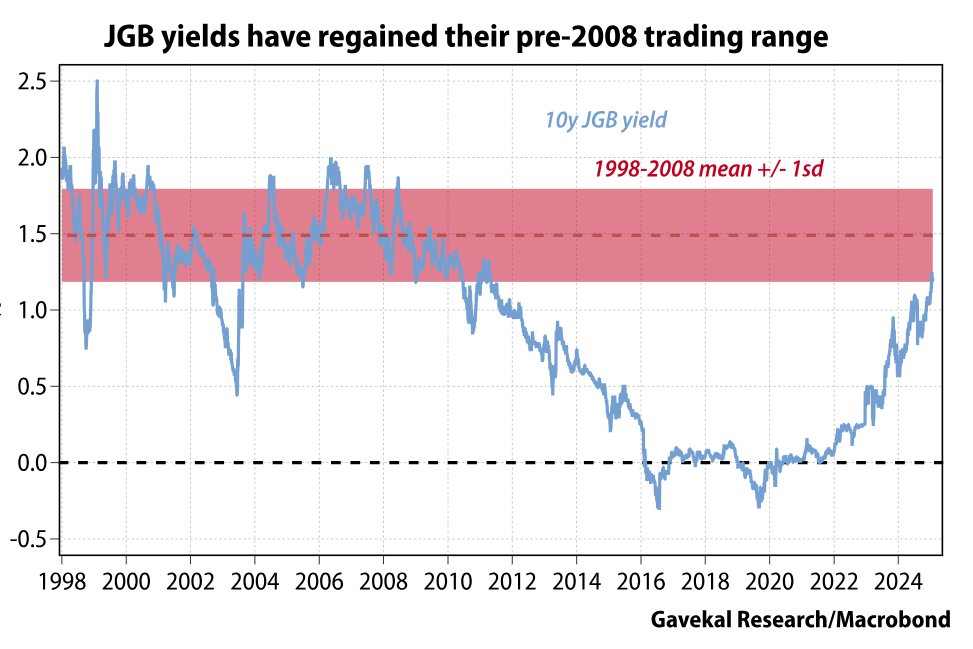

Bond Alarm(ed). Moving on to a room with a (BBG) view … a note titled and mostly ‘bout ESG but words (and visuals)on BoJ caught my attention …

BLOOMBERG: ESG's real sin isn't ideology, but that it's useless

…Where does the BOJ go from here? The market expects more hikes, although the magnitude and timing are unclear, and Bloomberg Economics’ Taro Kimura believes the BOJ’s guidance was aimed at heading off renewed yen strength:

In his commentary, we detected subtle signs that start to build a case for the next hike. We maintain our baseline scenario that the BOJ will deliver two more quarter-point increases this year — in April and July — taking its target rate up to 1.0%, the lower end of estimates of Japan’s neutral rate.

Such policy signaling hasn’t always been apparent, as shown by the July surprise that led to the carry trade unwind. Before this month’s meeting, Deputy Governor Ryozo Himino’s subtle hints of an imminent hike a week earlier guided market expectations. Whether such guidance will be a thing going forward is hard to tell, but investors now seem confident that rates will soon be their highest since 1994:

Policy signaling isn’t sacrosanct, especially with material external factors at play. Gavekal Research’s Udith Sikand argues against BOJ bullishness. He sees little evidence that wage gains translate into more consumption, while household spending in real terms declined almost every month last year. Trump tariffs might have an impact. Sikand adds that Japan’s $70 billion trade surplus with the US and the yen’s undervaluation makes it an easy trade war target. When the BOJ says it wants to“conduct monetary policy so that the zero lower bound would not be reached,” he argues that “the BOJ wants to raise rates now so that it has ammunition to expend during the next downturn.”

Sikand argues this could cause investors to revise upward their inflation expectations, short rates and term premiums — the three building blocks of long-term bond yields. This Gavekal chart shows the 10-year Japanese government bond yield has regained its pre-2008 trading range:

With the 40-year JGB yield recently hitting a record 2.8%, Sikand suggests the BOJ could fuel another deluge of repatriation flows, much likethose that triggered last summer’s bout of global volatility. People the world over have gotten used to cheap money and liquidity from Japan. Removing it now, when the US is trying to change many other long-lived assumptions, carries risks.

Disinflationary bias risk still at work? May just be …

DISCIPLINE FUNDS: Three Things I Think I Think – Weekend Reading

…1) There’s Still a Strong Disinflationary Bias at Work.

One of the most important pieces of news this week was the New Tenants Rent Index. The NTRI leads the actual CPI rental data and came in at a the lowest rate of change this cycle at -2.4%. This has been and continues to be the main reason why I am not really worried about inflation flaring up again.

Given how big the shelter component of CPI and PCE is you’d need a huge offset in some other component of the data. The most likely culprit would be energy and commodity prices, but we’re not seeing a huge move there. And given how energy friendly Trump was in his first term I find it hard to believe that we’re going to see a huge surge in oil and gasoline prices under his leadership.

The thing is, even when this data reverses you’re going to have a huge lag in the way it feeds thru to positive contributions in CPI because the current readings are so low. In the case of the GFC it took 3-4 years for shelter to start contributing to any upside in shelter because the data was so weak. And we’re right at the same levels we saw back then. So, I continue to be skeptical of the theory that inflation is a major upside risk from here.

AND Sam Ro with his latest which is ALWAYS worth a glance, especially for any like myself who is a chart fan …

TKer by Sam Ro: Reflecting on the stock market's headwind-defying run Plus a charted review of the macro crosscurrents

… After hitting a few bumps over the past month, the bull market resumed and stocks hit record highs last week.

This happened despite some notable headwinds intensifying in recent months.

Long-term interest rates, while off their highs, remain above levels we’ve experienced in recent years. This is a headwind for anyone needing to borrow money or refinance debt.

The yield on the 10-year Treasury Note remains elevated. (Source: FRED)

On the short end of the yield curve, expectations for rate cuts from the Federal Reserve have been coming down, a hawkish development that has market bears salivating.

The U.S. dollar, meanwhile, has appreciated significantly against many major foreign currencies. This is a headwind for multinational U.S.-based corporations doing a lot of business in non-U.S. markets.

The U.S. dollar has strengthened against major foreign currencies. (Source: FRED)

All of this has been occurring as valuation metrics like the price-to-earnings (P/E) ratio suggest the stock market is expensive relative to history.

Higher interest rates, fewer Fed rate cuts, a strengthening dollar, and elevated valuation ratios are all things that many market pundits will cite as reasons to be cautious on the stock market.

…The bottom line …For investors, the question is not whether some development will be a headwind for the stock market. Rather, investors should be asking if the companies underlying the market can overcome the headwind and deliver on earnings.